SouthKorea

Executive Summary

South Korea's AA-category sovereign credit profile reflects robust institutional frameworks and strong external buffers that have demonstrated resilience through significant political turbulence, balanced against structural vulnerabilities in household indebtedness and demographic decline. The December 2024 martial law declaration and subsequent presidential impeachment represented the most severe constitutional crisis since democratisation, yet the National Assembly's swift rejection of emergency measures and orderly transition to the Lee Jae-myung administration in June 2025 validated the strength of democratic institutions. All three major rating agencies maintained stable outlooks throughout the crisis, citing effective crisis management capabilities and sound economic fundamentals. Korea's external position remains exceptionally strong, with foreign exchange reserves of $415.6 billion and a current account surplus of $99 billion in 2024, underpinned by technological leadership in semiconductors where Korean firms command 60.5% of the global memory market share. The banking system maintains robust capital adequacy at 16.9% with historically low non-performing loan ratios of 0.4%, though concentrated exposures in real estate project finance totalling KRW 132.2 trillion within non-bank financial institutions warrant continued regulatory vigilance.

The economic outlook for 2025-2026 faces material headwinds from external trade pressures and subdued domestic demand. The July 2025 agreement with the United States imposing 15% tariffs on Korean goods—alongside Korea's $350 billion US investment commitment—has prompted the Bank of Korea to revise 2025 growth projections downward to a range of 0.9-2.0%, substantially below potential. Semiconductor exports, which drove the 2024 recovery and contributed to 2.2% GDP growth, face uncertain demand conditions amid global technology cycle volatility and intensifying US-China technological competition that complicates supply chain positioning for Korean manufacturers. Domestic consumption remains constrained by household debt burdens at 91.7% of GDP—the second-highest ratio globally—limiting monetary policy transmission despite rate cuts to 3.25%. The construction sector continues to contract, with real estate project finance exposures creating potential financial stability risks should property market corrections deepen. Inflation has moderated to 2.3% in 2024, approaching the central bank's 2% target and providing scope for accommodative monetary policy, though currency volatility with the won reaching 1,400 per US dollar complicates policy calibration.

Fiscal dynamics reflect cyclical pressures and structural spending commitments, with the deficit widening to 4.1% of GDP in 2024 from corporate tax shortfalls, whilst government debt approaches 50% of GDP. The new administration's policy agenda emphasising expanded social spending to address demographic challenges and income inequality introduces upward pressure on medium-term fiscal trajectories, though debt levels remain moderate by international standards and financing conditions benefit from deep domestic capital markets. Demographic headwinds intensify, with the world's lowest fertility rate necessitating structural reforms to labour markets, pension systems, and immigration policies to sustain potential growth and fiscal sustainability. The transition to the Lee administration provides political stability after months of uncertainty, yet policy shifts toward potential foreign policy realignment and expanded state intervention in strategic industries introduce execution risks. Korea's credit strengths—including technological competitiveness, strong external buffers, and demonstrated institutional resilience—provide substantial capacity to navigate near-term challenges, though successful management of household debt vulnerabilities, restoration of domestic demand growth, and strategic adaptation to shifting geopolitical and trade environments will prove critical to maintaining the current rating level over the medium term.

Ratings Summary

South Korea maintains strong investment-grade sovereign credit ratings across all three major international rating agencies, reflecting the country's robust economic fundamentals and institutional resilience despite significant political turbulence. The ratings have demonstrated remarkable stability through the December 2024 martial law crisis and subsequent presidential impeachment, with all agencies affirming their assessments and citing effective democratic response mechanisms, strong external balance sheets, and sound policy frameworks. S&P Global reaffirmed its AA rating with Stable outlook on 15 April 2025, explicitly noting that whilst political turbulence "hurt confidence in political stability," Korea's economic fundamentals remained intact, supported by resilient export performance, prudent fiscal management, and adequate foreign exchange reserves. Moody's has maintained its Aa2 rating with Stable outlook since December 2015, emphasising the country's strong institutional framework, economic resilience, and sound policy environment as key supporting factors. Fitch Ratings holds Korea at AA- with Stable outlook, last reviewed on 6 March 2024, highlighting economic resilience, export recovery, and effective crisis management capabilities. During the political crisis, Fitch published special commentary stating "Korea's Credit Fundamentals Still Intact Amid Political Volatility" whilst cautioning that prolonged political instability could pressure the ratings. Common themes across all three agencies include Korea's strong international competitiveness in key export sectors, particularly semiconductors, robust institutional frameworks that withstood political stress, sound external balance sheets with foreign reserves exceeding $415 billion, and demonstrated financial market stabilisation capabilities during periods of volatility.

