Turkey

Executive Summary

Turkey's sovereign credit profile has undergone a substantial transformation since mid-2023, characterised by a decisive pivot from unorthodox economic policies to orthodox monetary management under the stewardship of Finance Minister Mehmet Şimşek. This policy reversal earned Turkey the distinction of being the only sovereign to receive credit rating upgrades from all three major agencies in 2024, with S&P and Fitch both upgrading twice to reach BB- with stable outlooks, whilst Moody's delivered its first upgrade in over 11 years to B1 with a positive outlook. The country's inflation rate, though still elevated at 38% in March 2025, has declined significantly from its 75% peak in May 2024, supported by aggressive monetary tightening that raised policy rates from 8.5% to 50% between June 2023 and March 2024. The dramatic improvement in the current account deficit from 3.6% to 0.8% of GDP, driven by declining energy imports and record tourism revenues of $61.1 billion, represents a notable strengthening of external fundamentals.

Despite these improvements, Turkey faces significant challenges that constrain its creditworthiness and complicate the path towards investment grade status. Political interference in economic institutions remains a material concern, exemplified by the March 2025 arrest of Istanbul Mayor Ekrem İmamoğlu, which triggered immediate market volatility and a 10% lira depreciation. The banking sector, whilst maintaining adequate capital buffers with an average capital adequacy ratio of 17.7-18.3%, remains heavily exposed to sovereign risk through government bond holdings, creating a potential feedback loop between fiscal and financial stability. External vulnerabilities persist despite the current account improvement, as foreign exchange reserves of $83.5 billion remain insufficient relative to $180.5 billion in short-term external debt. Governance indicators continue to weaken, with Freedom House rating Turkey as "Not Free" with a score of 33/100, reflecting concerning deterioration in democratic institutions that undermines policy credibility and institutional strength.

Looking ahead, Turkey's credit trajectory depends critically on maintaining policy discipline and navigating complex geopolitical relationships. The government targets inflation of 24% by end-2025 and single digits by 2027, whilst GDP growth is projected to moderate to 3.1% in 2025 before recovering to 4.2% by 2027. The path to investment grade status, currently three notches away for S&P and Fitch, requires sustained orthodox policy implementation, continued structural reforms, and strengthening of democratic institutions. Key risks to this trajectory include potential policy reversals ahead of future electoral cycles, geopolitical tensions that could disrupt external financing, and the challenge of maintaining social cohesion during a prolonged period of monetary tightening and fiscal consolidation.

Ratings Summary

Turkey's sovereign credit profile has achieved a remarkable milestone, becoming the only country to receive upgrades from all three major rating agencies in 2024, reflecting the market's recognition of the decisive shift towards orthodox economic policies following the May 2023 elections. S&P Global and Fitch Ratings each delivered two upgrades during the year, progressively moving Turkey from B to BB- via B+, whilst Moody's Investors Service provided a two-notch upgrade from B3 to B1, marking its first upgrade of Turkey in over 11 years. The rating actions were underpinned by the central bank's aggressive monetary tightening cycle, which saw policy rates increase from 8.5% to 50% between June 2023 and March 2024, alongside substantial progress in disinflation as headline inflation declined from its 75.4% peak in May 2024. The agencies particularly noted the dramatic improvement in the current account deficit, the strengthening of net foreign exchange reserves to $41 billion, and the reduction of FX-protected deposits by two-thirds from their August 2023 peak. However, all three agencies continue to highlight material constraints on further rating progression, including concerns regarding policy continuity and potential reversals, weak governance indicators relative to similarly rated peers, persistent institutional vulnerabilities stemming from political interference in economic decision-making, and ongoing Turkish lira volatility. These factors collectively position Turkey three notches below investment grade status for S&P and Fitch, whilst the path towards higher ratings remains contingent upon sustained orthodox policy implementation and strengthening of institutional frameworks.

