Norway

Executive Summary

Norway maintains the highest possible credit rating (AAA/Aaa) from all three major rating agencies with stable outlooks as of January 2026, underpinned by an exceptional fiscal position anchored by the Government Pension Fund Global valued at NOK 19,742 billion (approximately $1.9 trillion). The sovereign benefits from very high GDP per capita approaching $87,000, strong democratic institutions ranked amongst the world's best, and a robust external position with consistent current account surpluses averaging 15-17% of GDP. The Norwegian banking system demonstrates exceptional resilience with capital ratios near 19%, non-performing loans below 1%, and return on equity reaching 17.5%, placing it amongst Europe's strongest financial sectors. This formidable credit profile is further reinforced by highly transparent governance frameworks, a prudent fiscal rule that limits petroleum revenue spending, and massive net external assets that provide unprecedented buffers against economic shocks.

Despite these considerable strengths, Norway confronts structural challenges that temper its otherwise exceptional profile. The petroleum sector accounts for approximately 62% of goods exports and 24% of GDP, creating significant vulnerability to oil price volatility and long-term energy transition risks as global decarbonisation accelerates. Household debt remains elevated at over 200% of disposable income, representing a key financial stability concern despite low unemployment and strong social safety nets. Productivity growth has stagnated at 0.6-0.8% annually—well below historical averages—constraining potential economic growth and competitiveness. An ageing population will intensify fiscal pressures in coming decades, though the massive sovereign wealth fund provides substantial buffer capacity. The country also faces geopolitical exposure stemming from proximity to Russia and the ongoing Ukraine conflict, though this has paradoxically strengthened Norway's strategic importance as Europe's largest energy supplier after Russia.

The economic outlook shows resilience amid global uncertainty, with mainland GDP growth forecast at 1.5% in 2025 and inflation declining towards the 2% target by 2027, allowing Norges Bank to begin policy normalisation with rate cuts from 4.5% to 4.0%. The expansionary fiscal stance, supported by record petroleum revenues and prudent sovereign wealth fund management, positions Norway to weather near-term shocks whilst pursuing gradual economic diversification away from hydrocarbon dependence. Credit rating agencies unanimously affirm that Norway's vulnerabilities are substantially mitigated by unparalleled fiscal flexibility, with the GPFG representing approximately 380% of GDP and providing multi-generational economic security that distinguishes Norway from all other highly-rated sovereigns globally. The combination of strong institutional frameworks, substantial fiscal buffers, and proactive policy responses supports the stable outlook, though successful navigation of the energy transition and sustained productivity improvements remain critical to maintaining Norway's exceptional credit standing over the medium to long term.

Ratings Summary

Norway maintains the highest possible credit rating of AAA/Aaa from all three major rating agencies with stable outlooks as of January 2026, positioning it amongst an exclusive group of only 9-10 countries globally that hold this distinction across all three agencies simultaneously. All three major rating agencies have consistently affirmed Norway's top-tier ratings throughout 2024 and 2025, with no rating changes in the past two years. S&P Global's March 2025 affirmation emphasised Norway's exceptional fiscal position supported by the Government Pension Fund Global, which provides robust fiscal buffers and long-term sustainability, whilst noting that projected GDP per capita of nearly $87,000 in 2025 ranks amongst the highest of all rated sovereigns. Moody's June 2025 assessment highlighted the sovereign wealth fund's value of NOK 19,742 billion at end-2024, representing 380% of GDP and reflecting a 13.1% increase from 2023, whilst assigning Norway its highest possible institutional assessment (aaa) and noting the fund has achieved a 6.3% average annual return since 1998. Fitch's June 2025 affirmation focused on the standout sovereign balance sheet and exceptional institutional strengths, noting that the 2022-2023 energy price surge further strengthened fiscal and external buffers. The rating agencies identify common credit strengths including the world's largest sovereign wealth fund providing unprecedented fiscal flexibility, highly transparent and efficient governance with a prudent fiscal rule, very high and equitably distributed wealth, massive net external asset position, and a robust macroeconomic policy framework, though all three agencies cite consistent challenges related to petroleum sector concentration and elevated household debt levels.

