Saudi Arabia

Executive Summary

Saudi Arabia maintains a robust A/A1 investment-grade credit profile underpinned by substantial financial buffers, moderate government debt levels, and accelerating progress in economic diversification under the Vision 2030 reform programme. As of April 2025, the Kingdom holds stable outlooks from S&P Global and Moody's, whilst Fitch Ratings has assigned a positive outlook following an upgrade from A- in October 2024, signalling potential for further ratings improvement. The sovereign's credit strength derives primarily from its massive foreign exchange reserves of $467 billion (covering over 30 months of imports), a manageable debt-to-GDP ratio of 25.4%, and the continued profitability of Saudi Aramco, which generated $123.8 billion in profit during 2024. These financial strengths position Saudi Arabia amongst the stronger emerging market sovereign credits, though the Kingdom remains below its wealthier Gulf neighbours Qatar and the UAE in the ratings hierarchy.

The Saudi economy has demonstrated notable resilience amid oil market volatility, with preliminary 2024 GDP growth reaching 2.7% and the non-oil economy expanding by a robust 4.8%, significantly outpacing overall economic growth. Private sector activity has strengthened considerably, recording 5.1% growth in the fourth quarter of 2024, the strongest quarterly performance since 2019. Fiscal consolidation efforts have yielded substantial results, with the fiscal deficit narrowing to 1.2% of GDP in 2024 from 4.2% in the previous year, supported by the introduction of 15% VAT, reduced energy subsidies, and improved spending efficiency. The current account surplus stood at 6.3% of GDP in 2024, whilst inflation remained moderate at 3.2%, well within the Saudi Central Bank's target range. Oil revenues, though still dominant at 65% of government receipts, have declined from 77% in 2018, reflecting tangible progress in revenue diversification.

The Kingdom faces several structural challenges that constrain its credit profile, most notably its continued heavy dependence on hydrocarbon revenues despite diversification efforts, exposure to oil price volatility, and the substantial fiscal requirements of Vision 2030 mega-projects. Regional geopolitical tensions, particularly with Iran, and ongoing involvement in Yemen present persistent security risks, whilst the pace of political reforms continues to lag behind economic and social changes. The government's reliance on Saudi Aramco dividends, which totalled $97.8 billion in 2024, creates fiscal vulnerability to oil sector performance. Additionally, the Kingdom's ambitious development plans, including the $500 billion NEOM project and THE LINE linear city, require sustained high levels of capital expenditure that could pressure fiscal balances if oil prices weaken materially.

The forward outlook for Saudi Arabia's credit profile remains constructive, supported by projected GDP growth of 3.2-4.0% in 2025, continued non-oil sector expansion, and advancing Vision 2030 implementation. The recent opening of NEOM's first hotel in late 2024 and the commencement of THE LINE construction demonstrate tangible progress in flagship diversification projects. The Kingdom's substantial financial buffers provide considerable resilience against potential oil price shocks, whilst fiscal discipline and structural reforms are gradually reducing hydrocarbon dependency. The normalization of relations with Israel, though contingent on progress toward a Palestinian state, represents a significant foreign policy shift that could enhance regional stability and economic opportunities. Fitch's positive outlook suggests potential for ratings upgrades should the Kingdom maintain fiscal consolidation and achieve further diversification milestones, though sustained progress will require continued reform momentum and favourable oil market conditions.

Ratings Summary

Saudi Arabia maintains strong investment-grade sovereign credit ratings from all three major international rating agencies, reflecting the Kingdom's substantial financial buffers, moderate government debt levels, and ambitious structural reform agenda under Vision 2030. As of April 2025, the ratings position Saudi Arabia amongst the stronger emerging market sovereign credits, though below its wealthier Gulf neighbours Qatar and the United Arab Emirates. Fitch Ratings holds the most constructive view with a positive outlook, signalling potential for future upgrades based on continued fiscal discipline and diversification progress, whilst both S&P Global and Moody's maintain stable outlooks. The ratings reflect confidence in the Kingdom's capacity to navigate oil market volatility and regional geopolitical tensions through its massive foreign exchange reserves and accelerating economic diversification efforts.

| Rating Agency | Current Rating | Outlook | Last Action Date |

|---|---|---|---|

| S&P Global | A | Stable | January 2025 |

| Moody's | A1 | Stable | March 2025 |

| Fitch Ratings | A | Positive | October 2024 |

Economic Indicators

Saudi Arabia's economy has demonstrated considerable resilience in recent years, navigating oil market volatility whilst maintaining solid growth momentum. The Kingdom's economic trajectory reflects both the cyclical nature of hydrocarbon revenues and the structural transformation underway through Vision 2030 reforms.