| Rating Agency | Current Rating | Outlook | Last Action Date |

|---|---|---|---|

| S&P Global | AA | Stable | 15 April 2025 |

| Moody's | Aa2 | Stable | Maintained since December 2015 |

| Fitch Ratings | AA- | Stable | 6 March 2024 |

Economic Indicators

| Indicator | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 Proj |

|---|---|---|---|---|---|---|

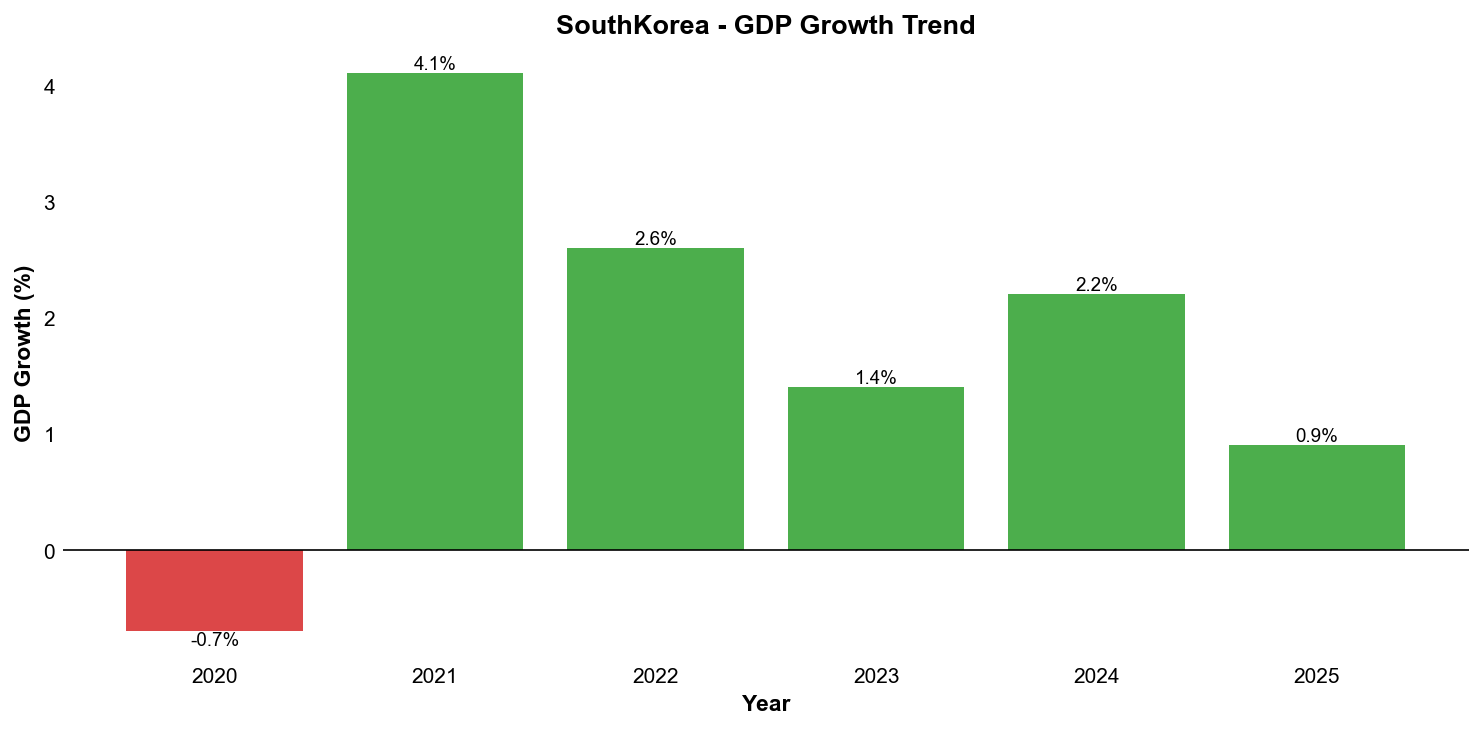

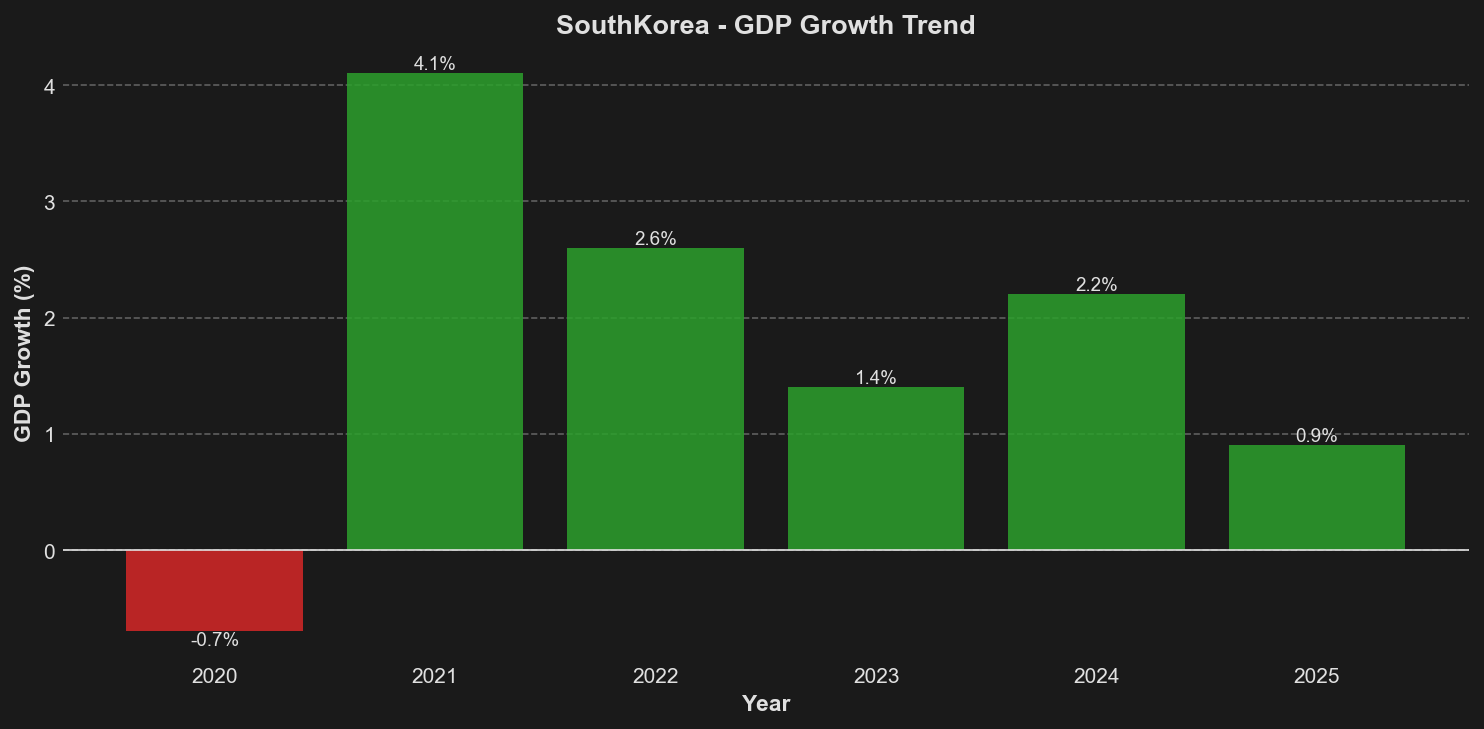

| Real GDP Growth (%) | -0.7 | 4.1 | 2.6 | 1.4 | 2.2 | 0.9-2.0 |

| Inflation (CPI %) | 0.5 | 2.5 | 5.1 | 3.6 | 2.3 | 2.0 |

| Government Debt/GDP (%) | 41.2 | 43.5 | 45.8 | 48.4 | 47.4 | ~50 |

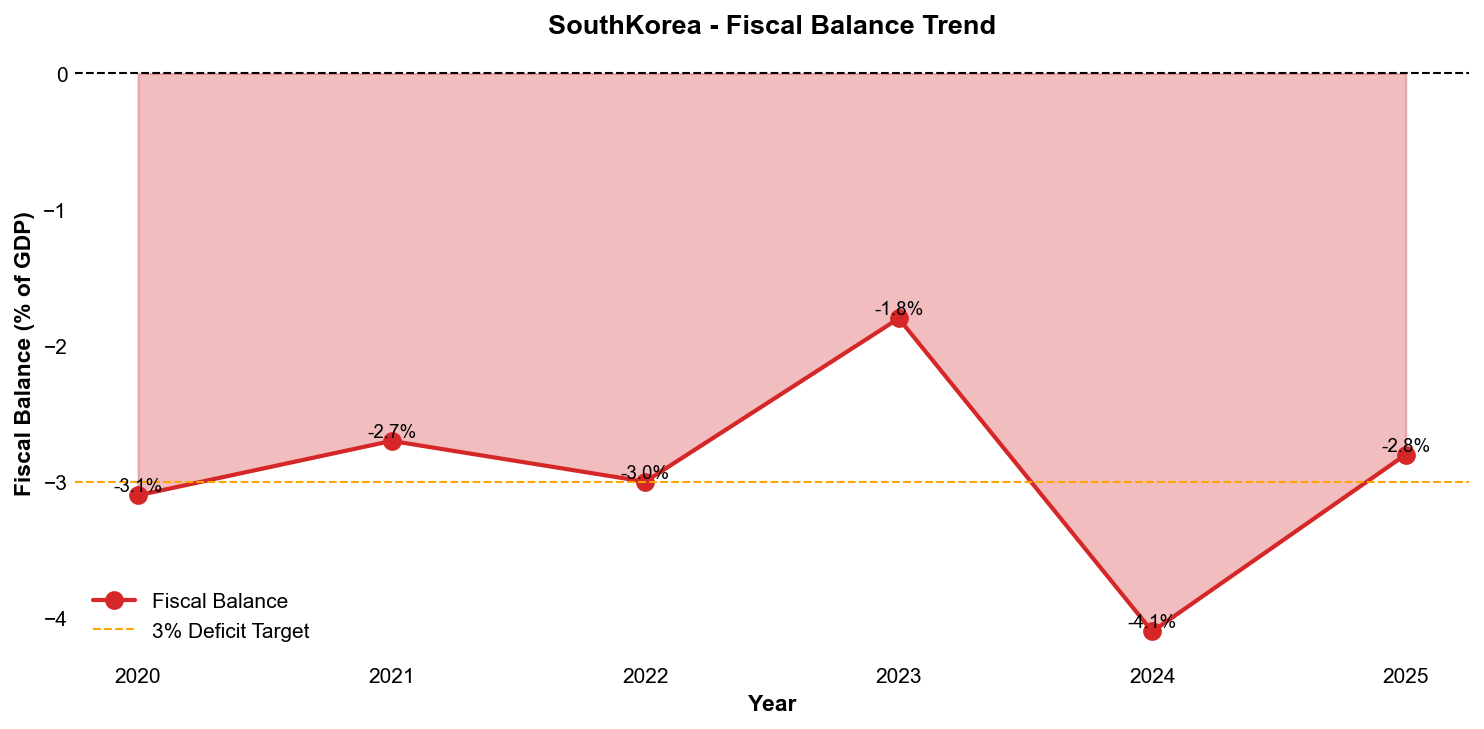

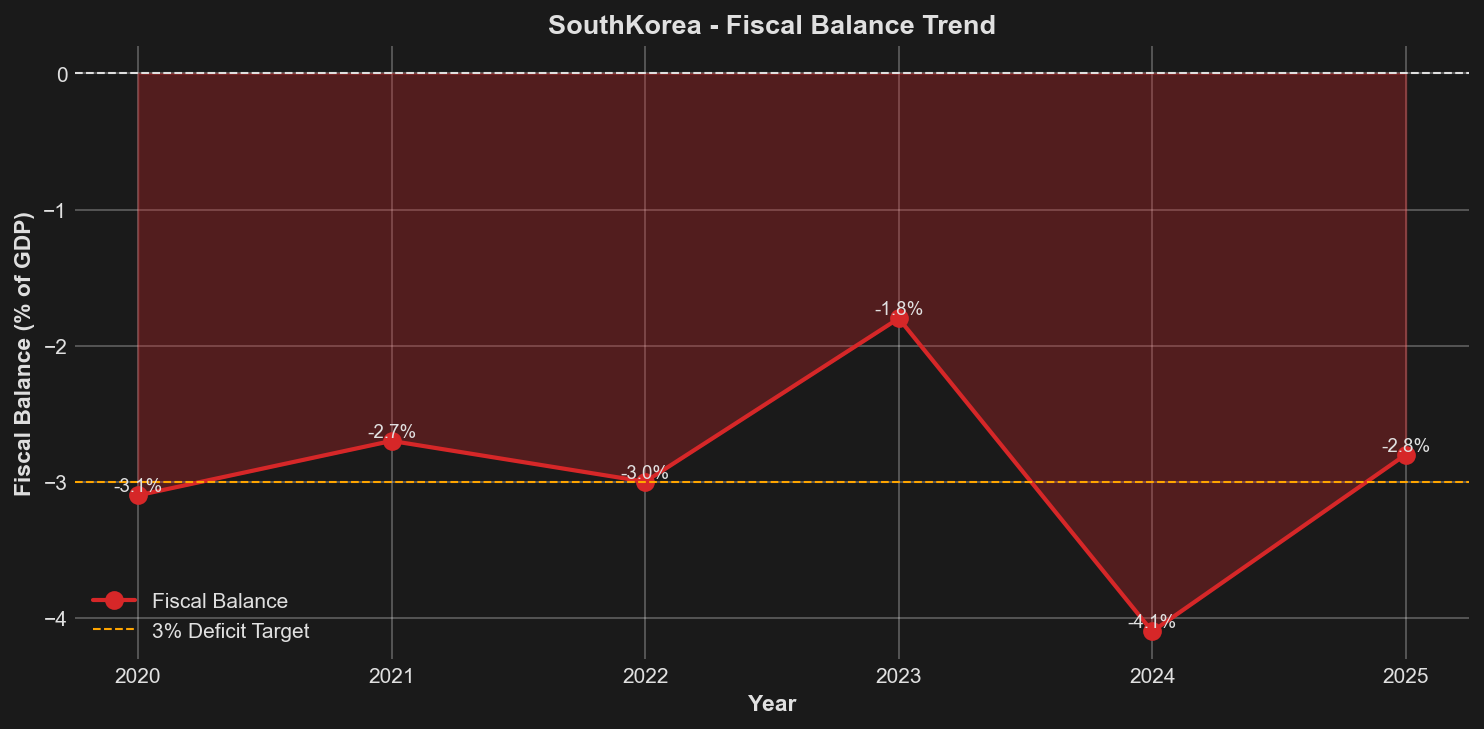

| Fiscal Balance/GDP (%) | -3.1 | -2.7 | -3.0 | -1.8 | -4.1 | -2.8 |

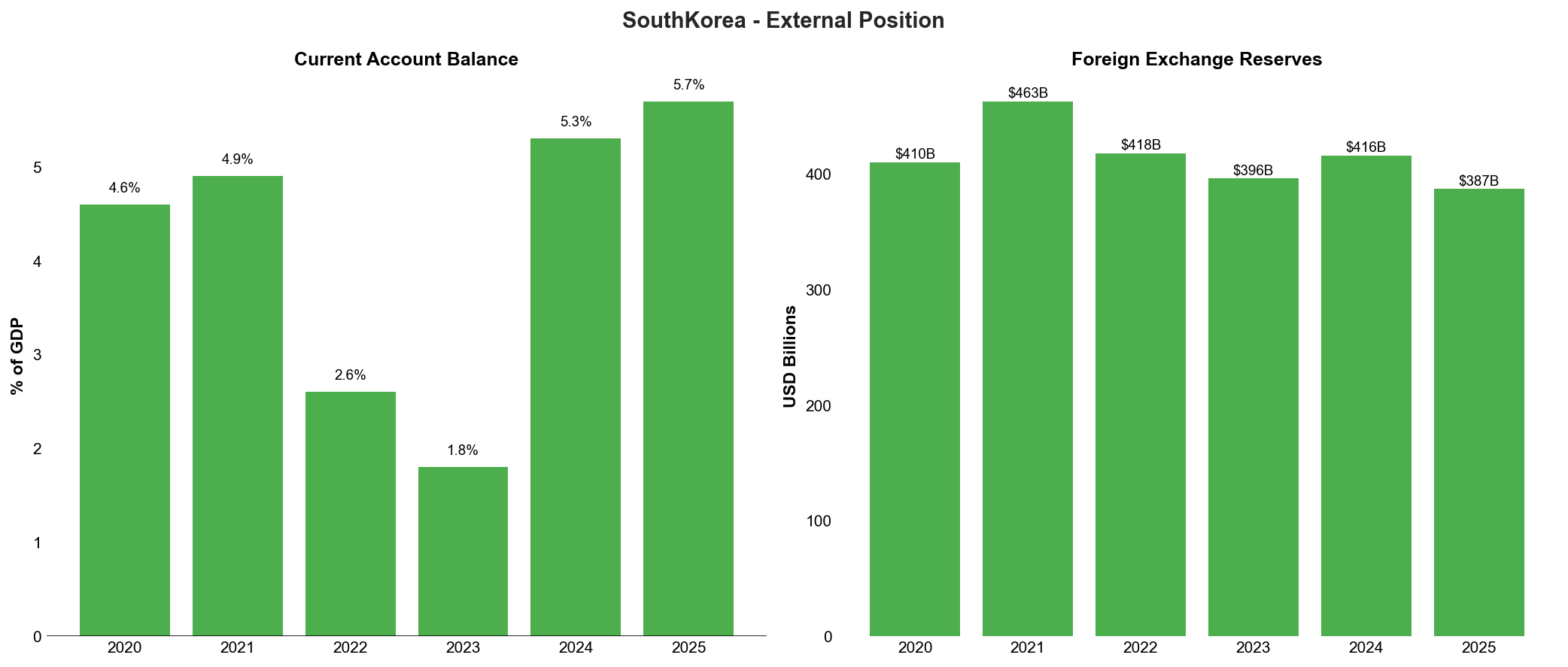

| Current Account/GDP (%) | 4.6 | 4.9 | 2.6 | 1.8 | 5.3 | 5.7 |

| FX Reserves (USD bn) | 410 | 463 | 418 | 396 | 416 | 387-416 |

| Exchange Rate (KRW/USD) | 1,180 | 1,144 | 1,292 | 1,305 | 1,400 | High volatility |

South Korea's economic trajectory demonstrates resilience through multiple external shocks, though growth momentum has moderated significantly from the post-pandemic rebound. Following the sharp contraction of 0.7% in 2020 during the initial COVID-19 impact, the economy staged a robust recovery with 4.1% growth in 2021, supported by aggressive fiscal stimulus and strong export performance. However, subsequent years have witnessed a deceleration, with growth slowing to 2.6% in 2022 amid global monetary tightening and supply chain disruptions, before further weakening to 1.4% in 2023 as domestic demand faltered and the construction sector contracted. The modest improvement to 2.2% in 2024 was driven primarily by a semiconductor-driven export resurgence, though this remained below potential output levels due to persistent weakness in domestic consumption and investment.

The 2025 growth outlook has deteriorated markedly, with projections ranging from 0.9% to 2.0% depending on the severity of US tariff impacts. The July 2025 bilateral agreement imposing 15% tariffs on Korean goods, whilst representing a reduction from the initially threatened 25% rate, nonetheless creates significant economic drag on the export-dependent economy. The Bank of Korea revised its 2025 growth projections downward from 1.5% following the tariff announcement, with the lower bound of 0.9% reflecting scenarios where trade tensions escalate further or global demand weakens more substantially than anticipated. This growth deceleration occurs against a backdrop of structural headwinds including demographic decline, elevated household debt constraining consumption, and ongoing adjustments in the real estate sector.

Inflationary pressures, which surged to 5.1% in 2022 driven by energy price shocks and supply chain bottlenecks, have moderated substantially toward the Bank of Korea's 2% target. Consumer price inflation declined to 3.6% in 2023 and further to 2.3% in 2024, creating space for monetary policy easing. The central bank reduced its policy rate to 3.25% as inflation dynamics normalised, though policymakers remain vigilant regarding potential second-round effects from won depreciation and imported inflation. The 2025 inflation projection of 2.0% suggests continued price stability, though tariff-related supply chain adjustments and exchange rate volatility present upside risks to this baseline scenario.

The fiscal position has deteriorated from the relatively contained deficits of 2021-2023, with the fiscal balance reaching -4.1% of GDP in 2024, significantly wider than the budgeted 3.6%. This shortfall primarily reflects corporate tax revenue underperformance as profit margins compressed in key export sectors and domestic economic activity remained subdued. Government debt has risen steadily from 41.2% of GDP in 2020 to 47.4% in 2024, with projections indicating a breach of the 50% threshold in 2025. Whilst this debt level remains moderate by international standards and well below advanced economy averages, the trajectory warrants monitoring, particularly given the new administration's commitment to expanded social spending programmes and the potential need for counter-cyclical fiscal support if growth weakens further.