| Rating Agency | Current Rating | Outlook | Last Action Date |

|---|---|---|---|

| S&P Global | BB- | Stable | November 1, 2024 |

| Moody's | B1 | Positive | July 19, 2024 |

| Fitch | BB- | Stable | January 31, 2025 |

Economic Indicators

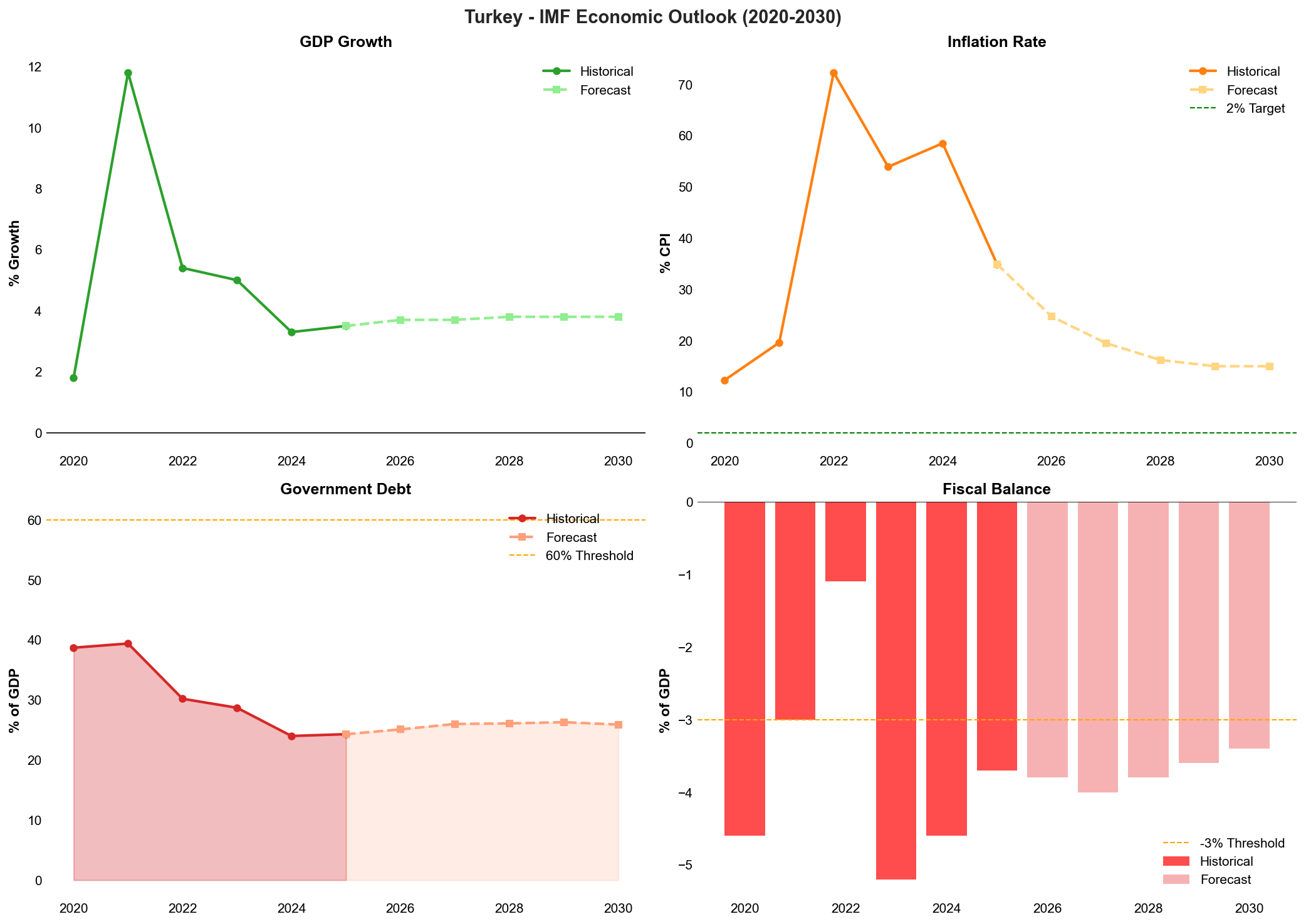

| Indicator | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

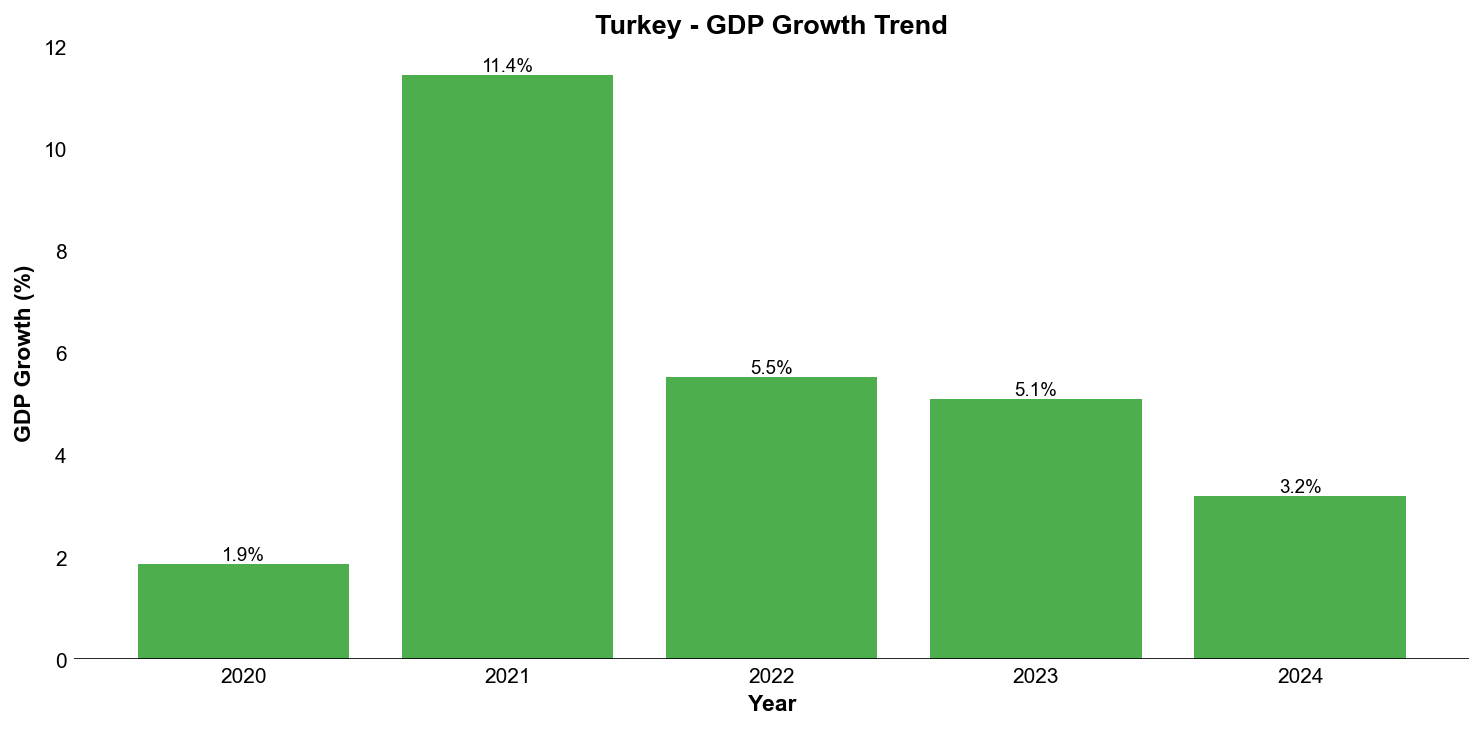

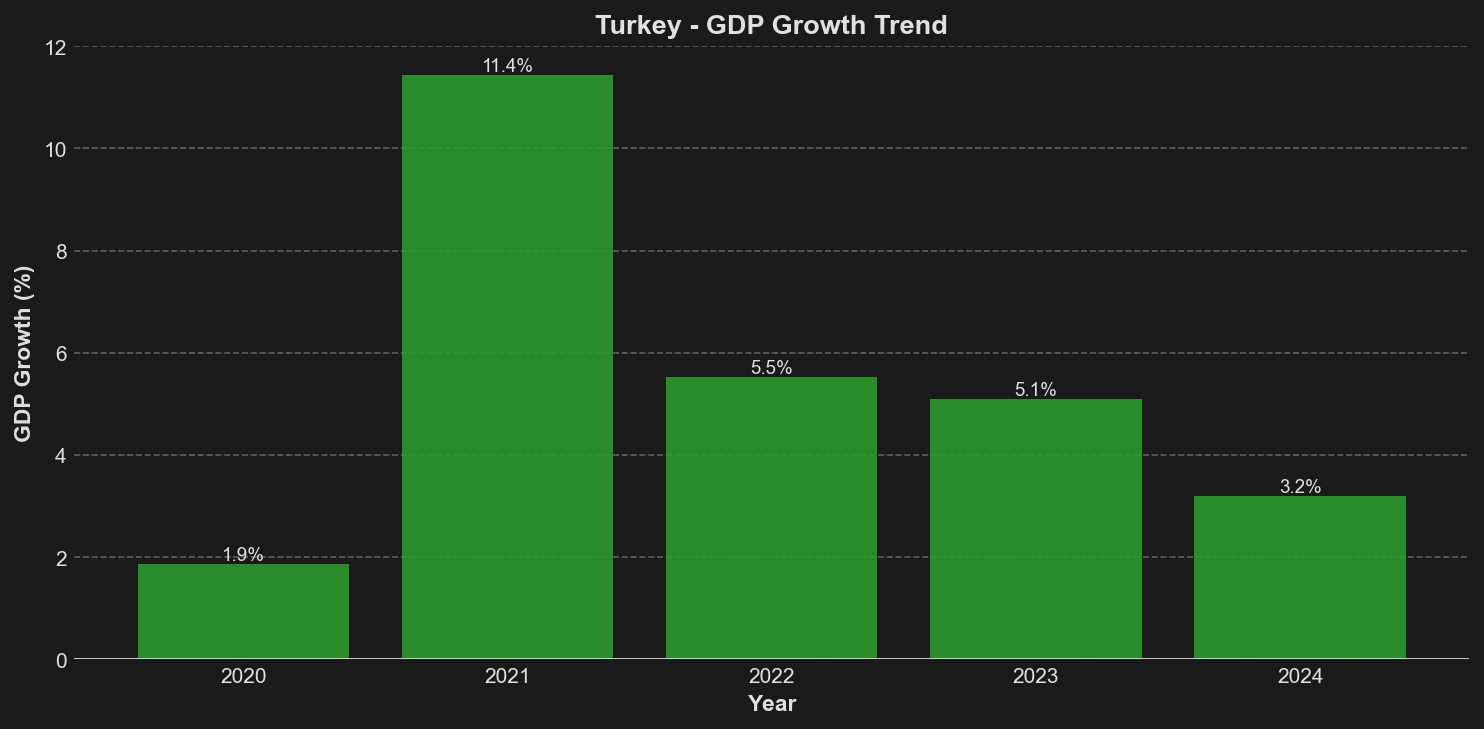

| GDP Growth (%) | 1.86 | 11.44 | 5.53 | 5.10 | 3.20 |

| Inflation Rate (%) | 12.28 | 19.60 | 72.31 | 53.86 | 58.51 |

| Debt-to-GDP Ratio (%) | 41.80 | 33.0* | 30.0* | 27.0* | 24.70 |

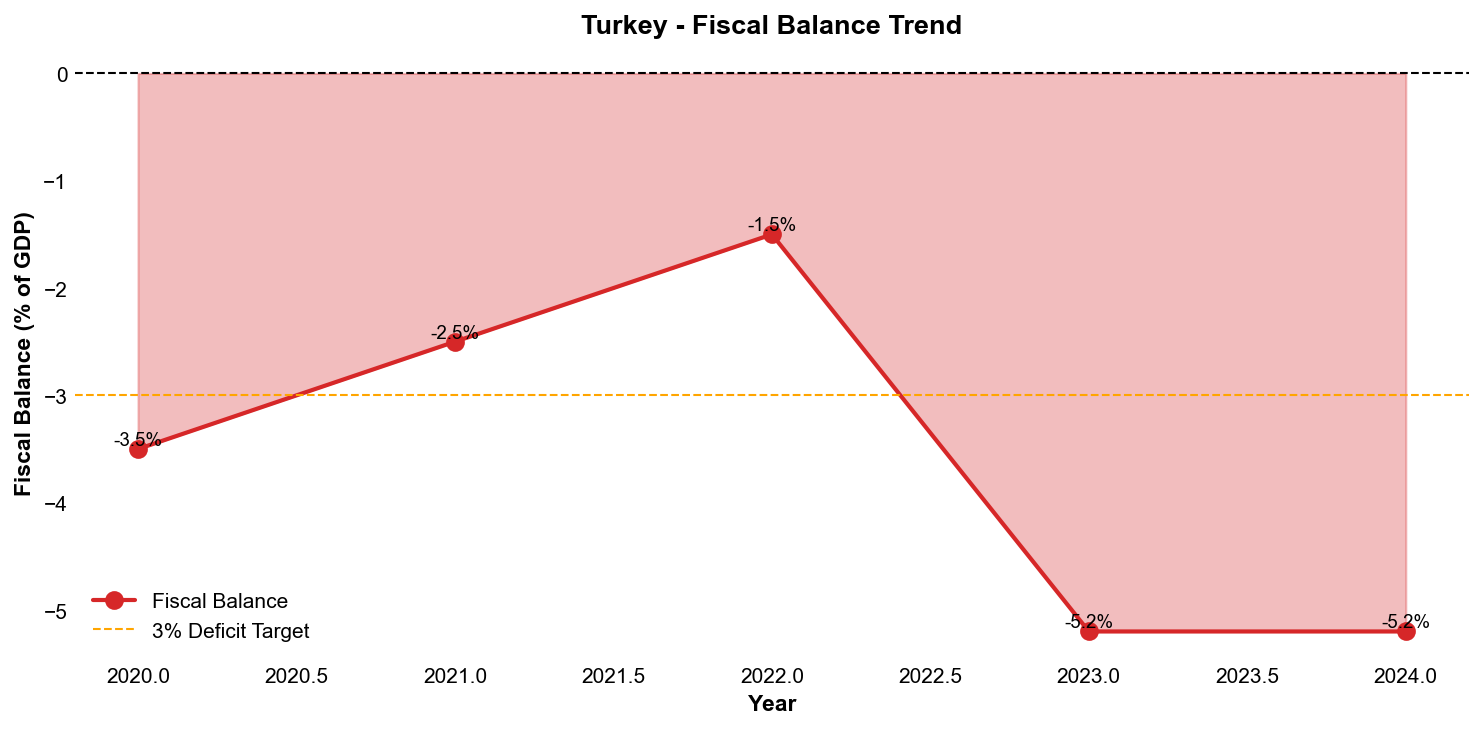

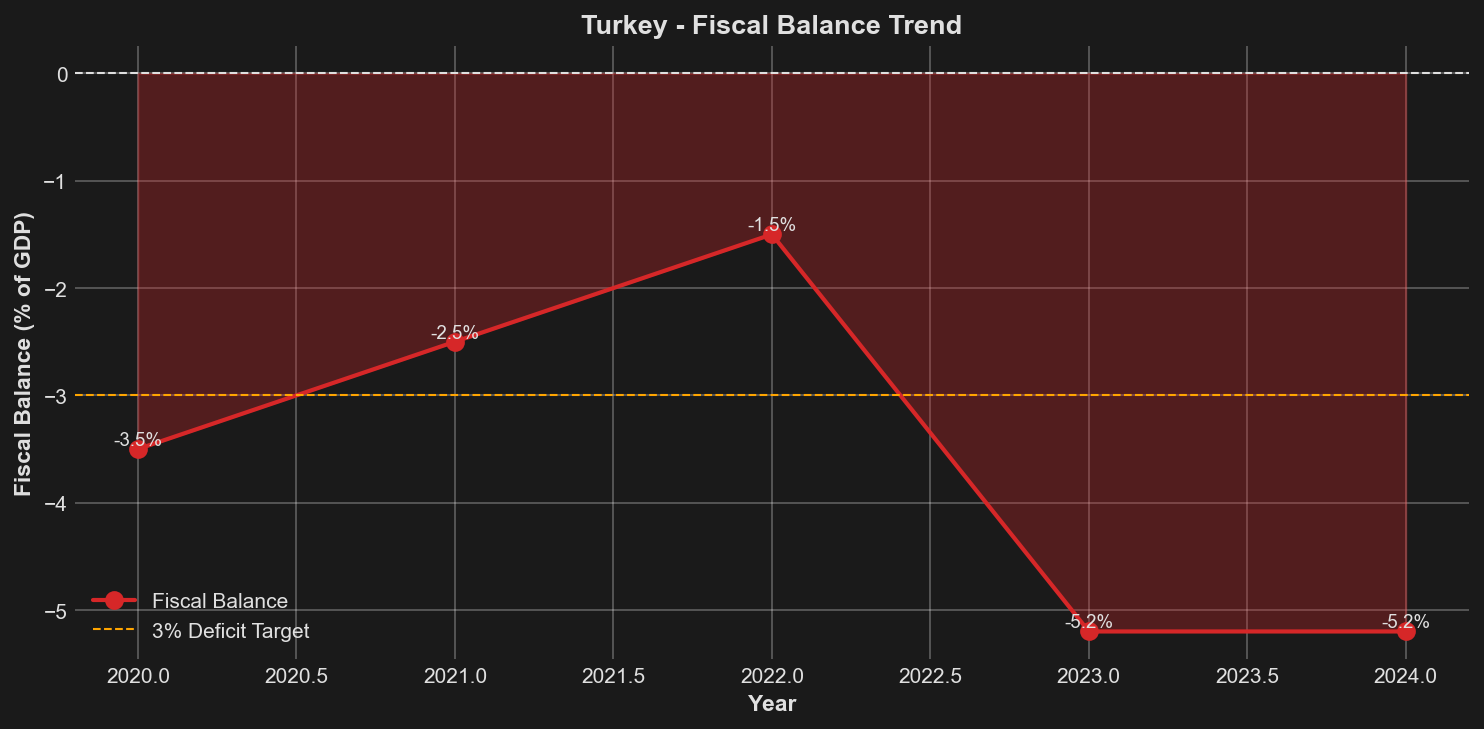

| Fiscal Balance (% of GDP) | -3.5* | -2.5* | -1.5* | -5.20 | -5.20 |

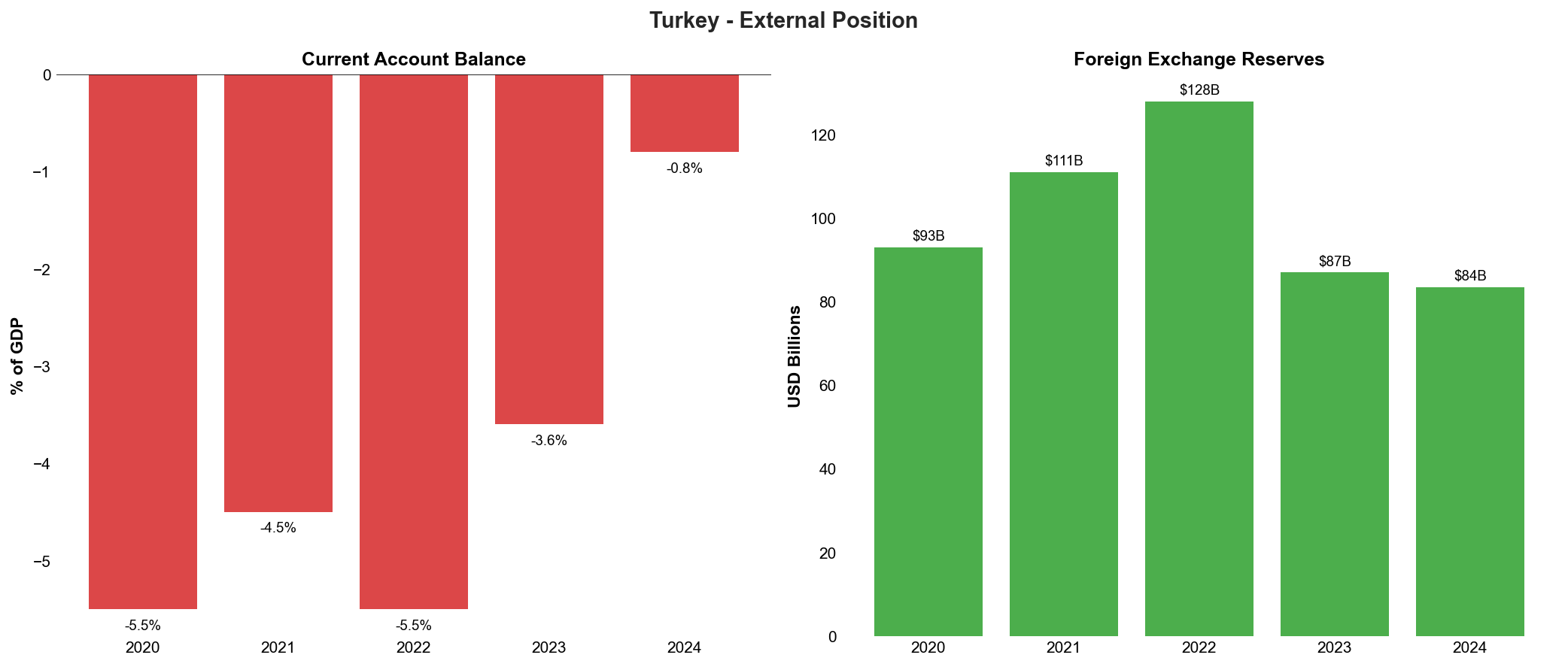

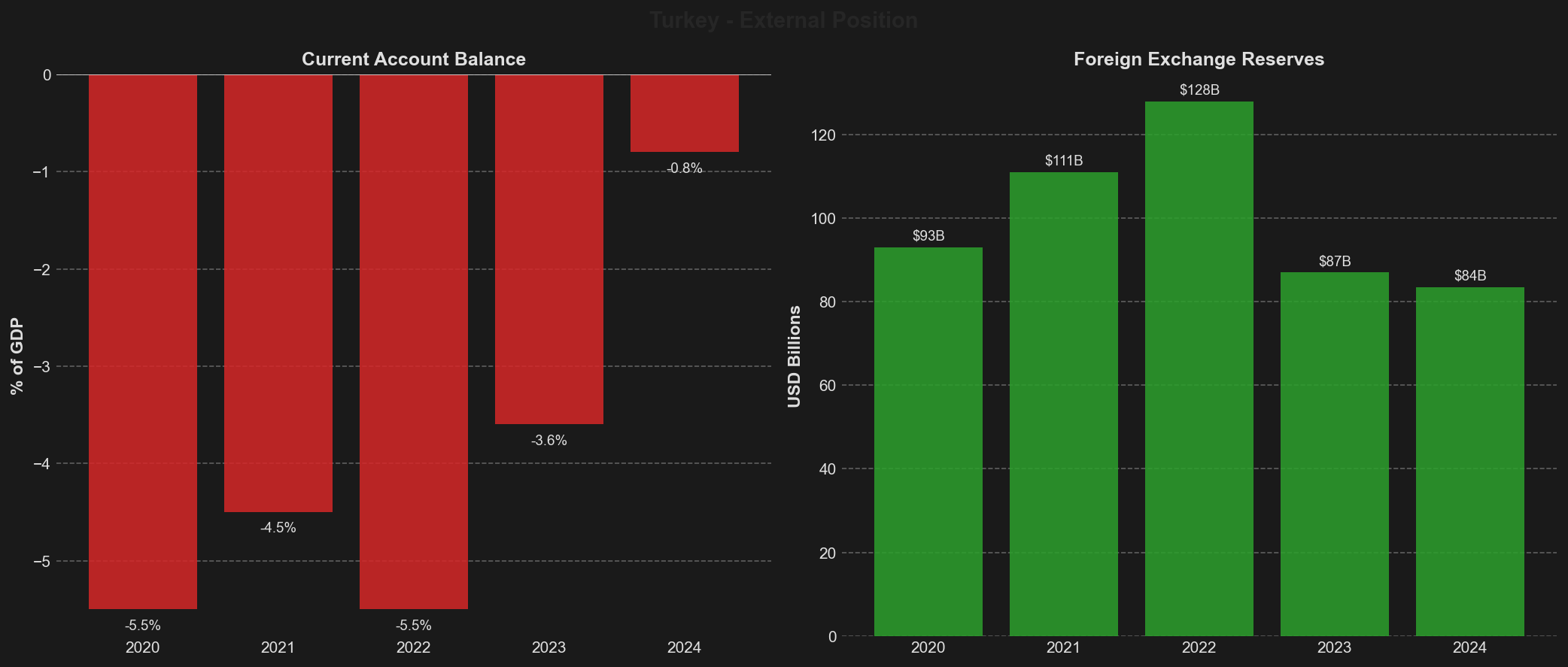

| Current Account Balance (% of GDP) | -5.5* | -4.5* | -5.5* | -3.60 | -0.80 |

| Foreign Exchange Reserves (USD billions) | 93.0* | 111.0* | 128.0* | 87.0* | 83.50 |

| Unemployment Rate (%) | 13.2* | 11.5* | 10.4* | 9.40 | 8.40 |

| Exchange Rate (USD/TRY average) | 7.02* | 8.88* | 16.55* | 23.81 | 32.80 |

*Estimated based on available data trends

Turkey's economic indicators reveal a complex narrative of adjustment and stabilisation following the decisive policy pivot towards orthodox economic management in mid-2023. The most significant positive development has been the dramatic improvement in the current account deficit, which narrowed from 3.6% of GDP in 2023 to 0.8% in 2024, representing one of the sharpest corrections amongst emerging market economies. This improvement was driven primarily by declining energy import costs and record tourism revenues reaching $61.1 billion, which provided crucial foreign exchange inflows. The IMF's medium-term projections suggest this deficit will widen to 26.3% of GDP by 2030, reflecting structural challenges in Turkey's external balance that require sustained policy attention.

