Uruguay

Executive Summary

Uruguay maintains a robust investment-grade credit profile, with ratings of BBB+ from S&P, Baa1 from Moody's, and BBB from Fitch, all carrying stable outlooks. This positioning reflects the sovereign's exceptional institutional strength and policy credibility, which have established Uruguay as the lowest-risk credit in Latin America with sovereign spreads of just 125 basis points, substantially below the regional average of 381 basis points. The country's credit standing is fundamentally anchored by its 83rd percentile ranking in World Bank governance metrics, its distinction as South America's only "full democracy", and a demonstrated track record of fiscal discipline operating within a constitutional fiscal rule framework. The March 2024 upgrade by Moody's from Baa2 to Baa1 underscored the strength of Uruguay's institutions in supporting structural reforms and maintaining compliance with fiscal and monetary policy frameworks.

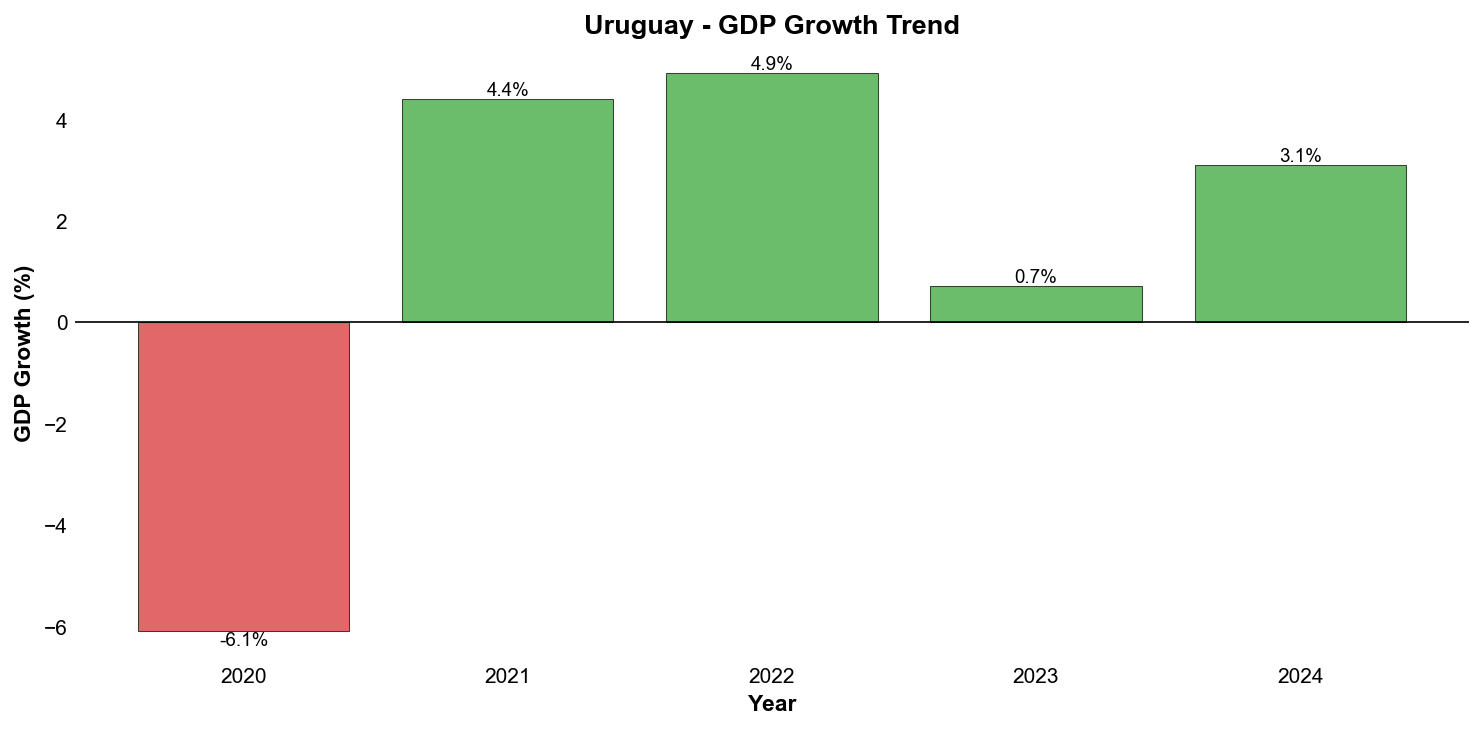

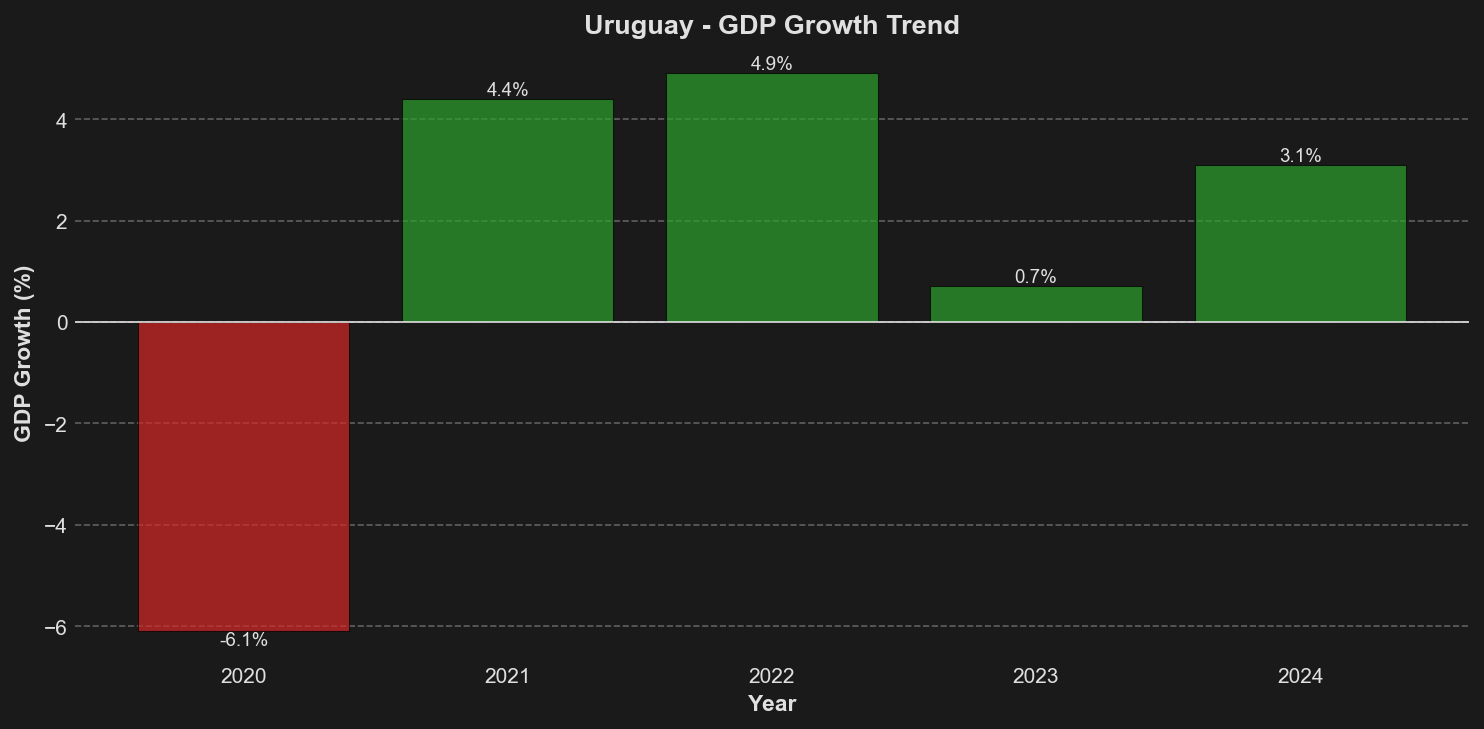

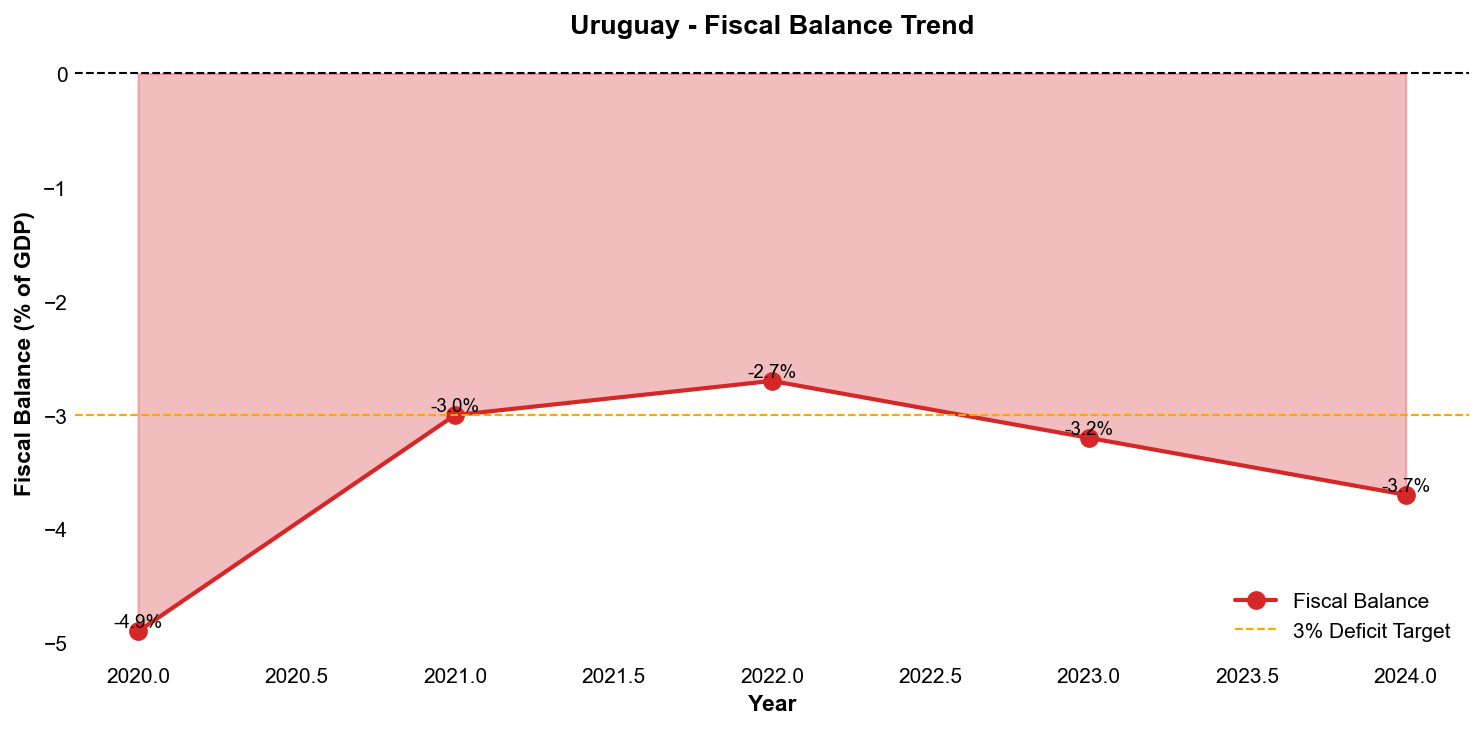

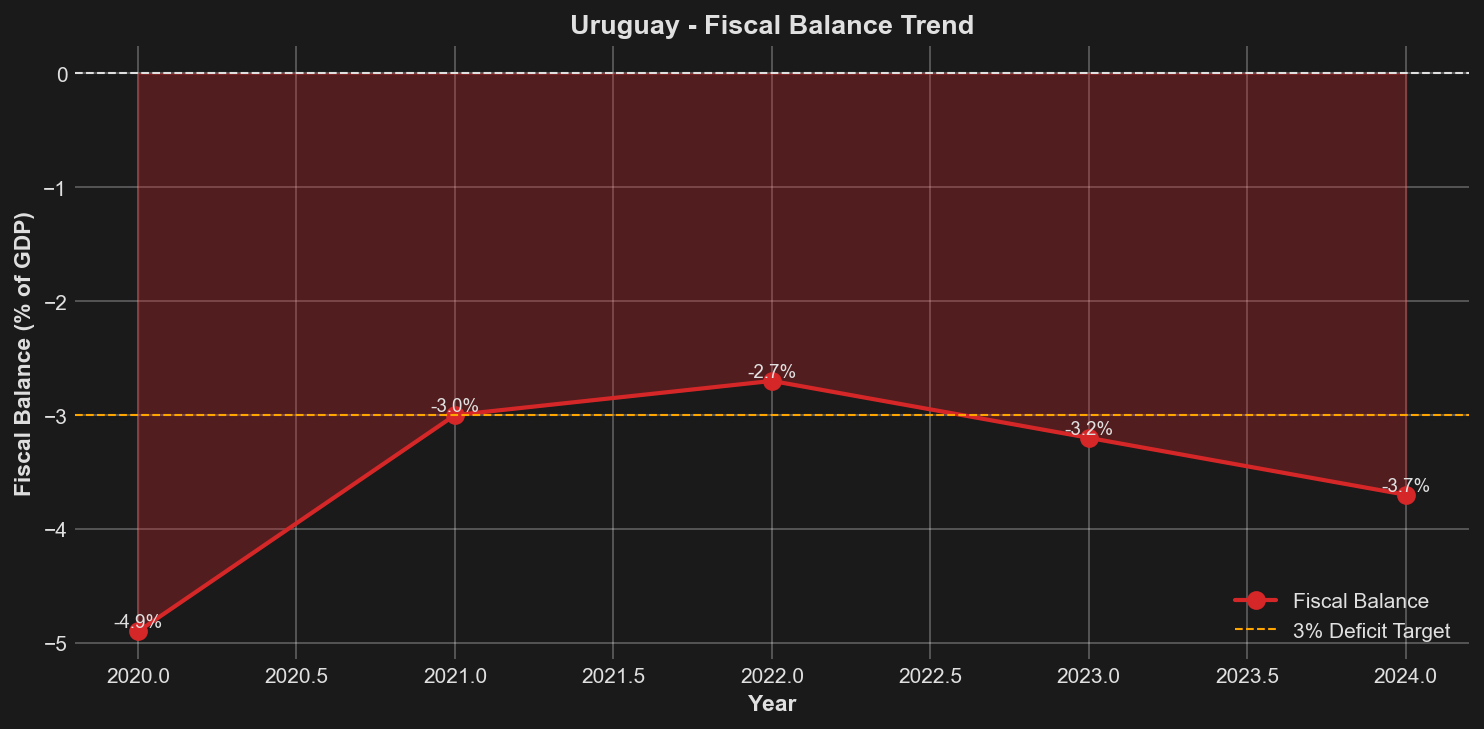

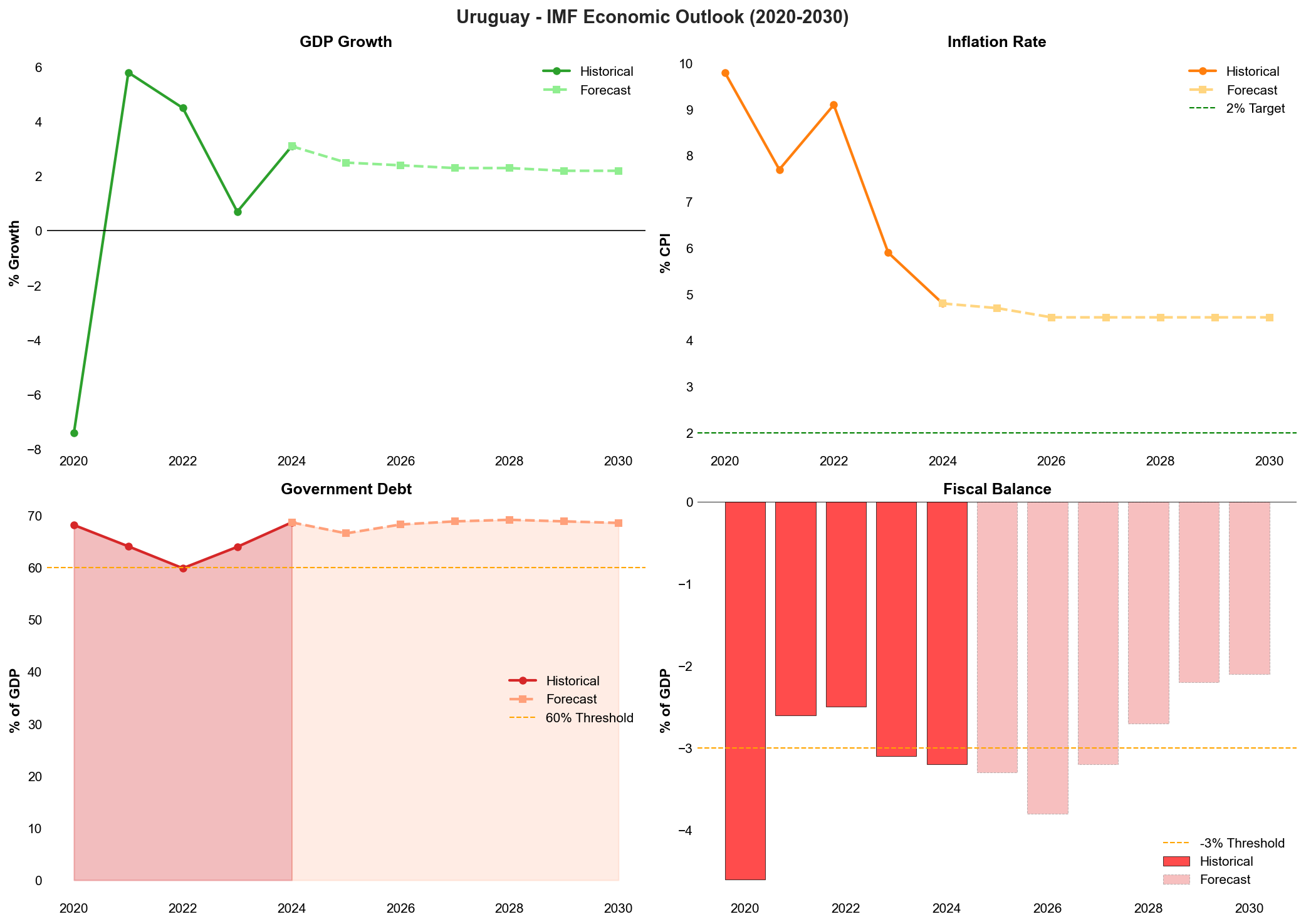

The Uruguayan economy has demonstrated considerable resilience through recent cyclical challenges, achieving 3.1% GDP growth in 2024 following recovery from the severe 2023 drought that contracted agricultural output by 25% and constrained overall growth to just 0.7%. Macroeconomic stabilisation has progressed effectively, with inflation successfully returning to the Central Bank's 3–6% target range at 4.8%, down from 9.1% in 2022, whilst the current account deficit has narrowed markedly to 0.8% of GDP. Foreign exchange reserves have strengthened to USD 17.4 billion, supporting external resilience. The fiscal deficit widened modestly to 3.7% of GDP in 2024, whilst the debt-to-GDP ratio increased to 68.7%, reflecting both cyclical pressures and the government's countercyclical policy response.