South Korea's external position remains a fundamental credit strength, with the current account surplus widening substantially to 5.3% of GDP in 2024 from 1.8% in 2023, driven by record semiconductor exports and improved terms of trade. The surplus is projected to expand further to 5.7% of GDP in 2025, providing a crucial buffer against external shocks and supporting the won despite political volatility. Foreign exchange reserves stood at $415.6 billion in 2024, representing adequate coverage of short-term external debt and import requirements. However, reserve projections for 2025 show potential volatility, with estimates ranging from $387 billion to $416 billion depending on intervention requirements to stabilise the exchange rate amid heightened market uncertainty.

The Korean won experienced significant depreciation pressure, weakening from 1,305 per US dollar in 2023 to 1,400 in 2024, reflecting both domestic political turbulence and broader US dollar strength. Exchange rate volatility is expected to remain elevated in 2025 as markets digest the implications of US tariff policies, potential shifts in the new administration's foreign policy orientation, and ongoing US-China technological competition. The Bank of Korea has demonstrated willingness to intervene in foreign exchange markets to prevent disorderly movements, though sustained one-way pressure could deplete reserves more rapidly than baseline projections suggest. The exchange rate serves as a key adjustment mechanism for the export-oriented economy, though excessive volatility poses risks to inflation expectations and corporate balance sheets with unhedged foreign currency exposures.

Net Foreign Assets & External Position

South Korea's external position represents a fundamental pillar of sovereign creditworthiness, characterised by substantial net creditor status, robust foreign exchange reserves, and persistent current account surpluses that provide critical resilience against external shocks. The country's net international investment position (NIIP) stood at approximately 30% of GDP as of end-2024, reflecting decades of current account surpluses and prudent external debt management. This strong external balance sheet proved instrumental during the December 2024 political crisis, enabling authorities to stabilise financial markets without depleting reserves or requiring external assistance. The external position provides significant policy flexibility as Korea navigates heightened trade tensions with the United States and manages the economic implications of the July 2025 tariff agreement.

Foreign exchange reserves totalled USD 415.6 billion at end-2024, representing adequate coverage against external financing needs and short-term vulnerabilities. Whilst reserves declined from the 2021 peak of USD 463 billion due to foreign exchange intervention during periods of won weakness, the current level maintains comfortable coverage ratios. Reserves represent approximately 8.5 months of goods and services imports and exceed short-term external debt by a substantial margin, providing robust protection against sudden capital flow reversals. The Bank of Korea's projections indicate reserves may decline to a range of USD 387-416 billion during 2025, reflecting potential intervention to manage exchange rate volatility associated with US tariff implementation and global trade policy uncertainty. The won traded at approximately 1,400 per US dollar at end-2024, having depreciated from 1,305 at end-2023, with authorities signalling tolerance for greater exchange rate flexibility whilst maintaining readiness to address disorderly market conditions.