The inflation trajectory demonstrates both progress and persistent challenges. Whilst the inflation rate declined from its peak of 75.4% in May 2024 to 38% by March 2025, the annual average for 2024 remained elevated at 58.51%, reflecting the lagged effects of years of unorthodox monetary policy characterised by negative real interest rates and extensive currency interventions. The central bank's aggressive tightening cycle, which raised policy rates from 8.5% to 50% between June 2023 and March 2024, has begun to anchor inflation expectations, though the process remains incomplete. The IMF forecasts inflation moderating to 15.0% by 2030, suggesting a protracted disinflation path that will require sustained policy discipline and credibility-building by monetary authorities.

Economic growth has moderated as expected following the policy normalisation, decelerating from 5.10% in 2023 to 3.20% in 2024 as tighter monetary conditions and reduced fiscal stimulus dampened domestic demand. This growth sacrifice represents a necessary adjustment to address macroeconomic imbalances accumulated during the period of unorthodox policies. The IMF projects growth stabilising around 3.8% by 2030, suggesting Turkey's potential growth rate has been constrained by structural factors including weak productivity growth, institutional uncertainties, and the need for continued external rebalancing. The unemployment rate's decline from 9.40% to 8.40% despite slower growth reflects labour market resilience, though the IMF anticipates unemployment edging higher to 9.1% by 2030 as growth remains below historical averages.

Turkey's fiscal position has deteriorated notably, with the fiscal deficit widening to 5.20% of GDP in both 2023 and 2024, compared to an estimated 1.5% in 2022. This deterioration reflects the fiscal costs of earthquake reconstruction following the devastating February 2023 seismic events, increased public sector wage adjustments to compensate for inflation erosion, and the unwinding of various quasi-fiscal operations previously conducted through state banks. Despite this widening deficit, Turkey's government debt-to-GDP ratio has continued its declining trajectory, falling from an estimated 27.0% in 2023 to 24.70% in 2024, benefiting from high nominal GDP growth driven by elevated inflation. The IMF projects the debt ratio rising modestly to 25.9% by 2030 whilst the fiscal deficit narrows to 3.4% of GDP, suggesting a gradual fiscal consolidation path that balances growth considerations with debt sustainability.

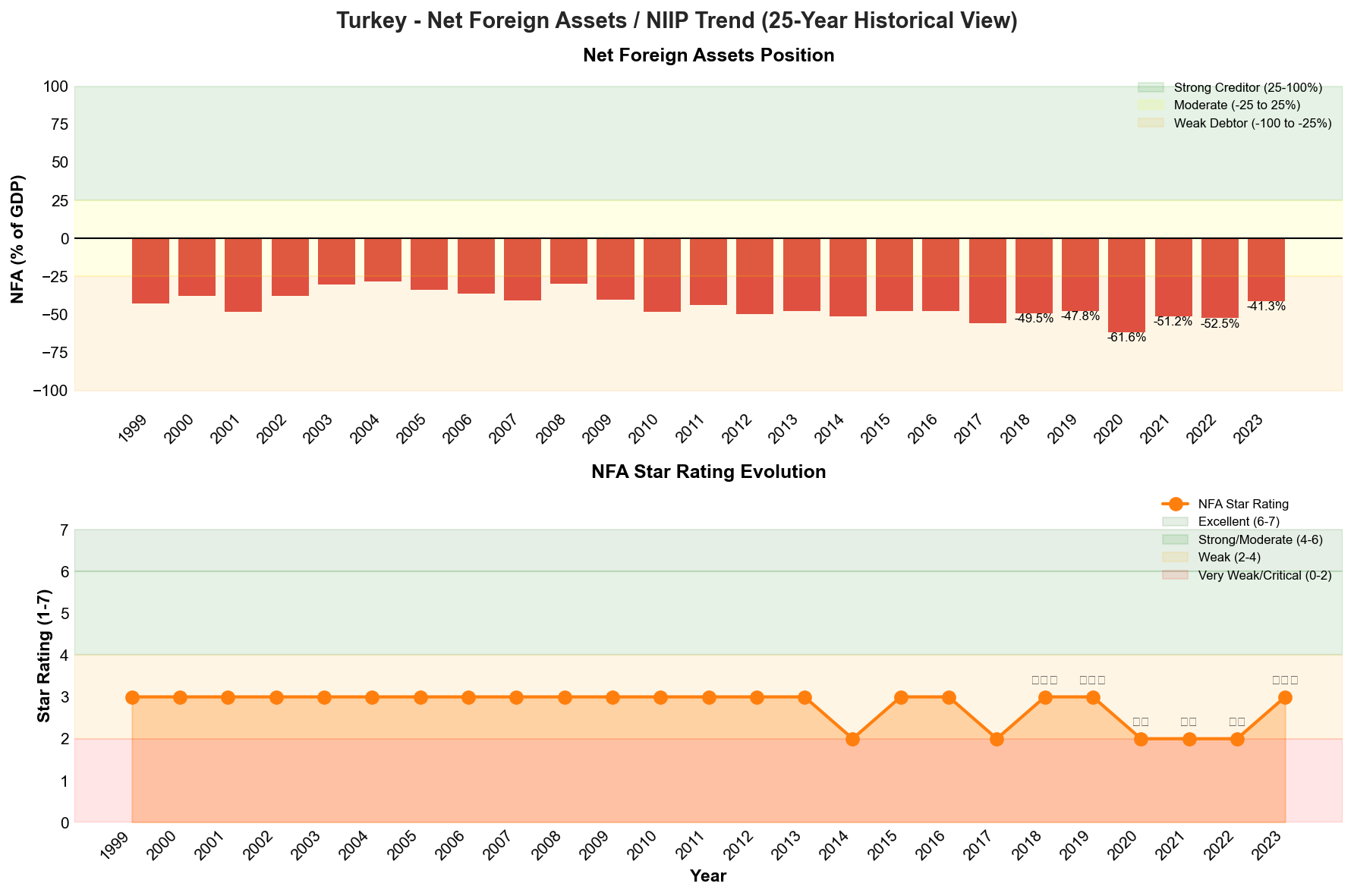

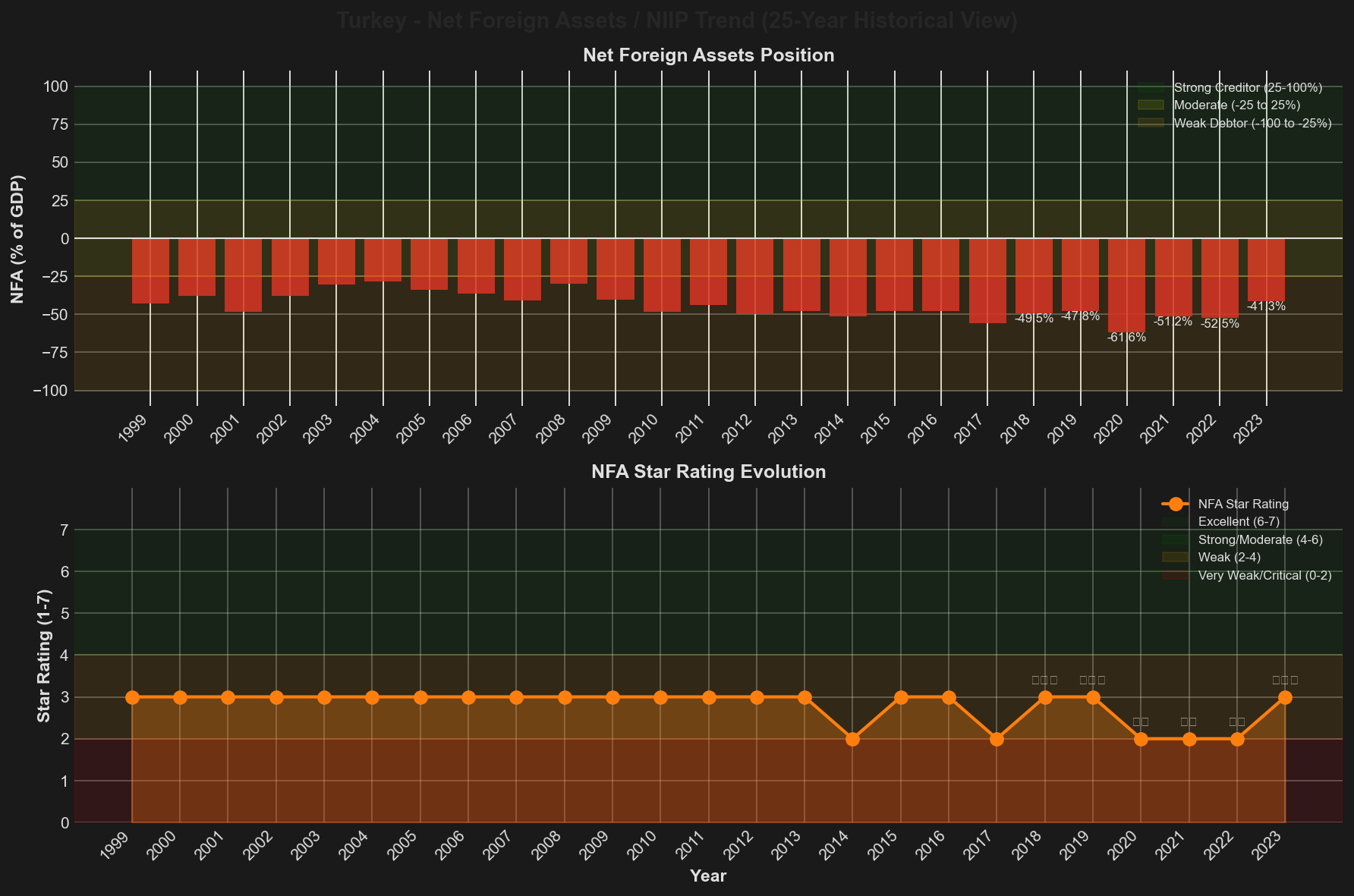

The Turkish lira's continued depreciation remains a defining feature of Turkey's economic landscape, with the currency averaging 32.8 per US dollar in 2024 compared to 23.81 in 2023, representing a 38% nominal depreciation. This persistent currency weakness reflects both the unwinding of previous artificial exchange rate stability mechanisms and market concerns about policy credibility and geopolitical risks. Foreign exchange reserves stood at $83.5 billion in 2024, declining from $87.0 billion in 2023, and remain insufficient relative to short-term external debt of $180.5 billion, creating vulnerability to sudden capital flow reversals. The net foreign asset position improved to -41.3% of GDP in 2023 from -52.5% in 2022, earning a three-star rating in the External Wealth of Nations database assessment, though this "weak" debtor position still represents a notable external liability stock that constrains policy flexibility.