| Indicator | 2021 | 2022 | 2023 | 2024 | 2025 (proj.) | 2030 (IMF) |

|---|---|---|---|---|---|---|

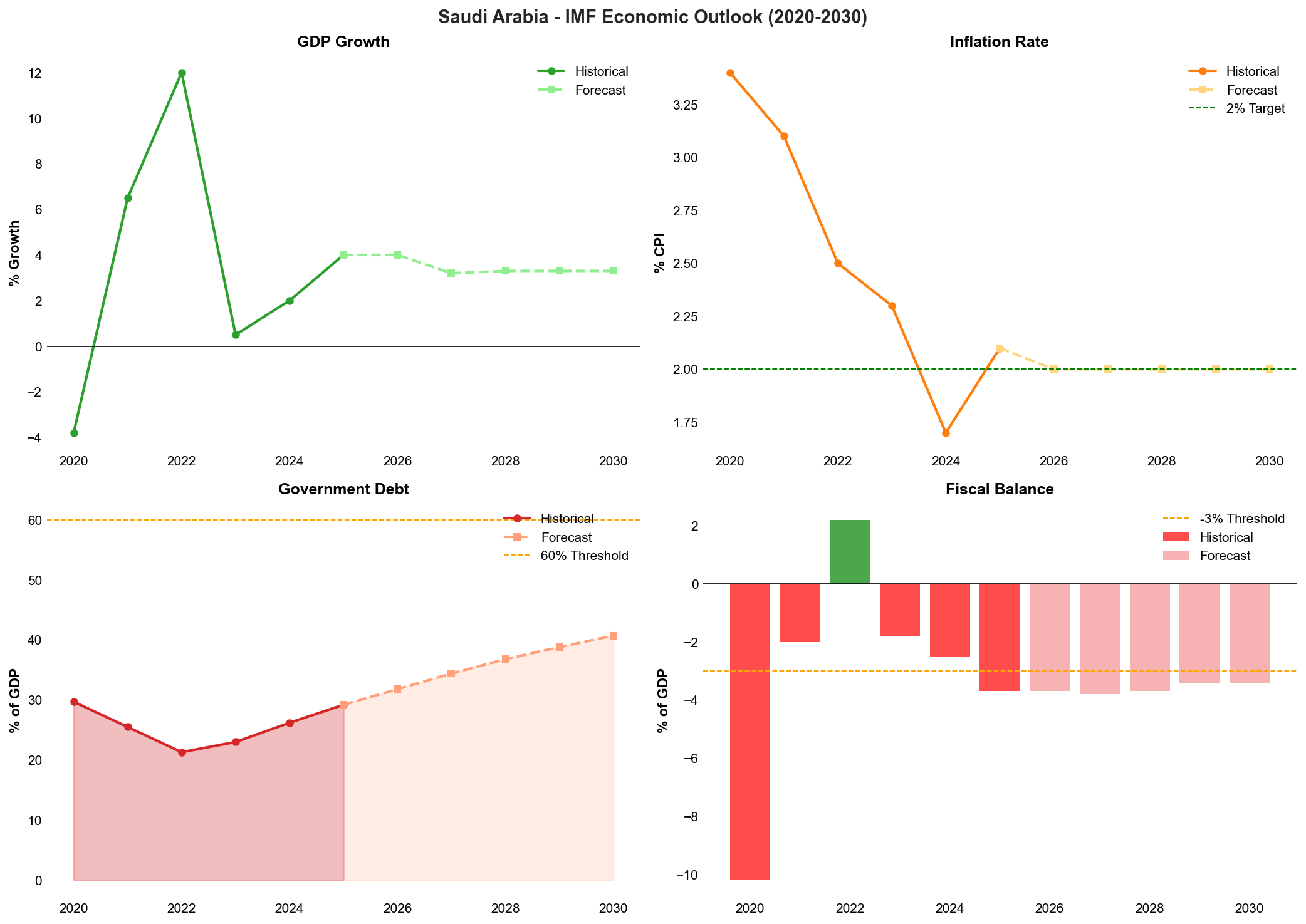

| GDP Growth (%) | 3.2 | 8.7 | 0.8 | 2.7 | 3.2-4.0 | 3.3 |

| Non-oil GDP Growth (%) | - | - | - | 4.8 | - | - |

| Inflation (%) | - | - | 2.5 | 3.2 | 2.8 | 2.0 |

| Fiscal Balance (% GDP) | - | - | -4.2 | -1.2 | - | -3.4 |

| Current Account (% GDP) | - | - | - | 6.3 | - | -44.9 |

| Government Debt (% GDP) | - | - | - | - | 25.4 | 40.7 |

| Unemployment (%) | - | - | - | - | - | 3.5 |

| FX Reserves (USD bn) | - | - | - | - | 467 | - |

Growth dynamics and diversification progress

The Kingdom's economic performance has exhibited marked volatility in recent years, primarily reflecting fluctuations in oil sector activity. Following the exceptional 8.7% expansion in 2022—driven by elevated crude prices and increased production—growth decelerated sharply to 0.8% in 2023 as oil sector output contracted in line with OPEC+ production agreements. The recovery to 2.7% growth in 2024 demonstrates improving economic momentum, with projections of 3.2-4.0% for 2025 suggesting continued strengthening.

Particularly noteworthy is the robust performance of the non-oil economy, which expanded by 4.8% in 2024, substantially outpacing overall GDP growth. This divergence underscores meaningful progress in economic diversification efforts, with private sector growth reaching 5.1% in the fourth quarter of 2024—the strongest quarterly performance since 2019. The IMF's projection of 3.3% growth for 2030 suggests expectations of sustained, albeit moderate, expansion as the economy matures and diversification efforts continue.

Inflation environment and monetary conditions

Inflation has remained well-contained within moderate parameters, registering 2.5% in 2023 and 3.2% in 2024 before moderating to an annualised 2.8% in the first quarter of 2025. These levels remain comfortably within the Saudi Central Bank's target range and below global averages, reflecting the currency peg to the US dollar and relatively stable domestic demand conditions. The IMF's forecast of 2.0% inflation for 2030 suggests expectations of continued price stability, which should allow monetary authorities to maintain accommodative policy settings supportive of non-oil sector growth.

Fiscal consolidation and debt trajectory

Saudi Arabia has achieved substantial progress in fiscal consolidation since the pandemic-induced deterioration of 2020. The fiscal deficit narrowed markedly from 4.2% of GDP in 2023 to 1.2% in 2024, reflecting both improved oil revenues and enhanced spending discipline. This consolidation has been supported by structural reforms including the introduction of value-added taxation at 15%, reduction of energy subsidies, and improved expenditure efficiency across government operations.

The government debt-to-GDP ratio has declined to 25.4% as of the first quarter of 2025, down from 30.0% in 2020, positioning Saudi Arabia amongst the least leveraged major emerging market sovereigns. However, the IMF's projection of 40.7% debt-to-GDP by 2030 suggests expectations of renewed fiscal expansion, likely reflecting the substantial capital requirements of Vision 2030 megaprojects. Whilst this trajectory implies rising leverage, debt levels would remain moderate by international standards and well within the Kingdom's substantial debt servicing capacity.