| Rating Agency | Current Rating | Outlook | Last Action Date |

|---|---|---|---|

| S&P Global Ratings | AAA/A-1+ | Stable | March 7, 2025 |

| Moody's Investors Service | Aaa | Stable | June 10, 2025 |

| Fitch Ratings | AAA | Stable | June 13, 2025 |

Economic Indicators

| Indicator | 2022 | 2023 | 2024 | 2025* | 2026* |

|---|---|---|---|---|---|

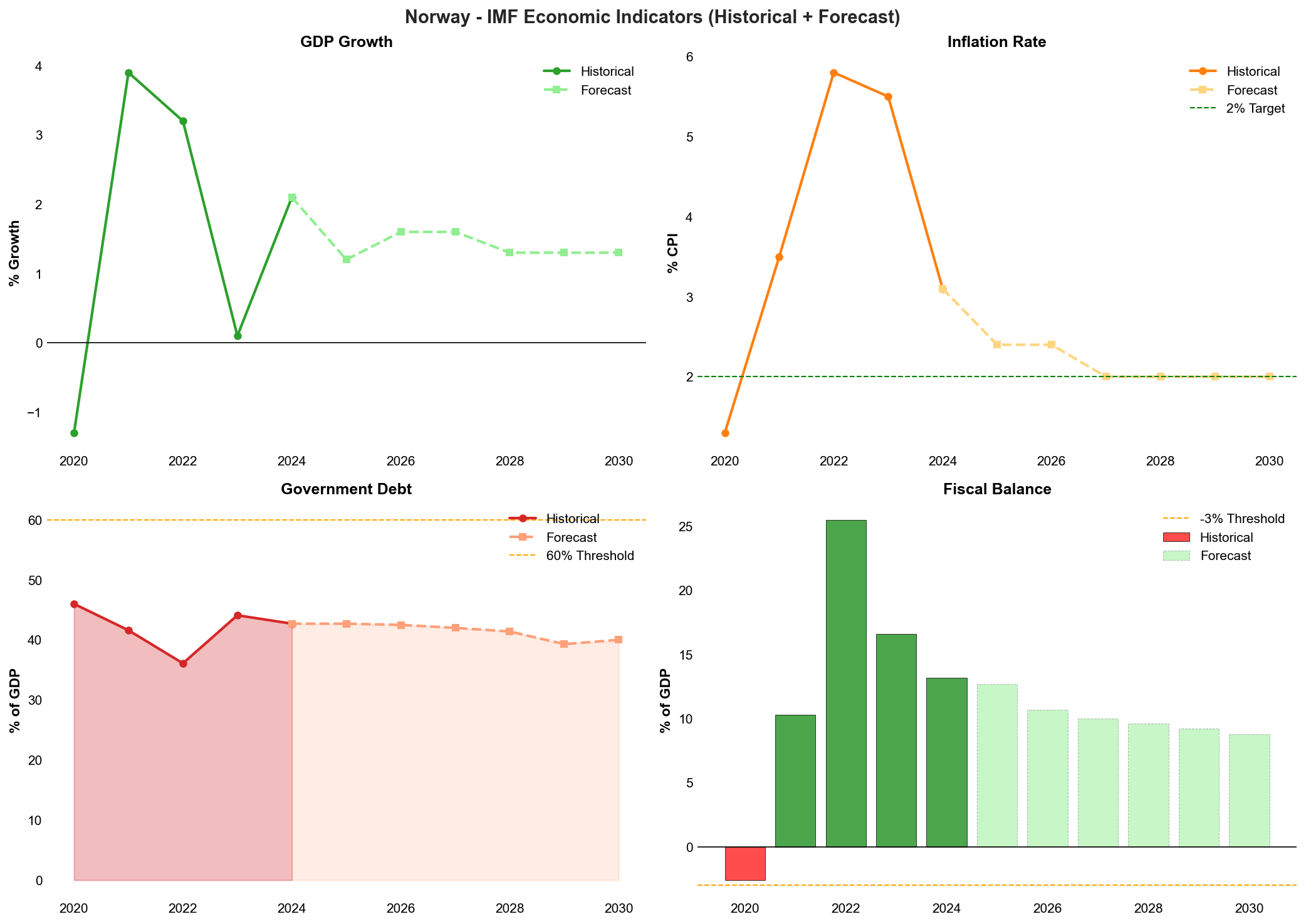

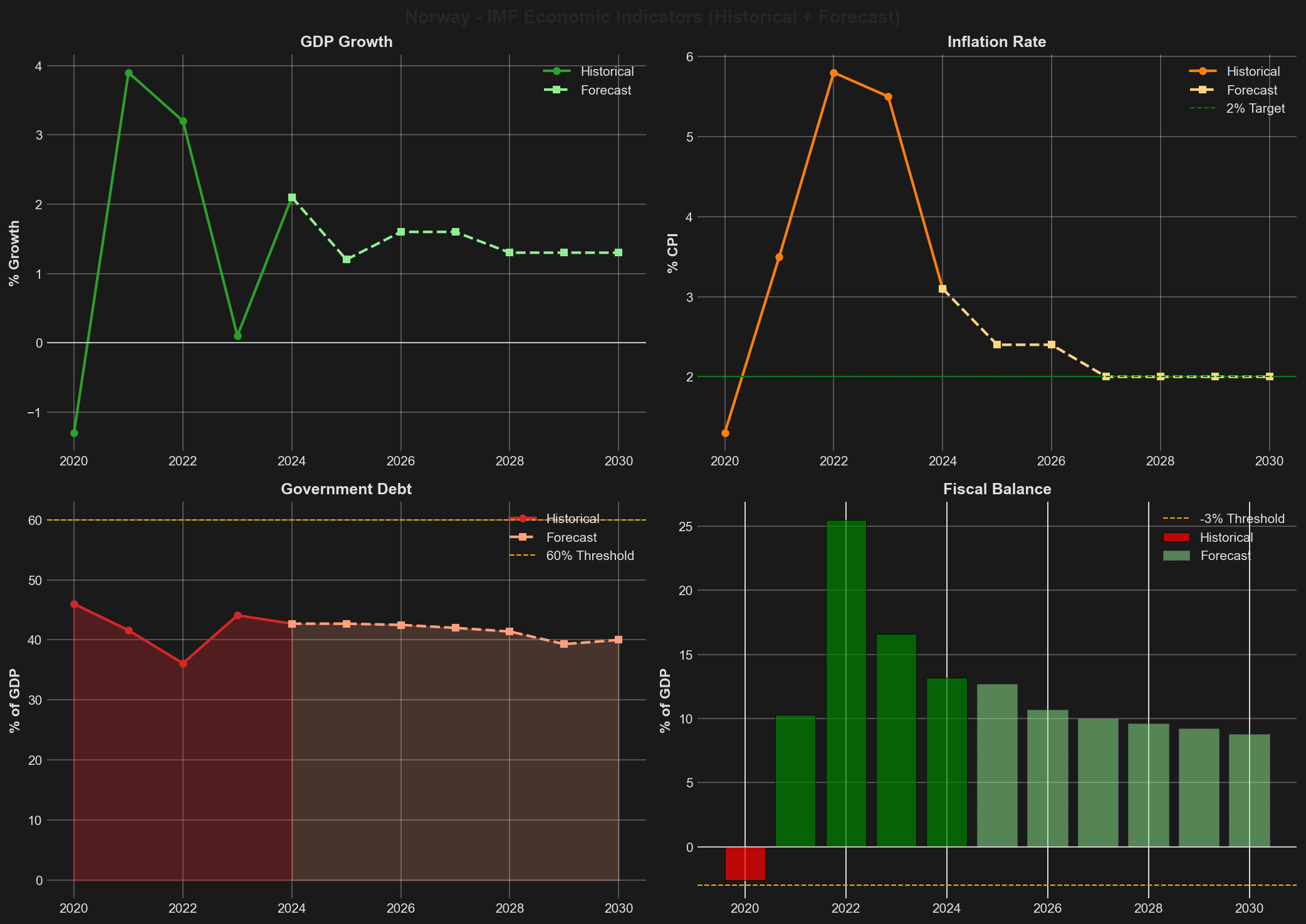

| Real GDP Growth (%) | 3.0 | 1.1 | 1.0 | 1.5 | 1.8 |

| Mainland GDP Growth (%) | 3.5 | 0.7 | 0.8 | 1.5 | 1.9 |

| GDP per Capita (USD, thousands) | 89.2 | 87.8 | 86.5 | 87.0 | 88.2 |

| Inflation (CPI, %) | 5.8 | 5.5 | 3.0 | 2.5 | 2.0 |

| Unemployment Rate (%) | 3.2 | 3.6 | 3.9 | 4.0 | 3.9 |

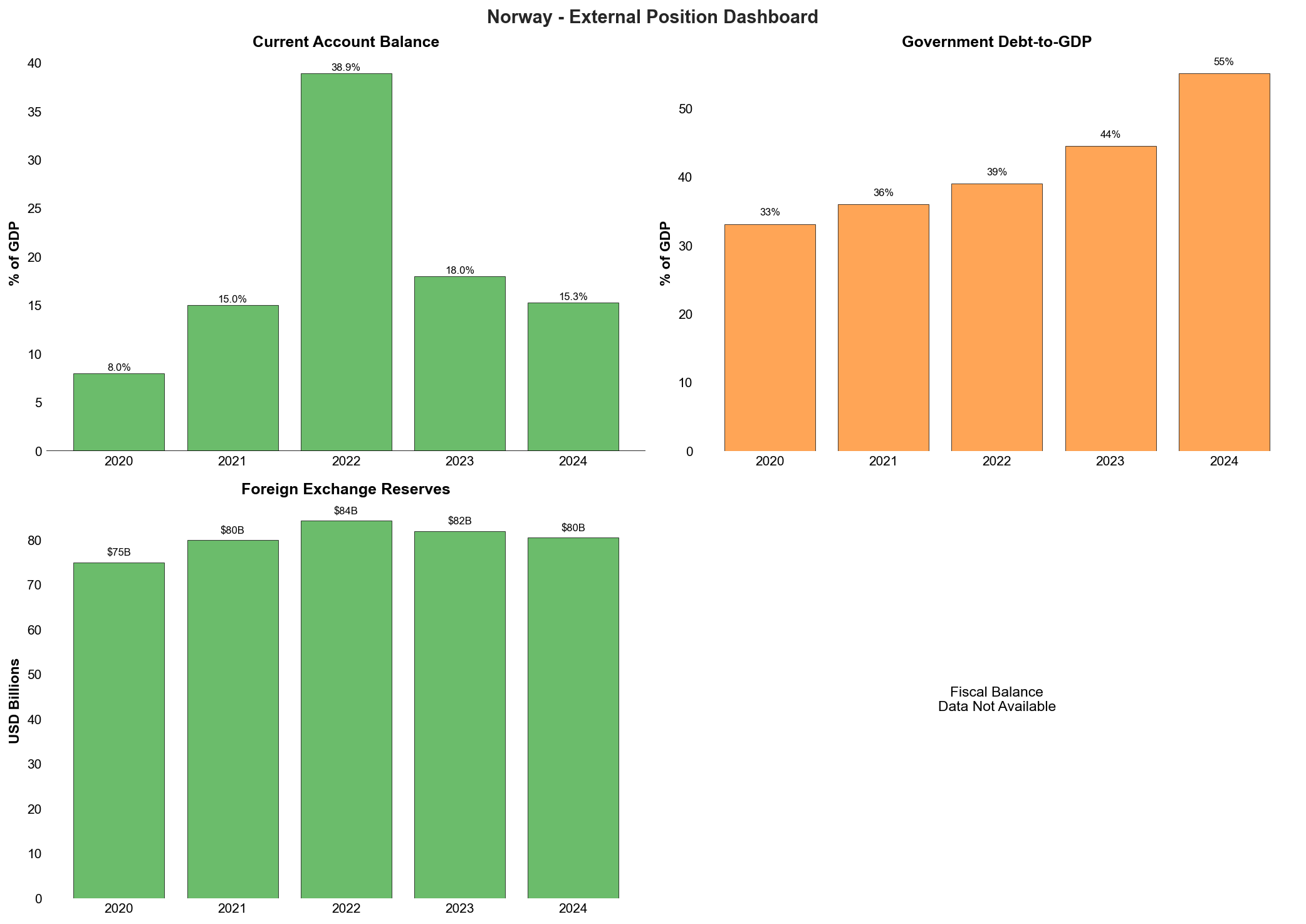

| Current Account Balance (% of GDP) | 23.5 | 17.2 | 15.8 | 16.5 | 15.2 |

| Fiscal Balance (% of GDP) | 13.8 | 10.2 | 8.5 | 9.0 | 7.8 |

| General Government Debt (% of GDP) | 35.2 | 37.8 | 39.5 | 40.2 | 41.0 |