Nevertheless, Uruguay confronts structural headwinds that constrain medium-term growth potential and pose ongoing policy challenges. High financial dollarisation, with 70% of deposits denominated in foreign currency, limits monetary policy effectiveness and creates balance sheet vulnerabilities. Climate vulnerability represents an increasing risk, as evidenced by the 2023 drought's severe economic impact on the agriculture-dependent economy. Growth potential has moderated significantly, averaging just 1.6% since 2015 compared with 5.4% in the preceding decade, reflecting demographic constraints, limited scale, and productivity challenges. Unemployment has remained elevated at 8.4%, indicating persistent labour market slack despite the economic recovery.

Looking ahead, Uruguay's investment-grade status appears secure, supported by strong institutional foundations, manageable debt dynamics, and demonstrated capacity to navigate external shocks whilst maintaining market confidence. The new Frente Amplio administration under President Yamandú Orsi faces the challenge of balancing social spending priorities with fiscal discipline within the constitutional fiscal framework. Policy continuity, underpinned by Uruguay's robust democratic institutions and broad political consensus on macroeconomic stability, should support credit stability over the medium term. The sovereign's 98% renewable energy matrix, improving external position, and well-capitalised banking system provide additional buffers, though addressing structural growth constraints whilst managing climate risks will be essential to sustaining Uruguay's favourable credit trajectory.

Ratings Summary

Uruguay maintains investment-grade credit ratings across all three major rating agencies, reflecting the sovereign's exceptional institutional strength and demonstrated policy credibility. Standard & Poor's rates Uruguay at BBB+ with a stable outlook, affirmed most recently on 6 November 2024. Moody's Investors Service rates the sovereign at Baa1 with a stable outlook, following an upgrade from Baa2 on 15 March 2024 that cited "strong institutions that support implementation of structural reforms and continued compliance with fiscal and monetary policy frameworks." Fitch Ratings maintains a BBB rating with stable outlook, last affirmed on 4 June 2024. The Moody's upgrade represents the most significant recent rating action, recognising Uruguay's exceptional governance quality, with the country ranking 19th