External position and reserve adequacy

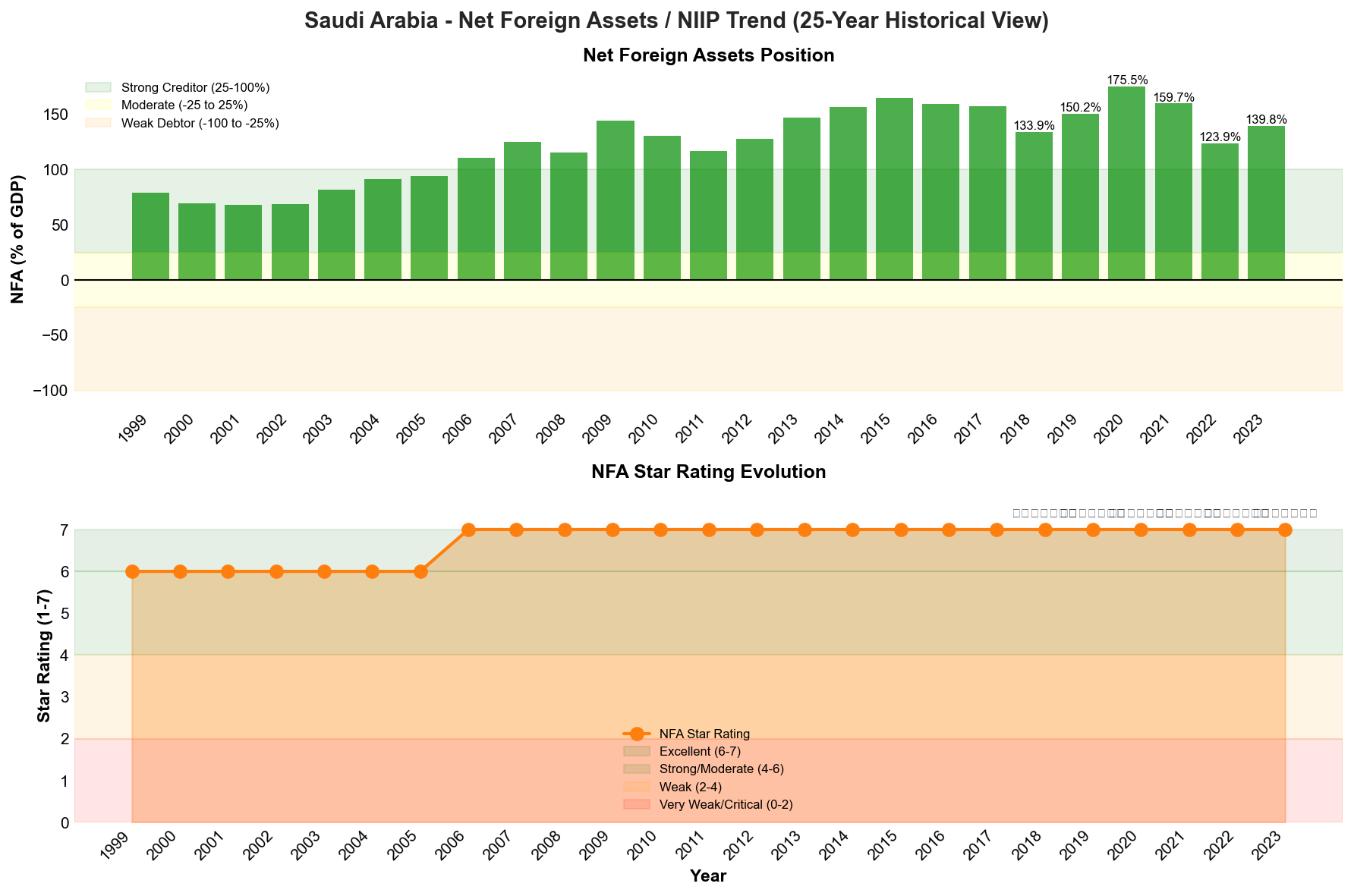

The Kingdom maintains an exceptionally strong external position, with net foreign assets reaching 139.8% of GDP in 2023—a seven-star rating denoting excellent creditor status. Whilst this represents a decline from the peak of 175.5% in 2020, the position remains robust and provides substantial buffers against external shocks. Foreign exchange reserves stood at USD 467 billion in March 2025, providing coverage for over 30 months of imports and significantly exceeding standard adequacy metrics.

The current account registered a healthy surplus of 6.3% of GDP in 2024, supported by elevated oil export revenues. However, the IMF's projection of a substantial current account deficit of 44.9% of GDP by 2030 warrants careful consideration. This dramatic shift likely reflects the import-intensive nature of Vision 2030 infrastructure projects and assumes sustained high levels of capital goods imports. Whilst such deficits would erode the net foreign asset position, the Kingdom's substantial existing buffers and access to international capital markets should ensure external financing remains manageable.

Labour market conditions

Unemployment stood at 3.5% in 2024 according to IMF data, reflecting relatively tight labour market conditions. However, this aggregate figure masks significant disparities, with youth unemployment and female labour force participation remaining policy priorities. The government's Saudisation initiatives, aimed at increasing private sector employment of nationals, continue to progress alongside efforts to expand female workforce participation—a key pillar of Vision 2030's social and economic transformation agenda.

Net Foreign Assets & External Position

Saudi Arabia maintains an exceptionally strong external position, ranking among the world's largest net creditor nations with net foreign assets equivalent to 139.8% of GDP as of 2023. This substantial creditor position provides the Kingdom with formidable buffers against external shocks and underpins its investment-grade sovereign ratings. The external strength reflects decades of accumulated oil wealth, prudent reserve management, and sustained current account surpluses, though the trajectory has moderated from the peak levels observed during the 2020 oil price recovery.

Exceptional creditor status with strategic deployment underway

The Kingdom's net international investment position (NIIP) has consistently maintained an "Excellent" seven-star rating throughout the 2019-2023 period, reflecting net foreign assets well above 100% of GDP. The position peaked at 175.5% of GDP in 2020 during the pandemic-era oil market disruptions, before moderating to 123.9% in 2022 as the government drew down reserves to finance Vision 2030 infrastructure investments and manage fiscal deficits during lower oil prices. The subsequent recovery to 139.8% in 2023 coincided with improved oil revenues and fiscal consolidation, demonstrating the resilience of Saudi Arabia's external buffers even as the Kingdom pursues ambitious domestic transformation.

Foreign exchange reserves stood at $467 billion as of March 2025, representing over 30 months of import cover and providing substantial liquidity to defend the riyal's peg to the US dollar at 3.75 SAR/USD. The Saudi Central Bank (SAMA) manages these reserves conservatively, predominantly in US Treasury securities and other high-quality sovereign debt, ensuring both security and liquidity. Beyond official reserves, the Public Investment Fund (PIF) controls an estimated $700 billion in assets under management, including substantial foreign holdings that contribute to the Kingdom's overall external creditor position. These sovereign wealth resources are increasingly being repatriated and deployed domestically to finance Vision 2030 megaprojects, representing a strategic shift from external asset accumulation to domestic capital formation.

Current account dynamics reflecting structural transformation

Saudi Arabia recorded a current account surplus of 6.3% of GDP in 2024, supported by oil export revenues averaging $82 per barrel for Brent crude and sustained non-oil export growth. The surplus has narrowed from the double-digit levels observed in 2021-2022 during the post-pandemic oil price surge, reflecting both moderated oil prices and rising import demand associated with Vision 2030 construction activity. Merchandise exports remain heavily concentrated in hydrocarbons, with crude oil and refined products accounting for approximately 75% of total exports, though petrochemical exports have grown to represent nearly 15% of the total. Services imports have increased substantially, driven by technology transfers, engineering consultancy, and tourism-related expenditures as the Kingdom develops its non-oil sectors.

The IMF projects a dramatic shift in Saudi Arabia's external position over the medium term, forecasting the current account balance to deteriorate to a deficit of 44.9% of GDP by 2030. This projection reflects the anticipated fiscal expansion required to complete Vision 2030 infrastructure investments, including NEOM, the Red Sea Project, and Qiddiya entertainment city, alongside assumptions of moderate oil prices and continued OPEC+ production discipline. Whilst such a substantial current account deficit would represent a significant structural shift, Saudi Arabia's exceptional starting position provides ample capacity to finance this transformation through orderly drawdown of external assets. The Kingdom's ability to sustain large deficits without compromising external stability distinguishes it from most emerging market peers and reflects the credibility afforded by its accumulated wealth.

External vulnerabilities remain manageable despite concentration risks

Despite the Kingdom's formidable external buffers, several vulnerabilities warrant monitoring. Oil price volatility remains the primary external risk, with government revenues and export earnings highly sensitive to global energy market dynamics. A sustained decline in oil prices below $70 per barrel would pressure both fiscal and external balances, potentially accelerating reserve drawdown and complicating Vision 2030 financing. The Kingdom's external debt remains modest at approximately 35% of GDP, predominantly comprising Saudi Aramco's international bond issuances and government Eurobonds, with comfortable debt service ratios given the substantial asset base. However, the planned increase in external borrowing to finance diversification investments will gradually raise external financing requirements.

Geopolitical risks, including regional tensions with Iran and potential disruption to oil export routes through the Strait of Hormuz, represent tail risks to external stability, though Saudi Arabia has demonstrated resilience through previous episodes of regional instability. The concentration of foreign assets in US dollar-denominated securities creates currency risk should the dollar depreciate significantly, though this exposure is partially offset by the riyal's dollar peg. Climate transition risks pose a longer-term structural challenge to the external position, as global decarbonisation efforts may permanently reduce demand for hydrocarbon exports beyond the 2030 horizon. The Kingdom's strategy of investing oil wealth into domestic productive capacity and international assets aims to mitigate this secular risk, though execution remains critical to maintaining external strength through the energy transition.