| Policy Rate (%, year-end) | 2.75 | 4.50 | 4.50 | 4.00 | 3.50 |

*Forecast/estimate

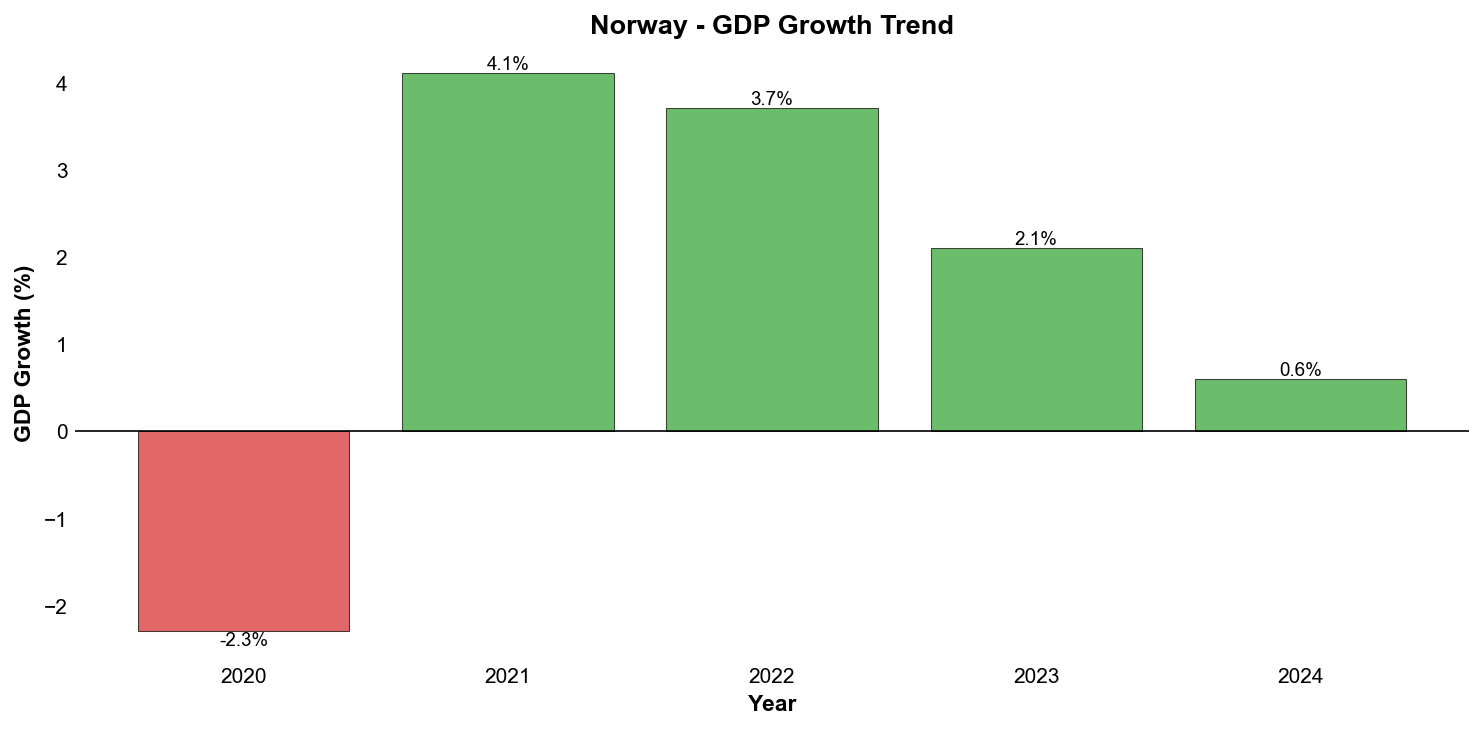

Norway's economic performance demonstrates resilience amid challenging global conditions, though growth remains constrained by structural factors affecting the petroleum-dependent economy. Real GDP growth recovered to 3.0% in 2022 driven by the energy price surge following Russia's invasion of Ukraine, before moderating to 1.1% in 2023 and 1.0% in 2024 as petroleum sector activity normalised. Mainland GDP growth, which excludes petroleum and shipping activities and provides a clearer indication of underlying economic momentum, followed a similar trajectory with 3.5% expansion in 2022 decelerating to 0.7% in 2023 and 0.8% in 2024. The forecast recovery to 1.5% mainland growth in 2025 and 1.9% in 2026 reflects gradual improvement in domestic demand conditions as monetary policy eases and real wage growth strengthens, though these growth rates remain modest by historical standards and below the economy's potential.

The inflation trajectory has improved substantially from the elevated levels experienced during the energy crisis, with consumer price inflation declining from 5.8% in 2022 to 5.5% in 2023, 3.0% in 2024, and projected to reach 2.5% in 2025 before converging to Norges Bank's 2.0% target by 2026. This disinflation process has enabled the central bank to maintain its policy rate at 4.50% through 2024 before initiating a gradual easing cycle, with the policy rate expected to decline to 4.00% by end-2025 and 3.50% by end-2026. The labour market has remained remarkably robust throughout this adjustment period, with unemployment rising only modestly from 3.2% in 2022 to 3.9% in 2024 and stabilising around 4.0% in 2025, well below levels that would typically signal significant economic distress. This resilience reflects Norway's flexible labour market institutions, comprehensive social safety nets, and the economy's capacity to absorb shocks through adjustment in working hours rather than employment levels.