globally in corruption control. All three agencies emphasise Uruguay's institutional strengths as the primary rating driver, including its status as the only "full democracy" in South America, robust external balance sheet, and track record of fiscal rule compliance. The stable outlooks across all agencies indicate low likelihood of rating changes over the medium term, underpinned by confidence in Uruguay's policy framework, successful pension reform in 2023, and demonstrated ability to maintain economic stability through political transitions. Uruguay's 98 per cent renewable energy matrix and strong external position provide additional credit support.

| Rating Agency | Current Rating | Outlook | Last Action Date |

|---|---|---|---|

| S&P Global | BBB+ | Stable | 6 November 2024 |

| Moody's | Baa1 | Stable | 15 March 2024 |

| Fitch | BBB | Stable | 4 June 2024 |

Economic Indicators

| Indicator | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

| GDP Growth (%) | -6.1 | 4.4 | 4.9 | 0.7 | 3.1 |

| Inflation Rate (%) | 9.8 | 7.8 | 9.1 | 5.9 | 4.8 |

| Debt-to-GDP Ratio (%) | 68.1 | 64.8 | 59.3 | 64.5 | 68.7 |

| Fiscal Balance (% of GDP) | -4.9 | -3.0 | -2.7 | -3.2 | -3.7 |

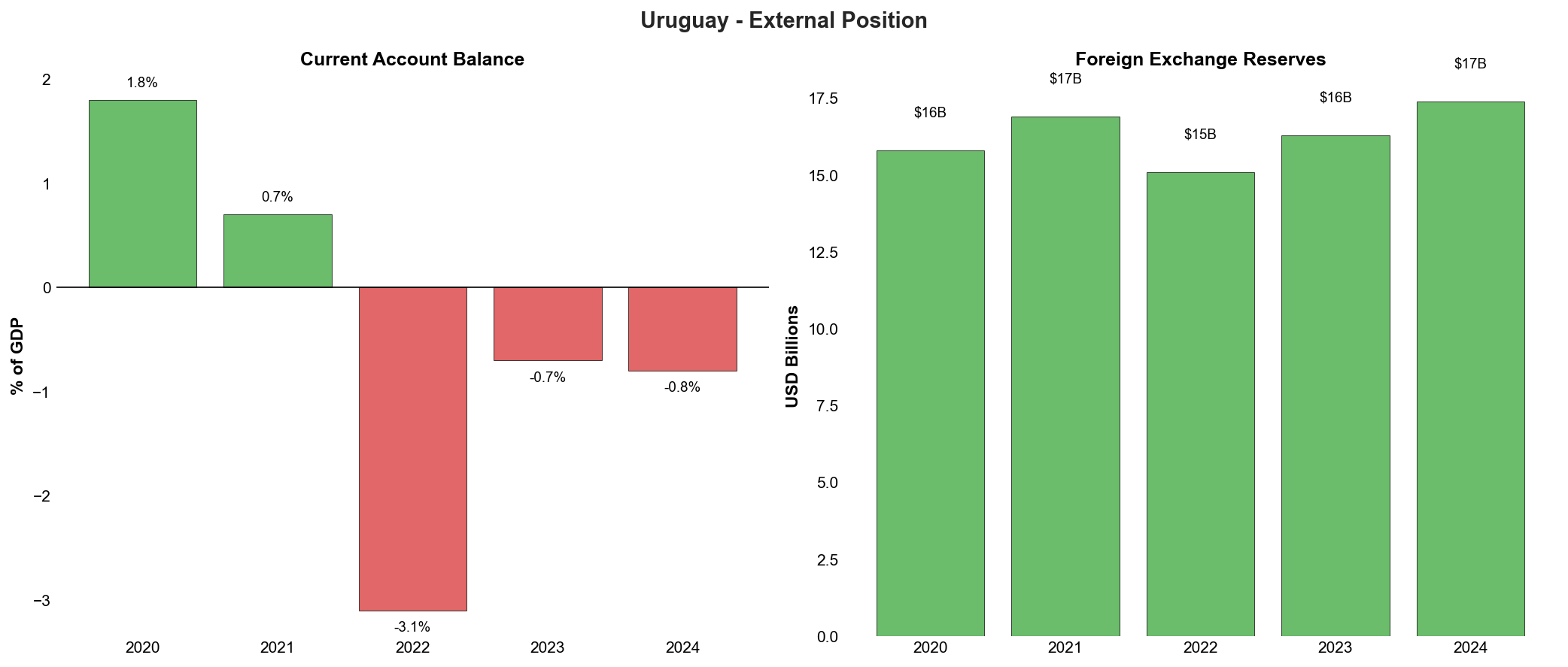

| Current Account Balance (% of GDP) | 1.8 | 0.7 | -3.1 | -0.7 | -0.8 |

| Foreign Exchange Reserves (USD billions) | 15.8 | 16.9 | 15.1 | 16.3 | 17.4 |

| Unemployment Rate (%) | 10.4 | 9.4 | 7.8 | 8.3 | 8.4 |

Economic Trends Analysis

Uruguay's economic performance demonstrates strong cyclical resilience with robust recovery patterns following external shocks. After the severe COVID-19 contraction of 6.1% in 2020, the economy achieved sustained growth of 4.4% and 4.9% in 2021-2022, reflecting effective policy responses and the economy's adaptive capacity. The historic drought of 2023 significantly impacted agricultural output, which contracted by 25%, constraining overall GDP growth to just 0.7%. However, the strong 3.1% rebound in 2024 underscores the economy's fundamental resilience and the effectiveness of countercyclical policy measures. IMF projections indicate a moderation to 2.2% growth by 2030, consistent with Uruguay's structural growth potential and demographic constraints.