Credit Strengths & Vulnerabilities

Strengths

Saudi Arabia's sovereign credit profile is underpinned by exceptional financial buffers that provide substantial resilience against external shocks. The Kingdom's foreign exchange reserves stood at $467 billion as of March 2025, representing coverage of over 30 months of imports—a level that significantly exceeds typical adequacy metrics and positions Saudi Arabia amongst the most liquid emerging market sovereigns. This substantial reserve position, combined with the assets held by the Public Investment Fund and other sovereign wealth vehicles, provides the government with considerable fiscal flexibility to navigate periods of oil market volatility or geopolitical stress.

The fiscal position has strengthened markedly following the consolidation efforts initiated in 2020. Government debt remains moderate at 25.4% of GDP in the first quarter of 2025, having declined from 30.0% in 2020, whilst the fiscal deficit narrowed substantially to 1.2% of GDP in 2024 from 4.2% the previous year. This improvement reflects both higher oil revenues and the government's success in implementing structural fiscal reforms, including the introduction of value-added taxation at 15%, the reduction of energy subsidies, and enhanced spending efficiency across government departments. The current account surplus of 6.3% of GDP in 2024 further demonstrates the Kingdom's strong external position.

Progress in economic diversification, whilst still at an early stage, has begun to yield tangible results that enhance the medium-term growth outlook. The non-oil economy expanded by 4.8% in 2024, outpacing overall GDP growth and demonstrating that Vision 2030 initiatives are gaining traction beyond the hydrocarbon sector. Private sector growth reached 5.1% in the fourth quarter of 2024, marking the strongest quarterly performance since 2019 and suggesting that structural reforms are beginning to stimulate entrepreneurial activity and investment outside the traditional oil economy. The reduction in oil revenues as a proportion of total government revenue—from 77% in 2018 to 65% in 2024—whilst still indicating heavy hydrocarbon dependence, nonetheless signals meaningful progress towards a more balanced revenue structure.

Political stability under the consolidated leadership of Crown Prince Mohammed bin Salman provides policy continuity and decisive implementation of the Vision 2030 reform agenda. The domestic political environment remains stable despite regional tensions, with social reforms including expanded women's rights, tourism sector development, and entertainment industry growth generally increasing popular support, particularly amongst the Kingdom's young population with a median age of 31 years. The government's capacity to implement ambitious structural reforms without significant domestic opposition represents a distinct advantage relative to many emerging market peers facing political fragmentation or reform fatigue.

Vulnerabilities

The Saudi economy remains fundamentally dependent on hydrocarbon revenues despite diversification efforts, creating substantial vulnerability to oil price volatility and the global energy transition. Oil revenues continue to account for 65% of government income, whilst the petroleum sector dominates export earnings and overall economic activity. Average production of 9.0 million barrels per day in 2024, constrained by OPEC+ agreements despite capacity of 12.3 million barrels per day, illustrates the Kingdom's exposure to collective production management decisions that may not always align with domestic fiscal requirements. The government's fiscal breakeven oil price, whilst declining, remains above current market levels, creating ongoing pressure on the budget balance during periods of softer crude prices.

The ambitious scale of Vision 2030 projects, particularly mega-developments such as NEOM's $500 billion investment programme, presents execution risks and places considerable demands on fiscal resources. Whilst these initiatives are essential to the diversification strategy, their successful implementation requires sustained capital deployment over extended timeframes, coordination across multiple government entities, and the attraction of substantial private sector and foreign direct investment. Any significant delays, cost overruns, or shortfalls in private capital mobilisation could strain public finances and undermine confidence in the reform programme. The concentration of decision-making authority and the rapid pace of change also create potential governance and implementation challenges.

Regional geopolitical tensions, particularly the ongoing rivalry with Iran and continued involvement in Yemen, pose persistent security risks that could escalate and impact economic activity or investor confidence. Whilst the domestic security situation has improved markedly in recent years, the Kingdom's position in a volatile region creates exposure to potential conflict spillovers, attacks on critical infrastructure, or disruptions to regional trade and investment flows. The recent steps towards normalisation with Israel, whilst potentially beneficial economically, remain conditional and could generate domestic or regional opposition if perceived as insufficiently addressing Palestinian concerns.

The labour market structure, characterised by high youth unemployment amongst Saudi nationals and continued dependence on expatriate workers in key sectors, represents a structural vulnerability that could generate social pressures if not adequately addressed. Despite efforts to increase private sector employment of citizens through Saudisation policies, meaningful progress has been uneven, with many nationals still preferring public sector positions. The need to create sufficient quality employment opportunities for a growing young population whilst simultaneously reducing the public sector wage bill creates a challenging policy dilemma that will require sustained attention and innovative solutions.

Opportunities

Accelerating momentum in Vision 2030 implementation creates potential for faster-than-anticipated diversification gains that could materially strengthen the Kingdom's credit profile over the medium term. The opening of NEOM's first hotel in late 2024 and the commencement of THE LINE construction demonstrate that flagship projects are progressing from planning to execution phases. Success in attracting private capital and international partnerships to these developments could catalyse broader economic transformation, generate new revenue streams, and reduce hydrocarbon dependence more rapidly than currently projected. The expansion of the tourism sector, supported by the new e-visa system launched in 2024, offers particular promise given Saudi Arabia's religious tourism advantages and emerging leisure destinations.

Saudi Aramco's downstream expansion strategy, including the $7 billion petrochemical complex in South Korea announced in January 2025, positions the Kingdom to capture greater value from its hydrocarbon resources through vertical integration. This approach of moving up the value chain into refining, petrochemicals, and speciality products offers the potential to maintain strong revenues from the oil sector even as global crude demand potentially plateaus, whilst simultaneously developing industrial capabilities and employment opportunities domestically. The company's exceptional profitability, with $123.8 billion in earnings during 2024 representing the second-highest annual profit ever recorded, provides substantial resources to fund both upstream capacity maintenance and downstream diversification.

Regional economic integration initiatives, including the development of transport corridors, digital infrastructure, and financial market linkages across the Gulf Cooperation Council, could enhance Saudi Arabia's position as a regional economic hub. The Kingdom's large domestic market, strategic location between Asia, Europe, and Africa, and substantial investment capacity position it to benefit disproportionately from deeper regional integration. Progress towards full normalisation with Israel, should it materialise, could unlock additional trade, investment, and technology transfer opportunities that would support diversification objectives.

The global focus on energy security following recent geopolitical disruptions has reinforced the strategic importance of reliable suppliers such as Saudi Arabia, potentially supporting sustained demand for the Kingdom's crude exports and strengthening its diplomatic influence. The Kingdom's spare production capacity and its leadership role in OPEC+ provide leverage in global energy markets that can be deployed to support both economic and foreign policy objectives.

Threats

The accelerating global energy transition towards renewable sources and electric vehicles poses an existential long-term threat to the economic model that has underpinned Saudi prosperity for decades. Whilst oil demand continues to grow in the near term, particularly in Asia, the trajectory of technological change and climate policy suggests that peak demand could occur within the next decade, potentially stranding hydrocarbon assets and undermining the fiscal foundation of the Saudi state before diversification efforts have sufficiently matured. The risk that Vision 2030 initiatives may not generate adequate alternative revenue sources quickly enough to offset declining oil income represents the most significant structural challenge facing the Kingdom's credit profile over the medium to long term.