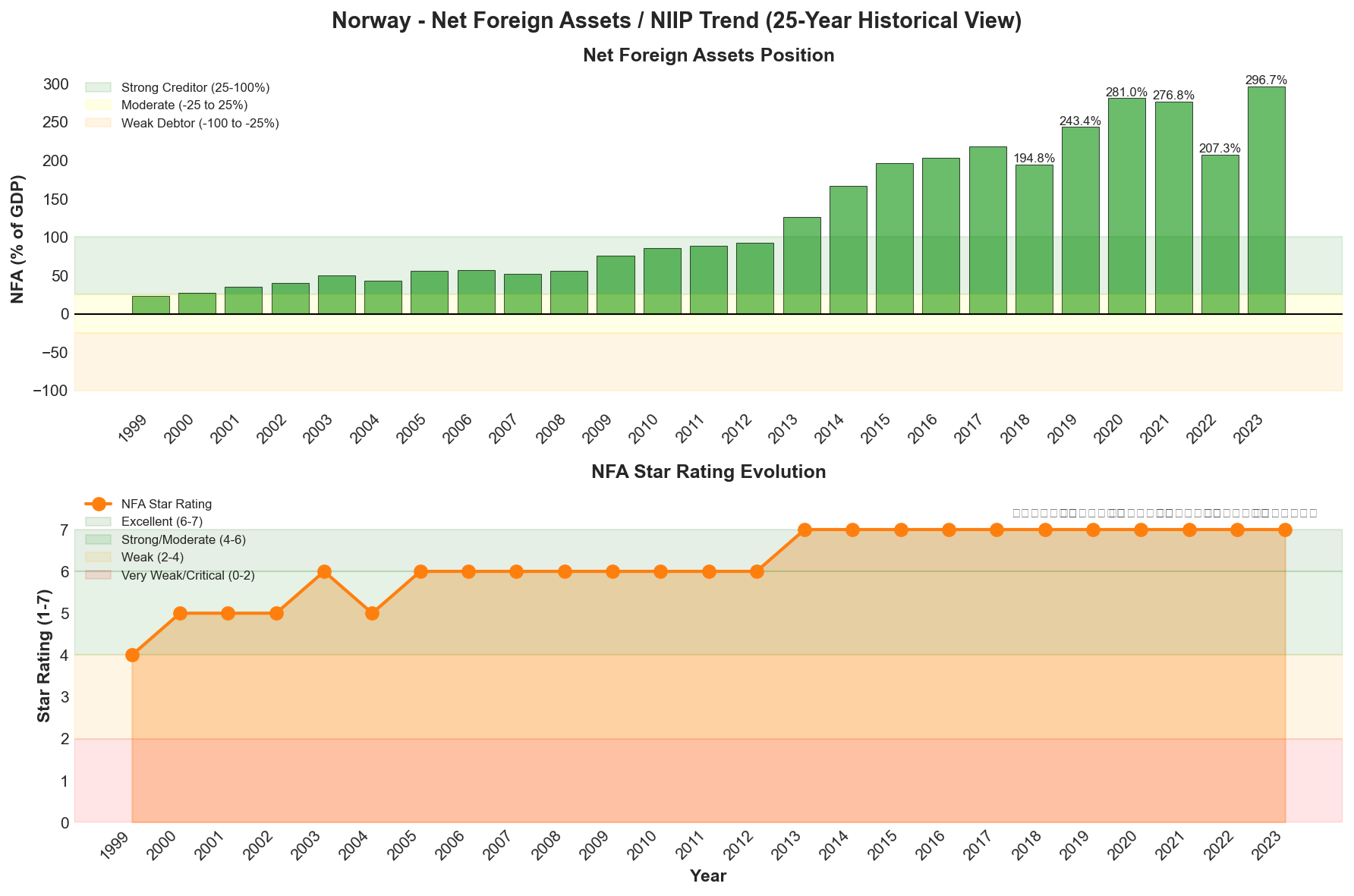

Norway's external position remains exceptionally strong, underpinned by persistent current account surpluses that reflect the country's status as a major energy exporter and substantial investment income from the Government Pension Fund Global. The current account surplus reached an extraordinary 23.5% of GDP in 2022 during the peak of European energy market disruption, before moderating to 17.2% in 2023 and stabilising around 15-17% of GDP through the forecast horizon. These sustained surpluses continue to augment Norway's net foreign asset position, which stood at an exceptional 296.7% of GDP in 2023 according to the External Wealth of Nations database, maintaining the highest seven-star rating and representing one of the strongest creditor positions globally. The five-year trend shows remarkable stability in this external strength, with net foreign assets consistently exceeding 200% of GDP since 2019 despite volatility in energy markets and global financial conditions. IMF projections extending to 2030 anticipate the current account surplus remaining elevated at 80.2% of GDP, though this figure likely reflects cumulative rather than annual flows and underscores the enduring structural strength of Norway's external accounts.