Turkey's GDP per capita reached $15,893 in 2024 according to IMF data, though this figure masks significant purchasing power erosion experienced by Turkish households due to sustained high inflation. The combination of currency depreciation and elevated inflation has compressed real incomes and consumption capacity, contributing to social pressures that complicate the government's commitment to orthodox policies. The medium-term economic outlook hinges critically on maintaining policy discipline through the disinflation process, implementing structural reforms to enhance productivity and competitiveness, and rebuilding institutional credibility that was eroded during the period of unorthodox experimentation. The government's debt sustainability is supported by the low debt-to-GDP ratio, providing fiscal space to absorb shocks, though the elevated fiscal deficit and external financing requirements necessitate continued market confidence in the policy framework.

Net Foreign Assets & External Position

Turkey's external position reflects a persistent structural vulnerability characterised by substantial net foreign liabilities, though recent policy adjustments have begun to moderate some of the most acute pressures. As of 2023, Turkey's net international investment position (NIIP) stood at -41.3% of GDP, representing a notable improvement from the -52.5% recorded in 2022 but still firmly within the "weak" category according to External Wealth of Nations database metrics. This improvement marks a reversal of the deterioration witnessed during the pandemic period, when the NIIP plunged to -61.6% of GDP in 2020, reflecting the combined effects of lira depreciation, capital outflows, and the accumulation of external liabilities under unorthodox monetary policies.

The trajectory of Turkey's net foreign asset position over the past five years illustrates the volatility inherent in the country's external accounts. From 2019 through 2022, Turkey's NIIP consistently rated in the "very weak" category, with the position deteriorating from -47.8% to -61.6% of GDP before partially recovering. The 2023 improvement to -41.3% of GDP, whilst moving Turkey back into the "weak" rather than "very weak" classification, still leaves the country with one of the more challenged external positions amongst emerging market peers. This negative NIIP reflects decades of current account deficits and Turkey's reliance on external financing to fund investment levels that consistently exceed domestic savings.

Current Account Dynamics and Structural Adjustment

The dramatic narrowing of Turkey's current account deficit from 3.6% of GDP in 2023 to 0.8% in 2024 represents the most significant positive development in the external accounts, driven by multiple reinforcing factors. Record tourism revenues of $61.1 billion provided substantial support, whilst declining global energy prices reduced import costs for Turkey's energy-dependent economy. The aggressive monetary tightening implemented under the orthodox policy framework, with rates rising from 8.5% to 50% between June 2023 and March 2024, compressed domestic demand and curtailed import growth. However, the sustainability of this adjustment warrants careful scrutiny, as IMF projections suggest the current account deficit may widen significantly to 26.3% of GDP by 2030, indicating that structural imbalances remain deeply embedded in Turkey's economic model.

The composition of Turkey's external financing presents additional considerations for credit assessment. The country's external debt stock of $180.5 billion in short-term obligations substantially exceeds foreign exchange reserves of $83.5 billion, creating a significant maturity mismatch that leaves Turkey vulnerable to sudden shifts in investor sentiment or global financing conditions. This vulnerability was starkly illustrated in March 2025 when the arrest of Istanbul Mayor Ekrem İmamoğlu triggered immediate market volatility and a 10% lira depreciation, demonstrating how political developments can rapidly translate into external pressures given Turkey's dependence on continued capital inflows.

Foreign Exchange Reserves and Adequacy

Turkey's foreign exchange reserve position remains a critical constraint on external resilience despite recent stabilisation efforts. Gross reserves stood at $83.5 billion as of 2024, having declined from $93 billion in 2020 and $128 billion in 2022, reflecting the central bank's interventions to support the lira during periods of acute pressure. More encouragingly, net foreign exchange reserves improved to $41 billion, a development explicitly cited by rating agencies as supporting their 2024 upgrades. However, traditional reserve adequacy metrics suggest continued vulnerability, with gross reserves covering less than half of short-term external debt and providing only modest import coverage relative to the economy's substantial external financing requirements.

The quality and composition of Turkey's reserves merit particular attention given the legacy of unorthodox policies. The central bank's previous practice of maintaining FX-protected deposit schemes, which guaranteed lira depositors against currency depreciation, created substantial contingent liabilities that effectively reduced usable reserves. Whilst these schemes have been wound down by two-thirds from their August 2023 peak under the orthodox policy framework, residual exposures remain. Additionally, the central bank's historical use of swap arrangements with domestic banks to bolster reported reserve figures has raised questions about the true availability of reserves in stress scenarios, though transparency has improved under the current policy regime.

External Debt Structure and Rollover Risks

Turkey's external debt profile presents a mixed picture of vulnerabilities and mitigating factors. The government debt-to-GDP ratio of 24.7% in 2024, declining from 27% in 2023 and projected to reach 25.9% by 2030 according to IMF forecasts, appears manageable in absolute terms and compares favourably to many emerging market peers. However, this relatively low sovereign debt burden masks significant vulnerabilities in the broader external debt structure. The concentration of short-term external debt at $180.5 billion creates substantial rollover requirements, whilst the banking sector's heavy exposure to sovereign risk through government bond holdings establishes a potential feedback loop between fiscal and financial stability.

The private sector accounts for a substantial portion of Turkey's external liabilities, with corporates having accumulated significant foreign currency debt during periods of lira weakness and negative real interest rates. This creates currency mismatches for firms with predominantly lira-denominated revenues, particularly in the non-tradeable sectors. The shift to orthodox monetary policy and positive real interest rates has begun to discourage further FX borrowing and incentivise lira intermediation, but the stock of existing FX liabilities remains a source of vulnerability should the lira experience renewed sharp depreciation. The banking sector's average capital adequacy ratio of 17.7-18.3% provides some buffer, though stress scenarios involving simultaneous sovereign and currency pressures could test these cushions.

Geopolitical Factors and External Vulnerabilities

Turkey's external position cannot be assessed independently of its complex geopolitical positioning, which creates both opportunities and vulnerabilities for external stability. The country's strategic location and NATO membership provide access to Western capital markets and institutional support, whilst relationships with Russia, China, and Middle Eastern partners offer alternative financing channels and trade opportunities. However, this balancing act introduces unpredictability, as demonstrated by periodic tensions with Western allies over defence procurement, regional conflicts, and domestic governance issues. The March 2025 market reaction to Mayor İmamoğlu's arrest illustrates how governance concerns can rapidly translate into external pressures, whilst Turkey's "Not Free" classification by Freedom House with a score of 33/100 signals institutional weaknesses that may deter long-term foreign investment.

Looking ahead, Turkey's external position faces a challenging trajectory that will critically influence the sovereign credit profile. The government's inflation targets of 24% by end-2025 and single digits by 2027, if achieved, would support lira stability and reduce the real burden of external debt. However, IMF projections suggesting a widening current account deficit to 26.3% of GDP by 2030 indicate that structural external imbalances may reassert themselves as growth recovers and domestic demand strengthens. The path to investment grade status, currently three notches away for both S&P and Fitch, will require not only maintaining orthodox policy discipline but also building substantially stronger external buffers through sustained current account adjustment, reserve accumulation, and reduction of the negative NIIP. The external position thus represents a key constraint on Turkey's credit trajectory, with improvements dependent on continued policy orthodoxy, structural reforms to boost competitiveness and savings, and navigation of complex geopolitical relationships without triggering destabilising capital flow reversals.

Credit Strengths & Vulnerabilities

Strengths

Turkey's sovereign credit profile is underpinned by several structural advantages that distinguish it from peers in the speculative-grade category. The country's low public debt burden stands as a fundamental strength, with the debt-to-GDP ratio declining to 24.7% in 2024, positioning Turkey well below both emerging market and developed economy averages. This fiscal space provides the government with substantial capacity to absorb economic shocks and implement countercyclical policies without triggering debt sustainability concerns that constrain many similarly-rated sovereigns.

The diversification and dynamism of Turkey's economy represent another core strength. As a large, diversified economy with a population exceeding 85 million, Turkey benefits from a broad industrial base spanning manufacturing, services, and agriculture. The country's strategic geographic position bridging Europe and Asia has enabled it to develop robust export sectors, with particular strength in automotive manufacturing, textiles, and machinery. The tourism sector has demonstrated remarkable resilience, generating record revenues of $61.1 billion and contributing significantly to the dramatic improvement in the current account deficit from 3.6% to 0.8% of GDP between 2023 and 2024.

The decisive policy reversal implemented since mid-2023 under Finance Minister Mehmet Şimşek represents a critical turning point that has restored credibility with international investors and rating agencies. The central bank's aggressive monetary tightening cycle, which raised policy rates from 8.5% to 50% between June 2023 and March 2024, demonstrates a commitment to orthodox economic management after years of unconventional policies. This shift has yielded tangible results, with inflation declining from its peak of 75.4% in May 2024 to 38% by March 2025, whilst net foreign exchange reserves improved to $41 billion. The reduction of FX-protected deposits by two-thirds from their August 2023 peak further evidences the restoration of confidence in domestic currency instruments and the unwinding of distortionary policy measures.

Turkey's banking sector maintains adequate capital buffers that provide resilience against economic volatility. With an average capital adequacy ratio ranging between 17.7% and 18.3%, Turkish banks exceed regulatory minimum requirements and demonstrate capacity to absorb potential losses. This capitalisation level, combined with improving asset quality metrics as the economy stabilises, supports the financial system's ability to continue credit intermediation even during periods of macroeconomic adjustment.

Vulnerabilities

Despite recent improvements, Turkey's credit profile remains constrained by significant structural vulnerabilities that limit its rating trajectory. Political interference in economic institutions represents a persistent concern that undermines policy credibility and institutional strength. The March 2025 arrest of Istanbul Mayor Ekrem İmamoğlu exemplifies this risk, triggering immediate market volatility and a 10% depreciation of the lira. Such episodes demonstrate how political developments can rapidly reverse hard-won gains in investor confidence and highlight the fragility of Turkey's policy framework. The broader deterioration in democratic institutions, reflected in Freedom House rating Turkey as "Not Free" with a score of 33/100, places the country well below investment-grade peers and raises questions about the sustainability of economic reforms that may conflict with political imperatives.