Escalation of regional conflicts, particularly involving Iran, could directly threaten critical oil infrastructure and disrupt the production and export capabilities upon which government finances depend. The September 2019 attacks on Aramco facilities at Abqaiq and Khurais, which temporarily removed approximately half of Saudi production capacity, demonstrated the vulnerability of concentrated infrastructure to precision strikes. Any sustained disruption to oil exports would simultaneously reduce government revenues whilst potentially requiring increased security and military expenditures, creating a severe fiscal squeeze. Broader regional instability could also deter the foreign investment and international partnerships that are essential to Vision 2030's success.

Domestic social pressures could emerge if economic reforms fail to deliver improved living standards and employment opportunities for the growing youth population, particularly if oil revenues decline and necessitate fiscal austerity measures. Whilst recent social liberalisation has generally been well-received, the absence of political reforms and channels for public participation in governance creates potential for discontent if economic expectations are disappointed. The government's legitimacy increasingly rests on its ability to deliver prosperity and modernisation rather than traditional sources of authority, raising the stakes for successful reform implementation.

Global financial market conditions, including potential increases in borrowing costs or reduced appetite for emerging market debt, could constrain the Kingdom's ability to finance Vision 2030 projects through international capital markets. Whilst current debt levels remain moderate and the government retains substantial reserves, the scale of planned investments may require periodic recourse to external financing. Any significant deterioration in market access or increase in funding costs could necessitate project delays or reprioritisation that would slow diversification progress and potentially undermine confidence in the reform programme.

Economic Analysis

The Saudi Arabian economy has demonstrated notable structural evolution over the assessment period, with growth dynamics increasingly reflecting the Kingdom's deliberate pivot towards non-hydrocarbon sectors. Whilst the oil industry retains its position as the primary economic engine, the expanding contribution of alternative sectors represents a fundamental shift in the composition of national output that merits careful examination.

Growth dynamics and sectoral transformation

The Kingdom's economic trajectory over recent years illustrates the complex interplay between traditional hydrocarbon dependence and emerging diversification. The exceptional 8.7% expansion recorded in 2022 was predominantly attributable to elevated oil production and favourable pricing conditions, reflecting Saudi Arabia's capacity to leverage its position within global energy markets. However, the subsequent deceleration to 0.8% growth in 2023 underscored the vulnerability inherent in petroleum-centric economic models, as OPEC+ production restraints and softer global demand constrained the oil sector's contribution.

The recovery to 2.7% growth in 2024 marked a pivotal inflection point in the Kingdom's economic narrative. The non-oil economy's robust 4.8% expansion during this period significantly outpaced aggregate GDP growth, providing compelling evidence that Vision 2030 initiatives are beginning to generate tangible economic dividends. This divergence between oil and non-oil sector performance represents precisely the structural rebalancing that policymakers have sought to engineer since the programme's inception.

Particularly encouraging was the acceleration of private sector activity, which achieved 5.1% growth in the fourth quarter of 2024—the strongest quarterly performance since 2019. This private sector dynamism suggests that government-led investment programmes are successfully catalysing broader economic participation beyond state-directed projects. The expansion reflects increased activity across construction, retail trade, hospitality, and financial services, sectors that have benefited from regulatory reforms, infrastructure investment, and evolving consumer preferences amongst the Kingdom's youthful population.

The forward projection of 3.2% to 4.0% growth for 2025 appears credible given current momentum, though this outlook remains contingent upon sustained non-oil sector expansion compensating for continued oil production discipline. The Kingdom's ability to maintain growth within this range whilst adhering to OPEC+ commitments would represent a significant achievement in economic rebalancing.

Inflation dynamics and price stability

Saudi Arabia's inflation profile has remained remarkably benign throughout the assessment period, particularly when contextualised against the elevated price pressures experienced across advanced and emerging economies following the pandemic. The 2.5% inflation rate recorded in 2023 and the modest increase to 3.2% in 2024 reflect the Kingdom's unique economic characteristics, including the riyal's peg to the US dollar, substantial government subsidies for essential goods and services, and relatively limited exposure to global supply chain disruptions.

The subsequent moderation to an annualised 2.8% in the first quarter of 2025 suggests that inflationary pressures remain well-contained within the Saudi Central Bank's comfort zone. This price stability owes much to the currency peg, which effectively imports US monetary policy whilst insulating the Kingdom from exchange rate volatility. The peg has proven particularly advantageous during periods of dollar strength, anchoring inflation expectations and facilitating long-term economic planning.

Housing costs, which constitute a significant component of the consumer price index, have experienced upward pressure due to population growth, urbanisation, and increased economic activity associated with Vision 2030 projects. However, government initiatives to expand affordable housing supply have partially offset these pressures. Food price inflation has remained subdued due to continued subsidies and the Kingdom's substantial import capacity, supported by its formidable foreign exchange reserves.

The controlled inflation environment has afforded policymakers considerable flexibility in maintaining accommodative monetary conditions to support non-oil sector growth. This represents a marked advantage relative to many emerging market peers that have confronted the difficult trade-off between supporting growth and containing inflation.

Monetary policy framework and financial conditions

The Saudi Central Bank's monetary policy stance remains fundamentally constrained by the riyal's fixed exchange rate regime, which pegs the currency at 3.75 riyals per US dollar. This arrangement necessitates that domestic interest rates broadly track US Federal Reserve policy to maintain the peg's credibility and prevent destabilising capital flows. Consequently, the Saudi Central Bank has mirrored Federal Reserve rate adjustments, with the repo rate standing at levels consistent with US policy rates as of early 2025.

Despite this constraint, the monetary authority has demonstrated considerable skill in employing macroprudential tools and liquidity management operations to influence domestic credit conditions. The banking sector remains well-capitalised with an average capital adequacy ratio exceeding 18%, providing substantial capacity to support lending growth. Credit to the private sector expanded by approximately 11% in 2024, reflecting both robust demand for financing and banks' willingness to extend credit in an improving economic environment.

The financial sector has benefited from the government's deliberate efforts to deepen capital markets and expand the range of available financial instruments. The Tadawul stock exchange has attracted increased international participation following the Kingdom's inclusion in major emerging market indices, whilst the domestic bond market has developed considerably as both government entities and corporates have accessed debt financing. These developments have enhanced financial intermediation efficiency and reduced the economy's historical dependence on bank lending as the primary credit channel.

Liquidity conditions within the banking system have remained comfortable, supported by substantial government deposits and the repatriation of foreign assets by both public and private sector entities to fund domestic investment opportunities. This ample liquidity has facilitated competitive lending rates and supported the transmission of accommodative monetary conditions to the real economy.

The current account surplus of 6.3% of GDP recorded in 2024 reflects the Kingdom's continued external strength, driven by oil export revenues that substantially exceed import requirements despite elevated capital goods imports for Vision 2030 projects. The foreign exchange reserves of $467 billion as of March 2025 provide exceptional external buffers, covering over 30 months of imports and representing approximately 45% of GDP. These reserves afford the monetary authority substantial capacity to defend the currency peg against speculative pressures whilst providing confidence to international investors regarding the Kingdom's external stability.