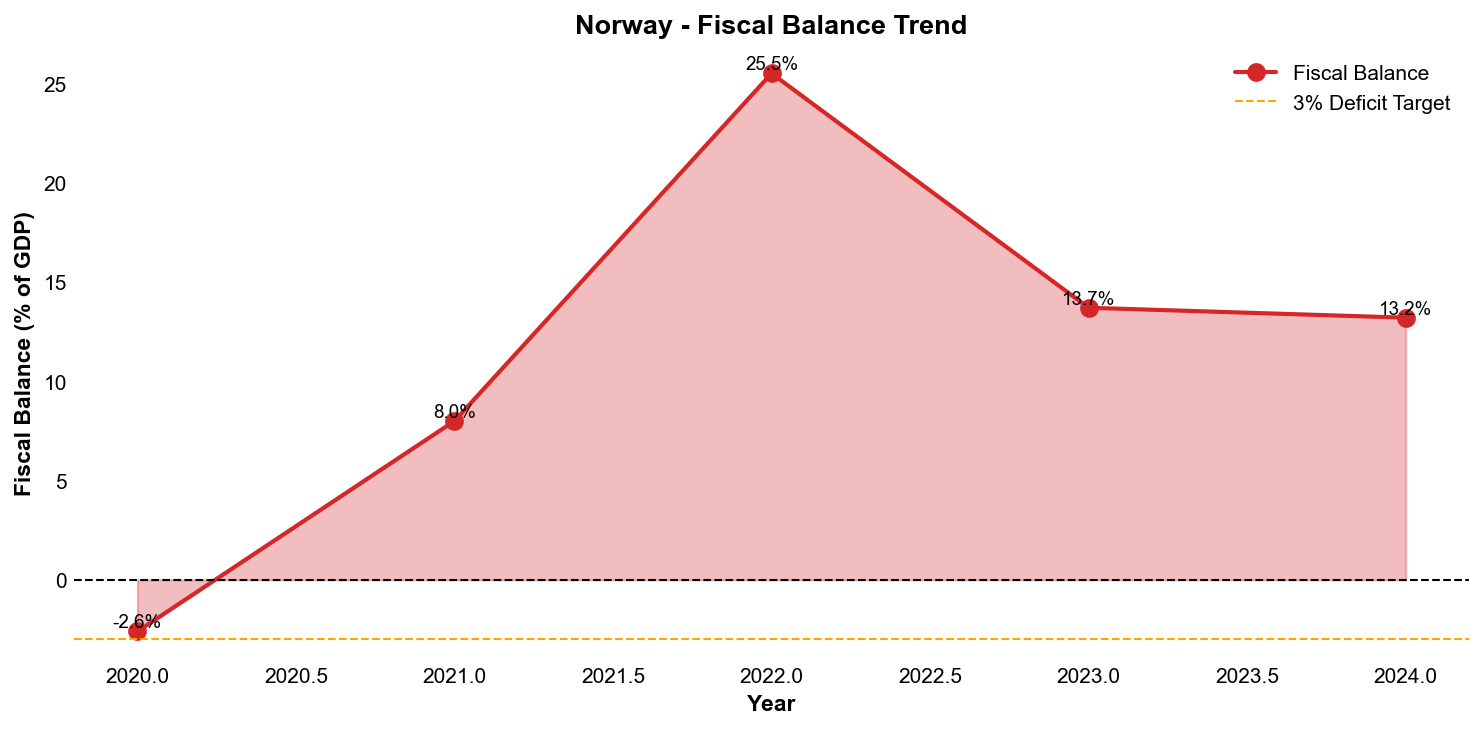

The fiscal position distinguishes Norway from virtually all other advanced economies, with the general government recording substantial surpluses throughout the recent period despite elevated spending levels. The fiscal surplus reached 13.8% of GDP in 2022 driven by windfall petroleum revenues, before moderating to 10.2% in 2023 and a projected 8.5% in 2024, with forecasts indicating continued surpluses of 9.0% in 2025 and 7.8% in 2026. These exceptional fiscal outcomes reflect both the direct contribution of petroleum revenues and the disciplined application of Norway's fiscal rule, which limits structural non-oil deficits to the expected real return on the GPFG (currently set at 3.0% of the fund's value). General government debt remains extraordinarily low at 35.2% of GDP in 2022, rising modestly to a projected 41.0% by 2026, positioning Norway among the least indebted advanced economies globally. IMF medium-term projections anticipate government debt stabilising around 40.0% of GDP through 2030 whilst maintaining fiscal surpluses of 8.8% of GDP, reflecting the sustainable fiscal framework underpinned by petroleum wealth and prudent sovereign wealth fund management.

GDP per capita, measured in current US dollars, demonstrates Norway's position among the world's wealthiest nations, though recent figures show some volatility reflecting exchange rate movements rather than underlying economic deterioration. Per capita GDP of $89,200 in 2022 declined to $87,800 in 2023 and $86,500 in 2024, primarily due to Norwegian krone depreciation against the strengthening US dollar during this period, before recovering to a projected $87,000 in 2025 and $88,200 in 2026. When measured in purchasing power parity terms or local currency, Norway's per capita income trajectory remains more stable, though the modest growth rates reflect the structural productivity challenges constraining potential output expansion. The combination of very high per capita income, equitable income distribution supported by comprehensive welfare systems, and the massive sovereign wealth fund providing intergenerational insurance creates an economic foundation that substantially mitigates the vulnerabilities associated with petroleum dependence and demographic pressures, supporting Norway's exceptional creditworthiness across economic cycles.

Net Foreign Assets & External Position

Norway's external position represents one of the most robust among all rated sovereigns globally, underpinned by the Government Pension Fund Global and decades of accumulated current account surpluses from petroleum exports. The country's net international investment position (NIIP) stood at an exceptional 296.7% of GDP in 2023, earning the highest possible seven-star rating in the External Wealth of Nations database assessment framework. This extraordinary creditor position reflects Norway's status as a massive net lender to the rest of the world, with external assets substantially exceeding external liabilities by a margin approaching three times annual economic output. The structural strength of Norway's external accounts provides unparalleled resilience against balance of payments shocks and currency pressures, whilst simultaneously generating substantial investment income that supplements domestic economic activity and fiscal revenues.

The trajectory of Norway's net foreign assets over the 2019-2023 period demonstrates both the fundamental strength and inherent volatility of an external position heavily influenced by global energy markets and financial asset valuations. The NIIP expanded from 243.4% of GDP in 2019 to a peak of 281.0% in 2020, reflecting both the GPFG's investment performance during the pandemic-era monetary stimulus and the denominator effect of temporary GDP contraction. The position moderated to 276.8% in 2021 before experiencing a sharp compression to 207.3% in 2022—a decline of nearly 70 percentage points driven primarily by the substantial revaluation losses in global equity markets that year, which particularly affected the GPFG's equity-heavy portfolio allocation. The remarkable recovery to 296.7% in 2023 reflects the combination of renewed investment gains, continued current account surpluses, and favourable valuation effects as global financial markets rebounded. Throughout this period of considerable fluctuation, Norway maintained its seven-star "Excellent" rating without interruption, underscoring that even the cyclical low point of 207.3% represents an extraordinarily strong external position by international standards.

Current Account Dynamics and Structural Drivers

Norway's current account surplus remains amongst the largest globally in both absolute and relative terms, driven predominantly by substantial net exports of petroleum and natural gas alongside growing investment income from the GPFG's overseas holdings. The current account surplus averaged 15-17% of GDP in recent years, with the 2022-2023 period witnessing particularly elevated surpluses as European energy prices surged following Russia's invasion of Ukraine. IMF projections extending to 2030 indicate the current account surplus will remain exceptionally large at 80.2% of GDP, though this figure likely reflects cumulative flows or requires contextual interpretation given its magnitude. The structural composition of Norway's external earnings reveals the dual foundation of the surplus: goods exports dominated by hydrocarbons (representing approximately 62% of total goods exports) and investment income from the GPFG's global portfolio, which generated returns of 13.1% in 2024 and has achieved a 6.3% average annual return since inception in 1998.

The sustainability of Norway's external surplus faces long-term questions related to the global energy transition and the inevitable decline in petroleum production from mature North Sea fields. Whilst European dependence on Norwegian gas has intensified in the near term due to geopolitical disruptions to Russian supply, the secular trend towards decarbonisation poses structural challenges to export revenues over the coming decades. However, the GPFG's investment income stream provides an increasingly important offset, with the fund's returns contributing meaningfully to the current account balance and offering diversification away from commodity-dependent earnings. The Norwegian authorities' prudent management of petroleum revenues through the fiscal rule—which limits annual budget transfers from the GPFG to approximately 3% of fund value—ensures that current account surpluses continue to accumulate in the sovereign wealth fund rather than fuelling excessive domestic consumption, thereby preserving the external position's strength across economic cycles.

