Panama

Executive Summary

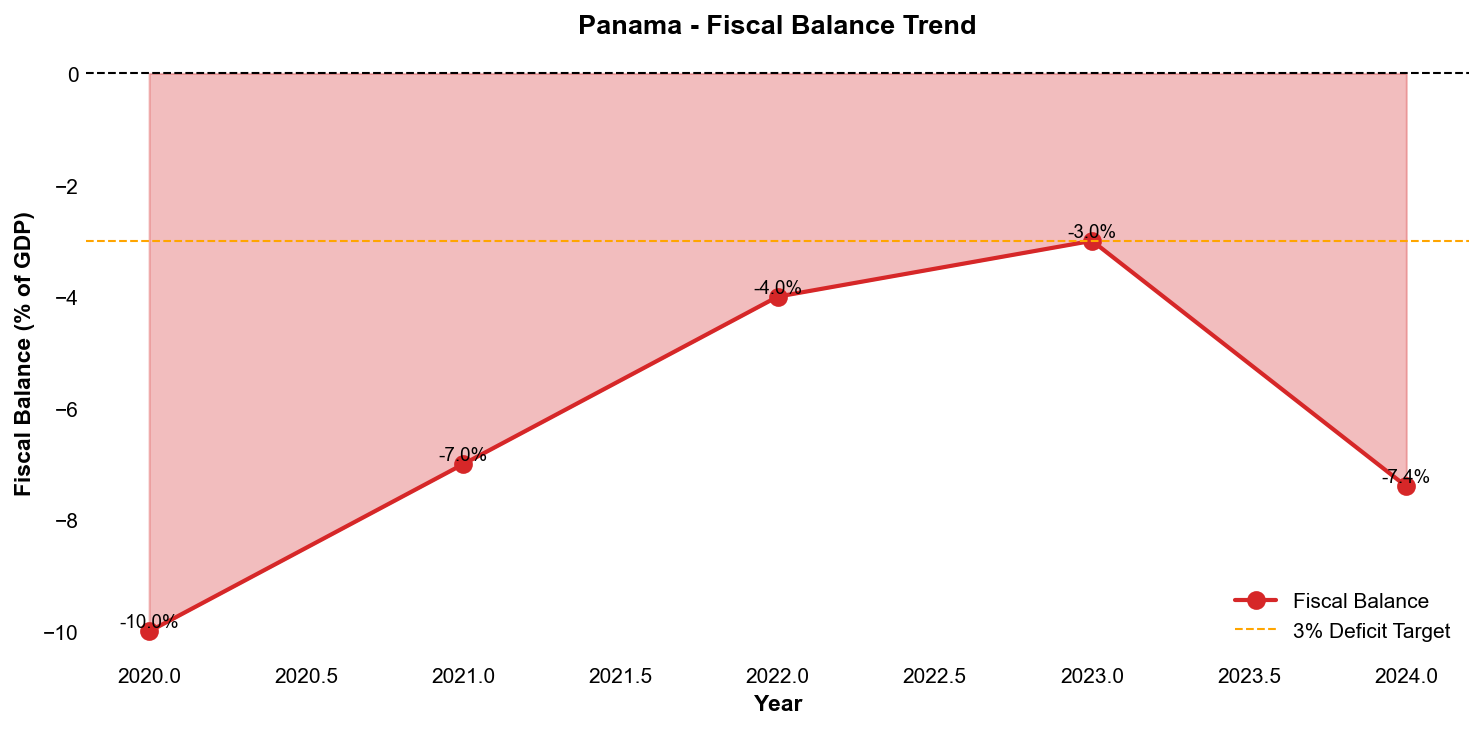

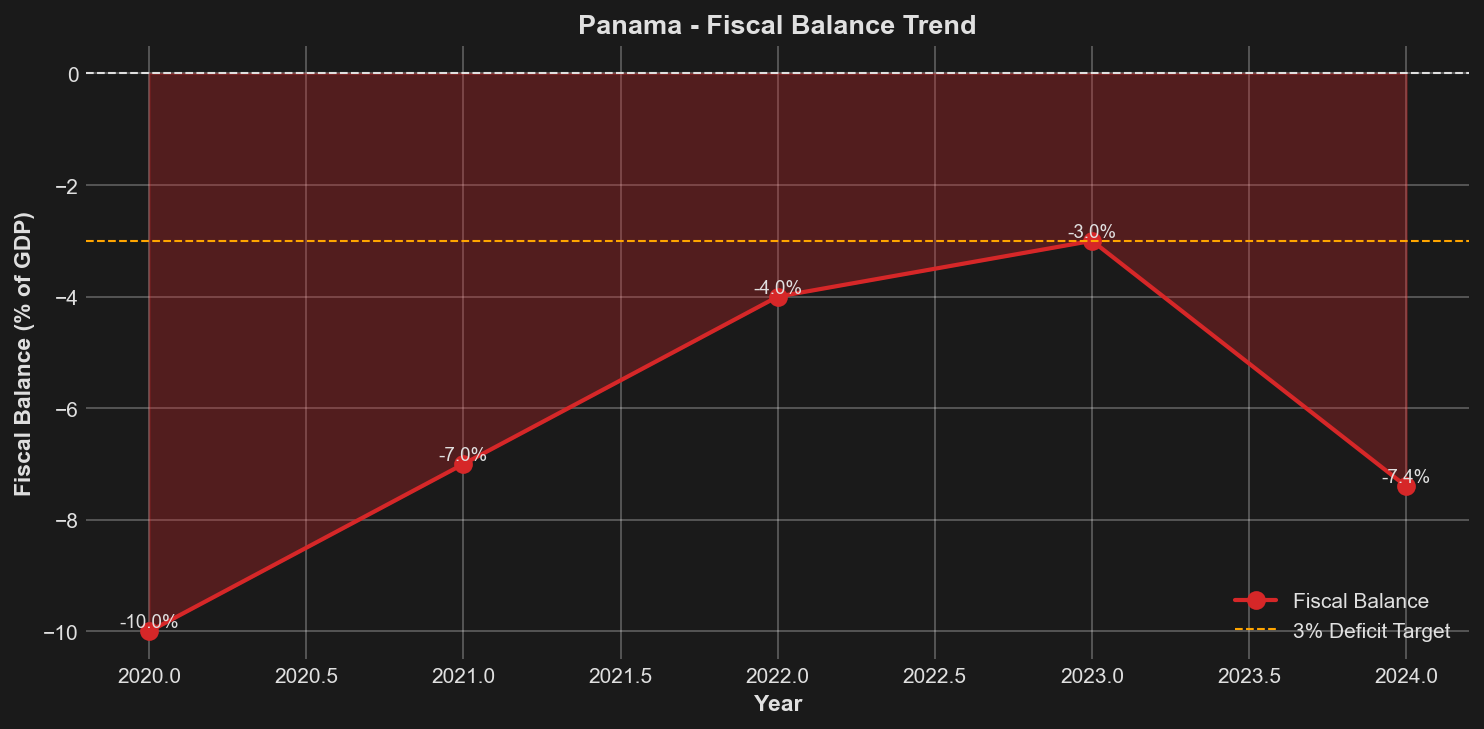

Panama's sovereign credit profile has deteriorated markedly since 2023, with the country now positioned at the threshold of investment grade status. Fitch downgraded Panama to non-investment grade (BB+) in March 2024, whilst S&P and Moody's maintain the lowest tier of investment grade ratings (BBB- and Baa3, respectively) with stable and negative outlooks. The closure of the Cobre Panama copper mine in late 2023—representing approximately 5% of GDP and 7% of current external receipts—following a Supreme Court ruling that invalidated the mining contract, has significantly impacted the country's fiscal and economic trajectory. The debt-to-GDP ratio has risen sharply to 61.6% in 2024, exceeding the median of 56% for similarly rated sovereigns, whilst the fiscal deficit has widened to an estimated -7.4% of GDP, substantially breaching the fiscal rule limit. The interest-to-income ratio has climbed to 19%, well above the peer median of 10%, reflecting increased debt servicing pressures.