Looking forward, the monetary policy framework is likely to remain anchored by the dollar peg, which continues to serve the Kingdom's interests by providing nominal stability and facilitating its integration into global financial markets. However, the authorities have demonstrated increasing sophistication in deploying complementary policy tools to influence domestic financial conditions, suggesting that the effective policy space may be broader than the formal exchange rate constraint might imply.

Political & Institutional Assessment

Governance Structure and Political Stability

Saudi Arabia operates as an absolute monarchy under the House of Saud, with political authority concentrated within the royal family and exercised through a system of consensus amongst senior princes. King Salman bin Abdulaziz, aged 89, retains formal sovereignty whilst increasingly delegating executive authority to Crown Prince Mohammed bin Salman (MBS), who functions as the de facto ruler and principal architect of the Kingdom's economic transformation agenda. The Crown Prince has systematically consolidated control across governmental, military, and economic institutions since his appointment in 2017, creating a highly centralised decision-making structure that enables rapid policy implementation but concentrates political risk.

The domestic political environment remains stable, underpinned by substantial hydrocarbon wealth, an extensive welfare system, and the legitimacy derived from the monarchy's custodianship of Islam's two holiest sites. The median age of 31 years characterises a predominantly young population that has generally responded favourably to the government's ambitious social reform programme. These reforms represent a significant departure from the Kingdom's historically conservative social policies and include the expansion of women's rights encompassing driving privileges, independent travel, and enhanced employment opportunities. The development of a domestic entertainment sector, marked by the introduction of cinemas, international concerts, and major sporting events, alongside the launch of a streamlined e-visa system in 2024 to facilitate tourism, demonstrates the leadership's commitment to social modernisation.

The government has strategically reduced the enforcement powers of the religious police, signalling a recalibration of the relationship between state authority and religious conservatism. Whilst these social and economic reforms have accelerated, political reforms have progressed more cautiously, with limited expansion of public participation in governance structures. The Consultative Assembly (Majlis al-Shura) remains an appointed advisory body without legislative authority, and civil society organisations operate within tightly defined parameters.

Regional Dynamics and Foreign Policy

Saudi Arabia's external environment is characterised by persistent regional tensions, particularly with Iran, which manifest through proxy conflicts and competing spheres of influence across the Middle East. The Kingdom's military involvement in Yemen, though reduced from peak levels, continues to present fiscal costs and reputational challenges. However, the leadership has demonstrated pragmatic diplomatic flexibility, exemplified by the Chinese-brokered rapprochement with Iran in 2023 and the ongoing normalisation process with Israel. Full diplomatic relations with Israel remain contingent upon substantive progress towards a Palestinian state, reflecting the Kingdom's need to balance strategic interests with domestic and broader Arab public opinion.

The Kingdom's foreign policy increasingly emphasises economic diplomacy and investment partnerships as instruments of influence, aligning with Vision 2030's diversification objectives. Saudi Arabia has strengthened ties with Asian economies, particularly China and India, whilst maintaining its strategic security partnership with the United States despite periodic tensions over energy policy and human rights concerns.

Institutional Capacity and Policy Effectiveness

The Saudi government has demonstrated enhanced institutional capacity in implementing complex economic reforms, evidenced by the successful introduction of value-added taxation at 15 per cent, the reduction of energy subsidies, and improved public spending efficiency. These measures contributed to fiscal consolidation that reduced the debt-to-GDP ratio from 30.0 per cent in 2020 to 25.4 per cent in the first quarter of 2025, whilst narrowing the fiscal deficit from 4.2 per cent of GDP in 2023 to 1.2 per cent in 2024.

The centralisation of authority under the Crown Prince has facilitated decisive policymaking and reduced bureaucratic impediments to reform implementation. However, this concentration of power also introduces succession uncertainty and limits institutional checks on executive decision-making. The establishment of new governmental entities focused on Vision 2030 delivery, including sector-specific development authorities, has created parallel structures that enhance project execution capacity but may generate coordination challenges with traditional ministries.

The Saudi Central Bank maintains credibility in monetary policy management, with inflation contained at moderate levels—3.2 per cent in 2024 and 2.8 per cent annualised in the first quarter of 2025—within the institution's target range. The riyal's peg to the US dollar, maintained since 1986, provides nominal stability and is supported by substantial foreign exchange reserves of $467 billion as of March 2025, covering over 30 months of imports.

Governance Risks and Reform Trajectory

Whilst the Kingdom's governance framework enables rapid policy implementation, it remains vulnerable to key person risk given the concentration of authority and the absence of institutionalised succession mechanisms beyond royal family consensus. The pace and scope of social reforms, though popular amongst younger demographics, have generated tensions with conservative elements within society and the religious establishment, requiring careful political management.

The government's capacity to sustain reform momentum depends substantially on hydrocarbon revenues, which constituted 65 per cent of government revenue in 2024 despite declining from 77 per cent in 2018. This ongoing fiscal dependence on oil exposes the reform programme to commodity price volatility, though substantial financial buffers provide resilience against temporary shocks. The leadership's commitment to economic diversification appears credible, supported by significant capital allocation to Vision 2030 projects and structural reforms that have enabled non-oil GDP growth of 4.8 per cent in 2024, outpacing overall economic expansion.

Banking Sector & Financial Stability

The Saudi banking sector has demonstrated considerable resilience and robust capitalisation throughout the recent period of economic transformation, maintaining its position as one of the most stable and well-regulated financial systems in the Gulf region. The sector's strength provides critical support to the Kingdom's ambitious diversification agenda whilst managing the inherent risks associated with continued dependence on hydrocarbon revenues.

Sector fundamentals and capitalisation

Saudi Arabia's banking system comprises twelve domestic banks and eleven foreign bank branches, with total assets reaching SAR 3.8 trillion (approximately $1.0 trillion) as of December 2024, representing roughly 100% of GDP. The sector remains highly concentrated, with the five largest institutions accounting for approximately 70% of total banking assets. The National Commercial Bank (now SNB following its merger with Samba Financial Group in 2021), Al Rajhi Bank, and Riyad Bank dominate the retail and corporate banking landscape.

Capital adequacy ratios across the sector remain substantially above regulatory minimums, with the aggregate Capital Adequacy Ratio standing at 19.8% as of Q4 2024, well above the Saudi Central Bank's (SAMA) minimum requirement of 12.5%. Tier 1 capital ratios averaged 17.2% across the sector, reflecting conservative capital management and SAMA's prudent supervisory approach. The sector's strong capitalisation provides substantial buffers against potential credit losses and supports continued lending growth to the non-oil economy.

Return on equity for the banking sector improved to 14.3% in 2024, up from 12.8% in 2023, driven by higher net interest margins following global interest rate increases and robust growth in fee-based income. Net interest margins expanded to 3.1% in 2024 from 2.8% in the previous year, benefiting from the Saudi riyal's peg to the US dollar and corresponding alignment with Federal Reserve monetary policy.

Asset quality and credit growth

Non-performing loan ratios have remained remarkably stable despite the economic volatility of recent years, standing at 1.6% of total loans as of December 2024, marginally improved from 1.8% at year-end 2023. This compares favourably with regional peers and reflects both the quality of Saudi Arabia's credit culture and SAMA's stringent provisioning requirements. Loan loss coverage ratios remained robust at 178%, providing substantial protection against potential deterioration in asset quality.