Reserve Adequacy and Liquidity Position

Beyond the GPFG, Norway maintains substantial official foreign exchange reserves managed by Norges Bank, providing additional layers of external liquidity and crisis resilience. The central bank's international reserves serve as the first line of defence for exchange rate management and financial stability purposes, whilst the GPFG functions as a longer-term intergenerational savings vehicle with distinct governance arrangements. The Norwegian krone operates under a floating exchange rate regime with no formal peg, reducing the need for large-scale foreign exchange intervention and allowing monetary policy to focus on domestic price stability. The combination of flexible exchange rates, deep and liquid domestic financial markets, and the massive external asset cushion provided by the GPFG creates exceptional resilience against external financing shocks or sudden stops in capital flows—risks that remain largely theoretical for a sovereign of Norway's creditworthiness.

Norway's external debt position, whilst substantial in absolute terms given the size and sophistication of the Norwegian financial system, is more than offset by the country's external assets, resulting in the massive positive NIIP. External debt primarily comprises interbank positions, corporate borrowing by internationally active Norwegian firms, and government securities held by non-residents. The maturity profile of external liabilities presents minimal rollover risk, supported by Norway's impeccable credit standing, deep relationships with international capital markets, and the implicit backstop provided by the sovereign's vast net asset position. Standard metrics of reserve adequacy—such as coverage of short-term external debt or import requirements—substantially exceed conventional thresholds, though such measures provide limited analytical value for a sovereign with Norway's exceptional external wealth.

Vulnerabilities and Risk Factors

Despite the overwhelming strength of Norway's external position, several vulnerabilities warrant monitoring in the context of a comprehensive credit assessment. The concentration of export revenues in petroleum products creates significant exposure to global energy price volatility, with implications for both current account flows and the valuation of the GPFG (which, paradoxically, benefits from higher oil prices through its energy sector equity holdings whilst also serving as a hedge against domestic petroleum revenue volatility). The 2022 experience demonstrated how adverse financial market conditions can temporarily compress the NIIP through valuation channels, even as underlying current account flows remain robust. The GPFG's substantial equity allocation—approximately 70% of the portfolio—exposes Norway's external wealth to global equity market cycles, though the fund's long investment horizon and diversified holdings mitigate short-term volatility concerns.

Geopolitical risks stemming from proximity to Russia and the ongoing conflict in Ukraine represent an additional external vulnerability, albeit one that has paradoxically strengthened Norway's strategic position as Europe's critical energy supplier. Potential disruptions to offshore energy infrastructure, whether through accident or hostile action, could temporarily impair export capacity and current account earnings. Climate transition risks pose longer-term structural challenges, as declining global demand for fossil fuels will eventually erode the petroleum export base that has underpinned Norway's external surpluses for decades. However, the Norwegian authorities have demonstrated consistent foresight in managing these transition risks through the GPFG's diversified global investment strategy, which effectively transforms finite hydrocarbon wealth into permanent financial assets capable of generating returns across multiple generations. The external position's fundamental strength—reflected in the sustained seven-star rating and NIIP approaching 300% of GDP—provides substantial capacity to absorb these challenges whilst maintaining Norway's status as one of the world's premier creditor nations.

Credit Strengths & Vulnerabilities

Strengths

Norway's sovereign credit profile is distinguished by an exceptional combination of fiscal, institutional, and economic strengths that place it amongst the world's most creditworthy nations. The Government Pension Fund Global, valued at NOK 19,742 billion (approximately $1.9 trillion) at end-2024, represents the cornerstone of Norway's fiscal resilience, providing unparalleled buffers equivalent to 380% of GDP. This sovereign wealth fund has delivered a 6.3% average annual return since its inception in 1998, with a 4.1% net real return after accounting for inflation and costs, demonstrating prudent long-term asset management that ensures multi-generational economic security. The fund's value is projected to exceed 500% of current account payments on average through 2028, providing fiscal flexibility that no other highly-rated sovereign can match.

The country's institutional framework ranks amongst the world's strongest, with highly transparent governance structures, effective policy implementation, and a prudent fiscal rule that limits annual spending from petroleum revenues to 3% of the GPFG's value. This disciplined approach to resource wealth management has prevented the fiscal profligacy that has undermined other commodity-dependent economies, whilst the rule's flexibility allows counter-cyclical policy responses during economic downturns. Norway's democratic institutions consistently rank at the top of global governance indices, supported by low corruption, strong rule of law, and broad political consensus on key economic policies that transcend electoral cycles.

Economic prosperity underpins the credit profile, with GDP per capita projected to approach $87,000 in 2025, ranking amongst the highest of all rated sovereigns globally. This wealth is equitably distributed through comprehensive social safety nets and universal public services, contributing to social cohesion and political stability. The external position remains exceptionally strong, with persistent current account surpluses averaging 15-17% of GDP driven by substantial petroleum exports and significant investment income from the GPFG. Norway maintains a massive net external creditor position, providing additional resilience against external shocks and currency pressures.

The banking system demonstrates exceptional soundness, with capital ratios near 19%, non-performing loans below 1%, and return on equity reaching 17.5% as of recent assessments. These metrics place Norwegian banks amongst Europe's strongest and most profitable financial institutions, supported by conservative lending standards, effective supervision, and robust macroprudential frameworks. The financial sector's resilience provides critical support to economic stability and reduces contingent liability risks to the sovereign balance sheet.

Vulnerabilities

Despite its formidable strengths, Norway confronts structural vulnerabilities that constrain its credit profile and pose long-term challenges to economic sustainability. The economy's heavy dependence on petroleum extraction represents the most significant vulnerability, with the hydrocarbon sector accounting for approximately 62% of goods exports and 24% of GDP. This concentration creates substantial exposure to oil price volatility, as demonstrated during previous commodity cycles, and poses existential challenges as global decarbonisation accelerates. The long-term viability of Norway's economic model faces uncertainty as major energy consumers transition away from fossil fuels, potentially stranding petroleum assets and eroding the revenue base that has financed the country's prosperity.