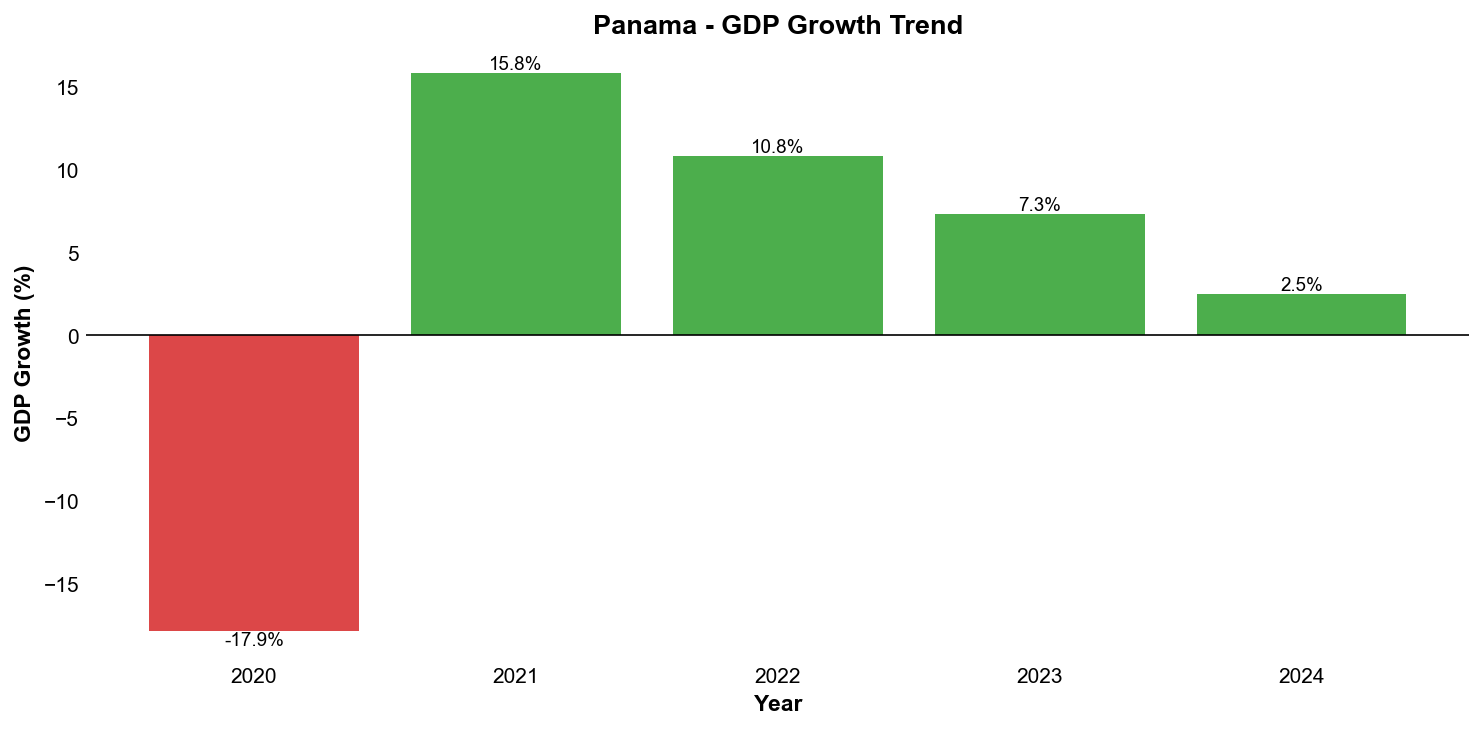

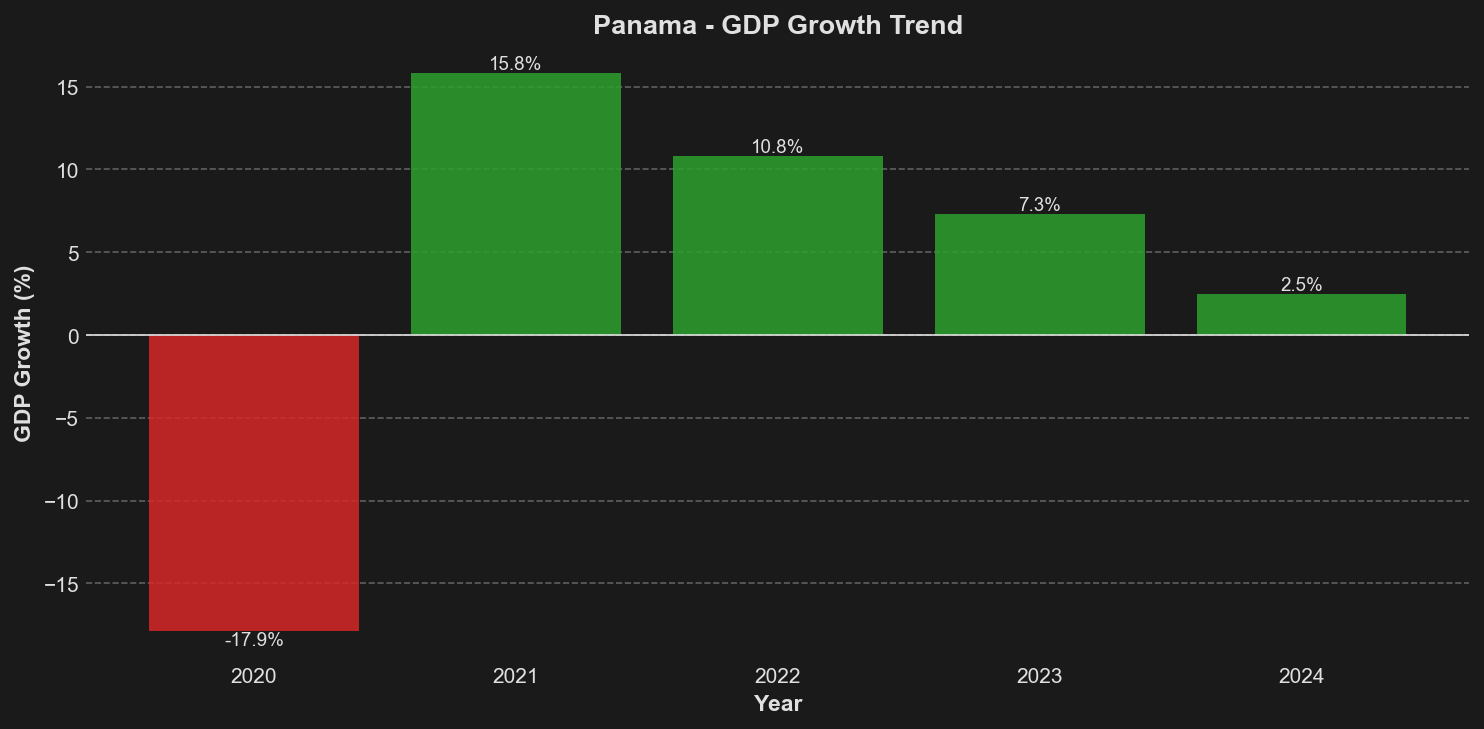

Despite these challenges, Panama retains fundamental credit strengths anchored by its strategic geographic position and control of the Panama Canal, which contributes approximately 6% to GDP. The country's dollarised economy provides monetary stability, with inflation remaining subdued at 1.3% projected for 2024. Panama's banking sector remains robust and well-capitalised, with assets representing 69.8% of GDP, whilst the diversified service-based economy has demonstrated resilience. Following the severe pandemic-induced contraction of -17.9% in 2020, Panama achieved remarkable recovery with GDP growth of 15.8% in 2021, 10.8% in 2022, and 7.3% in 2023. However, growth has decelerated considerably to a projected 2.5% in 2024, reflecting the combined impact of the mine closure and drought conditions affecting Panama Canal operations.

The administration of President José Raúl Mulino, inaugurated in July 2024, confronts substantial fiscal and governance challenges. The government must navigate a fragmented political landscape whilst implementing credible fiscal consolidation measures to restore adherence to fiscal rules and stabilise the debt trajectory. Key priorities include addressing the economic void created by the Cobre Panama mine closure, managing potential contingent liabilities arising from related litigation, and advancing structural reforms to strengthen institutional frameworks. The outlook remains cautious, with Panama's ability to maintain investment grade status with S&P and Moody's contingent upon demonstrable progress in fiscal consolidation, successful implementation of institutional reforms, and resolution of the mining dispute. Failure to achieve meaningful fiscal adjustment could trigger further downgrades, potentially resulting in a complete loss of investment grade status across all major rating agencies.

Ratings Summary

Panama's sovereign credit profile has deteriorated markedly since 2023, with the country now precariously positioned at the threshold of investment grade status. Fitch Ratings took the most decisive action in March 2024, downgrading Panama to non-investment grade at BB+ with a stable outlook, citing persistent fiscal and governance challenges exacerbated by the closure of the Cobre Panama copper mine. S&P Global Ratings followed with a downgrade to BBB- in November 2024, placing Panama at the lowest tier of investment grade, though the agency maintained a stable outlook. Moody's Investors Service has kept its Baa3 rating—equivalent to S&P's BBB-—but revised the outlook to negative in November 2024, signalling heightened downgrade risk. The common themes underpinning these rating actions include sustained fiscal deterioration, with the deficit reaching an estimated 7.4% of GDP in 2024, governance weaknesses, and the substantial economic impact of the Cobre Panama mine closure, which eliminated approximately 5% of GDP and 7% of current external receipts. Rating agencies have expressed particular concern regarding Panama's rising debt burden, which climbed to 61.6% of GDP in 2024, exceeding the median for similarly rated sovereigns, whilst the interest-to-income ratio has increased to 19%, well above the peer median of 10%. The potential for contingent liabilities arising from litigation related to the mine closure adds further uncertainty to the credit outlook.