The current account surplus reached USD 99 billion in 2024, equivalent to 5.3% of GDP, marking a substantial strengthening from 1.8% in 2023. This improvement primarily reflected record semiconductor exports as the global memory chip cycle recovered, with Korea's dominant position in DRAM and NAND flash memory markets driving export revenues. The trade balance benefited from both higher semiconductor prices and volumes, whilst energy import costs moderated from 2022 peaks. Projections indicate the current account surplus will expand further to 5.7% of GDP in 2025, though this forecast predates full assessment of US tariff impacts. The July 2025 agreement imposing 15% tariffs on Korean goods—alongside Korea's USD 350 billion US investment commitment—introduces significant uncertainty regarding export performance and current account dynamics. The Bank of Korea's revised growth projections incorporating tariff effects suggest potential compression of the trade surplus, though the magnitude depends on won depreciation, demand elasticity, and supply chain adjustments.

External Debt Dynamics

South Korea's external debt profile reflects moderate levels with favourable composition weighted toward long-term maturities and substantial foreign currency assets offsetting liabilities. Total external debt stood at approximately 35% of GDP at end-2024, with long-term debt comprising roughly 70% of the total. The banking sector holds significant external liabilities related to trade finance and foreign currency funding operations, though these are largely matched by foreign currency assets, limiting net exposure. Corporate external debt remains manageable, concentrated in large conglomerates with substantial export revenues providing natural hedges. The government maintains minimal foreign currency debt, with sovereign issuance primarily serving to establish benchmark curves rather than financing needs.

Short-term external debt by remaining maturity represents the primary vulnerability metric, though coverage by foreign exchange reserves remains comfortable at approximately 2.5 times. The maturity structure has lengthened since the Asian Financial Crisis, reflecting improved market access and creditor confidence in Korean obligors. External debt service ratios remain low relative to export earnings, indicating minimal refinancing stress under baseline scenarios. However, the concentration of external liabilities in the banking sector creates potential vulnerabilities if global financial conditions tighten sharply or if Korean banks face reduced access to international wholesale funding markets.

Structural Vulnerabilities and Risk Factors

Despite the strong headline external position, several structural factors warrant careful monitoring. The concentration of export revenues in semiconductors—which accounted for approximately 20% of total exports in 2024—creates vulnerability to cyclical downturns in global chip demand and technological disruption. Korea's 60.5% share of the global memory market represents both competitive strength and concentration risk, with pricing volatility in commodity memory chips directly impacting export revenues and current account performance. The intensifying US-China technological competition poses strategic challenges, as Korea maintains deep economic integration with China whilst relying on US technology and security partnerships.

The won's exchange rate volatility has increased substantially, with the currency experiencing sharp depreciation during periods of global risk aversion and domestic political uncertainty. The December 2024 martial law crisis triggered significant capital outflows, with foreign investors reducing holdings of Korean equities and bonds. Whilst authorities successfully stabilised markets through foreign exchange intervention and liquidity provision, the episode demonstrated sensitivity to confidence shocks. The won's depreciation to 1,400 per US dollar by end-2024 reflected both domestic political factors and broader US dollar strength, with technical analysts identifying potential for further weakness if trade tensions escalate or if domestic demand remains subdued.

The external financing requirements of non-bank financial institutions represent an emerging vulnerability, particularly for institutions with significant real estate project finance exposures. Whilst banks maintain strong foreign currency liquidity positions, some non-bank lenders have relied on external funding to support domestic lending growth. The KRW 132.2 trillion in real estate project finance exposures across the financial system includes foreign currency-denominated loans, creating potential currency mismatches if property developers face cash flow difficulties. Regulatory authorities have enhanced monitoring of foreign currency liquidity at non-bank institutions, though systemic risks could emerge if property market stress intensifies.

Policy Framework and Reserve Management

The Bank of Korea maintains a comprehensive framework for external stability, encompassing foreign exchange intervention, macroprudential measures targeting foreign currency liquidity, and bilateral currency swap arrangements. Korea maintains swap lines with major central banks including the Federal Reserve, People's Bank of China, and regional partners through the Chiang Mai Initiative Multilateralisation. These arrangements provide additional liquidity backstops beyond foreign exchange reserves, though authorities have not activated swap lines since the 2008-2009 global financial crisis.

Reserve management emphasises safety and liquidity whilst generating modest returns, with holdings diversified across major currencies and high-quality sovereign securities. The Bank of Korea has gradually increased reserve transparency, publishing aggregate composition data whilst maintaining confidentiality regarding specific holdings. The reserve adequacy framework considers multiple metrics including import coverage, short-term debt coverage, and broader measures of external financing needs. Current reserve levels exceed all standard adequacy benchmarks, providing substantial buffers against external shocks.

The external position outlook remains favourable under baseline scenarios, supported by technological competitiveness, diversified export markets, and prudent macroeconomic management. However, downside risks have intensified due to US tariff implementation, potential escalation of trade tensions, and geopolitical fragmentation of supply chains. The USD 350 billion investment commitment to the United States will generate substantial capital outflows over coming years, though these flows are manageable given Korea's strong savings rate and current account surpluses. Successful navigation of the evolving trade environment whilst maintaining external stability represents a key policy challenge for the Lee Jae-myung administration, requiring careful balancing of exchange rate flexibility, reserve management, and structural competitiveness enhancement.

Credit Strengths & Vulnerabilities

Strengths

South Korea's sovereign credit profile rests on a foundation of exceptional external resilience and technological competitiveness that distinguishes it amongst advanced economies. The nation's foreign exchange reserves of $415.6 billion as of December 2024 provide substantial buffers against external shocks, representing approximately 7.5 months of import cover and positioning Korea amongst the world's largest reserve holders. This external strength manifests most clearly in the persistent current account surplus, which reached $99 billion or 5.3% of GDP in 2024, driven by record semiconductor exports that capitalised on the global artificial intelligence boom. The structural nature of this surplus—sustained across economic cycles—reflects Korea's deep integration into global technology supply chains and competitive advantages in high-value manufacturing sectors.

The semiconductor industry exemplifies Korea's technological leadership, with Samsung and SK Hynix commanding a combined 60.5% share of the global memory chip market. This dominance extends beyond market share to encompass cutting-edge production capabilities in advanced nodes and high-bandwidth memory essential for AI applications. The sector's resilience proved particularly evident during 2024, when semiconductor exports surged despite broader global trade uncertainties, underscoring Korea's position as an indispensable node in critical technology supply chains. Beyond semiconductors, the economy demonstrates diversified export competitiveness across secondary batteries, displays, shipbuilding, and automotive components, reducing dependence on any single sector whilst maintaining technological sophistication.

Korea's institutional framework demonstrated remarkable resilience during the December 2024 constitutional crisis, when the National Assembly swiftly rejected President Yoon Suk Yeol's martial law declaration within hours and subsequently impeached him through constitutional procedures. The Constitutional Court's expedited review process and the orderly transition to the Lee Jae-myung administration in June 2025 validated the strength of democratic institutions and rule of law. All three major rating agencies explicitly cited this institutional response as justification for maintaining stable outlooks, with S&P noting that whilst political turbulence "hurt confidence in political stability," the swift resolution demonstrated "effective democratic response mechanisms." The financial markets' relatively contained reaction—with the KOSPI declining only 2.3% on the day following the martial law declaration before recovering—further evidenced confidence in institutional stability.

The banking system maintains robust fundamentals with capital adequacy ratios of 16.9% as of September 2024, well above regulatory minimums and providing substantial loss absorption capacity. Non-performing loan ratios remain historically low at 0.4%, reflecting conservative underwriting standards and effective risk management practices developed through previous financial crises. The Bank of Korea's credible monetary policy framework, anchored by inflation targeting and operational independence, has successfully guided inflation down from 5.1% in 2022 to 2.3% in 2024, approaching the 2% target and creating space for accommodative policy to support growth. Fiscal fundamentals remain sound relative to advanced economy peers, with government debt at 47.4% of GDP in 2024—substantially below the OECD average—and debt service costs manageable despite recent increases in borrowing costs.

Vulnerabilities

The household debt burden represents South Korea's most significant structural vulnerability, with the ratio reaching 91.7% of GDP in 2024—the second highest amongst OECD economies after Switzerland. The absolute level of household debt stood at approximately KRW 1,900 trillion, with mortgage debt comprising roughly 60% of the total. This elevated indebtedness constrains domestic consumption, as households allocate increasing shares of income to debt service rather than discretionary spending, creating a persistent drag on economic growth. The vulnerability intensifies given the prevalence of variable-rate mortgages and bullet repayment structures, which expose borrowers to interest rate risk and refinancing challenges. Whilst the Bank of Korea's recent rate cuts to 3.25% provide some relief, the cumulative impact of previous tightening—rates rose from 0.5% in 2021 to 3.5% by 2023—continues to pressure household balance sheets.

Real estate project finance exposures pose acute systemic risks, with outstanding PF loans totalling KRW 132.2 trillion as of mid-2024, concentrated in non-bank financial institutions including savings banks, mutual finance institutions, and insurance companies. The construction sector downturn, triggered by rising interest rates and weakening property demand, has resulted in numerous project delays and defaults, particularly affecting small and medium-sized developers. The government established a KRW 5 trillion stabilisation fund in 2023 and expanded support measures in 2024, yet vulnerabilities persist as property market weakness continues. Non-bank financial institutions face particular stress, with some regional savings banks reporting elevated NPL ratios exceeding 5% on construction-related exposures. The interconnected nature of real estate finance—linking developers, financial institutions, households, and local government revenues—amplifies potential contagion risks should property market stress intensify.