Inflation control represents a major policy success for the Central Bank of Uruguay, with the inflation rate declining steadily from 9.8% in 2020 to 4.8% in 2024, firmly within the 3-6% target range. The monetary authority effectively managed the disinflation process through a well-calibrated tightening cycle, raising the policy rate from 4.5% to 11.25% before gradually reducing it to 8.75% by end-2024 as inflationary pressures subsided. This achievement is particularly notable given the external price shocks experienced during the period, including elevated global commodity prices and supply chain disruptions. The IMF forecasts inflation stabilising at 4.5% by 2030, suggesting sustained price stability anchored by credible monetary policy frameworks.

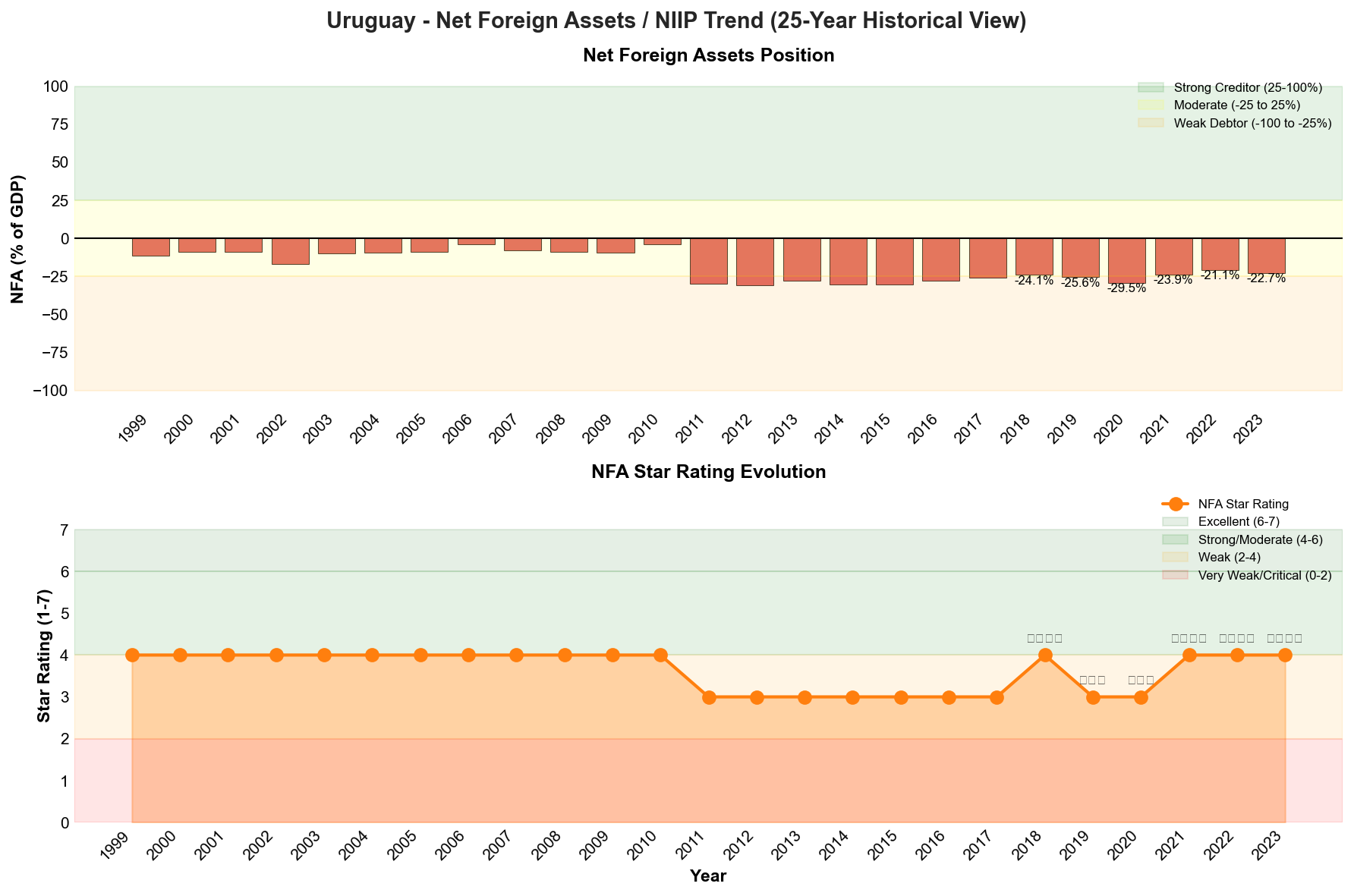

The current account position has strengthened significantly, narrowing from a deficit of 3.1% of GDP in 2022 to just 0.8% in 2024, representing a four-year low. This improvement reflects both cyclical factors, including the recovery of agricultural exports following the drought, and structural adjustments in the trade balance. Foreign exchange reserves increased to USD 17.4 billion in 2024, providing substantial buffers against external shocks and supporting the Central Bank's capacity to manage exchange rate volatility. Uruguay's net foreign asset position improved from -29.5% of GDP in 2020 to -22.7% in 2023, earning a four-star rating in the External Wealth of Nations assessment and reflecting a moderate debtor position. The IMF projects the current account deficit widening modestly to 1.9% of GDP by 2030, remaining within manageable parameters given Uruguay's strong external financing capacity and investment-grade credit status.

Fiscal dynamics present a more challenging picture, with the deficit widening from 2.7% of GDP in 2022 to 3.7% in 2024, approaching the constitutional fiscal rule ceiling. The debt-to-GDP ratio increased to 68.7% in 2024 from a post-pandemic low of 59.3% in 2022, reflecting both the denominator effect of slower growth in 2023 and increased borrowing requirements. The new Frente Amplio administration faces the delicate task of balancing social spending commitments with fiscal consolidation imperatives. However, the IMF's projection of the fiscal deficit narrowing to 2.1% of GDP by 2030, with debt stabilising at 68.6% of GDP, suggests confidence in Uruguay's institutional capacity to maintain fiscal discipline within its constitutional framework. The successful implementation of pension reform in 2023 provides additional support for long-term fiscal sustainability.

The labour market shows persistent challenges, with unemployment remaining elevated at 8.4% in 2024, marginally higher than the 8.3% recorded in 2023. This reflects structural rigidities in the labour market and the economy's moderate growth potential, which has averaged just 1.6% since 2015, down from 5.4% in the prior decade. The IMF projects unemployment declining modestly to 8.0% by 2030, contingent on continued structural reforms to enhance labour market flexibility and productivity growth. Overall, Uruguay's economic indicators reflect a sovereign with strong institutional foundations and policy credibility, capable of navigating external shocks whilst maintaining macroeconomic stability, though facing structural constraints on growth potential and fiscal space.

Net Foreign Assets & External Position

Uruguay's external position reflects a moderate net debtor status that has demonstrated meaningful improvement over the medium term, supported by prudent macroeconomic management and a diversified external funding base. The country's Net International Investment Position (NIIP) stood at -22.7% of GDP in 2023, representing a substantial strengthening from the -29.5% trough recorded during the 2020 pandemic shock. This improvement trajectory has elevated Uruguay's external position rating to four stars (⭐⭐⭐⭐) in the moderate category, indicating that external liabilities moderately exceed assets within a manageable range of -25% to +25% of GDP.

The evolution of Uruguay's NIIP demonstrates notable resilience and structural improvement. Following deterioration to -29.5% of GDP in 2020 amid pandemic-related pressures, the external position has strengthened consistently, improving by 6.8 percentage points through 2023. This recovery reflects Uruguay's robust export performance, particularly in agricultural commodities and services, alongside disciplined external borrowing practices. The progression from a weak three-star rating in 2019-2020 to a moderate four-star rating from 2021 onwards underscores the effectiveness of Uruguay's external adjustment mechanisms and policy frameworks.

Reserve Adequacy and External Buffers

Uruguay maintains substantial foreign exchange reserves that provide critical buffers against external shocks and support the credibility of monetary policy in a highly dollarised economy. Reserves increased from USD 15.8 billion in 2020 to USD 17.4 billion in 2024, representing approximately 15% of GDP and covering roughly 10 months of goods and services imports. This reserve accumulation occurred despite periodic interventions by the Central Bank of Uruguay to smooth exchange rate volatility, demonstrating the strength of underlying balance of payments dynamics.

The reserve position is particularly important given Uruguay's 70% deposit dollarisation rate, which creates potential vulnerabilities to sudden shifts in confidence or external liquidity conditions. However, the banking system's favourable solvency and liquidity metrics, combined with the Central Bank's demonstrated willingness to deploy reserves judiciously, mitigate these risks. The authorities have maintained reserve adequacy well above IMF metrics for emerging markets, providing substantial capacity to address potential external pressures.