| Rating Agency | Current Rating | Outlook | Last Action Date |

|---|---|---|---|

| S&P | BBB- | Stable | November 26, 2024 |

| Moody's | Baa3 | Negative | November 29, 2024 |

| Fitch | BB+ | Stable | March 28, 2024 |

Economic Indicators

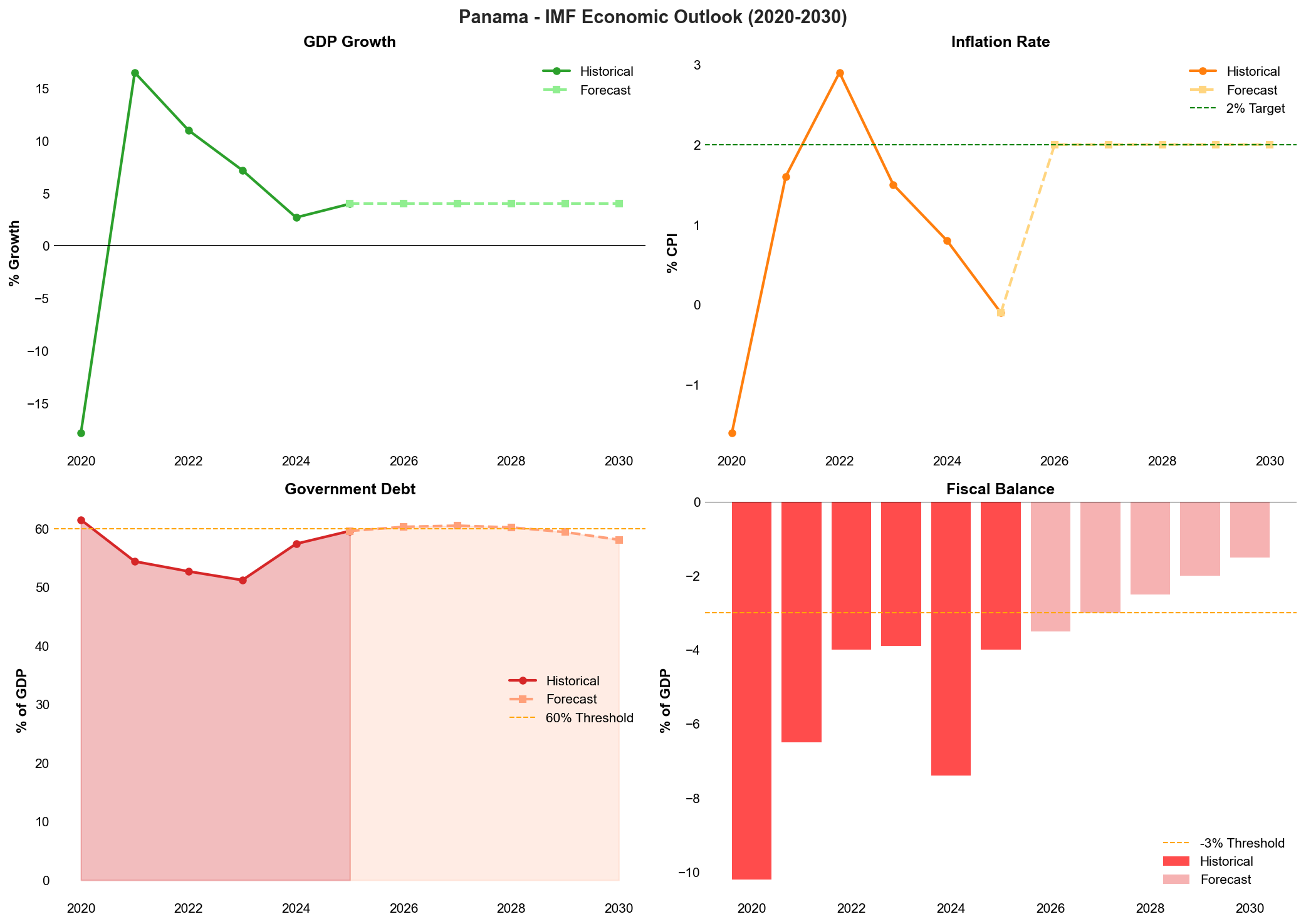

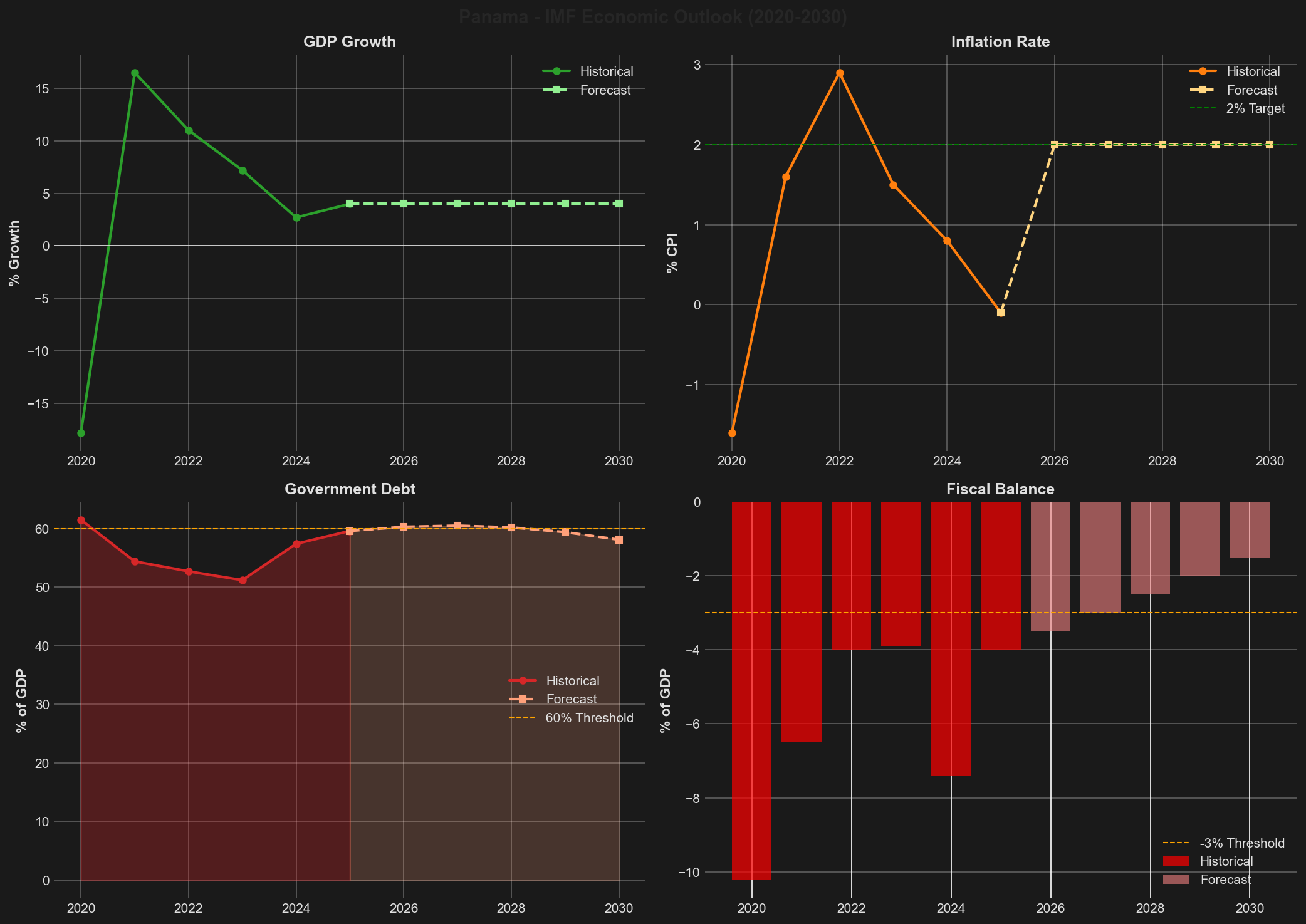

| Indicator | 2021 | 2022 | 2023 | 2024 | 2025F | 2026F |

|---|---|---|---|---|---|---|

| GDP Growth (%) | 16.5% | 11.0% | 7.2% | 2.7% | 4.0% | 4.0% |

| Inflation (%) | 1.6% | 2.9% | 1.5% | 0.8% | -0.1% | 2.0% |

| Unemployment (%) | 11.3% | 9.9% | 7.4% | 9.5% | 8.0% | 7.7% |

| Government Debt (% GDP) | 54.4% | 52.7% | 51.2% | 57.4% | 59.6% | 60.3% |

| Fiscal Balance (% GDP) | -6.5% | -4.0% | -3.9% | -7.4% | -4.0% | -3.5% |

| Current Account (% GDP) | -1.2% | 0.0% | -3.1% | 1.9% | -0.9% | -1.7% |

*Note: 2024 figures marked as (A) for actual data, (E) for estimated data, and (P) for projected data.

Panama's economic trajectory demonstrates a pronounced V-shaped recovery from the severe pandemic-induced contraction, followed by a marked deceleration reflecting structural challenges. The economy experienced an exceptional rebound from the -17.9% contraction in 2020, posting robust growth of 15.8% in 2021 and 10.8% in 2022, driven by the resumption of Panama Canal operations, recovery in logistics and financial services, and the ramp-up of the Cobre Panama copper mine. Growth remained solid at 7.3% in 2023, though the economy began to face headwinds from drought conditions affecting Canal operations. The sharp deceleration to an estimated 2.5% in 2024 reflects the material impact of the Cobre Panama mine closure, which eliminated approximately 5% of GDP, alongside reduced Canal throughput due to persistent water management challenges. IMF projections suggest a gradual recovery trajectory, with growth forecast to reach 4.0% by 2030, contingent upon successful fiscal consolidation and structural reforms.

The fiscal position has deteriorated significantly, reversing the consolidation gains achieved during the post-pandemic recovery period. After peaking at -10.0% of GDP in 2020, the fiscal deficit improved steadily to -3.0% of GDP in 2023 as economic activity normalised and revenues recovered. However, the estimated -7.4% deficit in 2024 represents a substantial setback, driven by the loss of tax revenues and royalties from the Cobre Panama mine, increased social spending pressures, and higher debt servicing costs. This fiscal slippage significantly exceeds Panama's fiscal rule limit and has been a primary driver of recent credit rating downgrades. The debt-to-GDP ratio, which had declined from its pandemic peak of 69.7% to 54.2% by 2023, reversed course to reach an estimated 61.6% in 2024, surpassing the median for similarly rated sovereigns. The IMF projects gradual fiscal consolidation, with the deficit narrowing to -1.5% of GDP and debt stabilising at 58.1% of GDP by 2030, though achieving these targets will require sustained political commitment to expenditure restraint and revenue enhancement measures.