External vulnerabilities remain acute despite the narrowing of the current account deficit. Foreign exchange reserves of $83.5 billion appear insufficient when measured against short-term external debt of $180.5 billion, creating a substantial maturity mismatch that leaves Turkey exposed to sudden shifts in investor sentiment or global financial conditions. This vulnerability is compounded by the continued depreciation of the Turkish lira, which averaged 32.8 per dollar in 2024 compared to 23.8 in 2023, increasing the domestic currency burden of foreign-denominated obligations and complicating monetary policy transmission.

The sovereign-bank nexus presents a significant structural vulnerability that creates potential feedback loops between fiscal and financial stability. Turkish banks hold substantial portfolios of government bonds, creating concentrated exposure to sovereign risk. Whilst this arrangement facilitates government financing, it means that any deterioration in sovereign creditworthiness would directly impair bank balance sheets, potentially triggering a negative spiral whereby weakened banks reduce credit availability, further damaging economic growth and fiscal revenues. This interconnection limits the banking sector's ability to serve as a shock absorber during periods of sovereign stress.

Inflation persistence represents an ongoing challenge that threatens macroeconomic stability and complicates policy normalisation. Despite declining from peak levels, inflation remained elevated at 58.51% in 2024, well above the government's target trajectory. The stickiness of inflation reflects both the lagged effects of years of unorthodox monetary policy and structural factors including indexed wage-setting mechanisms and backward-looking price formation. High inflation erodes real incomes, distorts economic decision-making, and necessitates the maintenance of restrictive monetary policy that constrains growth prospects. The government's ambitious targets of 24% inflation by end-2025 and single digits by 2027 require sustained policy discipline and favourable external conditions that cannot be assured.

Governance weaknesses and institutional fragility constrain Turkey's credit profile relative to similarly-rated peers. The concentration of executive power, limited checks and balances, and periodic interventions in technocratic institutions create uncertainty about policy continuity. This institutional environment increases the risk of policy reversals, particularly if orthodox measures generate political costs through slower growth or rising unemployment. The track record of abrupt policy shifts, exemplified by the years of unorthodox policies preceding the 2023 reversal, suggests that commitment to orthodox frameworks remains contingent on political calculations rather than embedded in robust institutional structures.

Opportunities

Turkey's path towards investment-grade status, currently three notches away for both S&P and Fitch, represents a significant opportunity that could transform its financing costs and capital access. Continued implementation of orthodox policies and structural reforms could trigger further rating upgrades, with Moody's positive outlook suggesting near-term upward momentum. Achievement of investment-grade status would unlock access to a broader investor base, including institutional investors with mandates restricting speculative-grade holdings, potentially reducing borrowing costs by 100-200 basis points and generating substantial fiscal savings given Turkey's financing needs.

The government's comprehensive economic programme, targeting inflation reduction to 24% by end-2025 and single digits by 2027, provides a clear roadmap that, if successfully executed, would address one of the primary constraints on Turkey's credit rating. Success in achieving these inflation targets would enable gradual monetary policy normalisation, reducing the growth sacrifice associated with restrictive policy whilst rebuilding central bank credibility. Lower inflation would also support real income growth, enhancing social stability and reducing political pressure for policy reversals.

Geopolitical positioning offers Turkey opportunities to enhance its economic relationships and diversify its external partnerships. The country's strategic location and NATO membership provide leverage in negotiations with both Western and Eastern partners. Turkey's role in regional energy transit, particularly for natural gas flows between Russia and Europe, generates transit revenues and strategic importance. Successful navigation of complex geopolitical relationships, including potential progress on EU accession processes or enhanced trade agreements, could unlock additional foreign investment and technology transfer whilst strengthening institutional frameworks through alignment with European standards.

Structural reform implementation presents opportunities to enhance productivity and potential growth. The government's reform agenda includes labour market flexibility improvements, judicial reforms to strengthen contract enforcement, and measures to improve the business environment. Successful execution of these reforms could attract foreign direct investment, which has remained subdued relative to Turkey's potential, and support a shift towards higher value-added production. Enhanced productivity growth would enable Turkey to achieve higher sustainable growth rates without generating inflationary pressures or current account deterioration.

Threats

Policy reversal represents the most significant threat to Turkey's improved credit trajectory. The orthodox policy framework implemented since mid-2023 has generated economic costs, including slower growth and real income compression, that create political pressures for accommodation. Presidential elections scheduled before 2028 may incentivise a return to growth-supportive policies that prioritise short-term activity over medium-term stability. Any signal of wavering commitment to orthodox policies would likely trigger rapid capital outflows, currency depreciation, and rating downgrades that could reverse years of progress within months.

Global financial conditions tightening or risk-off episodes pose acute threats given Turkey's external vulnerabilities. The country's reliance on external financing to roll over short-term debt creates exposure to shifts in global liquidity conditions or investor risk appetite. A sudden stop in capital flows, whether triggered by global factors such as US monetary policy tightening or idiosyncratic concerns about Turkish policy credibility, could precipitate a balance of payments crisis. The limited foreign exchange reserve coverage relative to short-term external debt means Turkey has minimal buffers to weather sustained capital outflows without either sharp currency depreciation or emergency policy measures.

Geopolitical tensions present multifaceted threats to Turkey's economic stability. The country's complex relationships with NATO allies, particularly regarding defence procurement and regional military operations, create risks of sanctions or restricted access to Western capital markets. Simultaneously, Turkey's economic ties with Russia, including energy dependence and tourism flows, expose it to spillover effects from Western sanctions regimes and create tensions with European and American partners. Escalation of regional conflicts, particularly involving Syria, Iraq, or the Eastern Mediterranean, could trigger refugee flows, security costs, and disruption to trade routes that would strain fiscal resources and investor confidence.

Domestic political instability or social unrest could derail economic reforms and trigger capital flight. The arrest of opposition figures, as exemplified by the İmamoğlu case, demonstrates how political developments can generate immediate market reactions. More broadly, sustained economic adjustment with high inflation and compressed real wages creates social pressures that could manifest in labour unrest or political opposition to reform measures. Any perception that political considerations are overriding economic policy discipline would undermine the credibility that has been painstakingly rebuilt since 2023.

Banking sector stress represents a contingent liability that could rapidly escalate into a sovereign crisis given the interconnections between banks and the government. Whilst current capital buffers appear adequate, rapid currency depreciation or a sharp economic downturn could impair asset quality and erode bank capital. The concentration of government bond holdings on bank balance sheets means that sovereign stress would directly weaken banks, whilst any requirement for government support of troubled banks would increase public debt and potentially trigger a negative feedback loop. The memory of Turkey's 2001 banking crisis, which required fiscal costs exceeding 30% of GDP, underscores the potential magnitude of banking sector risks.

Economic Analysis

Growth Dynamics and Structural Transformation

Turkey's economic trajectory has entered a period of deliberate moderation following years of credit-fuelled expansion, with growth dynamics reflecting the necessary adjustment costs of returning to orthodox macroeconomic management. The economy expanded by 3.2% in 2024, representing a marked deceleration from the 5.1% recorded in 2023 and substantially below the double-digit growth of 11.44% achieved in 2021. This slowdown, whilst initially appearing concerning, represents a calculated recalibration rather than economic distress, as policymakers prioritise price stability and external balance over short-term output maximisation. The government's medium-term projections anticipate further moderation to 3.1% growth in 2025 before a gradual recovery to 4.2% by 2027, suggesting authorities recognise that sustainable expansion requires a foundation of macroeconomic stability rather than the artificial stimulus that characterised the pre-2023 policy framework.

The composition of growth has shifted meaningfully alongside this deceleration, with domestic demand cooling in response to tighter monetary conditions whilst external demand has provided crucial support through the tourism sector's exceptional performance. Record tourism revenues of $61.1 billion have not only bolstered growth but also played a pivotal role in financing the current account adjustment, demonstrating Turkey's capacity to leverage its geographic and cultural assets even during periods of domestic policy uncertainty. The unemployment rate's decline to 8.4% in 2024 from 9.4% in 2023 suggests the labour market has remained resilient despite the growth slowdown, though this metric warrants careful monitoring as the full effects of monetary tightening permeate the real economy with the characteristic lags associated with transmission mechanisms in emerging markets.

Inflation Dynamics and Disinflation Progress

Turkey's inflation trajectory represents perhaps the most critical dimension of its economic normalisation, with the country grappling with the legacy of years of negative real interest rates and currency depreciation that embedded inflation expectations deeply within economic behaviour. Consumer price inflation reached 58.51% in 2024 on an average basis, though this figure masks significant intra-year dynamics, with inflation peaking at 75.4% in May 2024 before declining to 38% by March 2025. This disinflation progress, whilst substantial in absolute terms, has proven slower than initially anticipated by policymakers, reflecting the persistence of second-round effects from previous currency shocks, the stickiness of inflation expectations after prolonged periods of price instability, and the ongoing pass-through from administered price adjustments that had been suppressed during the pre-election period.

The government's inflation targets of 24% by end-2025 and single digits by 2027 represent ambitious objectives that will require sustained policy discipline and favourable external conditions. Achieving these targets faces several structural headwinds, including Turkey's high degree of dollarisation in both pricing and savings behaviour, which amplifies the inflationary impact of exchange rate movements, and the prevalence of backward-looking indexation mechanisms in wage-setting and contract negotiations. The central bank's credibility, whilst improving under the orthodox policy framework, remains incomplete after years of political interference, meaning inflation expectations adjust only gradually to policy signals. Nevertheless, the direction of travel has been unambiguously positive, with core inflation measures also declining and survey-based inflation expectations showing signs of anchoring at lower levels, suggesting the disinflation process, though protracted, has gained traction.