Total credit to the private sector grew by 11.2% year-on-year in 2024, the strongest growth rate since 2019, with particularly robust expansion in construction and real estate lending (up 15.3%), reflecting the acceleration of Vision 2030 megaprojects. Consumer lending, which comprises approximately 35% of total credit, grew by 8.7%, supported by rising employment levels and continued improvement in household confidence. Corporate lending to non-oil sectors expanded by 12.8%, demonstrating the banking sector's critical role in financing economic diversification.

Liquidity and funding dynamics

The Saudi banking sector maintains comfortable liquidity positions, with the loan-to-deposit ratio standing at 83.4% as of December 2024, providing substantial capacity for further credit expansion. Customer deposits, which constitute approximately 75% of total funding, grew by 9.3% in 2024, reflecting both increased government spending on Vision 2030 projects and rising private sector savings. The sector's reliance on wholesale funding remains limited, reducing vulnerability to external funding shocks.

SAMA's substantial foreign exchange reserves of $467 billion as of March 2025 provide an additional layer of systemic stability, ensuring the credibility of the riyal's peg to the US dollar and supporting confidence in the banking system. The central bank has demonstrated its willingness to inject liquidity when needed, having provided targeted support during the 2020 pandemic-related disruptions.

Regulatory environment and supervision

SAMA maintains a reputation as one of the region's most effective banking supervisors, implementing Basel III standards comprehensively and often exceeding international minimum requirements. The regulator has introduced several prudential measures in recent years, including enhanced stress testing requirements, stricter large exposure limits, and improved corporate governance standards for banking institutions.

The introduction of open banking regulations in 2024 represents a significant modernisation of the regulatory framework, facilitating greater competition and innovation whilst maintaining robust consumer protection standards. SAMA has also accelerated the licensing of fintech companies, with over 80 entities now operating under various regulatory sandboxes, supporting the Kingdom's ambitions to become a regional financial technology hub.

Risks and vulnerabilities

Despite the sector's overall strength, several vulnerabilities warrant monitoring. The banking system's exposure to government-related entities and Vision 2030 megaprojects has increased substantially, with estimates suggesting that such exposures now comprise approximately 25-30% of total corporate lending. Whilst these projects benefit from explicit or implicit government support, delays or scope reductions could create asset quality pressures.

The sector's profitability remains sensitive to oil price volatility through both direct exposures to hydrocarbon-related corporates and indirect effects on government spending and overall economic activity. A sustained period of oil prices below $70 per barrel would likely pressure asset quality and credit growth, though the sector's strong capital buffers provide substantial absorption capacity.

Concentration risk remains elevated, with the five largest borrowing groups accounting for a significant portion of corporate exposures at most major banks. SAMA's large exposure limits provide some mitigation, but the relatively small number of large-scale private sector enterprises in the Kingdom limits diversification opportunities.

The rapid growth in real estate and construction lending, whilst supporting Vision 2030 objectives, has created potential vulnerabilities should property markets experience corrections. SAMA has implemented macroprudential measures including loan-to-value limits on mortgage lending, but continued vigilance is warranted given the scale of ongoing property development.

Digital transformation and innovation

Saudi banks have made substantial progress in digital transformation, with mobile and internet banking penetration rates exceeding 85% of the adult population as of 2024. Investment in technology infrastructure reached SAR 4.2 billion in 2024, up 18% from the previous year, as institutions compete to enhance customer experience and operational efficiency.

The emergence of digital-only banks, including STC Bank (launched in 2022) and D360 Bank (launched in 2024), has intensified competitive dynamics and accelerated innovation across the sector. Traditional banks have responded by substantially upgrading their digital capabilities, with several institutions now offering comprehensive digital onboarding and lending services.

The sector's embrace of financial technology extends to blockchain applications, with several banks participating in pilot programmes for cross-border payments and trade finance digitalisation. These initiatives position Saudi Arabia's banking sector favourably for the evolving regional and global financial landscape, though cyber security risks have correspondingly increased.

Outlook & Scenarios

Short-Term Outlook (12 months)

Saudi Arabia's near-term economic trajectory appears favourable, underpinned by robust non-oil sector momentum and stabilising hydrocarbon revenues. Over the next twelve months, we anticipate GDP growth to settle within the 3.2-4.0% range, driven primarily by continued expansion in the private sector and accelerating Vision 2030-related investments. The non-oil economy should maintain its growth trajectory above 4.5%, supported by increased tourism receipts, construction activity linked to mega-projects, and expanding manufacturing capacity. The Kingdom's fiscal position is expected to strengthen further, with the budget deficit likely narrowing to below 1.0% of GDP by year-end 2026, assuming Brent crude prices remain within the $75-85 per barrel range. This consolidation reflects both improved revenue collection through enhanced tax administration and continued expenditure discipline, particularly in recurrent spending categories.

The external position should remain comfortably in surplus, with the current account balance projected at 5.5-6.5% of GDP, providing continued support for foreign exchange reserves which are expected to stabilise around $470-480 billion. Inflation pressures are likely to remain contained within the 2.5-3.5% band, though upside risks exist from housing costs in major urban centres and potential pass-through effects from global commodity price movements. The Saudi riyal's peg to the US dollar remains unquestionably credible, backed by substantial reserve buffers and the Saudi Central Bank's demonstrated commitment to the exchange rate regime. Political stability should persist under Crown Prince Mohammed bin Salman's leadership, though regional geopolitical tensions—particularly concerning Iran and Yemen—warrant continued monitoring as potential sources of external shock.

Medium-Term Outlook (1-3 years)

The medium-term outlook for Saudi Arabia centres on the Kingdom's ability to sustain diversification momentum whilst managing the inherent challenges of structural economic transformation. Between 2026 and 2028, we expect the non-oil sector to consolidate its position as the primary growth engine, potentially contributing 60-65% of overall GDP expansion compared to approximately 55% currently. This shift reflects the maturation of several Vision 2030 initiatives, including NEOM's initial operational phases, expanded tourism infrastructure following the opening of new Red Sea resorts, and increased foreign direct investment attracted by regulatory reforms and special economic zones. The government's target of raising non-oil revenue to 50% of total receipts by 2028 appears achievable given current trajectory, though success depends critically on continued VAT compliance improvements and the phased introduction of additional revenue measures.

Fiscal sustainability should improve markedly over this horizon, with the debt-to-GDP ratio potentially declining to 20-22% by 2028 under our base case scenario, assuming prudent expenditure management and oil prices averaging $80 per barrel. The Public Investment Fund's expanding portfolio of domestic and international assets—estimated at $700 billion by end-2025—provides an additional fiscal buffer and revenue diversification channel. However, significant execution risks accompany the Kingdom's ambitious infrastructure programme, with total Vision 2030-related capital commitments exceeding $1 trillion. Cost overruns, project delays, or lower-than-anticipated returns on mega-projects could strain fiscal resources and necessitate increased borrowing. The labour market transformation remains perhaps the most critical medium-term challenge, as the government seeks to increase private sector employment of Saudi nationals from current levels around 23% towards the 30% target. Success requires not only job creation but fundamental shifts in educational outcomes, wage expectations, and private sector hiring incentives.