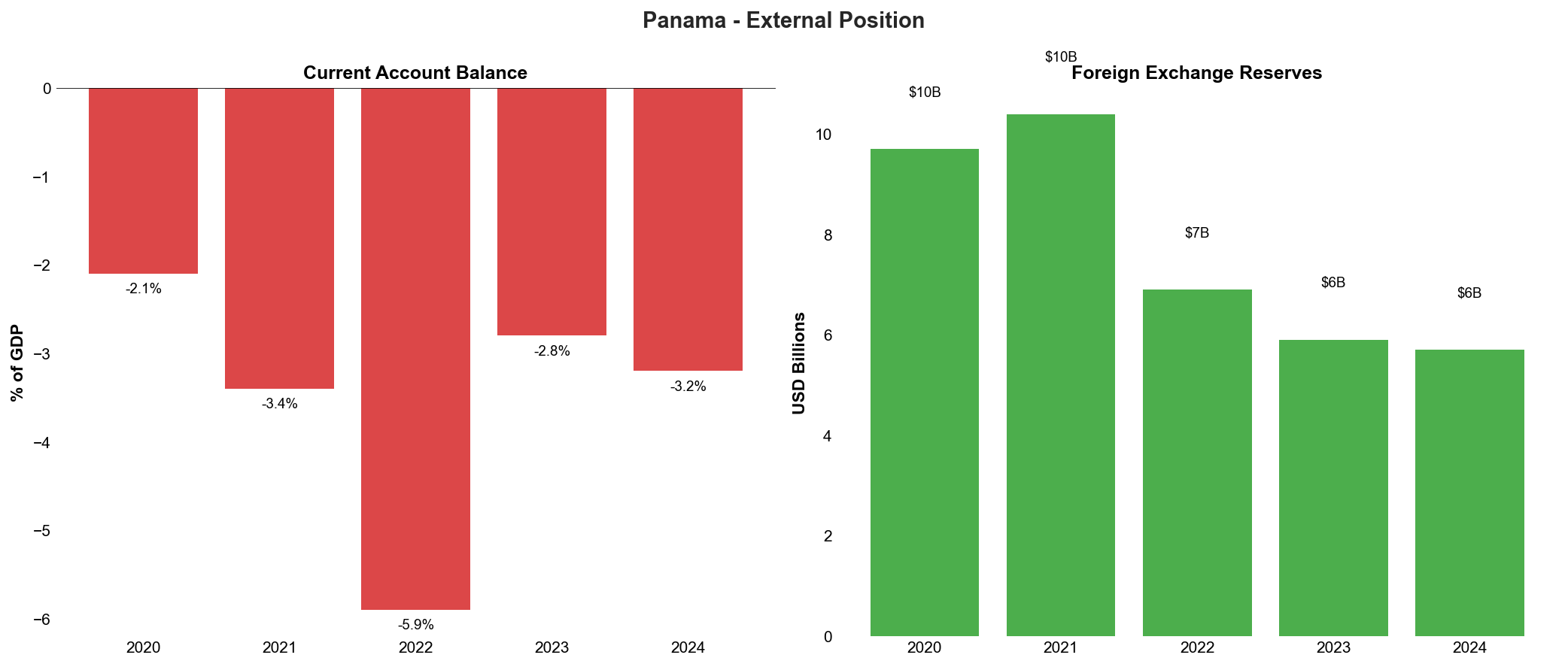

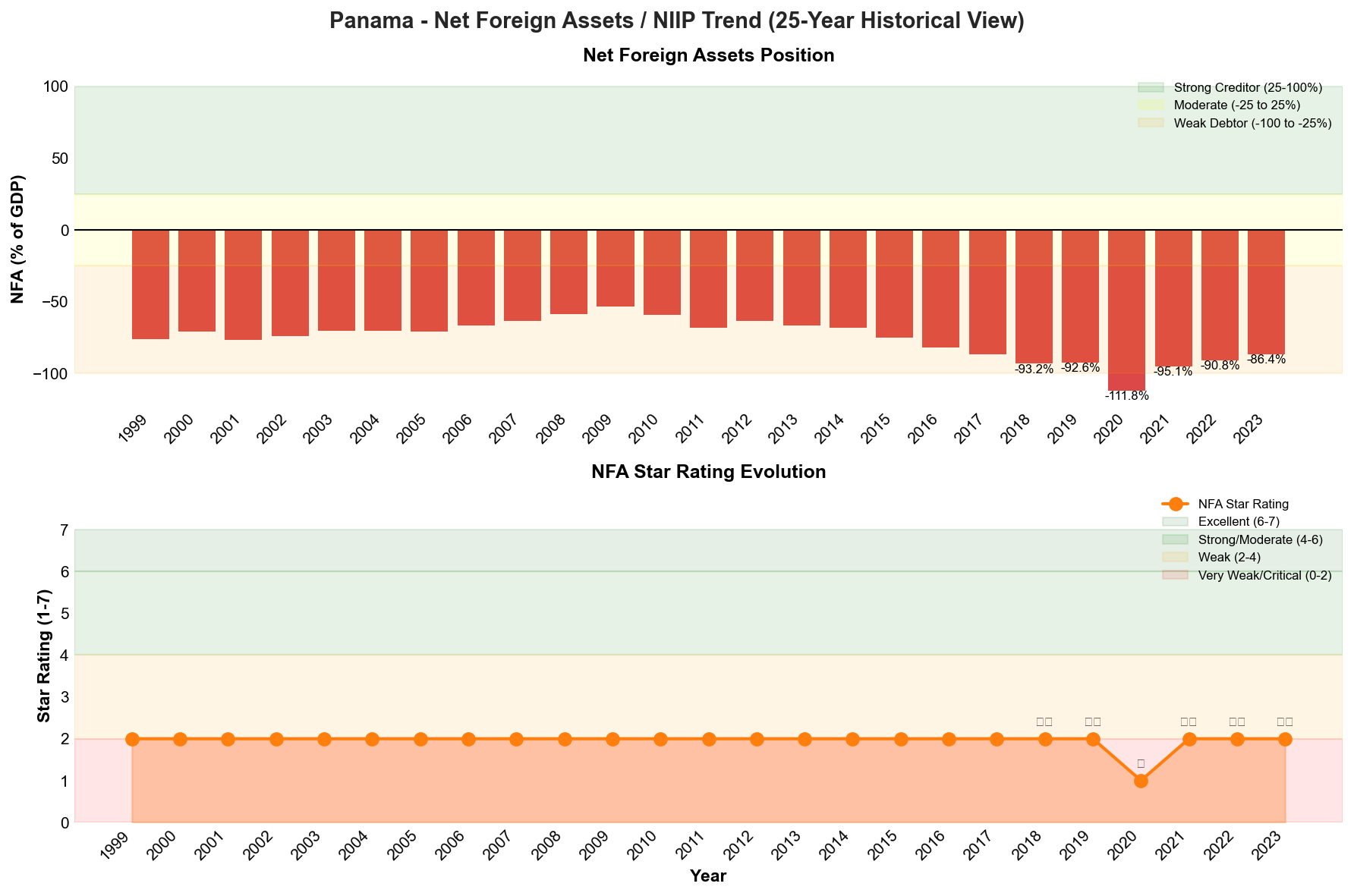

Panama's external position reflects persistent current account deficits and a very weak net foreign asset position, though the dollarised economy provides a degree of stability. The current account deficit widened from -2.1% of GDP in 2020 to -5.9% in 2022, driven by strong import demand during the recovery phase, before moderating to -2.8% in 2023 and an estimated -3.2% in 2024. The closure of the Cobre Panama mine, which had contributed approximately 7% of current external receipts, has adversely affected the external accounts, though this has been partially offset by resilient services exports, particularly from the Panama Canal and the Colón Free Zone. Panama's net foreign asset position stood at -86.4% of GDP in 2023, categorised as "Very Weak" with a two-star rating, reflecting significant external vulnerability. Whilst this represents an improvement from the critical -111.8% recorded in 2020, the position remains substantially negative and exposes the economy to external financing risks. Foreign exchange reserves declined from USD 10.4 billion in 2021 to USD 5.7 billion in 2024, equivalent to approximately three months of imports, a level that provides limited buffer against external shocks. The IMF projects the current account deficit to stabilise at around -3.0% of GDP through 2030, assuming continued strength in services exports and gradual recovery in Canal revenues as water management challenges are addressed.

Inflation has remained well-contained throughout the period, reflecting the disciplining effect of dollarisation and subdued domestic demand pressures. After recording deflation of -1.6% in 2020 during the pandemic contraction, inflation returned to positive territory at 1.6% in 2021 and peaked at 2.9% in 2022, driven primarily by imported food and energy price increases. Inflation moderated to 1.5% in 2023 and is projected at 1.3% for 2024, well below regional averages. The IMF forecasts inflation to stabilise at 2.0% by 2030, consistent with Panama's dollarised monetary framework and assuming no major external price shocks. The absence of an independent monetary policy constrains the authorities' ability to respond to economic shocks through conventional tools, placing greater emphasis on fiscal policy flexibility and structural competitiveness.

The Panama Canal remains a critical economic asset, though its contribution to GDP has fluctuated due to operational challenges. Canal revenues peaked at 7.7% of GDP in 2023 before declining to an estimated 6.0% in 2024, reflecting reduced transit volumes due to drought-induced draft restrictions that limited the passage of larger vessels. The Canal Authority has implemented water management measures and is exploring long-term solutions to enhance water security, though climate variability poses ongoing risks to operations. Tourism arrivals have recovered progressively from the pandemic trough of 0.5 million in 2020 to an estimated 2.5 million in 2024, approaching pre-pandemic levels, supported by Panama's position as a regional hub and improved air connectivity. The banking sector, a cornerstone of Panama's service-based economy, maintains substantial assets equivalent to 69.8% of GDP in 2024, down from 89.8% in 2020, reflecting both GDP recovery and some deleveraging. The sector remains well-capitalised and profitable, providing stability to the financial system, though it faces increased credit risks from the economic slowdown and fiscal pressures.

Net Foreign Assets & External Position

Panama's external position remains structurally weak, characterised by a persistently negative net international investment position (NIIP) that reflects the country's historical reliance on foreign capital to finance its service-based economy and infrastructure development. As of 2023, Panama's net foreign assets stood at -86.4% of GDP, placing the country in the "Very Weak" category with a two-star rating (⭐⭐) on a seven-point scale. Whilst this represents a modest improvement from the critical -111.8% recorded in 2020 during the pandemic-induced economic contraction, the external position remains a significant vulnerability that constrains the sovereign's creditworthiness and limits fiscal flexibility. The negative NIIP reflects substantial foreign ownership of domestic assets, particularly in the banking sector and infrastructure projects, alongside external debt obligations accumulated over decades of development financing.

The trajectory of Panama's net foreign assets over the past five years demonstrates both the severity of the pandemic shock and the subsequent partial recovery. The NIIP deteriorated sharply from -92.6% of GDP in 2019 to -111.8% in 2020 as the denominator effect of the 17.9% GDP contraction magnified the external liability position. The remarkable economic rebound in 2021-2022, with cumulative growth exceeding 26%, facilitated a gradual improvement in the ratio, which continued through 2023 to reach -86.4% of GDP. However, this improvement trajectory has likely stalled in 2024-2025 given the economic headwinds from the Cobre Panama mine closure and reduced Panama Canal revenues due to drought conditions. The persistent classification in the "Very Weak" category across all years except 2020 underscores the structural nature of Panama's external vulnerability, which stems from its position as a regional financial centre and logistics hub requiring substantial foreign investment to maintain its competitive advantages.