Current Account Dynamics and Sustainability

Uruguay's current account position has strengthened markedly, narrowing from a deficit of -3.1% of GDP in 2022 to just -0.8% in 2024, representing a four-year low and reflecting improved terms of trade alongside robust services exports, particularly tourism and business services. This adjustment occurred despite the severe 2023 drought that contracted agricultural output by 25%, demonstrating the economy's diversification benefits and external resilience. IMF projections indicate the current account deficit widening modestly to -1.9% of GDP by 2030, remaining well within sustainable parameters given Uruguay's access to diverse financing sources.

The composition of external financing enhances sustainability, with foreign direct investment consistently covering a substantial portion of current account financing needs. Uruguay's investment-grade credit ratings and status as Latin America's lowest-risk sovereign, with spreads of just 125 basis points compared to the regional average of 381 basis points, ensure continued market access on favourable terms. The sovereign's track record of meeting external obligations without interruption, combined with its diversified creditor base spanning multilateral institutions, bilateral partners, and private markets, provides additional external stability.

Structural Vulnerabilities and Risk Factors

Despite the improved external position, Uruguay faces structural vulnerabilities that warrant monitoring. The high dollarisation rate of 70% creates currency mismatches and limits monetary policy effectiveness, though this is partially offset by the Central Bank's credibility and the economy's demonstrated capacity to generate dollar revenues through exports. Climate vulnerability represents an emerging external risk, as evidenced by the 2023 drought's impact on agricultural exports, which constitute a significant portion of goods exports. However, Uruguay's 98% renewable energy matrix and ongoing economic diversification efforts mitigate concentration risks.

The moderate net debtor position, whilst improved, leaves Uruguay exposed to shifts in global financial conditions and investor sentiment towards emerging markets. Rising global interest rates or risk aversion could increase external financing costs and pressure the exchange rate. Nevertheless, Uruguay's exceptional institutional quality, ranking in the 83rd percentile for World Bank governance metrics and maintaining status as South America's only "full democracy," provides substantial resilience against such shocks. The demonstrated ability to maintain market confidence through political transitions and external stress episodes supports the assessment that Uruguay's external position remains sustainable over the medium term, consistent with its investment-grade credit profile.

Credit Strengths & Vulnerabilities

Strengths

Uruguay's credit profile is fundamentally anchored by its exceptional institutional quality, which distinguishes it amongst Latin American sovereigns. The country ranks in the 83rd percentile globally in the World Bank's governance indicators and holds the distinction of being South America's only "full democracy" according to The Economist Intelligence Unit. This institutional strength manifests in consistent policy implementation across political cycles, with the country demonstrating a robust track record of fiscal rule compliance and sustained commitment to macroeconomic stability frameworks. The sovereign's 19th global ranking in corruption control reflects deep-rooted transparency and accountability mechanisms that underpin investor confidence and facilitate access to international capital markets at favourable terms.

The sovereign's market positioning represents a significant credit strength, with Uruguay maintaining the lowest risk spreads in Latin America at 125 basis points—substantially below the regional average of 381 basis points. This preferential market access reflects investor recognition of Uruguay's policy credibility and institutional resilience. The country's investment-grade ratings across all three major agencies (S&P: BBB+, Moody's: Baa1, Fitch: BBB) with stable outlooks provide a solid foundation for continued favourable financing conditions. Moody's March 2024 upgrade from Baa2 to Baa1 particularly underscores the strengthening trajectory of Uruguay's credit fundamentals, with the agency citing "strong institutions that support implementation of structural reforms and continued compliance with fiscal and monetary policy frameworks."

Uruguay's external position constitutes a notable credit strength, characterised by a robust balance sheet and demonstrated resilience to external shocks. Foreign exchange reserves increased to USD 17.4 billion in 2024, providing substantial coverage against external financing needs. The current account deficit narrowed markedly to just 0.8% of GDP in 2024 from 3.1% in 2022, representing a four-year low and reflecting improved terms of trade and export competitiveness. The sovereign's 98% renewable energy matrix not only enhances energy security but also positions Uruguay favourably in the global transition towards sustainable development, reducing vulnerability to fossil fuel price volatility whilst attracting environmentally conscious investment flows.

Monetary policy credibility represents an additional pillar of credit strength, with the Central Bank successfully navigating the disinflation process to bring inflation to 4.8% in 2024, comfortably within the 3-6% target range. This achievement followed a well-calibrated tightening cycle that saw policy rates increase from 4.5% to 11.25% before gradual normalisation to 8.75% by end-2024. The monetary authority's operational independence and transparent communication framework have established strong anchoring of inflation expectations, contributing to macroeconomic stability and supporting the real economy's adjustment capacity during external shocks such as the 2023 drought.

Vulnerabilities

Uruguay's high degree of financial dollarisation constitutes a structural vulnerability that constrains monetary policy effectiveness and amplifies financial stability risks. With 70% of bank deposits denominated in US dollars, the sovereign faces persistent currency mismatches that limit the Central Bank's ability to act as lender of last resort in foreign currency and increase the economy's sensitivity to external financial conditions. This dollarisation reflects historical inflation volatility and incomplete credibility in the domestic currency, though recent inflation control success has begun to gradually shift preferences. The elevated dollarisation also complicates debt management, as exchange rate depreciation directly increases the local currency burden of foreign-denominated obligations.

The sovereign's debt dynamics present moderate vulnerabilities, with the debt-to-GDP ratio rising to 68.7% in 2024 from 59.3% in 2022. This upward trajectory reflects both cyclical factors—including the fiscal impact of the 2023 drought and associated support measures—and structural pressures from social spending commitments. The fiscal deficit widened to 3.7% of GDP in 2024, approaching the constitutional fiscal rule ceiling and limiting the government's capacity to absorb future shocks without breaching fiscal constraints. The new Frente Amplio administration under President Yamandú Orsi faces the challenge of balancing campaign commitments for enhanced social spending with the imperative of maintaining fiscal discipline and market confidence.

Climate vulnerability represents an increasingly material credit constraint, as demonstrated by the severe 2023 drought that contracted agricultural output by 25% and reduced overall GDP growth to just 0.7%. Agriculture and agro-industry constitute significant components of Uruguay's export base and fiscal revenues, creating direct transmission channels through which climate shocks impact sovereign creditworthiness. The frequency and severity of extreme weather events appear to be increasing, with implications for long-term growth potential, infrastructure investment requirements, and fiscal planning. Whilst Uruguay's renewable energy matrix provides some resilience, water-dependent hydroelectric generation also faces vulnerability to drought conditions.

Uruguay's modest growth potential constitutes a structural vulnerability that constrains fiscal space and debt sustainability over the medium term. Economic expansion has averaged just 1.6% since 2015, markedly below the 5.4% average of the prior decade, reflecting both external headwinds and domestic structural constraints. The economy's small scale and limited diversification restrict opportunities for productivity gains, whilst demographic trends point towards population ageing that will intensify pension and healthcare expenditure pressures. Unemployment remained elevated at 8.4% in 2024, indicating persistent labour market slack despite cyclical recovery. This subdued growth trajectory limits the sovereign's capacity to reduce debt ratios through expansion and necessitates continued fiscal discipline to maintain debt sustainability.

Opportunities

The new administration's commitment to maintaining institutional continuity whilst pursuing targeted reforms presents opportunities for credit enhancement. President Yamandú Orsi's Frente Amplio government has signalled adherence to the constitutional fiscal rule framework and continuation of prudent macroeconomic policies, which should sustain investor confidence and market access on favourable terms. The government's focus on education reform and human capital development could enhance productivity and growth potential over the medium term, addressing one of Uruguay's key structural constraints. Successful implementation of social policies within fiscal constraints would demonstrate the resilience of Uruguay's institutional framework across the political spectrum.

Uruguay's strategic positioning in regional and global trade architecture offers opportunities for economic diversification and growth acceleration. The country's Mercosur membership combined with its pragmatic approach to trade negotiations provides potential for expanded market access, particularly as global supply chains undergo reconfiguration. Uruguay's reputation for regulatory quality and political stability positions it favourably to attract nearshoring investment from companies seeking reliable production platforms in Latin America. The sovereign's strong governance metrics and transparent business environment create competitive advantages in attracting foreign direct investment in higher value-added sectors beyond traditional agriculture and agro-industry.

The global transition towards sustainable development and renewable energy presents significant opportunities aligned with Uruguay's existing strengths. The country's 98% renewable energy matrix and demonstrated commitment to environmental sustainability position it favourably for green finance initiatives and climate-related investment flows. Uruguay could leverage its renewable energy capacity to develop green hydrogen production and other emerging clean technologies, potentially creating new export sectors and employment opportunities. Enhanced access to concessional climate finance and green bonds could support infrastructure investment whilst improving debt profile metrics through favourable financing terms.