Demographic pressures represent an inexorable long-term challenge, with South Korea recording the world's lowest total fertility rate of 0.72 in 2023, declining further to an estimated 0.68 in 2024. The working-age population (15-64 years) peaked in 2017 and has entered sustained decline, projected to fall from 72% of total population in 2020 to 56% by 2040 according to Statistics Korea. This demographic transition threatens potential growth through labour force contraction whilst simultaneously increasing fiscal pressures from pension and healthcare obligations. The National Pension Service faces projected fund depletion by 2055 under current contribution and benefit structures, necessitating either substantial contribution increases, benefit reductions, or fiscal transfers. The government has announced various pro-natalist policies including expanded childcare support and housing assistance for young families, yet these measures have thus far failed to reverse fertility decline, suggesting the challenge reflects deeper structural factors including high education costs, competitive labour markets, and changing social preferences.

The fiscal position deteriorated notably in 2024, with the deficit reaching 4.1% of GDP—substantially wider than the 3.6% budgeted—due primarily to corporate tax revenue shortfalls as semiconductor companies' profits normalised from previous peaks. Government debt rose to 47.4% of GDP, and the trajectory points toward 50% by 2025 under current policies. Whilst these levels remain manageable relative to advanced economy peers, the trend concerns given limited fiscal space to address demographic pressures and potential economic shocks. The Lee administration's policy platform includes expanded social spending commitments, including universal basic income pilots and enhanced welfare provisions, which could further pressure fiscal balances absent offsetting revenue measures. Debt service costs have increased as borrowing costs rose, consuming a growing share of government expenditure and potentially crowding out productive investments.

Opportunities

The global artificial intelligence revolution presents substantial opportunities for Korean semiconductor manufacturers, with demand for high-bandwidth memory and advanced logic chips accelerating as AI applications proliferate across industries. Samsung and SK Hynix have positioned themselves as essential suppliers for AI infrastructure, with SK Hynix's HBM3E products securing dominant market share in AI accelerators. The sector's capital intensity and technological complexity create high barriers to entry, protecting Korean firms' competitive positions whilst generating substantial export revenues and supporting current account surpluses. Government initiatives including the K-Chips Act provide tax incentives and regulatory support for continued semiconductor investment, aiming to maintain technological leadership through the next generation of process nodes and memory architectures.

Economic integration with ASEAN markets offers diversification opportunities as Korea seeks to reduce dependence on China, which absorbed 20% of Korean exports in 2024 down from peaks above 25% in previous years. The Regional Comprehensive Economic Partnership (RCEP), which entered force in 2022, provides preferential market access across 15 Asia-Pacific economies, whilst bilateral free trade agreements with ASEAN members facilitate deeper integration. Korean firms have accelerated investments in Vietnam, Indonesia, and other ASEAN economies, establishing production bases that serve both local markets and export platforms. This geographic diversification reduces concentration risks whilst positioning Korean companies to benefit from ASEAN's demographic dividends and rising middle-class consumption.

The green transition creates opportunities across multiple sectors where Korean firms possess competitive advantages, including secondary batteries for electric vehicles, hydrogen technologies, and renewable energy equipment. Korean battery manufacturers—LG Energy Solution, Samsung SDI, and SK On—command approximately 30% of the global EV battery market, with substantial order backlogs from major automotive manufacturers. The government's Green New Deal commits KRW 73.4 trillion through 2025 toward low-carbon infrastructure, renewable energy deployment, and green technology development, creating domestic demand whilst supporting export competitiveness. International partnerships, including joint ventures with European and American firms seeking to diversify supply chains away from China, provide growth avenues and technology transfer opportunities.

Financial market deepening and capital market reforms present opportunities to enhance resource allocation efficiency and develop Seoul as a regional financial centre. The government's "Corporate Value-Up Programme" launched in 2024 aims to improve corporate governance, increase shareholder returns, and reduce the "Korea discount"—the persistent valuation gap between Korean equities and global peers. Measures include tax incentives for companies that enhance shareholder value, regulatory reforms to facilitate mergers and acquisitions, and pension fund governance improvements to encourage active ownership. Success in these reforms could attract substantial foreign portfolio investment, reduce capital costs for Korean firms, and enhance overall economic efficiency.

Threats

US trade policy represents the most immediate external threat, with the July 2025 agreement imposing 15% tariffs on Korean goods—reduced from threatened 25% levels—alongside Korea's commitment to $350 billion in US investments over five years. The Bank of Korea estimates these tariffs could reduce 2025 GDP growth to 0.9% in a severe scenario, down from baseline projections of 1.5-2.0%, through direct export impacts and indirect confidence effects. The tariff structure particularly affects automotive and electronics exports, sectors where Korea maintains substantial trade surpluses with the United States. Beyond immediate economic impacts, the agreement constrains policy flexibility and diverts investment resources toward politically-motivated rather than economically-optimal allocations. Uncertainty regarding future US trade policy—including potential additional measures or renegotiation demands—complicates corporate planning and investment decisions.

Geopolitical tensions surrounding Taiwan and broader US-China technological competition place Korean firms in increasingly untenable positions, forced to navigate conflicting demands from their two largest export markets. US restrictions on semiconductor equipment exports to China and pressure on allied countries to implement similar controls directly affect Korean manufacturers' access to the Chinese market, which absorbed approximately 40% of Korean semiconductor exports in recent years. Simultaneously, China has accelerated domestic semiconductor development and implemented preferential procurement policies favouring local suppliers, threatening Korean market share over the medium term. Any military conflict or severe crisis regarding Taiwan would devastate Korean semiconductor supply chains, which depend on Taiwanese equipment suppliers and maintain substantial production facilities vulnerable to disruption.

Domestic political polarisation persists despite the constitutional crisis's resolution, with deep divisions between progressive and conservative factions regarding economic policy, North Korea engagement, and foreign policy orientation. The Lee administration's policy platform represents a significant departure from previous approaches, including more accommodative North Korea policies, potential recalibration of US alliance priorities, and expanded state intervention in the economy. These shifts create policy uncertainty and risk alienating conservative constituencies and business communities. The narrow legislative majorities and fractious coalition dynamics suggest potential governance challenges, including difficulties passing controversial reforms or responding decisively to economic shocks. Political instability could resurface if economic conditions deteriorate or if North Korea provocations intensify, potentially triggering renewed market volatility and confidence shocks.

The property market downturn threatens to intensify, with leading indicators suggesting continued weakness in housing transactions and construction activity. Property prices in Seoul declined approximately 8% from 2022 peaks through 2024, whilst unsold housing inventory accumulated in provincial cities and new metropolitan areas. Further price declines could trigger negative wealth effects on consumption, increase household debt burdens relative to collateral values, and intensify stress on construction-related lending. The government faces difficult policy trade-offs between supporting the property market—risking moral hazard and inflating another bubble—and allowing market corrections that could trigger financial instability. Demographic trends suggest structural headwinds for property demand over the long term, particularly in non-metropolitan areas experiencing population decline, implying that cyclical recovery may prove elusive without addressing fundamental supply-demand imbalances.

Economic Analysis

Growth Dynamics and Structural Challenges

South Korea's economic performance in 2024 demonstrated resilience amid political turbulence, achieving 2.2% real GDP growth despite the constitutional crisis that erupted in December. This expansion represented a notable acceleration from the subdued 1.4% recorded in 2023, driven primarily by a robust recovery in semiconductor exports that capitalised on the global artificial intelligence investment cycle. The technology sector's resurgence proved sufficiently powerful to offset persistent weakness in domestic consumption and a pronounced contraction in construction activity, underscoring the economy's continued dependence on external demand dynamics.

The growth composition reveals structural imbalances that constrain medium-term potential. Private consumption remains subdued, weighed down by elevated household debt servicing burdens and deteriorating consumer confidence following the political crisis. The construction sector faces acute distress, with project finance exposures totalling KRW 132.2 trillion creating systemic risks that have necessitated government intervention and regulatory forbearance. Real estate market corrections, particularly in the unsold housing inventory, have dampened residential investment whilst commercial property valuations face downward pressure from rising vacancy rates and tightening credit conditions for developers.

The external sector provided the principal growth engine in 2024, with the current account surplus surging to 5.3% of GDP—the highest ratio since 2015—as semiconductor exports reached record levels. Memory chip shipments benefited from inventory restocking cycles and robust demand from data centre operators deploying generative AI infrastructure. However, this export concentration creates vulnerability to technological cycles and geopolitical supply chain disruptions, particularly given intensifying US-China competition for semiconductor supremacy.

Looking toward 2025, growth projections have deteriorated markedly following the July tariff agreement with the United States. The Bank of Korea's downward revision to 0.9% growth reflects the anticipated drag from 15% tariffs on Korean exports, though this represents a more favourable outcome than the 25% universal tariffs initially threatened. The agreement's requirement for $350 billion in US investment commitments over the coming years may provide partial offset through increased capital expenditure by Korean conglomerates, particularly in semiconductor fabrication facilities and electric vehicle production capacity located in the United States. Nevertheless, the near-term impact remains contractionary, with export-oriented manufacturers facing margin compression and potential market share losses to competitors benefiting from more favourable tariff treatment.