Composition and Vulnerabilities

Panama's negative net foreign asset position reflects a complex external balance sheet dominated by the country's role as an international banking centre. The banking sector holds substantial external assets, estimated at approximately 70% of GDP as of 2024, but these are largely offset by external liabilities including foreign deposits, interbank borrowing, and cross-border lending activities. The public sector's external debt represents a significant component of the negative NIIP, with government and government-guaranteed external obligations estimated at approximately 35-40% of GDP. Foreign direct investment liabilities, primarily in infrastructure, logistics, real estate, and financial services, constitute another major element of the external position, reflecting decades of inward investment attracted by Panama's strategic location and business-friendly regulatory environment.

The structural characteristics of Panama's external liabilities provide some mitigating factors to the headline vulnerability. A substantial portion of the negative NIIP comprises equity-like instruments, particularly foreign direct investment in long-term infrastructure projects and real estate, which do not create immediate repayment pressures and tend to be more stable during periods of financial stress. The banking sector's external position, whilst large, is predominantly denominated in US dollars and benefits from the country's dollarised monetary system, which eliminates currency mismatch risk. However, this dollarisation also removes the shock-absorbing capacity of exchange rate adjustment, meaning that external imbalances must be corrected through potentially painful adjustments to domestic demand and prices rather than currency depreciation.

Reserve Adequacy and Liquidity

Panama's foreign exchange reserves have declined significantly from their post-pandemic peak of USD 10.4 billion in 2021 to USD 5.7 billion as of 2024, representing approximately 6-7% of GDP. This reduction reflects both the normalisation of precautionary balances accumulated during the pandemic and the fiscal pressures that have required drawing down liquid assets. The current reserve level provides approximately 2.5-3.0 months of import cover, which is below the conventional adequacy threshold of three months and represents a vulnerability for a dollarised economy without access to a lender of last resort or the ability to print currency in times of stress. The reserve position is further constrained by the need to maintain adequate liquidity in the banking system, which operates under a dollarised framework requiring sufficient US dollar liquidity to meet potential deposit withdrawals and maintain confidence.

The adequacy of Panama's reserves must be assessed in the context of the country's unique monetary arrangements and external financing structure. As a fully dollarised economy, Panama cannot conduct conventional monetary policy or provide unlimited liquidity support to the banking system through central bank operations. This places a premium on maintaining adequate international reserves to serve as a buffer against external shocks and to support confidence in the financial system. The decline in reserves to USD 5.7 billion, whilst still representing a meaningful cushion, has reduced the country's capacity to weather external shocks without requiring adjustment in domestic demand or seeking external financial support. The reserve position is particularly vulnerable to potential contingent liabilities arising from the Cobre Panama dispute, which could result in arbitration awards requiring substantial foreign currency payments.

Current Account Dynamics and Financing

Panama's current account deficit has fluctuated significantly in recent years, widening from -2.1% of GDP in 2020 to -5.9% in 2022 before moderating to -2.8% in 2023 and an estimated -3.2% in 2024. The IMF projects the current account deficit to stabilise at approximately -3.0% of GDP through 2030, suggesting a persistent but manageable external financing requirement. The current account dynamics are heavily influenced by Panama Canal revenues, which contribute approximately 6-7% of GDP in foreign exchange earnings, and by the import intensity of the economy, which relies on foreign goods for consumption and investment. The closure of the Cobre Panama mine has removed a significant source of export earnings that previously contributed approximately 7% of current external receipts, creating a structural deterioration in the trade balance that must be offset by increased service exports or reduced imports.

The financing of Panama's current account deficit relies primarily on foreign direct investment, which has historically exceeded the external financing requirement and contributed to reserve accumulation. However, FDI flows have become more volatile in recent years, reflecting both global financing conditions and country-specific factors including governance concerns and policy uncertainty. The government's external financing needs have increased substantially due to the widening fiscal deficit, with gross external financing requirements (including debt amortisation) estimated at 15-20% of GDP annually. This creates vulnerability to shifts in investor sentiment and increases the cost of external borrowing, as evidenced by the widening of sovereign spreads following the rating downgrades. The concentration of external financing in international capital markets rather than concessional sources further exposes Panama to refinancing risk and interest rate volatility.

Outlook and Risk Assessment

The outlook for Panama's external position remains challenging, with limited prospects for significant improvement in the net foreign asset position over the medium term. The structural current account deficit, combined with continued fiscal financing needs and the loss of Cobre Panama export revenues, suggests that external liabilities will continue to accumulate relative to GDP absent a significant adjustment in domestic demand or a surge in foreign direct investment. The IMF's projection of a -3.0% of GDP current account deficit through 2030, whilst stable, implies continued external financing requirements that will gradually worsen the NIIP if not fully offset by equity-like inflows. The government's fiscal consolidation plans, if successfully implemented, could reduce public sector external borrowing and contribute to a more sustainable external trajectory, but execution risks remain substantial given the political challenges and social pressures.

Key risks to the external position include potential adverse arbitration awards related to the Cobre Panama dispute, which could create large one-off foreign currency outflows; continued drought conditions affecting Panama Canal operations and revenues; deterioration in global trade volumes impacting logistics sector earnings; and tightening of global financial conditions that could reduce capital inflows and increase borrowing costs. The dollarised monetary system, whilst providing inflation stability, constrains the adjustment mechanisms available to address external imbalances and places the full burden of adjustment on fiscal policy and structural competitiveness. Conversely, potential upside factors include resolution of the mining dispute through negotiated settlement rather than arbitration, recovery of Panama Canal operations with improved rainfall, and successful implementation of structural reforms that enhance competitiveness and attract sustained foreign direct investment. The external position will remain a key constraint on Panama's sovereign credit profile, requiring careful management of fiscal policy and continued efforts to maintain investor confidence in the face of structural vulnerabilities.

Credit Strengths & Vulnerabilities

Strengths

Panama's sovereign credit profile is underpinned by several structural advantages that distinguish it from regional peers. The country's strategic geographic position at the crossroads of global maritime trade provides a unique and enduring competitive advantage. The Panama Canal, which remains under Panamanian control, contributes approximately 6% to GDP and generates substantial foreign exchange earnings, though this figure has declined from the 7.7% peak recorded in 2023 due to drought-related operational constraints. The Canal's strategic importance extends beyond direct revenue generation, as it anchors a broader logistics and maritime services ecosystem that has positioned Panama as a regional hub for trade, finance, and business services.

The country's dollarised economy represents a fundamental strength, providing monetary stability and eliminating exchange rate risk. This monetary framework has contributed to maintaining low and stable inflation, with the rate projected at 1.3% for 2024, well below regional averages. Dollarisation also facilitates trade and investment flows, reduces transaction costs, and provides a credible nominal anchor that has historically supported macroeconomic stability. The absence of an independent monetary policy, whilst constraining countercyclical policy options, has prevented the monetary financing of fiscal deficits and the currency crises that have periodically afflicted other emerging market economies.

Panama's banking sector remains robust and well-capitalised, serving as a pillar of financial stability despite the challenging operating environment. The sector's assets, whilst declining from 89.8% of GDP in 2020 to 69.8% in 2024, continue to represent a substantial financial base that supports economic activity. The banking system benefits from prudent regulation, strong capitalisation ratios, and diversified funding sources. Panama's status as an international financial centre has attracted significant foreign banking presence, enhancing the sophistication and resilience of the financial system whilst providing access to international capital markets.

The economy's diversification across service sectors provides resilience against sector-specific shocks. Beyond the Canal, Panama has developed significant capabilities in logistics, financial services, tourism, and business process outsourcing. The tourism sector has demonstrated strong recovery momentum, with arrivals rebounding from pandemic lows of 0.5 million in 2020 to a projected 2.5 million in 2024, approaching pre-pandemic levels. This diversified economic base has historically supported employment generation and provided multiple engines of growth, reducing dependence on any single sector or commodity.

Vulnerabilities

Panama's fiscal position has deteriorated markedly and represents the most significant vulnerability to the sovereign credit profile. The fiscal deficit has widened to an estimated 7.4% of GDP in 2024, substantially exceeding the fiscal rule limit and reversing the consolidation progress achieved in prior years when the deficit had narrowed to 3.0% of GDP in 2023. This deterioration reflects both revenue shortfalls from the closure of the Cobre Panama copper mine and expenditure rigidities that have constrained the government's ability to adjust spending in response to revenue shocks. The breach of the fiscal rule undermines the credibility of the fiscal framework and raises questions about the authorities' commitment to fiscal sustainability.

The debt trajectory has reversed course, with the debt-to-GDP ratio climbing to 61.6% in 2024 from a post-pandemic low of 54.2% in 2023. This increase is particularly concerning as it exceeds the median of 56% for similarly rated sovereigns, as noted by Moody's. More troubling is the rising debt service burden, with the interest-to-income ratio reaching 19%, substantially above the 10% median for comparable credits. This elevated debt service absorbs an increasing share of government revenues, crowding out productive expenditures and reducing fiscal flexibility to respond to future shocks. The combination of rising debt levels and higher interest costs creates a challenging dynamic that could become self-reinforcing if market confidence deteriorates further.

The closure of the Cobre Panama copper mine in late 2023 has created a significant economic void that will take years to fill. The mine represented approximately 5% of GDP and 7% of current external receipts, and its closure has immediate impacts on growth, fiscal revenues, and the external accounts. Beyond these direct effects, the closure has created substantial contingent liabilities through ongoing litigation with First Quantum Minerals, which could result in significant arbitration awards against the government. The circumstances surrounding the mine's closure, following a Supreme Court ruling that invalidated the contract, have also raised concerns about legal certainty and the predictability of the regulatory environment for foreign investors.