Financial sector deepening and de-dollarisation progress represent opportunities to enhance monetary policy effectiveness and financial stability. Continued success in maintaining low and stable inflation could gradually shift deposit preferences towards local currency, reducing currency mismatches and expanding the Central Bank's policy toolkit. Development of local currency capital markets would diversify funding sources for both sovereign and private sector borrowers, reducing dependence on external financing and vulnerability to global financial conditions. Strengthening of pension fund assets and institutional investor base could support deeper domestic debt markets and more stable financing structures.

Threats

External financial conditions tightening represents a significant threat to Uruguay's credit profile, particularly given the sovereign's reliance on international capital markets and sensitivity to global risk sentiment. Rising US interest rates or deteriorating emerging market sentiment could increase borrowing costs and complicate debt refinancing, especially given Uruguay's elevated debt-to-GDP ratio of 68.7%. The sovereign's investment-grade status provides some insulation from capital flow volatility, but sustained deterioration in global financial conditions could pressure spreads and fiscal sustainability. Uruguay's small economy size and limited domestic investor base amplify vulnerability to shifts in external financing availability.

Regional economic and political instability poses contagion risks despite Uruguay's strong institutional differentiation. Significant economic deterioration or political crises in neighbouring Argentina or Brazil—Uruguay's primary trading partners—could impact export demand, tourism revenues, and regional financial stability. Historical episodes have demonstrated transmission channels through trade linkages, financial sector exposures, and confidence effects. Whilst Uruguay's governance quality typically allows it to decouple from regional stress, severe or prolonged regional crises could overwhelm these buffers and impact growth prospects and fiscal revenues.

Intensifying climate change impacts threaten to increase the frequency and severity of extreme weather events, with material implications for economic stability and fiscal sustainability. The 2023 drought's severe impact—contracting agricultural output by 25% and reducing GDP growth to 0.7%—illustrates the economy's vulnerability to climate shocks. Projections suggest increasing water stress and weather volatility in the region, which could necessitate substantial adaptation investments and create recurring fiscal pressures. Persistent climate impacts could undermine agricultural productivity and export competitiveness whilst increasing infrastructure maintenance costs and disaster response expenditures.

Political pressures for increased social spending present risks to fiscal discipline and debt sustainability, particularly as the new administration seeks to implement campaign commitments. The constitutional fiscal rule provides an important anchor, but political pressures to expand social programmes or public sector employment could test the government's commitment to fiscal constraints. Failure to maintain fiscal discipline would likely trigger negative rating actions and increase borrowing costs, creating adverse debt dynamics. The challenge of balancing social demands with fiscal sustainability will intensify if growth remains subdued or external shocks require countercyclical policy responses that approach fiscal rule limits.

Economic Analysis

Growth Dynamics and Structural Performance

Uruguay's economic trajectory reflects a sovereign navigating the transition from cyclical recovery to structural deceleration, with growth dynamics increasingly constrained by demographic headwinds and limited productivity gains. The economy's 3.1% expansion in 2024 represents a robust cyclical rebound from the drought-induced slowdown, yet masks underlying structural challenges that have reduced the country's medium-term growth potential to approximately 1.6% annually since 2015, a marked deterioration from the 5.4% average recorded in the preceding decade.

The 2023-2024 growth cycle illustrates Uruguay's vulnerability to climate-related shocks whilst simultaneously demonstrating the economy's resilience mechanisms. The historic drought of 2023 contracted agricultural output by 25%, directly impacting a sector that accounts for approximately 6% of GDP but generates nearly 70% of merchandise exports. This external shock reduced headline growth to just 0.7%, yet the economy avoided technical recession through offsetting strength in services, particularly tourism and financial intermediation. The subsequent recovery to 3.1% growth in 2024 was driven by agricultural normalisation, sustained domestic consumption supported by real wage growth, and continued expansion in the renewable energy sector.

However, the structural growth deceleration reflects deeper challenges. Uruguay's small domestic market of 3.4 million inhabitants limits economies of scale, whilst an ageing demographic profile constrains labour force expansion. The working-age population growth rate has declined to approximately 0.3% annually, reducing potential output growth absent significant productivity improvements. Investment rates, whilst stable at approximately 17% of GDP, remain insufficient to drive transformational growth, particularly given the economy's already high capital stock relative to regional peers.

The sectoral composition of growth reveals both strengths and vulnerabilities. Services account for approximately 65% of GDP, with financial services, tourism, and information technology demonstrating particular dynamism. Uruguay has successfully positioned itself as a regional technology hub, with software exports growing at double-digit rates and the sector now employing over 15,000 professionals. The agricultural sector, whilst volatile, benefits from exceptional land quality and sustainable production practices that command premium prices in international markets. Manufacturing, however, has stagnated at approximately 12% of GDP, constrained by high labour costs relative to productivity and limited integration into global value chains beyond agricultural processing.

Inflation Dynamics and Price Stability

Uruguay's inflation performance represents a significant monetary policy achievement, with the Central Bank successfully navigating the global inflation surge whilst maintaining credibility and anchoring expectations. The decline in headline inflation from 9.1% in 2022 to 4.8% in 2024 places Uruguay amongst the most successful inflation targeters in emerging markets, with price pressures now firmly within the 3-6% target range after several years of elevated readings.

The inflation trajectory reflects both external and domestic factors. The 2022 peak of 9.1% was driven primarily by imported inflation, particularly energy and food commodities, compounded by peso depreciation pressures as the US Federal Reserve initiated its tightening cycle. Domestic demand pressures were relatively contained, with core inflation consistently running below headline measures. The Central Bank's decisive response, raising the policy rate from 4.5% to a peak of 11.25%, successfully prevented second-round effects and wage-price spiral dynamics despite Uruguay's relatively rigid labour market characterised by strong union presence and backward-looking wage indexation mechanisms.

The disinflation process accelerated through 2023-2024 as global commodity prices normalised and monetary policy transmission mechanisms gained traction. The Central Bank's credibility, built over two decades of inflation targeting, proved instrumental in anchoring expectations even as inflation temporarily exceeded the target range. Survey-based inflation expectations remained well-anchored around 6%, preventing the de-anchoring observed in several regional peers. The successful return to target allowed the monetary authority to commence a gradual easing cycle, reducing rates to 8.75% by end-2024 whilst maintaining a cautiously restrictive stance.

Structural factors support Uruguay's inflation outlook. High dollarisation, whilst presenting monetary policy challenges, provides a natural hedge against sustained peso depreciation and imported inflation. Approximately 70% of bank deposits are denominated in US dollars, reflecting deep-seated preferences shaped by historical inflation episodes. This dollarisation constrains the Central Bank's ability to act as lender of last resort but simultaneously imposes market discipline on fiscal and monetary authorities. The 98% renewable energy matrix insulates Uruguay from fossil fuel price volatility, a significant advantage relative to regional peers dependent on hydrocarbon imports.

Monetary Policy Framework and Financial Conditions

Uruguay's monetary policy operates within a flexible inflation targeting framework adopted in 2007, with the Central Bank enjoying operational independence enshrined in its organic charter. The framework targets headline CPI inflation within a 3-6% range, with tolerance bands allowing for temporary deviations in response to supply shocks. The policy rate serves as the primary instrument, complemented by reserve requirements and foreign exchange intervention to manage excessive volatility.

The monetary transmission mechanism functions reasonably effectively despite structural constraints imposed by high dollarisation. Interest rate pass-through to peso-denominated lending rates occurs with approximately six-month lags, whilst dollar-denominated rates remain largely determined by US monetary policy and country risk premia. The Central Bank has developed sophisticated intervention protocols to manage exchange rate volatility without compromising the inflation target, accumulating reserves during capital inflow episodes and allowing orderly adjustment during stress periods.

Financial conditions through 2024 remained moderately restrictive, consistent with the Central Bank's objective of consolidating disinflation gains. Real policy rates turned positive in early 2024 as inflation declined faster than nominal rate cuts, providing continued restraint on domestic demand. Credit growth moderated to approximately 5% in real terms, concentrated in mortgage lending and consumer finance, whilst corporate credit remained subdued reflecting cautious business sentiment and elevated uncertainty surrounding the political transition.

The banking system's health supports monetary policy effectiveness. Capital adequacy ratios exceed 14%, well above regulatory minimums, whilst non-performing loans remain contained at approximately 2% of total loans. Liquidity coverage ratios exceed 200%, reflecting conservative funding structures and substantial holdings of liquid assets. The system's high dollarisation necessitates careful liquidity management, with the Central Bank maintaining swap facilities and reserve buffers to address potential dollar liquidity stress. Foreign exchange reserves of USD 17.4 billion represent approximately 23% of GDP and provide comfortable coverage of short-term external obligations, supporting confidence in the monetary framework.

Political & Institutional Assessment

Uruguay's political and institutional framework represents the strongest in Latin America, underpinning the sovereign's investment-grade credit ratings and distinguishing it from regional peers. The country maintains its status as the only "full democracy" in South America according to The Economist Intelligence Unit's Democracy Index, whilst achieving an 83rd percentile ranking in the World Bank's Worldwide Governance Indicators. This exceptional institutional quality translates directly into policy credibility and market confidence, evidenced by the sovereign's 125 basis point risk spread—the lowest in the region and substantially below the Latin American average of 381 basis points.