The new Lee Jae-myung administration's policy agenda introduces additional uncertainty regarding growth trajectories. Campaign commitments to expand social welfare programmes, including universal basic income pilots and enhanced unemployment benefits, suggest a shift toward consumption-supporting fiscal measures. However, implementation timelines remain unclear, and the stimulative impact may be constrained by fiscal consolidation pressures as government debt approaches 50% of GDP. The administration's stated intention to pursue closer economic engagement with China—Korea's largest trading partner—could provide export diversification benefits but risks complicating relations with the United States and potentially exposing Korean firms to secondary sanctions related to technology transfers.

Demographic headwinds continue to intensify, with Korea's fertility rate remaining the world's lowest and creating long-term constraints on potential growth. The working-age population has entered structural decline, necessitating productivity improvements to sustain economic expansion. Whilst automation and artificial intelligence adoption offer pathways to enhanced efficiency, the transition requires substantial capital investment and workforce retraining that may prove challenging given fiscal constraints and rigid labour market structures.

Inflation Dynamics and Price Stability

Inflationary pressures moderated substantially throughout 2024, with consumer price inflation declining to 2.3% from the previous year's 3.6%, approaching the Bank of Korea's 2% target. This disinflation reflected multiple factors, including base effects from 2022's energy price spike, won appreciation during the first half of the year, and persistent weakness in domestic demand that limited pricing power across service sectors. Core inflation excluding food and energy decelerated more gradually, suggesting underlying price pressures remained somewhat elevated despite headline moderation.

The inflation trajectory benefited from favourable external developments, particularly stabilisation in global commodity markets and easing supply chain constraints that had driven goods price inflation during the pandemic period. Domestic agricultural price volatility—historically a significant contributor to headline inflation variability—remained contained through 2024, though weather-related supply disruptions created periodic spikes in fresh food categories. Administered prices, including public transportation fares and utility charges, saw limited adjustments as authorities prioritised cost-of-living relief amid political uncertainty.

Looking forward to 2025, inflation projections centring on 2.0% suggest continued convergence toward the policy target, though several factors warrant monitoring. The won's depreciation to 1,400 per US dollar by year-end 2024 creates pass-through risks for imported goods prices, particularly given Korea's substantial energy import dependence. The tariff agreement with the United States introduces additional complexity, as Korean exporters may attempt to pass through tariff costs to US consumers whilst domestic prices could face upward pressure from reduced import competition in certain categories.

Wage dynamics present a potential inflation risk, particularly if the new administration pursues labour-friendly policies including minimum wage increases exceeding productivity growth. The tight labour market in certain skilled sectors, notably semiconductor engineering and software development, has generated wage pressures that could broaden if economic growth accelerates. However, overall wage growth remains moderate given employment concentration in small and medium enterprises facing profitability pressures, limiting aggregate demand impacts.

Monetary Policy Framework and Financial Conditions

The Bank of Korea navigated a complex policy environment in 2024, balancing inflation normalisation against growth concerns and financial stability risks. Following an extended period of restrictive policy, the central bank initiated a gradual easing cycle, reducing the base rate to 3.25% as inflation decelerated and growth momentum weakened. This policy recalibration reflected confidence that inflationary pressures had been contained whilst acknowledging the need to support economic activity amid external headwinds and domestic political uncertainty.

The monetary easing proceeded cautiously given persistent financial stability concerns, particularly regarding household debt sustainability and real estate market vulnerabilities. At 91.7% of GDP, Korea's household debt ratio ranks second globally, creating significant interest rate sensitivity that constrains monetary policy flexibility. The central bank's Financial Stability Report has repeatedly emphasised risks from floating-rate mortgage exposures and high debt service ratios among younger households with recent property purchases at elevated valuations. Rate reductions provide debt servicing relief but risk reigniting speculative property demand that authorities have sought to contain through macroprudential measures.

The December 2024 political crisis tested the Bank of Korea's crisis management capabilities, with foreign exchange and equity markets experiencing acute volatility. The central bank responded through coordinated interventions, deploying foreign exchange reserves to stabilise the won whilst providing liquidity support to financial institutions facing temporary funding pressures. These actions, conducted in consultation with the Ministry of Economy and Finance, demonstrated effective policy coordination and helped contain contagion risks. Market functioning normalised relatively quickly, validating the institutional frameworks established following the 1997-98 Asian Financial Crisis and refined during subsequent episodes of external stress.

Looking ahead, monetary policy faces a challenging environment characterised by conflicting pressures. The growth slowdown anticipated from US tariffs argues for continued easing to support domestic demand, whilst won depreciation and potential inflation pass-through effects counsel caution. The Bank of Korea's forward guidance suggests a data-dependent approach prioritising inflation stability whilst remaining prepared to provide accommodation if growth deteriorates more severely than projected. Market expectations as of early 2026 anticipate further modest rate reductions, though the pace and magnitude remain contingent on inflation trajectories and financial stability assessments.

The effectiveness of monetary transmission mechanisms warrants consideration given structural features of Korea's financial system. High household debt levels amplify interest rate impacts on consumption through debt servicing channels, whilst corporate sector responses remain heterogeneous. Large conglomerates with substantial cash reserves and access to international capital markets demonstrate limited sensitivity to domestic rate changes, whereas small and medium enterprises reliant on bank lending face more binding financial constraints. This heterogeneity complicates policy calibration and may necessitate complementary fiscal and regulatory measures to achieve desired macroeconomic outcomes.

Exchange rate dynamics constitute an additional monetary policy consideration, particularly given Korea's export dependence and the won's role as a regional bellwether currency. The depreciation to 1,400 per US dollar reflects multiple factors including interest rate differentials with the United States, risk-off sentiment during the political crisis, and structural current account dynamics. Whilst competitiveness benefits accrue to exporters, excessive volatility disrupts corporate planning and creates balance sheet risks for firms with unhedged foreign currency exposures. The Bank of Korea's intervention framework seeks to smooth volatility rather than target specific levels, though the distinction becomes blurred during periods of acute market stress.

Political & Institutional Assessment

South Korea's political and institutional framework has undergone severe stress testing through the December 2024 constitutional crisis, yet demonstrated fundamental resilience that underpins the sovereign's high credit standing. The attempted martial law declaration by President Yoon Suk Yeol on 3 December 2024 represented the gravest challenge to democratic governance since the country's transition from authoritarian rule in the late 1980s. However, the National Assembly's swift rejection of the emergency measures within hours, followed by the constitutional impeachment process and subsequent transfer of power, validated the strength of institutional checks and balances embedded in Korea's democratic architecture.

The Constitutional Court's ruling on the impeachment and the subsequent presidential election resulted in the inauguration of President Lee Jae-myung in June 2025, marking the first transfer of power from the conservative People Power Party to the progressive Democratic Party since 2017. This transition occurred within constitutional parameters and established timelines, demonstrating institutional continuity despite political turbulence. The new administration's policy platform emphasises expanded social welfare programmes, increased fiscal support for household debt relief, and a recalibration of foreign policy positioning between the United States and China. Whilst these policy shifts introduce new uncertainties regarding fiscal trajectory and geopolitical alignment, the orderly transition itself reinforces confidence in Korea's democratic institutions.

The National Assembly maintains its constitutional role as a check on executive power, having demonstrated its capacity to act decisively during the martial law crisis. The legislature's composition following the April 2024 general elections, which delivered a supermajority to opposition parties, creates a divided government structure that necessitates consensus-building for major policy initiatives. This configuration has historically constrained executive overreach whilst occasionally complicating fiscal policy implementation, particularly regarding budget approvals and structural reform legislation. The judiciary, including the Constitutional Court, has maintained independence throughout the political crisis, with its handling of the impeachment proceedings broadly viewed as procedurally sound and constitutionally grounded.

Korea's civil service and regulatory institutions demonstrated operational continuity throughout the political upheaval. The Ministry of Economy and Finance maintained fiscal discipline, the Financial Services Commission coordinated market stabilisation measures, and the Bank of Korea operated monetary policy independently. These technocratic institutions benefit from professional career structures largely insulated from political cycles, providing policy continuity across administrations. The Financial Supervisory Service's handling of real estate project finance exposures and household debt monitoring has shown technical competence, though the effectiveness of macroprudential measures remains subject to political pressures regarding implementation stringency.

The political crisis has nonetheless left lasting implications for governance quality and policy predictability. Public confidence in political institutions suffered measurable deterioration, with approval ratings for major political parties declining significantly in the crisis aftermath. The polarisation between progressive and conservative political camps has intensified, complicating consensus formation on structural reforms addressing demographic decline, labour market rigidities, and pension system sustainability. The Lee administration's policy priorities, including expanded social spending and potential recalibration of the US-ROK alliance framework, introduce uncertainties regarding fiscal consolidation pathways and geopolitical risk management.

Corruption perceptions and governance indicators place Korea in the upper tier of emerging markets but below advanced economy peers. Transparency International's Corruption Perceptions Index consistently ranks Korea in the 30-35 range globally, reflecting ongoing challenges with business-government relations and political accountability. The prosecution and conviction of multiple former presidents on corruption charges demonstrates both the prevalence of governance issues and the judiciary's willingness to hold senior officials accountable. The current administration has pledged governance reforms, though implementation effectiveness remains to be demonstrated.

The institutional response to the December 2024 crisis ultimately reinforced rather than undermined credit fundamentals. Rating agencies explicitly cited the National Assembly's swift action and constitutional processes as evidence of institutional resilience. S&P noted that whilst political turbulence "hurt confidence in political stability," the democratic response mechanisms functioned effectively. Fitch emphasised that "Korea's institutional framework proved robust under stress," whilst Moody's highlighted the "effective operation of constitutional checks and balances." This institutional performance distinguishes Korea from emerging markets where political crises typically trigger institutional breakdown or extra-constitutional interventions.