Governance challenges and institutional weaknesses have been highlighted by all three major rating agencies as material credit concerns. Panama's fragmented political landscape complicates the implementation of necessary fiscal and structural reforms, as the new administration under President José Raúl Mulino must navigate a congress where no party holds a clear majority. This political fragmentation increases the risk of policy gridlock and may delay or dilute reform initiatives. Historical patterns of corruption and weak institutional capacity further constrain policy effectiveness and undermine investor confidence. The country's performance on governance indicators lags behind higher-rated peers, reflecting weaknesses in rule of law, regulatory quality, and control of corruption.

Opportunities

The resolution of the Cobre Panama mining dispute presents a potential opportunity to restore investor confidence and generate fiscal revenues, though this remains highly uncertain. If the government can negotiate a settlement that balances fiscal, environmental, and social considerations whilst providing adequate legal certainty for investors, it could pave the way for the mine's eventual reopening or the development of alternative mining projects. Such an outcome would provide a significant boost to GDP growth, fiscal revenues, and external receipts, whilst demonstrating improved governance and regulatory predictability. However, achieving this outcome will require navigating complex legal, political, and social dynamics.

The Panama Canal expansion completed in 2016 continues to offer growth potential as global trade patterns evolve and vessel sizes increase. Whilst drought conditions have constrained operations in recent years, investments in water management infrastructure could enhance the Canal's operational resilience and capacity utilisation. The Canal's strategic importance is likely to increase as nearshoring trends and the reconfiguration of global supply chains create new trade flows. Maximising the Canal's contribution to the economy will require continued investment in supporting infrastructure, including ports, logistics facilities, and transport connections.

Structural reforms to enhance competitiveness and productivity could unlock higher sustainable growth rates. Panama has opportunities to improve its business environment, strengthen education and skills development, enhance infrastructure beyond the Canal zone, and reduce regulatory barriers to entrepreneurship and innovation. The country's strategic location and dollarised economy provide a foundation for attracting foreign direct investment in higher value-added activities, including technology services, advanced manufacturing, and regional headquarters operations. Realising this potential will require sustained commitment to institutional strengthening and human capital development.

The tourism sector offers significant upside potential as Panama leverages its natural assets, cultural heritage, and improved connectivity. The country has invested substantially in tourism infrastructure, including the expansion of Tocumen International Airport, which serves as a regional hub. With tourism arrivals still recovering towards pre-pandemic levels, there is scope for continued growth in visitor numbers and tourism receipts. Diversifying tourism offerings beyond Panama City to include ecotourism, beach destinations, and cultural experiences could broaden the sector's appeal and extend its economic benefits to a wider geographic area.

Threats

The risk of further credit rating downgrades represents an immediate and material threat to Panama's sovereign credit profile. With Fitch having already moved Panama to non-investment grade and both S&P and Moody's maintaining the country at the lowest tier of investment grade with stable and negative outlooks respectively, any additional deterioration in fiscal metrics or failure to implement credible consolidation measures could trigger downgrades by the remaining agencies. Loss of investment grade status from all three major agencies would result in forced selling by institutional investors with investment grade mandates, potentially triggering a sharp increase in borrowing costs and reduced market access. This would create a negative feedback loop, as higher interest costs would further deteriorate fiscal metrics and debt sustainability.

Climate-related risks pose increasing threats to Panama's economic model, particularly through impacts on the Panama Canal's operations. The drought conditions experienced in recent years have constrained the Canal's capacity and reduced transit volumes, directly impacting revenues. Climate models suggest that such drought events may become more frequent and severe, potentially requiring substantial investments in water management infrastructure to maintain operational capacity. Beyond the Canal, climate change threatens other economic sectors, including agriculture, tourism, and coastal infrastructure. The country's geographic characteristics, including extensive coastlines and mountainous terrain, create vulnerabilities to extreme weather events, sea-level rise, and changing precipitation patterns.

External shocks represent a persistent vulnerability given Panama's high degree of openness and dependence on global trade flows. A significant slowdown in global economic growth or disruption to international trade would directly impact Canal revenues, logistics activities, and the broader service economy. The country's dollarised monetary system, whilst providing stability benefits, eliminates the exchange rate as a shock absorber and places the entire burden of adjustment on fiscal policy and real economic variables. This amplifies the impact of external shocks and constrains policy responses. Panama's limited foreign exchange reserves, which have declined from USD 10.4 billion in 2021 to USD 5.7 billion in 2024, provide only modest buffers against external pressures.

Social and political tensions could intensify if fiscal consolidation measures are perceived as inequitable or if economic growth remains subdued. The protests that led to the closure of the Cobre Panama mine demonstrated the potential for social mobilisation around environmental and governance issues. Implementing the fiscal adjustments necessary to restore sustainability will likely require measures that affect public sector employment, subsidies, and social programmes, potentially triggering political opposition and social unrest. The government's ability to build consensus around difficult reforms is constrained by the fragmented political landscape and weak institutional capacity. Failure to address these challenges through inclusive dialogue and equitable policy design could result in policy paralysis or the adoption of populist measures that further undermine fiscal sustainability.

Economic Analysis

Growth Dynamics and Structural Challenges

Panama's economic trajectory over the past five years reflects a narrative of dramatic volatility followed by mounting structural headwinds. The economy's severe contraction of 17.9% in 2020 represented one of the sharpest downturns in Latin America during the COVID-19 pandemic, driven by the country's heavy reliance on services sectors particularly vulnerable to mobility restrictions, including tourism, logistics, and international financial services. The subsequent recovery proved equally dramatic, with Panama recording amongst the region's strongest rebounds at 15.8% in 2021 and maintaining robust momentum through 2022 and 2023 with growth rates of 10.8% and 7.3% respectively. This V-shaped recovery was underpinned by the resumption of Panama Canal operations at full capacity, the revival of international tourism, and strong domestic demand supported by fiscal stimulus measures.

However, the sharp deceleration to 2.5% projected growth in 2024 signals a fundamental shift in Panama's economic dynamics, driven by two significant exogenous shocks. The closure of the Cobre Panama copper mine in late 2023, following a Supreme Court ruling that invalidated the mining concession contract with First Quantum Minerals, has removed a substantial economic contributor representing approximately 5% of GDP and 7% of current external receipts. The mine's closure has created immediate negative impacts on export revenues, fiscal receipts, and employment, whilst simultaneously generating contingent liabilities through ongoing international arbitration proceedings. The second major constraint emerged from severe drought conditions affecting Panama Canal operations, reducing the waterway's transit capacity and consequently diminishing canal revenues, which had contributed 7.7% to GDP in 2023 but declined to an estimated 6.0% in 2024.

The confluence of these factors has exposed the vulnerability of Panama's growth model to concentrated sectoral dependencies, despite the economy's apparent diversification across services. The medium-term growth outlook remains constrained by the permanent loss of mining sector output, uncertainty regarding future large-scale investment projects given the mining dispute's implications for investor confidence, and the structural challenges facing the Panama Canal from climate-related water availability issues. The new administration's ability to catalyse alternative sources of growth through infrastructure investment, regulatory reforms to enhance the business environment, and measures to restore investor confidence will prove critical to sustaining growth rates consistent with Panama's historical performance and development trajectory.

Inflation Dynamics and Price Stability

Panama's inflation performance has remained remarkably benign throughout the period under review, with the country experiencing deflation of 1.6% in 2020 during the pandemic-induced demand collapse, followed by modest inflation rates of 1.6% in 2021, 2.9% in 2022, 1.5% in 2023, and a projected 1.3% in 2024. This sustained price stability stands in stark contrast to the elevated inflation experienced across much of Latin America and globally during 2021-2023, reflecting the unique characteristics of Panama's dollarised monetary system. The absence of an independent monetary policy and the use of the US dollar as legal tender effectively imports US monetary conditions whilst eliminating exchange rate pass-through effects on domestic prices.

The relatively subdued inflation in 2022, when many regional peers experienced inflation rates exceeding 8-10%, demonstrates the anchoring effect of dollarisation on inflation expectations and the discipline it imposes on fiscal and wage-setting behaviour. Panama's inflation dynamics are primarily driven by imported inflation from trading partners, domestic food price movements influenced by weather conditions and agricultural productivity, and services sector pricing power, which remains constrained by competitive market conditions. The projected decline in inflation to 1.3% in 2024 reflects weakening domestic demand conditions associated with slower economic growth, moderating global commodity prices, and the disinflationary impact of reduced economic activity following the mine closure.

Monetary Policy Framework and Financial Conditions

Panama's dollarised economy operates without a central bank capable of conducting conventional monetary policy, fundamentally distinguishing its macroeconomic policy framework from regional peers. The absence of an independent currency eliminates exchange rate risk for dollar-denominated transactions, provides a credible nominal anchor for inflation expectations, and facilitates financial integration with international capital markets. However, dollarisation also constrains the authorities' ability to respond to asymmetric shocks through monetary policy adjustments, places the entire burden of macroeconomic stabilisation on fiscal policy, and requires the maintenance of substantial banking sector liquidity buffers to ensure financial stability in the absence of a lender of last resort function.

The Superintendency of Banks of Panama serves as the primary financial sector regulator, maintaining prudential oversight of the country's internationally-oriented banking centre. Panama's banking sector has demonstrated considerable resilience throughout recent economic cycles, with the sector maintaining strong capitalisation ratios, adequate liquidity positions, and manageable non-performing loan levels despite the severe economic contraction in 2020 and subsequent volatility. Banking sector assets, whilst declining from 89.8% of GDP in 2020 to 69.8% in 2024, remain substantial and reflect both the domestic banking system and Panama's role as a regional financial centre serving Central American and Caribbean markets.