The institutional architecture demonstrates remarkable resilience across political cycles. Uruguay ranks 19th globally in Transparency International's Corruption Perceptions Index, reflecting deeply embedded governance standards that transcend individual administrations. The country's constitutional fiscal rule framework, established in 2005 and strengthened through subsequent reforms, has proven effective in constraining fiscal discretion whilst maintaining sufficient flexibility for counter-cyclical policy responses. Compliance with this framework has been consistent across administrations of differing political orientations, demonstrating the rule's legitimacy and institutional embedding.

The March 2024 presidential transition to the centre-left Frente Amplio coalition under President Yamandú Orsi proceeded smoothly, maintaining policy continuity despite the change in governing coalition. The new administration has signalled commitment to fiscal discipline within the constitutional framework whilst pursuing moderate social spending increases. This balance reflects Uruguay's mature political consensus around macroeconomic stability, which has been maintained since the 2002 financial crisis catalysed fundamental reforms to fiscal and monetary policy frameworks.

Moody's March 2024 upgrade to Baa1 explicitly recognised these institutional strengths, citing "strong institutions that support implementation of structural reforms and continued compliance with fiscal and monetary policy frameworks." The rating agency emphasised that Uruguay's governance quality provides confidence in the sovereign's capacity to navigate future challenges whilst maintaining policy credibility. Similarly, S&P's November 2024 affirmation highlighted the country's "strong democracy that sustains investor confidence," noting that institutional quality compensates for structural economic constraints including modest growth potential and high dollarization.

The Central Bank of Uruguay operates with de facto independence, maintaining credibility through consistent adherence to its inflation targeting framework. The monetary authority successfully navigated the 2022-2023 inflation surge, implementing a disciplined tightening cycle that restored inflation to the 3-6% target range by 2024. This policy effectiveness reflects both institutional capacity and political support for orthodox monetary management, which has been sustained across multiple administrations since inflation targeting was adopted in 2007.

Legislative dynamics support policy stability despite Uruguay's proportional representation system. The bicameral General Assembly operates with established procedures for coalition building, enabling effective governance even when no single party commands a majority. The 2023 pension reform—a politically sensitive structural adjustment—demonstrated the system's capacity to deliver difficult reforms through negotiated consensus. This reform improved the pension system's long-term sustainability whilst maintaining social cohesion, exemplifying Uruguay's institutional maturity.

Looking forward, the key institutional challenge centres on balancing the new administration's social spending priorities with fiscal rule compliance. The Frente Amplio government has proposed targeted increases in education and healthcare expenditure whilst committing to maintain the fiscal deficit within constitutional limits. The credibility of Uruguay's institutional framework will be tested by the administration's ability to deliver on social commitments without compromising fiscal sustainability. However, the track record of institutional resilience across political cycles provides confidence that policy discipline will be maintained, supporting the stable outlook across all three major rating agencies.

Banking Sector & Financial Stability

Uruguay's banking sector demonstrates exceptional resilience and represents a cornerstone of the sovereign's credit profile, characterised by robust capitalisation, strong liquidity buffers, and prudent regulatory oversight. The financial system has proven its capacity to withstand significant external shocks whilst maintaining stability, supported by a comprehensive regulatory framework that aligns with international best practices and a supervisory authority with demonstrated independence and technical capability.

Structural Characteristics and Systemic Strength

The Uruguayan banking system exhibits structural features that enhance financial stability whilst presenting unique challenges related to the economy's high dollarisation. With 70% of deposits denominated in foreign currency, primarily US dollars, the financial system operates within a dual-currency framework that requires sophisticated risk management and regulatory oversight. This dollarisation reflects historical patterns of inflation volatility and currency instability, though it has declined from peak levels exceeding 90% in the early 2000s. The Central Bank of Uruguay has implemented prudential regulations specifically designed to address foreign exchange risks, including differentiated reserve requirements and liquidity standards for dollar-denominated operations.

The banking sector's asset quality metrics reflect conservative lending practices and effective credit risk management. Non-performing loan ratios have remained contained despite economic volatility, supported by rigorous underwriting standards and proactive provisioning policies. The system's loan portfolio demonstrates diversification across sectors, with significant exposure to agriculture, commerce, and services, mirroring the economy's sectoral composition. Banks maintain substantial loan loss reserves that provide buffers against potential credit deterioration during economic downturns.

Capitalisation and Solvency Metrics

Capital adequacy represents a fundamental strength of Uruguay's banking system, with institutions maintaining solvency ratios well above regulatory minimums and international benchmarks. The sector's robust capitalisation provides substantial loss-absorption capacity and supports continued lending activity during periods of economic stress. Regulatory capital requirements align with Basel III standards, and the Central Bank has implemented countercyclical capital buffers that can be adjusted based on systemic risk assessments.

The banking system's profitability has remained solid, generating returns that support organic capital accumulation and dividend distributions whilst maintaining prudent retention policies. Net interest margins reflect the competitive dynamics of the market and the impact of monetary policy transmission, with banks demonstrating adaptability to changing interest rate environments. Operating efficiency metrics indicate well-managed cost structures, though the relatively small scale of the domestic market constrains economies of scale compared to larger regional financial systems.

Liquidity Management and Funding Stability

Liquidity conditions within the banking sector remain favourable, supported by substantial deposit bases and access to diverse funding sources. The system's liquidity coverage ratios exceed regulatory requirements, providing buffers to manage potential deposit outflows or market disruptions. Banks maintain significant holdings of liquid assets, including Central Bank reserves, government securities, and readily marketable instruments that can be deployed to meet funding needs.

The deposit base exhibits reasonable stability despite the high proportion of foreign currency deposits, reflecting depositor confidence in the banking system and the regulatory framework. Retail deposits constitute a significant portion of funding, providing a more stable foundation than wholesale funding sources. The Central Bank's role as lender of last resort, combined with the deposit insurance scheme, reinforces systemic stability and mitigates risks of deposit runs during periods of uncertainty.

Regulatory Framework and Supervisory Effectiveness

The Central Bank of Uruguay's supervisory capabilities represent a critical strength, with the institution demonstrating technical expertise, operational independence, and willingness to take corrective action when necessary. The regulatory framework encompasses comprehensive prudential standards covering capital adequacy, liquidity management, credit risk, market risk, and operational risk. Stress testing exercises conducted by both individual institutions and the supervisory authority provide forward-looking assessments of resilience under adverse scenarios.

The financial system's integration with international standards enhances credibility and facilitates cross-border operations. Uruguay has implemented anti-money laundering and counter-terrorism financing regulations that align with Financial Action Task Force recommendations, though the country has faced scrutiny regarding effectiveness of implementation. Ongoing efforts to strengthen compliance frameworks and enhance supervisory oversight address these concerns and support the jurisdiction's reputation as a regional financial centre.

Systemic Risk Considerations and Outlook

Whilst the banking sector's fundamental strengths support financial stability, several factors warrant ongoing monitoring. The high dollarisation creates vulnerability to external shocks and currency movements, though regulatory safeguards and banks' risk management practices mitigate these exposures. Climate risks represent an emerging consideration, given the agricultural sector's importance to the economy and banks' lending exposures to climate-sensitive activities. The 2023 drought's impact on agricultural borrowers highlighted these vulnerabilities, though the banking system absorbed the shock without significant distress.

The financial sector's capacity to support economic growth whilst maintaining stability remains adequate, with credit growth aligned with economic activity and prudent risk management. The new administration's policy priorities, including potential expansion of social programmes and infrastructure investment, may influence credit demand and banks' lending strategies. However, the established regulatory framework and supervisory oversight provide confidence that financial stability will be preserved as the economy evolves.

Looking forward, Uruguay's banking sector is well-positioned to maintain its role as a stabilising force within the sovereign credit profile. The combination of strong capitalisation, effective regulation, and demonstrated resilience through economic cycles supports the assessment that financial stability risks remain manageable and that the banking system will continue to function effectively in supporting economic activity whilst preserving depositor confidence and systemic integrity.

Outlook & Scenarios

Short-Term Outlook (12 months)

Uruguay's credit profile is expected to remain stable over the next twelve months, supported by robust institutional frameworks and demonstrated policy continuity despite the political transition to the Frente Amplio administration under President Yamandú Orsi. The sovereign's investment-grade ratings appear secure, underpinned by the country's exceptional governance metrics ranking in the 83rd percentile globally and its status as South America's only full democracy. The new government has signalled commitment to maintaining the constitutional fiscal rule framework, which constrains the structural deficit to 2.5 per cent of GDP, providing reassurance to credit markets that fiscal discipline will persist even as social spending priorities are addressed.