Monetary Policy Framework and Central Bank Independence

The transformation of Turkey's monetary policy framework represents the cornerstone of the broader economic normalisation, with the central bank executing one of the most aggressive tightening cycles amongst emerging markets by raising the policy rate from 8.5% to 50% between June 2023 and March 2024. This dramatic shift restored positive real interest rates for the first time in years, with real rates reaching approximately 12% by early 2025 when measured against forward-looking inflation expectations. The magnitude and speed of this tightening reflects both the depth of the macroeconomic imbalances that had accumulated under the previous unorthodox framework and the authorities' determination to re-establish credibility with international investors and rating agencies. The central bank has maintained the 50% policy rate through early 2025 despite the ongoing disinflation, signalling a commitment to ensuring inflation returns durably to target rather than prematurely declaring victory.

The effectiveness of monetary transmission, however, remains constrained by structural features of Turkey's financial system and the legacy of unconventional policy instruments. The prevalence of foreign exchange-protected deposits, whilst reduced by two-thirds from their August 2023 peak, continues to segment the financial system and dilute the impact of lira interest rates on savings behaviour. The banking sector's heavy exposure to government securities creates a channel through which monetary tightening affects fiscal dynamics, as higher rates increase debt service costs and complicate fiscal consolidation efforts. Moreover, the credibility of the central bank's independence remains conditional on continued political support from President Erdoğan, whose previous interventions in monetary policy precipitated the crisis that necessitated the current correction. The March 2025 arrest of Istanbul Mayor Ekrem İmamoğlu, which triggered immediate market volatility and a 10% lira depreciation, serves as a stark reminder that political developments retain the capacity to undermine monetary policy effectiveness regardless of the technical soundness of the policy framework itself.

The sustainability of the current monetary stance depends critically on the inflation outlook and the authorities' willingness to tolerate the growth trade-offs associated with restrictive policy. As disinflation progresses, pressure will inevitably build for rate cuts to support economic activity, particularly given Turkey's political calendar and the government's growth-oriented rhetoric. The central bank's ability to resist premature easing and maintain a data-dependent approach will serve as a crucial test of the durability of the orthodox policy framework. International experience suggests that emerging markets that ease too quickly after initial disinflation success often experience inflation resurgence, necessitating even more costly subsequent tightening. Turkey's monetary authorities face the delicate task of calibrating the pace of eventual policy normalisation to support growth recovery whilst ensuring inflation expectations remain anchored and the hard-won credibility gains are preserved.

Political & Institutional Assessment

Turkey's political and institutional framework presents a complex landscape characterised by concentrated executive authority, weakening democratic institutions, and persistent concerns regarding policy predictability. The country operates under a presidential system introduced through the 2017 constitutional referendum, which fundamentally restructured governance by abolishing the prime ministerial position and concentrating substantial powers in the presidency. This institutional architecture has contributed to a governance environment that international observers increasingly view as constraining checks and balances, with Freedom House rating Turkey as "Not Free" with a score of 33 out of 100, reflecting significant deterioration in democratic norms and institutional independence.

The May 2023 elections marked a critical juncture for Turkey's economic policy trajectory, resulting in President Erdoğan's re-election alongside a decisive pivot towards orthodox economic management. The appointment of Mehmet Şimşek as Finance Minister signalled this policy reversal, with the former Merrill Lynch economist bringing credibility to Turkey's commitment to conventional monetary and fiscal frameworks. This shift represented a stark departure from the unorthodox policies that had characterised the preceding period, during which political interference in central bank operations had severely undermined institutional credibility and contributed to currency instability and accelerating inflation.

Despite the positive policy recalibration, concerns regarding institutional independence persist, particularly with respect to the Central Bank of the Republic of Turkey. The central bank's history of frequent leadership changes—with four governors appointed between 2019 and 2021 alone—has left lasting scars on its credibility. Whilst the current policy stance demonstrates greater autonomy, with the central bank maintaining its policy rate at 50 per cent despite political pressure for easing, the institutional memory of past interference continues to weigh on investor confidence and constrains the country's sovereign credit assessment.

The March 2025 arrest of Istanbul Mayor Ekrem İmamoğlu exemplifies the ongoing political risks that can rapidly translate into market volatility and economic instability. İmamoğlu, widely regarded as the most prominent opposition figure and potential presidential challenger, faced detention on charges that international observers characterised as politically motivated. The immediate market reaction—a 10 per cent depreciation of the Turkish lira—underscores how political developments can swiftly undermine economic stability gains. This incident highlights the fragility of investor confidence and the premium that markets assign to political risk in Turkey, even as economic fundamentals show improvement.

The judiciary's independence remains a significant concern for international credit assessors, with the İmamoğlu case reinforcing perceptions of selective prosecution and politically influenced legal proceedings. The broader pattern of judicial actions against opposition politicians, journalists, and civil society organisations has contributed to Turkey's declining scores on governance indicators. These institutional weaknesses create uncertainty around property rights, contract enforcement, and the predictability of the business environment—factors that directly influence foreign investment decisions and Turkey's cost of capital.

Turkey's geopolitical positioning adds another layer of complexity to its institutional assessment. The country maintains a delicate balance between its NATO membership and increasingly independent foreign policy positions, including its relationship with Russia and its role in regional conflicts. Whilst this strategic autonomy provides certain economic opportunities, such as Turkey's position as an energy transit hub, it also introduces unpredictability that can complicate relationships with Western allies and international financial institutions. The country's blocking of Swedish NATO accession until March 2024 and its nuanced stance on the Russia-Ukraine conflict illustrate this balancing act.

Corruption perceptions represent an additional institutional challenge, with Turkey ranking poorly on international transparency indices relative to similarly rated sovereigns. The concentration of economic power amongst entities with close ties to the government, combined with concerns about procurement transparency and regulatory capture, undermines the efficiency of public spending and creates contingent liabilities that may not be fully reflected in official fiscal accounts. These governance weaknesses contribute to a risk premium in Turkey's borrowing costs and constrain the country's ability to attract sustained foreign direct investment beyond short-term portfolio flows.

The path towards strengthening Turkey's institutional framework requires sustained commitment to judicial independence, central bank autonomy, and transparent governance practices. Credit rating agencies have explicitly identified improvements in these areas as prerequisites for further upgrades towards investment grade status. However, the entrenched nature of Turkey's presidential system and the political incentives favouring centralised control suggest that meaningful institutional reform will require either significant political will from the current leadership or a fundamental shift in the country's political landscape. Until such reforms materialise, institutional weaknesses will continue to constrain Turkey's sovereign credit profile, regardless of improvements in macroeconomic indicators.

Banking Sector & Financial Stability

Turkey's banking sector has demonstrated notable resilience throughout the period of economic adjustment, maintaining adequate capital buffers with capital adequacy ratios ranging between 17.7% and 18.3%, comfortably above the regulatory minimum of 8% and the Basel III benchmark of 10.5%. This capitalisation provides an important cushion against potential shocks as the sector navigates the transition from unorthodox to orthodox monetary policy. However, the sector's structural characteristics reveal vulnerabilities that warrant careful monitoring, particularly regarding sovereign exposure and the lingering effects of the FX-protected deposit scheme introduced during the period of currency instability.

The most significant structural concern centres on the banking sector's heavy exposure to sovereign risk through substantial holdings of government bonds. This concentration creates a potentially destabilising feedback loop between fiscal and financial stability, whereby deterioration in sovereign creditworthiness would directly impair bank balance sheets, which could in turn constrain credit provision to the economy and further weaken fiscal dynamics. The sovereign-bank nexus represents a classic emerging market vulnerability that limits the sector's ability to serve as a shock absorber during periods of stress. This interconnection became particularly evident during the March 2025 political turbulence surrounding the arrest of Istanbul Mayor Ekrem İmamoğlu, when market volatility simultaneously affected both sovereign spreads and banking sector valuations.

The FX-protected deposit scheme, whilst successfully stabilising the lira during its peak crisis period, has left a complex legacy for the banking sector. Although these deposits have been reduced by two-thirds from their August 2023 peak, the remaining stock continues to represent a contingent liability that constrains monetary policy flexibility and maintains pressure on foreign exchange reserves. The unwinding of this scheme has proceeded more gradually than initially anticipated, reflecting both depositor preferences and the authorities' cautious approach to avoiding renewed currency instability. The scheme's gradual phase-out has contributed to the improvement in net foreign exchange reserves to $41 billion, yet the banking sector remains vulnerable to renewed currency pressures should depositor confidence waver.

Profitability dynamics within the Turkish banking sector have been heavily influenced by the dramatic shift in monetary policy stance. The central bank's aggressive tightening cycle, which raised policy rates from 8.5% to 50% between June 2023 and March 2024, has fundamentally altered the operating environment for banks. Net interest margins have expanded significantly as lending rates adjusted more rapidly than deposit costs, though this windfall has been partially offset by higher provisioning requirements as some borrowers struggle with elevated financing costs. The sector's ability to maintain profitability whilst absorbing credit losses will prove critical to sustaining confidence during the ongoing economic adjustment period.

Asset quality indicators warrant close attention as the effects of monetary tightening work through the economy. Non-performing loan ratios have remained contained thus far, reflecting both the relatively short period since policy normalisation began and the forbearance measures that remain in place for certain borrower categories. However, the full impact of 50% policy rates on borrower debt servicing capacity has yet to materialise completely, particularly for small and medium-sized enterprises that lack natural hedges against currency depreciation and face compressed margins in a slowing economy. The projected moderation in GDP growth to 3.1% in 2025 will test the resilience of bank loan portfolios, particularly in sectors exposed to domestic demand.

Liquidity management has emerged as a critical competency for Turkish banks navigating the volatile environment. The sector maintains adequate liquidity coverage ratios, yet the composition of funding sources remains skewed towards shorter maturities, reflecting depositor caution and limited access to long-term wholesale funding markets. Foreign currency liquidity represents a particular challenge, as banks must balance their foreign exchange positions whilst supporting trade finance and corporate hedging needs. The central bank's efforts to rebuild gross foreign exchange reserves, which stood at $83.5 billion against short-term external debt of $180.5 billion, provide only partial comfort given the banking sector's role as an intermediary for the country's substantial external financing requirements.

The regulatory environment has strengthened considerably under the orthodox policy framework, with supervisory authorities demonstrating greater willingness to enforce prudential standards and limit regulatory forbearance. This shift represents a positive development for long-term financial stability, though it has required banks to adjust business models that had become accustomed to more accommodative oversight. Enhanced macroprudential measures, including tighter limits on foreign exchange exposure and stricter loan-to-value ratios for certain lending categories, have contributed to more sustainable credit growth dynamics. The authorities' commitment to maintaining these standards will prove essential to preventing the re-emergence of the imbalances that characterised the pre-2023 period.