The dollarised framework has proven particularly valuable in maintaining financial stability during periods of regional currency volatility, as Panama avoids the balance sheet mismatches and sudden stop risks that have affected neighbouring economies with domestic currencies. However, the system's rigidity places premium importance on fiscal discipline and structural competitiveness, as the authorities cannot rely on exchange rate depreciation to restore external balance or monetary expansion to stimulate domestic demand. The current fiscal deterioration therefore poses heightened risks within this monetary framework, as the absence of monetary financing options limits the authorities' policy flexibility and increases reliance on market access for debt financing. Foreign exchange reserves, which declined from USD 10.4 billion in 2021 to USD 5.7 billion in 2024, provide only limited buffer capacity given the absence of exchange rate intervention requirements, serving primarily to support the government's liquidity management and provide confidence to international investors regarding the sustainability of dollarisation.

Political & Institutional Assessment

Panama's political and institutional framework presents a mixed profile characterised by democratic continuity alongside persistent governance challenges that have increasingly weighed on the sovereign credit assessment. The country operates under a presidential representative democratic republic with regular electoral transitions, though institutional effectiveness and policy implementation capacity remain constrained by structural weaknesses in governance, corruption vulnerabilities, and political fragmentation.

Political Landscape and Recent Transitions

President José Raúl Mulino assumed office in July 2024 following elections held in May 2024, marking another peaceful democratic transition in Panama's political history. Mulino, representing the Realizing Goals party, secured victory with approximately 34% of the vote in a fragmented electoral field. His administration inherited a challenging economic and fiscal environment, compounded by the immediate aftermath of the Cobre Panama mine closure and deteriorating public finances that had already triggered credit rating downgrades prior to his inauguration.

The political landscape remains highly fragmented, with multiple parties represented in the National Assembly and no single party commanding a clear majority. This fragmentation complicates the passage of significant legislative reforms and constrains the executive's ability to implement comprehensive fiscal consolidation measures or structural reforms. The Mulino administration's capacity to navigate this fragmented legislature whilst advancing necessary but potentially unpopular fiscal adjustments represents a critical determinant of Panama's medium-term credit trajectory.

Governance Challenges and Institutional Capacity

Governance weaknesses constitute a persistent constraint on Panama's sovereign credit profile, with rating agencies consistently highlighting institutional deficiencies as a key rating factor. The country's governance indicators have shown limited improvement over recent years, with corruption perceptions and rule of law metrics remaining below the median for investment-grade sovereigns. These institutional shortcomings manifest in several dimensions, including inconsistent policy implementation, weak public financial management, and limited transparency in government operations.

The closure of the Cobre Panama copper mine in late 2023 exemplifies the intersection of governance challenges and economic policy uncertainty. Following sustained public protests against the mining concession, Panama's Supreme Court ruled the contract with First Quantum Minerals unconstitutional, leading to the mine's immediate closure. Whilst the decision reflected judicial independence and responsiveness to public sentiment regarding environmental and sovereignty concerns, it also highlighted the unpredictability of the regulatory environment and created significant contingent liability risks from potential international arbitration claims. The mine had represented approximately 5% of GDP and 7% of current external receipts, making its abrupt closure a substantial economic shock that the government had limited capacity to mitigate.

Fiscal Governance and Rule Adherence

Panama's fiscal framework includes a fiscal responsibility law designed to constrain deficit spending and ensure debt sustainability. However, adherence to this framework has proven inconsistent, particularly during periods of economic stress. The fiscal deficit deteriorated sharply to an estimated 7.4% of GDP in 2024, significantly exceeding the fiscal rule limit of 2% of GDP. This breach reflects both the economic impact of the Cobre Panama closure and underlying structural fiscal weaknesses, including limited revenue mobilisation capacity and rigid expenditure commitments.

The government's ability to implement credible fiscal consolidation measures remains uncertain given the political constraints and social pressures. Previous attempts at fiscal reform, including efforts to broaden the tax base and reduce exemptions, have faced significant political resistance. The Mulino administration has signalled commitment to fiscal discipline and has engaged with international financial institutions regarding potential reform programmes, though concrete implementation remains at an early stage. The credibility of fiscal consolidation efforts will be critical to maintaining investment-grade status with S&P and Moody's, both of which have emphasised fiscal sustainability as a key rating determinant.

Institutional Strengths and Mitigating Factors

Despite governance challenges, Panama maintains certain institutional strengths that provide partial offsets to credit concerns. The Panama Canal Authority operates as a relatively well-managed autonomous entity with strong technical capacity and transparent financial reporting. The Canal's operations contribute approximately 6% to GDP and provide a stable source of government revenue through dividend transfers, though this contribution has been affected by drought conditions impacting transit capacity.

The banking sector regulatory framework demonstrates relative strength, with the Superintendency of Banks maintaining adequate supervisory standards and capital requirements. Panama's banking sector remains well-capitalised with assets representing 69.8% of GDP as of 2024, and the regulatory authority has demonstrated capacity to manage financial sector risks. The dollarised monetary system, whilst constraining monetary policy flexibility, provides institutional discipline and has contributed to maintaining low inflation and financial stability.

The judicial system, despite concerns about efficiency and occasional political interference, has demonstrated independence in high-profile cases, as evidenced by the Supreme Court's ruling on the Cobre Panama mining contract. This independence, whilst creating policy uncertainty in specific instances, represents an important institutional check on executive authority and provides some assurance regarding rule of law, albeit with inconsistent application across different policy domains.

Banking Sector & Financial Stability

Panama's banking sector represents a cornerstone of stability within an otherwise challenging sovereign credit profile, demonstrating resilience through successive economic shocks whilst maintaining robust capitalisation and liquidity metrics. The sector's assets, whilst declining from 89.8% of GDP in 2020 to 69.8% in 2024, remain substantial and reflect a well-developed financial system that serves both domestic and international clients. This contraction in the asset-to-GDP ratio primarily reflects the denominator effect of strong nominal GDP growth during the post-pandemic recovery period rather than an absolute reduction in banking sector health.

The Panamanian banking system operates under a dual structure comprising both domestic-oriented banks and international banking units, a configuration that has historically provided diversification benefits and enhanced the country's position as a regional financial hub. The sector's capitalisation levels remain well above regulatory minimums, with banks maintaining strong capital adequacy ratios that provide meaningful buffers against potential economic deterioration. This prudent capitalisation has been particularly important given the recent economic headwinds from the Cobre Panama mine closure and the fiscal challenges facing the sovereign.

Liquidity conditions within the banking sector have remained adequate despite the broader economic pressures, with banks maintaining sufficient liquid assets to meet potential deposit withdrawals and credit demands. The dollarised nature of Panama's economy eliminates currency mismatch risks that plague many emerging market banking systems, providing an inherent stability advantage. Banks hold deposits predominantly in US dollars, matching the currency composition of their loan portfolios, which removes a significant source of systemic vulnerability.

Asset quality metrics have shown resilience through the recent economic cycle, though the sector faces emerging challenges from the slowdown in economic growth and the fiscal pressures affecting both public and private sector borrowers. Non-performing loan ratios have remained manageable, supported by the strong post-pandemic recovery through 2023, but warrant close monitoring given the deteriorating macroeconomic environment in 2024 and beyond. The banking sector's exposure to the government, both through direct sovereign debt holdings and through lending to state-owned enterprises, creates a meaningful sovereign-bank nexus that could transmit fiscal stress into financial sector vulnerabilities.

The regulatory and supervisory framework governing Panama's banking sector has strengthened considerably over the past decade, with the Superintendency of Banks maintaining active oversight and implementing international best practices. The adoption of Basel III capital standards and enhanced risk management requirements has improved the sector's resilience to shocks. However, the effectiveness of supervision remains dependent on institutional capacity and political independence, factors that have come under scrutiny given the broader governance challenges highlighted by rating agencies.

The banking sector's role in financing economic activity remains critical, particularly given Panama's limited access to capital markets at the sovereign level. Banks have continued to extend credit to the private sector, supporting the services-based economy that drives growth, though credit growth has moderated in line with the economic slowdown. The sector's ability to maintain credit provision whilst preserving asset quality and capitalisation will be essential for supporting economic recovery and mitigating the impact of reduced mining sector activity.

Looking forward, the banking sector faces several key challenges that could test its resilience. The fiscal consolidation required to restore debt sustainability may create headwinds for economic growth, potentially affecting loan performance and credit demand. The sovereign's deteriorating credit profile and elevated financing needs could crowd out private sector credit or increase banks' exposure to sovereign risk. Additionally, any further economic shocks, whether from external factors or domestic policy uncertainty, could pressure asset quality and profitability. Nevertheless, the sector's strong starting position in terms of capitalisation and liquidity, combined with the structural advantages of dollarisation and its role as a regional financial centre, provide meaningful mitigants to these risks and support the assessment that the banking sector remains a relative strength within Panama's sovereign credit profile.

Outlook & Scenarios

Short-Term Outlook (12 months)

Panama's near-term credit trajectory remains precarious, with the country facing heightened risk of additional downgrades from the two agencies that continue to maintain investment-grade ratings. Over the next twelve months, the primary determinant of rating stability will be the government's ability to demonstrate credible progress towards fiscal consolidation whilst managing the economic fallout from the Cobre Panama mine closure. The Mulino administration's capacity to navigate these challenges is constrained by a fragmented political landscape, which complicates the passage of necessary fiscal reforms through the National Assembly.

The fiscal position represents the most immediate concern for rating agencies. With the deficit having deteriorated to an estimated 7.4% of GDP in 2024—significantly exceeding the fiscal rule limit—the government faces urgent pressure to implement consolidation measures. However, the political feasibility of expenditure cuts or revenue enhancements remains uncertain, particularly given public resistance to austerity measures and the administration's limited legislative majority. The absence of meaningful fiscal adjustment over the coming year would likely trigger downgrades from both S&P and Moody's, pushing Panama fully into sub-investment grade territory across all three major agencies.

Economic growth prospects for the near term remain subdued, with the permanent loss of the Cobre Panama mine's contribution—previously accounting for approximately 5% of GDP—creating a structural headwind that cannot be quickly offset. Whilst the Panama Canal continues to generate substantial revenues contributing roughly 6% to GDP, operational constraints related to water availability during drought periods introduce volatility into this critical revenue stream. The tourism sector's continued recovery, with arrivals projected to reach 2.5 million in 2024, provides some support to growth, though this remains below pre-pandemic levels and insufficient to compensate for mining sector losses.