Economic growth is projected to moderate to approximately 2.5-3.0 per cent in 2026, reflecting normalisation following the strong 3.1 per cent rebound in 2024 from drought-related disruptions. The Central Bank is expected to continue its gradual monetary easing cycle, with policy rates declining from 8.75 per cent towards 7.5-8.0 per cent as inflation remains anchored within the 3-6 per cent target range. The current account deficit should stabilise near 1.0-1.5 per cent of GDP, supported by resilient agricultural exports and continued tourism recovery. Foreign exchange reserves at USD 17.4 billion provide adequate coverage of approximately five months of imports, maintaining the external buffer that has historically supported market confidence.

The primary near-term risk centres on the government's ability to balance its social agenda with fiscal consolidation objectives. The Frente Amplio coalition has pledged increased spending on education, healthcare, and poverty reduction whilst simultaneously committing to fiscal rule compliance. This tension may test policy credibility if revenue performance disappoints or if political pressures mount to accelerate spending programmes. Additionally, Uruguay's high dollarisation rate of 70 per cent of deposits creates ongoing vulnerability to external financial conditions and US monetary policy, though the Central Bank's credibility and flexible exchange rate regime provide important shock absorbers. Climate risks remain elevated given the country's agricultural dependence, with potential drought recurrence representing a material downside scenario for growth and fiscal revenues.

Medium-Term Outlook (1-3 years)

Over the medium term, Uruguay's credit trajectory will be determined by the government's success in addressing structural challenges whilst preserving the institutional strengths that underpin its investment-grade status. The debt-to-GDP ratio, which increased to 68.7 per cent in 2024, is projected to stabilise around 65-68 per cent through 2028, assuming continued fiscal rule compliance and GDP growth averaging 2.0-2.5 per cent annually. This debt trajectory remains manageable given Uruguay's strong market access, diversified funding sources, and favourable debt composition with approximately 60 per cent denominated in local currency. The successful 2023 pension reform, which raised retirement ages and adjusted benefit calculations, has significantly improved long-term fiscal sustainability by reducing projected pension expenditures by approximately 1.5 percentage points of GDP over the coming decade.

The structural growth challenge represents the most significant medium-term constraint on Uruguay's credit profile. Following average annual growth of 5.4 per cent between 2005 and 2014, the economy has expanded by just 1.6 per cent annually since 2015, reflecting declining productivity growth, limited labour force expansion, and insufficient investment rates. Addressing this growth deceleration requires structural reforms to enhance competitiveness, reduce labour market rigidities, and attract foreign direct investment beyond traditional agricultural and tourism sectors. The government's ability to implement productivity-enhancing reforms whilst managing coalition politics and union relationships will be critical to lifting potential growth towards 3.0 per cent, which would materially strengthen debt dynamics and support rating stability.

Uruguay's external position is expected to remain a relative credit strength, supported by the country's 98 per cent renewable energy matrix, which insulates the economy from fossil fuel price volatility, and diversified export markets spanning Argentina, Brazil, China, and the European Union. The current account deficit should remain modest at 1.0-2.0 per cent of GDP, easily financed through foreign direct investment and portfolio flows given Uruguay's status as the lowest-risk sovereign in Latin America with spreads of just 125 basis points. However, persistent dollarisation constrains monetary policy effectiveness and maintains currency mismatch vulnerabilities, particularly for households and small businesses with dollar-denominated liabilities and peso incomes. Progress on gradual de-dollarisation through continued inflation control and financial market deepening would represent a positive credit development, though meaningful change is likely to require sustained effort over many years given deeply entrenched preferences.

Rating Scenarios

Upside Scenario (Probability: 20-25%)

An upgrade to A- from S&P or Baa1 to A3 from Moody's over the medium term would require Uruguay to demonstrate sustained progress on structural reform implementation that lifts potential growth towards 3.0-3.5 per cent whilst maintaining fiscal discipline. Specifically, successful labour market reforms that enhance flexibility without compromising social protections, coupled with regulatory improvements that attract diversified foreign investment beyond traditional sectors, would signal strengthening fundamentals. A debt-to-GDP trajectory declining towards 60 per cent through a combination of higher growth and continued primary surplus generation would provide quantitative support for an upgrade. Additionally, meaningful progress on financial de-dollarisation, evidenced by the share of dollar deposits declining from 70 per cent towards 60 per cent, would reduce structural vulnerabilities and enhance monetary policy effectiveness. The upside scenario also assumes continued institutional strengthening, with governance metrics improving further and successful navigation of the 2029 electoral cycle without policy disruption.

Base Case Scenario (Probability: 60-65%)

The most likely scenario involves rating stability across all three agencies over the next two to three years, with Uruguay maintaining its current BBB+/Baa1/BBB ratings and stable outlooks. This scenario assumes the Frente Amplio government successfully balances social spending priorities with fiscal rule compliance, keeping the structural deficit within the 2.5 per cent constitutional limit whilst addressing coalition demands for increased education and healthcare funding. GDP growth averages 2.0-2.5 per cent annually, sufficient to stabilise the debt-to-GDP ratio around 65-68 per cent but insufficient to generate material fiscal space or drive significant debt reduction. Inflation remains controlled within the 3-6 per cent target range, supporting Central Bank credibility and allowing gradual monetary normalisation. The current account deficit stays modest at 1.0-2.0 per cent of GDP, easily financed through stable capital inflows given Uruguay's regional safe-haven status. This scenario incorporates moderate climate shocks that temporarily affect agricultural output but do not fundamentally alter the growth trajectory, consistent with historical patterns of resilience and recovery.

Downside Scenario (Probability: 15-20%)

A downgrade to BBB from S&P or Baa2 from Moody's would most likely result from fiscal slippage that undermines the credibility of Uruguay's institutional framework. Specifically, sustained breaches of the constitutional fiscal rule driven by political pressures to expand social spending without offsetting revenue measures would signal weakening policy discipline. A debt-to-GDP trajectory rising above 72-75 per cent due to combination of fiscal deterioration and weak growth would raise sustainability concerns, particularly if accompanied by reduced market access or rising borrowing costs. The downside scenario could be triggered by severe climate shocks, such as consecutive drought years that contract agricultural output by 15-20 per cent and reduce fiscal revenues whilst necessitating emergency support spending. Additionally, significant external shocks including sharp deterioration in Argentina or Brazil that disrupts trade flows and tourism, coupled with tightening global financial conditions that pressure emerging market spreads, could test Uruguay's resilience. Political fragmentation that prevents necessary reforms or generates policy uncertainty, though currently unlikely given Uruguay's strong democratic institutions, would represent an additional downside risk factor that could erode the governance premium supporting the sovereign's ratings.

Conclusion

Uruguay's sovereign credit profile remains firmly anchored in the investment-grade category, underpinned by institutional quality that distinguishes it markedly from regional peers. The country's governance framework—evidenced by its 83rd percentile World Bank ranking and status as South America's sole "full democracy"—provides a robust foundation for policy credibility and economic resilience. This institutional strength has enabled Uruguay to maintain the lowest sovereign risk spreads in Latin America at 125 basis points, substantially below the regional average of 381 basis points, whilst securing stable outlooks from all three major rating agencies.

The economic trajectory through 2024 demonstrated the sovereign's capacity to navigate external shocks effectively. The 3.1% GDP growth recovery following the severe 2023 drought, coupled with successful inflation management bringing price pressures to 4.8% within the Central Bank's target range, reflects sound macroeconomic stewardship. The narrowing of the current account deficit to merely 0.8% of GDP and the accumulation of foreign exchange reserves to USD 17.4 billion further strengthen the external position. These achievements occurred within the framework of Uruguay's constitutional fiscal rule, which has proven instrumental in maintaining market confidence through political transitions.

Nevertheless, structural challenges warrant continued monitoring. The debt-to-GDP ratio's rise to 68.7% in 2024, whilst manageable, requires sustained fiscal discipline to prevent further deterioration. Uruguay's persistent high dollarisation at 70% of deposits creates ongoing vulnerabilities to exchange rate volatility and limits monetary policy autonomy. The economy's moderate growth potential—averaging just 1.6% since 2015 compared with 5.4% in the preceding decade—constrains the sovereign's capacity to reduce debt burdens through expansion alone. Climate vulnerability, starkly illustrated by the 2023 drought's 25% contraction in agricultural output, represents an intensifying risk factor requiring adaptive policy responses.

The transition to the Frente Amplio administration under President Yamandú Orsi introduces policy uncertainty, particularly regarding the balance between social spending commitments and fiscal consolidation imperatives. However, Uruguay's demonstrated institutional continuity across political cycles, successful implementation of pension reform in 2023, and track record of fiscal rule compliance provide reasonable assurance of policy stability. The sovereign's 98% renewable energy matrix and diversified economic base offer additional buffers against external shocks.

On balance, Uruguay's investment-grade status appears secure over the medium term, supported by exceptional governance metrics, manageable debt dynamics, and proven crisis management capabilities. The stable outlooks from S&P, Moody's, and Fitch reflect confidence that the sovereign will continue navigating the tension between growth constraints and fiscal discipline whilst maintaining its position as Latin America's most creditworthy emerging market. Sustained adherence to the fiscal framework and continued institutional strengthening will prove critical to preserving this favourable credit standing amidst evolving domestic priorities and external headwinds.