Geopolitical dynamics will continue shaping Saudi Arabia's medium-term trajectory. Normalisation with Israel, should it advance, could unlock additional trade and investment opportunities whilst potentially complicating regional relationships. The Kingdom's evolving relationship with China—evidenced by increasing bilateral trade and investment flows—reflects strategic diversification away from exclusive Western orientation, though the US security partnership remains foundational. Climate transition risks pose longer-term structural challenges to the hydrocarbon-dependent model, though Saudi Arabia's low production costs and expanding petrochemicals focus provide partial mitigation. The Kingdom's stated ambition to achieve net-zero emissions by 2060, whilst maintaining significant oil production, will require substantial investment in carbon capture and renewable energy technologies.

Rating Scenarios

Saudi Arabia's current rating positioning reflects a balance between substantial financial strengths and ongoing structural vulnerabilities related to hydrocarbon dependence. The stable outlook assigned by S&P Global and Moody's, alongside Fitch's positive outlook, suggests limited near-term rating migration risk, though medium-term trajectories could diverge based on diversification progress and fiscal performance.

An upgrade scenario would likely require demonstration of sustained non-oil revenue growth, with the non-oil sector consistently contributing above 55% of GDP and government non-oil revenues reaching 45-50% of total receipts. Specific triggers might include the debt-to-GDP ratio declining below 20% on a sustained basis, coupled with fiscal breakeven oil prices falling below $65 per barrel (currently estimated at $75-80). Successful execution of major Vision 2030 projects with demonstrated economic returns, alongside meaningful progress in labour market nationalisation without compromising private sector competitiveness, would strengthen the case for higher ratings. Fitch's positive outlook suggests the agency views such outcomes as plausible within the next 12-18 months. Additionally, further improvements in governance indicators, including enhanced fiscal transparency and institutional strengthening, could support upward rating momentum towards the AA category occupied by wealthier Gulf peers.

Conversely, a downgrade scenario would most likely emerge from a combination of sustained low oil prices—specifically Brent crude remaining below $65 per barrel for an extended period—and fiscal slippage resulting in the debt-to-GDP ratio rising above 35%. Significant cost overruns or abandonment of key Vision 2030 projects would signal weakening commitment to diversification and could trigger negative rating actions. A sharp deterioration in the regional security environment, particularly direct military conflict with Iran or major escalation in Yemen, would constitute a severe downside risk, potentially disrupting oil exports and necessitating substantial defence expenditures. Domestic political instability, whilst currently assessed as low probability, would fundamentally alter the credit profile given the concentration of decision-making authority. Failure to achieve meaningful progress in private sector job creation for Saudi nationals could necessitate unsustainable public sector expansion, undermining fiscal sustainability. A downgrade would likely see ratings migrate towards the BBB+ to A- range, reflecting increased vulnerability to external shocks and reduced fiscal flexibility.

The base case scenario, which underpins current stable outlooks from S&P and Moody's, assumes oil prices averaging $75-85 per barrel, continued gradual diversification progress with non-oil GDP growth of 4-5% annually, and fiscal deficits remaining below 2% of GDP. Under this scenario, Saudi Arabia maintains its current rating level through 2027-2028, with the debt-to-GDP ratio stabilising around 23-26%. This outcome requires competent execution of Vision 2030 initiatives without major setbacks, sustained political stability, and avoidance of significant regional conflicts. The probability-weighted assessment suggests roughly 60% likelihood of ratings remaining unchanged over the next 24 months, 25% probability of upgrade (primarily from Fitch given its positive outlook), and 15% probability of downgrade stemming from external shocks rather than domestic policy failures.

Conclusion

Saudi Arabia's sovereign credit profile reflects a compelling narrative of economic transformation underpinned by substantial financial buffers and accelerating structural reforms. The Kingdom's solid investment-grade ratings, ranging from A to A1 across the major agencies, appropriately capture both the strengths inherent in its vast hydrocarbon wealth and the challenges associated with its ongoing diversification efforts.

The credit assessment is fundamentally anchored by Saudi Arabia's exceptional financial resilience. Foreign exchange reserves of $467 billion as of March 2025 provide a formidable cushion against external shocks, covering more than 30 months of imports and representing one of the world's largest sovereign reserve positions. This financial strength is complemented by a moderate and declining debt-to-GDP ratio of 25.4%, which compares favourably to most investment-grade sovereigns and provides considerable fiscal headroom for continued investment in economic transformation. The improvement in the fiscal balance to negative 1.2% of GDP in 2024, alongside a healthy current account surplus of 6.3% of GDP, demonstrates effective fiscal management and reduced vulnerability to oil price volatility.

The Kingdom's economic diversification strategy, whilst still in its early stages, is beginning to yield tangible results that support the credit outlook. Non-oil GDP growth of 4.8% in 2024 significantly outpaced overall economic expansion, whilst private sector growth reached 5.1% in the fourth quarter, the strongest quarterly performance since 2019. These figures suggest that Vision 2030 initiatives are gaining genuine economic traction beyond the hydrocarbon sector. The reduction in oil revenues as a proportion of total government receipts from 77% in 2018 to 65% in 2024, though still representing substantial dependence, indicates meaningful progress towards a more balanced revenue structure.

Nevertheless, the credit profile remains constrained by the economy's continued reliance on oil for fiscal sustainability and export earnings. Saudi Aramco's $123.8 billion profit in 2024 and its $97.8 billion dividend payout underscore both the strength and the vulnerability inherent in this dependence. The Kingdom's fiscal breakeven oil price, whilst declining, remains elevated relative to current market prices, necessitating continued production management through OPEC+ coordination. This structural vulnerability to hydrocarbon price cycles represents the primary constraint on the sovereign's creditworthiness and limits the potential for significant rating upgrades in the near term.

The political environment provides both support and complexity to the credit assessment. The concentration of power under Crown Prince Mohammed bin Salman has enabled decisive policy implementation and rapid advancement of Vision 2030 projects, including the ambitious NEOM development. Social reforms have generally strengthened domestic legitimacy amongst the young population, whilst improved regional relations, including the potential normalisation with Israel, reduce geopolitical risk premiums. However, the absence of meaningful political pluralism and the regional security environment, particularly tensions with Iran and ongoing involvement in Yemen, introduce governance and geopolitical risks that temper the credit outlook.

Fitch's positive outlook, contrasting with the stable outlooks from S&P and Moody's, reflects the potential upside scenario in which continued fiscal discipline, accelerating diversification, and successful execution of Vision 2030 projects could warrant rating enhancement. The trajectory towards this outcome will depend critically on the Kingdom's ability to sustain non-oil growth momentum, further reduce fiscal dependence on hydrocarbons, and maintain macroeconomic stability through what is likely to remain a volatile period for global energy markets.

In summary, Saudi Arabia's credit profile represents a strong investment-grade sovereign undertaking an unprecedented economic transformation. The combination of substantial financial resources, improving fiscal metrics, and genuine progress in diversification supports the current rating level and provides a foundation for potential future upgrades. However, the persistence of oil dependence, execution risks associated with ambitious mega-projects, and regional geopolitical complexities ensure that the Kingdom's credit journey remains one requiring careful monitoring and measured assessment of reform implementation against stated objectives.