The resolution of litigation stemming from the Cobre Panama mine closure represents a significant contingent liability that could materialise within the twelve-month horizon. First Quantum Minerals has initiated arbitration proceedings seeking substantial compensation, with potential claims estimated in the billions of dollars. An adverse ruling or settlement would place additional strain on public finances and could necessitate further debt issuance, exacerbating the already elevated debt-to-GDP ratio of 61.6%. The uncertainty surrounding this litigation weighs on investor confidence and complicates the government's fiscal planning.

Medium-Term Outlook (1-3 years)

Over the medium term, Panama's credit profile will be shaped by the government's success in implementing structural reforms that address underlying fiscal vulnerabilities whilst fostering economic diversification to reduce dependence on a narrow range of sectors. The trajectory of the debt-to-GDP ratio, which has reversed its declining trend and now exceeds the median for similarly rated sovereigns, will serve as a critical indicator of fiscal sustainability. Stabilising and subsequently reducing this ratio will require sustained primary surpluses, a challenging objective given the political constraints on fiscal adjustment and the structural revenue loss from the mining sector.

The Mulino administration's reform agenda encompasses several priority areas, including strengthening governance frameworks, enhancing tax collection efficiency, and rationalising public expenditure. Progress on these fronts would bolster institutional credibility and potentially unlock additional financing from multilateral institutions. However, the implementation of structural reforms typically requires extended timeframes and faces resistance from vested interests. The government's ability to maintain reform momentum beyond the initial honeymoon period will be tested as the political costs of adjustment become more apparent.

Economic diversification represents both a necessity and an opportunity for Panama over the medium term. The country's strategic geographic position and well-developed logistics infrastructure provide a foundation for expanding activities in maritime services, international financial services, and regional distribution. The banking sector, which maintains robust capitalisation despite assets declining to 69.8% of GDP, continues to serve as a pillar of economic stability. Attracting foreign direct investment to develop new growth engines will require not only macroeconomic stability but also improvements in the regulatory environment and resolution of governance concerns that have contributed to rating downgrades.

The external position warrants careful monitoring over the medium term. Whilst Panama's dollarised economy eliminates exchange rate risk and provides monetary stability—with inflation remaining subdued at 1.3% projected for 2024—it also constrains policy flexibility in responding to external shocks. The current account deficit, projected at 3.2% of GDP for 2024, remains manageable but is sensitive to fluctuations in Panama Canal revenues and import demand. Foreign exchange reserves, which have declined to $5.7 billion, provide limited buffer relative to external financing needs, underscoring the importance of maintaining market access on favourable terms.

Climate-related risks pose an emerging challenge to Panama's medium-term outlook, particularly regarding water availability for Panama Canal operations. Recurring drought conditions have necessitated restrictions on vessel transits, reducing toll revenues and highlighting the vulnerability of this critical economic asset to environmental factors. Investment in water management infrastructure and adaptation measures will be essential to preserve the Canal's operational capacity and revenue-generating potential, though such investments require fiscal resources that are currently constrained.

Rating Scenarios

The rating trajectory for Panama over the coming years will be determined primarily by fiscal performance, with secondary factors including economic growth resilience, resolution of the Cobre Panama litigation, and progress on governance reforms. Three distinct scenarios capture the range of plausible outcomes, each with different implications for sovereign creditworthiness.

In an upside scenario, Panama successfully implements fiscal consolidation measures that reduce the deficit to below 4% of GDP within two years whilst stabilising the debt-to-GDP ratio. This outcome would require the government to secure legislative approval for revenue-enhancing measures, potentially including tax reforms that broaden the base and improve collection efficiency, alongside expenditure restraint that protects growth-critical investments whilst eliminating inefficiencies. Successful negotiation of the Cobre Panama litigation on terms that limit fiscal impact, combined with stronger-than-expected economic growth driven by Canal optimisation and tourism recovery, would support this scenario. Under these conditions, S&P could revise its outlook to positive, Moody's could stabilise its outlook at neutral, and Fitch could consider an upgrade back to investment grade, though the latter would require sustained demonstration of improved fiscal and governance metrics. This scenario would likely see the debt-to-GDP ratio declining towards 55% by 2027-2028, with interest payments as a percentage of revenue stabilising below 18%.

The baseline scenario, which represents the most probable outcome given current political and economic constraints, envisions gradual fiscal improvement that proves insufficient to fully satisfy rating agency concerns. In this scenario, the deficit narrows modestly to approximately 5-6% of GDP over the medium term, whilst the debt-to-GDP ratio stabilises around 60-62% but fails to decline meaningfully. Economic growth remains subdued in the 2.5-3.5% range, reflecting the permanent loss of mining sector contribution partially offset by modest gains in other sectors. The Cobre Panama litigation is resolved through a negotiated settlement that, whilst material, does not trigger a fiscal crisis. Under this scenario, S&P would likely maintain its BBB- rating with stable outlook, Moody's would face pressure to downgrade to Ba1 (non-investment grade) given its negative outlook, and Fitch would maintain its BB+ rating. This outcome would leave Panama with a split rating profile, complicating market access and potentially increasing borrowing costs, though the country would retain investment-grade status from at least one major agency.

In a downside scenario, fiscal consolidation efforts falter due to political gridlock or economic underperformance, with the deficit remaining above 6% of GDP and the debt-to-GDP ratio rising towards 65-70%. This scenario could be triggered by an adverse outcome in the Cobre Panama arbitration that imposes multi-billion dollar liabilities on the government, combined with weaker economic growth below 2% due to external shocks or further Canal operational constraints. Political instability or governance setbacks that undermine investor confidence would exacerbate these pressures. Under these conditions, both S&P and Moody's would downgrade Panama to sub-investment grade, likely to Ba1 or Ba2, whilst Fitch could implement a further downgrade to BB. The loss of investment-grade status across all three agencies would trigger forced selling by institutional investors with investment-grade mandates, significantly increasing borrowing costs and potentially creating market access challenges. This scenario would necessitate greater reliance on multilateral financing and could force more abrupt fiscal adjustment under crisis conditions, with negative implications for economic growth and social stability.

Conclusion

Panama's sovereign credit profile stands at a critical juncture as of January 2026, balancing significant structural strengths against mounting fiscal and governance challenges that have placed its investment-grade status in jeopardy. The country's credit trajectory has deteriorated markedly since 2023, culminating in Fitch's downgrade to non-investment grade (BB+) in March 2024, whilst S&P and Moody's maintain Panama at the lowest tier of investment grade (BBB- and Baa3 respectively) with stable and negative outlooks. This divergence amongst the rating agencies underscores the precarious nature of Panama's creditworthiness and the narrow margin for policy error.

The fundamental credit challenges facing Panama are substantial and multifaceted. The closure of the Cobre Panama copper mine in late 2023, following a Supreme Court ruling that invalidated the mining contract, has removed approximately 5% of GDP and 7% of current external receipts from the economy, creating both immediate economic headwinds and potential contingent liabilities from ongoing litigation. This shock has coincided with a sharp fiscal deterioration, with the deficit widening to an estimated 7.4% of GDP in 2024, significantly exceeding the fiscal rule limit and reversing the consolidation progress achieved in prior years. Consequently, the debt-to-GDP ratio has climbed to 61.6% in 2024, surpassing the median for similarly rated sovereigns, whilst the interest-to-income ratio has increased to 19%, well above peer medians and constraining fiscal flexibility.

These pressures are compounded by governance challenges and a fragmented political landscape that complicate the implementation of necessary structural reforms. The drought conditions affecting Panama Canal operations have further constrained a key revenue source, with Canal contributions to GDP declining from 7.7% in 2023 to an estimated 6.0% in 2024. The marked deceleration in economic growth from 7.3% in 2023 to a projected 2.5% in 2024 reflects these combined headwinds and raises concerns about the sustainability of debt dynamics absent fiscal consolidation.

Nevertheless, Panama retains important credit strengths that provide a foundation for potential stabilisation. The country's strategic geographic position and control of the Panama Canal continue to generate substantial revenues and underpin a diversified, service-based economy centred on logistics, financial services, and tourism. The dollarised monetary framework provides inherent stability, anchoring inflation expectations and eliminating exchange rate risk, with inflation remaining subdued at a projected 1.3% in 2024. Panama's banking sector remains robust and well-capitalised, with assets representing 69.8% of GDP in 2024, providing financial system resilience despite the broader economic challenges. The country's demonstrated capacity for rapid economic recovery, evidenced by the remarkable post-pandemic rebound with growth of 15.8% in 2021 and 10.8% in 2022, illustrates underlying economic dynamism.

The administration of President José Raúl Mulino, which assumed office in July 2024, faces the formidable task of restoring fiscal sustainability whilst managing the economic fallout from the mine closure and implementing structural reforms to strengthen governance and institutional frameworks. The credibility and effectiveness of the government's fiscal consolidation strategy will be paramount in determining whether Panama can stabilise its debt trajectory and preserve investment-grade status with S&P and Moody's. Resolution of the Cobre Panama mining dispute, whether through negotiated settlement or alternative development of the asset, would provide meaningful upside to the fiscal and growth outlook.

The outlook for Panama's sovereign credit remains cautious, with the balance of risks tilted to the downside in the near term. Failure to demonstrate credible fiscal consolidation, further deterioration in debt metrics, or additional governance setbacks could trigger downgrades from the remaining investment-grade agencies, potentially precipitating capital outflows and increasing borrowing costs. Conversely, successful implementation of fiscal reforms, resolution of the mining dispute, and sustained economic growth above 3% would support credit stabilisation and potentially lead to outlook revisions. The coming 12 to 18 months will prove decisive in determining whether Panama can arrest its credit deterioration and rebuild the fiscal buffers necessary to maintain its position amongst investment-grade sovereigns.