Looking forward, the restoration of political stability under the Lee administration provides a foundation for addressing medium-term structural challenges, though policy execution risks remain elevated. The government's ability to navigate US-China tensions whilst maintaining technological competitiveness, implement household debt reduction without triggering financial instability, and advance demographic policy responses will determine whether institutional strengths translate into sustained credit quality. The political consensus required for pension reform, labour market liberalisation, and fiscal consolidation remains elusive given partisan polarisation, potentially constraining policy flexibility in responding to external shocks or demographic pressures.

Banking Sector & Financial Stability

South Korea's banking sector demonstrates robust capitalisation and asset quality metrics that provide a substantial buffer against economic headwinds, though concentrated exposures in real estate project finance and elevated household indebtedness present material medium-term vulnerabilities requiring sustained regulatory vigilance. The sector's resilience was tested during the December 2024 political crisis, when financial institutions successfully maintained liquidity and operational continuity despite heightened market volatility, underscoring the effectiveness of post-2008 regulatory reforms and crisis management frameworks.

Capital Adequacy and Asset Quality

The banking system maintains strong capital adequacy ratios well above regulatory minimums, with the sector-wide Common Equity Tier 1 (CET1) ratio standing at 16.9% as of December 2024, significantly exceeding the Basel III minimum requirement of 7.0% including conservation buffers. This substantial capital cushion reflects conservative risk management practices and regulatory requirements that have been progressively strengthened since the 2008 global financial crisis. Total capital adequacy ratios across major commercial banks range from 15.2% to 18.4%, providing meaningful loss absorption capacity against potential credit deterioration.

Asset quality indicators remain exceptionally strong by international standards, with the non-performing loan (NPL) ratio across the banking sector registering just 0.4% as of year-end 2024, amongst the lowest globally. This reflects both rigorous underwriting standards and the relatively short duration of recent economic stress. Loan loss provisions stand at adequate levels relative to NPLs, with coverage ratios exceeding 150% at major institutions. However, these benign asset quality metrics partly reflect forbearance measures and restructuring arrangements that may mask underlying credit stress, particularly in commercial real estate and amongst highly leveraged households. Forward-looking indicators, including Stage 2 loans under IFRS 9 accounting standards, have shown modest increases, suggesting potential migration to non-performing status if economic conditions deteriorate further.

Household Debt Vulnerabilities

Household indebtedness represents the most significant structural vulnerability in Korea's financial system, with the household debt-to-GDP ratio reaching 91.7% in 2024, the second-highest amongst OECD economies after Switzerland. In absolute terms, household debt totalled approximately KRW 1,900 trillion (USD 1.36 trillion), with mortgage lending comprising roughly 45% of total household borrowing. The debt service ratio—measuring principal and interest payments relative to disposable income—stands at elevated levels, rendering household balance sheets sensitive to interest rate movements and income shocks.

The composition of household debt presents particular concerns, with significant exposure to variable-rate mortgages and bullet repayment structures that concentrate refinancing risk. Approximately 35% of mortgage loans feature interest-only payment structures during initial periods, creating potential payment shock when principal amortisation commences. Geographic concentration in Seoul and surrounding metropolitan areas, where property valuations have experienced substantial appreciation over the past decade, amplifies systemic risk should housing market corrections materialise.

Regulatory authorities have implemented macroprudential measures to contain household debt growth, including tightened loan-to-value (LTV) and debt-service-to-income (DSI) ratios, stress testing requirements for mortgage origination, and restrictions on lending to multiple property owners. These measures have moderated household debt growth to approximately 4.5% year-on-year in 2024, down from double-digit growth rates in previous years. However, the stock of existing debt remains elevated, and any significant deterioration in employment conditions or property valuations could trigger financial stress amongst leveraged households, with consequent implications for consumption, housing markets, and banking sector asset quality.

Real Estate Project Finance Exposures

Real estate project finance (PF) exposures represent a concentrated risk within Korea's financial system, with total exposures estimated at KRW 132.2 trillion (approximately USD 94 billion) as of December 2024. These exposures are distributed across commercial banks, non-bank financial institutions, and structured investment vehicles, with particular concentration amongst mid-tier banks and specialised construction finance entities. The exposures primarily relate to residential and commercial property development projects, many of which have experienced delays, cost overruns, or viability concerns amid weakening property market conditions and elevated construction costs.

Non-bank financial institutions, including mutual savings banks, credit cooperatives, and insurance companies, hold disproportionate exposures relative to their capital bases, creating potential systemic linkages should project failures proliferate. Approximately 15-20% of total project finance exposures are estimated to face elevated default risk, with particular concentration in regional markets outside Seoul where demand has softened more substantially. The government and financial regulators have established a KRW 20 trillion stabilisation fund to provide liquidity support and facilitate project restructuring, alongside encouraging financial institutions to extend maturities and provide additional funding for viable projects.

Whilst commercial banks' direct exposures remain manageable relative to capital bases—typically representing 5-8% of total loan portfolios at major institutions—indirect exposures through guarantees, credit enhancements, and counterparty relationships with non-bank lenders create potential contagion channels. Stress testing conducted by the Financial Supervisory Service suggests that even under severe scenarios involving 30-40% default rates on project finance exposures, systemically important banks would maintain capital ratios above regulatory minimums, though profitability would be materially impacted. The resolution of troubled projects will likely extend over multiple years, requiring sustained regulatory oversight and potential additional policy support measures.

Regulatory Framework and Supervision

Korea's financial regulatory architecture features multiple agencies with overlapping mandates, including the Financial Services Commission (FSC) as the primary policy-making body, the Financial Supervisory Service (FSS) as the operational supervisor, and the Bank of Korea maintaining financial stability oversight alongside monetary policy responsibilities. This structure has evolved to strengthen coordination mechanisms following past crises, though some analytical commentary suggests potential efficiency gains from further consolidation.

Regulatory standards have been progressively aligned with international best practices, including full implementation of Basel III capital and liquidity requirements, adoption of IFRS 9 accounting standards for credit loss provisioning, and establishment of macroprudential policy frameworks. The authorities maintain active use of macroprudential tools, including countercyclical capital buffers, sectoral capital requirements for real estate exposures, and loan underwriting restrictions calibrated to address emerging vulnerabilities.

Supervisory intensity has increased substantially, with enhanced on-site examinations, stress testing requirements, and early intervention frameworks for troubled institutions. The December 2024 political crisis prompted intensified monitoring of market conditions and liquidity positions, with regulators implementing temporary measures including expanded repo operations, foreign exchange swap facilities, and guidance on dividend distributions to preserve capital. These interventions proved effective in maintaining financial stability during the acute phase of political uncertainty, demonstrating both regulatory capability and institutional resilience.

Outlook & Scenarios

Short-Term Outlook (12 months)

The short-term outlook for South Korea's sovereign credit profile reflects a delicate balance between institutional resilience and mounting economic headwinds. The successful transition to the Lee Jae-myung administration in June 2025 has restored political stability following the constitutional crisis, yet policy uncertainties surrounding expanded social spending commitments and potential foreign policy realignment introduce new variables for credit assessment. The immediate twelve-month horizon is dominated by the economic impact of the July 2025 US tariff agreement, which imposes 15% duties on Korean exports alongside Korea's $350 billion investment commitment to the United States. This arrangement, whilst avoiding the more severe 25% tariff scenario initially threatened, nonetheless represents a substantial drag on export-dependent growth dynamics.

The Bank of Korea's downward revision of 2025 growth projections from 1.5% to a range of 0.9-2.0% captures the magnitude of tariff-related uncertainty, with the lower bound suggesting potential technical recession risks should external demand deteriorate more sharply than anticipated. Semiconductor exports, which drove the current account surplus to $99 billion in 2024, face dual pressures from both tariff costs and cyclical demand moderation in global technology markets. The won's depreciation to 1,400 per US dollar provides some competitive offset, though exchange rate volatility complicates corporate planning and may necessitate foreign exchange intervention that would draw down reserves from their current $415.6 billion level.

Domestic demand remains constrained by household debt servicing burdens, with the 91.7% debt-to-GDP ratio limiting consumption growth even as the Bank of Korea maintains accommodative monetary policy at 3.25%. The construction sector contraction continues to weigh on activity, with real estate project finance exposures of KRW 132.2 trillion representing a persistent vulnerability that requires careful monitoring of non-bank financial institution stress. Inflation is expected to remain well-anchored near the 2% target, providing scope for monetary support should growth disappoint, though the won's weakness introduces upside risks to import price pressures.

The fiscal position faces competing pressures between the new administration's social spending agenda and the imperative to maintain prudent debt dynamics that underpin sovereign ratings. The 2024 fiscal deficit of 4.1% of GDP, driven by corporate tax shortfalls, establishes an elevated baseline, with government debt projected to approach 50% of GDP in 2025. Whilst this remains moderate by advanced economy standards, the trajectory warrants attention given demographic pressures that will intensify fiscal demands over the medium term. The administration's ability to balance campaign commitments with fiscal discipline will prove critical to maintaining rating agency confidence.

Financial system stability appears robust in the near term, with banking sector capital adequacy at 16.9% and non-performing loan ratios at historically low 0.4% providing substantial buffers. However, concentrated exposures to real estate project finance in non-bank institutions require continued regulatory vigilance, particularly should property market stress intensify. The authorities demonstrated effective crisis management capabilities during the December 2024 political turbulence, with foreign exchange and equity markets stabilising rapidly following the National Assembly's rejection of martial law, reinforcing confidence in institutional response mechanisms.