Looking forward, the Turkish banking sector's trajectory depends critically on the broader success of economic stabilisation efforts. Continued disinflation progress towards the government's target of 24% by end-2025 would allow for gradual monetary easing, relieving pressure on borrowers whilst maintaining positive real interest rates. The sector's ability to support economic growth whilst managing legacy vulnerabilities will significantly influence Turkey's path towards investment grade status. Strengthening the sovereign-bank nexus through fiscal consolidation and diversifying bank funding sources beyond domestic deposits represent key priorities for enhancing financial stability and reducing systemic vulnerabilities that currently constrain the sector's credit profile.

Outlook & Scenarios

Short-Term Outlook (12 months)

Turkey's near-term credit trajectory through early 2027 hinges critically on the authorities' ability to maintain orthodox policy discipline whilst navigating heightened political uncertainty. The government's inflation target of 24% by end-2025 appears increasingly ambitious given the persistent stickiness in core inflation and the lira's continued volatility, as evidenced by the 10% depreciation following the March 2025 arrest of Istanbul Mayor Ekrem İmamoğlu. This incident underscores the fragility of market confidence and the potential for political developments to rapidly undermine macroeconomic stability gains. The central bank faces a delicate balancing act in maintaining its 50% policy rate whilst managing the economic slowdown, with GDP growth projected to moderate to 3.1% in 2025 as the effects of monetary tightening permeate through the economy.

The external position remains a focal point of vulnerability despite the remarkable improvement in the current account deficit. Foreign exchange reserves of $83.5 billion provide insufficient coverage against short-term external debt of $180.5 billion, leaving Turkey exposed to potential capital flow reversals should global risk sentiment deteriorate or domestic political tensions escalate. The banking sector's heavy exposure to sovereign risk through government bond holdings creates a concerning feedback loop, whereby any deterioration in fiscal metrics or market confidence could rapidly transmit to financial sector stability. However, the sector's adequate capital buffers with an average capital adequacy ratio between 17.7% and 18.3% provide some cushion against potential shocks.

Fiscal dynamics present an additional challenge, with the deficit remaining elevated at 5.2% of GDP despite the low debt-to-GDP ratio of 24.7%. The government's commitment to fiscal discipline will be tested by social spending pressures and the economic costs of monetary tightening, particularly as unemployment, whilst declining to 8.4%, remains a politically sensitive issue. The continuation of Finance Minister Mehmet Şimşek's orthodox policy framework represents the single most important factor for near-term stability, though the risk of policy reversal cannot be entirely discounted given Turkey's history of abrupt shifts in economic management.

Medium-Term Outlook (1-3 years)

Over the medium term, Turkey's credit profile evolution depends fundamentally on three interconnected factors: sustained policy orthodoxy, structural reform implementation, and the strengthening of institutional frameworks. The government's ambitious target of reducing inflation to single digits by 2027 requires not only continued monetary discipline but also complementary fiscal consolidation and productivity-enhancing reforms. The projected GDP growth recovery to 4.2% by 2027 assumes successful navigation of the current adjustment period and restoration of investor confidence sufficient to support private sector investment and capital inflows.

The path towards investment grade status, currently three notches away for both S&P and Fitch, necessitates addressing fundamental weaknesses in governance and institutional quality. Turkey's Freedom House rating as "Not Free" with a score of 33/100 represents a significant constraint on creditworthiness, as weak democratic institutions increase policy unpredictability and reduce the credibility of long-term reform commitments. The persistent concern regarding political interference in economic institutions, exemplified by the İmamoğlu arrest and its market impact, highlights the need for strengthening judicial independence and the rule of law as prerequisites for sustainable credit improvement.

External vulnerabilities require structural solutions beyond cyclical current account improvements. Whilst the reduction in the deficit to 0.8% of GDP represents substantial progress, Turkey's external financing needs remain considerable given the maturity profile of external debt. Building foreign exchange reserves to more comfortable levels and extending the maturity structure of external obligations will be essential for reducing vulnerability to external shocks. The reduction of FX-protected deposits by two-thirds from their August 2023 peak demonstrates progress in de-dollarisation, but further efforts are needed to restore confidence in lira-denominated assets and reduce currency substitution.

The banking sector's evolution will prove critical for medium-term stability and growth. Whilst current capital buffers appear adequate, the sector's heavy sovereign exposure creates concentration risk that could amplify any fiscal stress. Diversifying bank balance sheets, strengthening asset quality monitoring, and ensuring that credit growth supports productive investment rather than speculative activity will be essential for financial sector resilience. The sector's ability to intermediate capital efficiently whilst managing risks will directly influence Turkey's growth potential and external financing capacity.

Rating Scenarios

Upside Scenario (Upgrade Probability: Moderate): An upgrade trajectory towards investment grade would require Turkey to demonstrate sustained commitment to orthodox policies over an extended period, with inflation declining towards the government's single-digit target by 2027 and the central bank maintaining operational independence. Moody's positive outlook suggests potential for a near-term upgrade to Ba3, which would align Turkey's rating across the three major agencies at the BB-/Ba3 equivalent level. Further progression would necessitate fiscal consolidation that reduces the deficit below 3% of GDP whilst maintaining the low debt-to-GDP ratio, alongside continued current account improvement supported by structural export competitiveness rather than cyclical factors alone. Critically, meaningful progress on governance indicators, including strengthening of democratic institutions, judicial independence, and reduced political interference in economic policymaking, would be required to convince rating agencies of the sustainability of reforms. A successful navigation of the 2028 electoral cycle without policy reversal would provide strong evidence of institutional entrenchment of orthodox policies.

Baseline Scenario (Most Likely): The most probable scenario involves Turkey maintaining its current rating levels with gradual progress towards the lower end of investment grade over a three-to-five-year horizon. This assumes continued implementation of orthodox monetary policy with gradual disinflation to the low-20s percentage range by end-2026, though missing the government's more ambitious targets. GDP growth would stabilise in the 3-4% range, sufficient to support employment gains but below the economy's historical potential. The current account deficit would likely widen modestly from current levels to 1.5-2.0% of GDP as domestic demand recovers and import compression effects fade, though remaining manageable given improved tourism revenues and potential energy transit benefits. Political tensions would persist, creating periodic market volatility, but without triggering a fundamental policy reversal. Under this scenario, S&P and Fitch would maintain stable outlooks whilst Moody's might deliver its anticipated upgrade to Ba3, creating a narrow rating band across agencies. Progress towards investment grade would remain contingent on demonstrating multi-year policy consistency through electoral cycles.

Downside Scenario (Downgrade Risk: Low-to-Moderate): A negative rating action would most likely stem from a reversal of orthodox policies, potentially triggered by political pressures as the economic costs of disinflation become more acute or as electoral considerations dominate policymaking. Key warning signals would include premature monetary easing before inflation is firmly controlled, renewed central bank interference, or fiscal loosening that undermines debt sustainability. External shocks, such as a sharp deterioration in global risk appetite, geopolitical tensions affecting Turkey's regional position, or a sudden stop in capital flows, could expose the vulnerability created by low foreign exchange reserve coverage of short-term external debt. A renewed widening of the current account deficit beyond 3% of GDP, particularly if financed through short-term debt rather than foreign direct investment, would raise sustainability concerns. Banking sector stress, potentially triggered by rapid lira depreciation affecting borrowers' repayment capacity or sovereign-bank linkages amplifying fiscal pressures, represents an additional downside risk. Under this scenario, rating agencies would likely move outlooks to negative before implementing downgrades, with Moody's positive outlook being the first casualty of deteriorating conditions.

Conclusion

Turkey's sovereign credit profile stands at a critical juncture, reflecting both the substantial progress achieved through orthodox policy implementation and the persistent structural vulnerabilities that continue to constrain its creditworthiness. The country's remarkable achievement as the sole sovereign to receive upgrades from all three major rating agencies in 2024, culminating in BB- ratings from S&P and Fitch and a B1 rating with positive outlook from Moody's, underscores the credibility gained through Finance Minister Mehmet Şimşek's decisive policy pivot. The aggressive monetary tightening cycle, which elevated policy rates from 8.5% to 50% between June 2023 and March 2024, has begun to yield tangible results, with inflation declining from its 75% peak in May 2024 to 38% by March 2025, whilst the current account deficit has narrowed dramatically from 3.6% to 0.8% of GDP.

Nevertheless, Turkey's path towards investment grade status, currently three notches distant for both S&P and Fitch, remains fraught with considerable challenges that temper the positive momentum. The March 2025 arrest of Istanbul Mayor Ekrem İmamoğlu, which precipitated immediate market volatility and a 10% lira depreciation, serves as a stark reminder of the political risks that continue to overshadow economic fundamentals. The persistence of institutional weaknesses, reflected in Turkey's Freedom House rating of 33/100 and classification as "Not Free", raises fundamental questions about the sustainability of orthodox policies in an environment where political considerations have historically trumped economic rationality. The banking sector's heavy exposure to sovereign risk through substantial government bond holdings creates a potentially destabilising feedback loop between fiscal and financial stability, whilst foreign exchange reserves of $83.5 billion remain inadequate relative to short-term external debt of $180.5 billion, leaving Turkey vulnerable to sudden shifts in investor sentiment.

The government's medium-term targets of 24% inflation by end-2025 and single-digit inflation by 2027, alongside GDP growth projections of 3.1% in 2025 recovering to 4.2% by 2027, appear achievable provided policy discipline is maintained. However, the realisation of these objectives hinges critically on factors that extend beyond purely economic management. Sustained commitment to orthodox monetary policy, continued structural reforms to enhance competitiveness and productivity, strengthening of democratic institutions and the rule of law, and successful navigation of Turkey's complex geopolitical positioning between NATO allies and regional powers will all prove determinative. The country's ability to maintain the delicate balance between economic stabilisation and political pressures, whilst managing its strategic relationships in an increasingly multipolar world, will ultimately define whether Turkey can consolidate recent gains and progress towards investment grade status or risk reverting to the policy inconsistency that has characterised much of the past decade.