Medium-Term Outlook (1-3 years)

The medium-term credit trajectory hinges on South Korea's capacity to navigate structural transitions whilst preserving the economic fundamentals that support high sovereign ratings. Demographic pressures represent the most profound challenge, with the world's lowest fertility rate of 0.72 births per woman accelerating workforce contraction and intensifying fiscal demands for elderly care and pension systems. This demographic reality necessitates productivity enhancements and labour market reforms to sustain potential growth, yet political economy constraints may limit reform ambition under the new administration's progressive policy orientation.

Household debt dynamics constitute a critical vulnerability requiring sustained policy attention over the medium term. At 91.7% of GDP, Korea's household debt ratio ranks second globally, creating financial stability risks and constraining domestic demand growth essential for rebalancing away from export dependence. The concentration of debt in variable-rate mortgages amplifies sensitivity to monetary policy adjustments, whilst elevated debt service ratios limit households' capacity to absorb economic shocks. Successful debt stabilisation requires coordinated macroprudential measures, income growth support, and potentially extended timelines for deleveraging that may prolong domestic demand weakness.

Geopolitical positioning within intensifying US-China technological competition presents both opportunities and risks for Korea's semiconductor-centric industrial structure. Korea's commanding 60.5% share of global memory markets provides strategic leverage, yet supply chain concentration creates vulnerabilities to disruption and political pressure from both major powers. The $350 billion US investment commitment reflects partial alignment with American technology policy, though this may complicate economic relations with China, Korea's largest trading partner. Successfully navigating this strategic environment requires diplomatic dexterity and industrial policy that preserves market access across geopolitical divides whilst advancing technological capabilities.

The real estate sector's adjustment trajectory carries systemic implications extending beyond immediate project finance exposures. Prolonged property market weakness would impair household balance sheets given high homeownership rates and mortgage debt concentrations, potentially triggering broader financial stress. Non-bank financial institutions' KRW 132.2 trillion exposure to project finance represents a focal point for regulatory intervention, with authorities likely to extend forbearance measures and liquidity support to prevent disorderly unwinding. The pace and management of this adjustment will significantly influence financial stability assessments over the medium term.

Fiscal sustainability considerations intensify beyond the immediate horizon as demographic pressures translate into structural spending increases. Government debt approaching 50% of GDP provides fiscal space relative to advanced economy peers, yet the trajectory matters more than the level given Korea's rapid ageing dynamics. The new administration's expanded social spending commitments, including basic income proposals and enhanced welfare provisions, require credible financing frameworks to maintain rating agency confidence. Tax reform and expenditure prioritisation will prove essential to reconciling policy ambitions with debt sustainability, particularly should growth disappoint and revenue generation weaken.

Rating Scenarios

The current rating consensus of AA/Aa2/AA- with stable outlooks reflects balanced risks, though distinct scenarios could prompt rating actions over the medium term. Upside rating potential exists but appears limited given structural constraints, whilst downside scenarios centre on political instability persistence, fiscal deterioration, or financial system stress.

Upside Scenario (Low Probability): An upgrade trajectory would require demonstration of successful structural reform implementation that enhances potential growth and addresses demographic challenges. Specific catalysts might include comprehensive labour market reforms that increase workforce participation and productivity, credible fiscal frameworks that stabilise debt dynamics despite ageing pressures, and household debt reduction that proceeds without triggering financial instability or prolonged demand weakness. Additionally, successful navigation of US-China tensions that preserves market access whilst advancing technological capabilities, combined with political stability consolidation under the new administration with effective governance, would support positive rating momentum. However, the probability of this scenario remains constrained by political economy obstacles to reform and the structural nature of demographic headwinds.

Base Case (High Probability): Rating maintenance with stable outlooks represents the most likely scenario, predicated on continued institutional resilience and policy effectiveness. This scenario assumes political normalisation under the Lee administration without major governance disruptions, economic growth stabilisation in the 1.5-2.0% range following tariff adjustment, gradual household debt stabilisation through macroprudential measures without systemic stress, and fiscal deficits contained below 3% of GDP with debt stabilising near 50-55% of GDP. The external position would remain strong with current account surpluses sustained above 4% of GDP and foreign exchange reserves adequate at $350-400 billion. Financial system stability would be preserved through effective management of real estate exposures, whilst semiconductor competitiveness would be maintained despite geopolitical pressures. This scenario reflects rating agencies' demonstrated tolerance for political volatility provided institutional responses prove effective and economic fundamentals remain sound.

Downside Scenario (Moderate Probability): Negative rating actions could materialise through several channels, with political instability representing the most immediate risk. Prolonged political dysfunction under the new administration that impairs policy effectiveness, or renewed constitutional crisis that undermines institutional credibility, would challenge current rating levels. Economic deterioration through severe US tariff impacts that push growth below 1% for extended periods, or household debt distress triggering financial instability and credit contraction, would similarly pressure ratings. Fiscal slippage with deficits persistently exceeding 4% of GDP and debt rising above 60% without credible consolidation plans would concern rating agencies, as would external shocks including sharp won depreciation requiring substantial reserve intervention or current account deterioration below 2% of GDP. Financial system stress through disorderly real estate adjustment or non-bank institution failures requiring public sector support would also warrant negative consideration. Geopolitical scenarios involving severe US-China tensions that fragment Korean export markets or compromise semiconductor supply chains represent tail risks with potentially severe rating implications.

The probability distribution across scenarios suggests asymmetric risks tilted modestly toward the downside over the medium term, reflecting structural challenges that require sustained policy attention. However, Korea's demonstrated institutional resilience, strong external buffers, and technological competitiveness provide substantial rating support that would likely prevent precipitous downgrades absent severe shocks. Rating agencies' maintenance of stable outlooks through the December 2024 crisis establishes a high threshold for negative action, suggesting that gradual deterioration would more likely prompt outlook revisions before actual downgrades. Conversely, the structural nature of demographic and debt challenges limits upside potential, implying that current ratings may represent a ceiling absent transformative reforms. Investors should monitor political stability consolidation, household debt trajectories, fiscal policy credibility, and geopolitical developments as key indicators of rating direction over the outlook horizon.

Conclusion

South Korea's sovereign credit profile reflects a fundamental tension between robust structural strengths and emerging vulnerabilities that require careful navigation over the medium term. The maintenance of high investment-grade ratings (AA/Aa2/AA-) by all three major agencies through the December 2024 political crisis demonstrates the resilience of Korea's institutional framework and the depth of its economic fundamentals. The swift constitutional response to the martial law declaration, combined with the orderly transition to the Lee Jae-myung administration by June 2025, validated rating agencies' confidence in democratic institutions and crisis management capabilities.

Korea's external position remains exceptionally strong, underpinned by foreign exchange reserves of $415.6 billion, a current account surplus approaching 6% of GDP, and technological leadership in semiconductors commanding 60.5% of global memory market share. These strengths provide substantial buffers against external shocks and support the won's reserve currency characteristics. The banking system's capital adequacy ratio of 16.9% and historically low non-performing loan ratio of 0.4% further reinforce financial stability, whilst the government debt ratio below 50% of GDP leaves fiscal space for countercyclical measures.

However, structural vulnerabilities pose meaningful medium-term challenges to credit quality. Household debt at 91.7% of GDP—the second-highest globally—creates financial stability risks and constrains domestic consumption growth, particularly as interest rates remain elevated. Real estate project finance exposures totalling KRW 132.2 trillion in non-bank financial institutions require continued regulatory vigilance to prevent systemic spillovers. The world's lowest fertility rate compounds long-term fiscal pressures through pension and healthcare obligations, whilst the working-age population decline threatens potential growth.

Near-term growth prospects face significant headwinds from the 15% US tariff agreement, with Bank of Korea estimates suggesting GDP growth could decelerate to 0.9% in 2025 under adverse scenarios. This external demand shock arrives as domestic consumption remains weak and the construction sector contracts, limiting policy options given existing household leverage. The new administration's commitment to expanded social spending, whilst addressing inequality concerns, may accelerate fiscal deterioration beyond the projected 50% debt-to-GDP threshold.

Geopolitical positioning between the United States and China presents ongoing strategic challenges, particularly regarding semiconductor supply chain security and technology transfer restrictions. Korea's export concentration in technology sectors creates vulnerability to both trade policy shifts and cyclical demand fluctuations, as evidenced by the semiconductor downturn's impact on growth volatility.

The credit outlook hinges on several key factors: successful management of household debt deleveraging without triggering financial instability or sharp consumption contraction; effective resolution of real estate project finance exposures through orderly restructuring; restoration of political consensus to support structural reforms addressing demographic challenges; and strategic navigation of US-China competition to preserve market access whilst maintaining technological advantages. The banking system's resilience and substantial foreign reserves provide important shock absorbers, yet the convergence of domestic structural weaknesses with external trade headwinds narrows the margin for policy error.

Whilst current ratings appear well-supported by Korea's institutional strength and external buffers, sustained rating stability requires demonstrable progress on structural reform implementation, particularly regarding household debt sustainability and demographic adaptation. The political transition provides an opportunity for policy recalibration, though the new administration's policy direction introduces uncertainties around fiscal discipline and foreign policy alignment. Rating agencies will monitor closely the trajectory of growth recovery, fiscal consolidation credibility, and financial stability indicators over the coming 12 to 18 months as key determinants of medium-term credit quality.