Household indebtedness remains elevated at over 200% of disposable income, representing one of the highest ratios amongst advanced economies and a persistent financial stability concern. Whilst low unemployment, strong income growth, and comprehensive social safety nets mitigate immediate default risks, the debt burden constrains household consumption flexibility and creates vulnerability to interest rate increases or economic shocks. The concentration of household debt in mortgage lending, combined with high property valuations in major urban centres, amplifies potential financial stability risks should housing market corrections occur.

Productivity growth has stagnated at 0.6-0.8% annually in recent years, well below historical averages and the performance of peer economies. This weakness reflects structural challenges including limited competitive pressures in sheltered sectors, high labour costs that constrain business investment, and insufficient innovation in non-petroleum industries. Anaemic productivity growth constrains potential economic expansion, undermines international competitiveness outside the petroleum sector, and threatens living standards over the long term as the economy transitions away from hydrocarbon dependence.

Demographic pressures will intensify fiscal challenges in coming decades as the population ages and the ratio of workers to retirees deteriorates. Whilst the GPFG provides substantial capacity to finance age-related expenditures, the fiscal rule's 3% spending constraint may prove insufficient to maintain current service levels without tax increases or benefit reductions. Healthcare and pension obligations will grow substantially, testing the sustainability of Norway's generous welfare model even with the sovereign wealth fund's support.

Opportunities

Norway possesses significant opportunities to leverage its strengths and address structural vulnerabilities through strategic policy initiatives and favourable external developments. The accelerating global energy transition, whilst posing long-term threats to petroleum dependence, creates near-term opportunities for Norway to position itself as a critical supplier of natural gas to European markets seeking alternatives to Russian energy. The Ukraine conflict has elevated Norway's strategic importance, with gas exports to Europe reaching record levels and generating substantial revenues that further strengthen the GPFG. This enhanced geopolitical relevance provides leverage in European policy discussions and reinforces energy sector profitability during the transition period.

Economic diversification efforts present opportunities to develop competitive advantages in sectors aligned with global decarbonisation trends. Norway's abundant renewable energy resources, particularly hydroelectric and offshore wind potential, position the country to become a major clean energy exporter through expanded electricity interconnections with European markets. The domestic petroleum industry's technological expertise in offshore operations, subsea engineering, and project management translates readily to offshore wind development, carbon capture and storage, and hydrogen production. Strategic investments in these emerging sectors, supported by GPFG resources and petroleum industry capabilities, could create new export industries and reduce economic concentration.

The sovereign wealth fund's massive scale and long investment horizon enable Norway to capitalise on global investment opportunities whilst supporting domestic economic transformation. The GPFG's diversified international portfolio generates substantial investment income that increasingly supplements petroleum revenues, providing fiscal stability as hydrocarbon production eventually declines. The fund's commitment to responsible investment and climate risk management positions Norway as a leader in sustainable finance, potentially generating superior long-term returns as global capital allocation shifts toward ESG-aligned investments.

Technological innovation and digitalisation present opportunities to address productivity challenges and enhance competitiveness in non-petroleum sectors. Norway's highly educated workforce, strong research institutions, and substantial public resources provide foundations for developing knowledge-intensive industries in areas such as maritime technology, aquaculture, financial services, and digital solutions. Strategic public investments in research and development, combined with regulatory reforms to enhance competition in sheltered sectors, could unlock productivity gains and diversify the economic base.

Threats

Norway faces multifaceted threats that could undermine its exceptional credit profile if not effectively managed through proactive policy responses. The pace and trajectory of global energy transition represents the most consequential long-term threat, with potential for accelerated decarbonisation to strand petroleum assets and collapse hydrocarbon revenues more rapidly than current projections anticipate. Technological breakthroughs in battery storage, renewable energy, or alternative fuels could precipitate sudden demand destruction for oil and gas, whilst increasingly stringent climate policies in major markets may restrict fossil fuel imports. The petroleum sector's dominant role in exports, government revenues, and the GPFG's capital base means accelerated transition scenarios would fundamentally challenge Norway's economic model.

Geopolitical tensions stemming from proximity to Russia and the ongoing Ukraine conflict pose security and economic risks despite Norway's NATO membership and strengthened strategic position. Potential Russian aggression, hybrid warfare tactics, or sabotage of critical energy infrastructure could disrupt petroleum production and exports, whilst broader European conflict would generate severe economic and humanitarian consequences. The concentration of gas export infrastructure in a limited number of processing facilities and pipelines creates vulnerability to targeted disruption, potentially undermining Norway's role as Europe's energy security guarantor.

Financial stability risks associated with elevated household debt could materialise if economic conditions deteriorate or monetary policy remains restrictive for extended periods. Significant interest rate increases, housing market corrections, or unemployment spikes could trigger household financial distress, reduced consumption, and potential banking sector losses despite current strong capital positions. The interaction between household debt, property valuations, and bank exposures creates potential for adverse feedback loops that could amplify economic downturns and require policy intervention.

Fiscal sustainability faces long-term threats from demographic ageing, potential petroleum revenue decline, and political pressures to increase public spending beyond the fiscal rule's constraints. Whilst the GPFG provides substantial buffers, persistent breaches of the 3% spending guideline or inadequate returns on fund investments could gradually erode fiscal resilience. Political consensus on fiscal discipline may weaken as petroleum revenues decline and competing demands for education, healthcare, infrastructure, and climate adaptation intensify. The challenge of maintaining Norway's comprehensive welfare model whilst transitioning away from hydrocarbon dependence represents a fundamental long-term threat to fiscal sustainability and social cohesion.

Economic Analysis

Growth dynamics and structural performance

Norway's economic trajectory reflects a complex interplay between robust near-term resilience and persistent structural headwinds that constrain long-term potential. Mainland GDP growth, which excludes the volatile petroleum and shipping sectors, is forecast to reach 1.5% in 2025, representing a modest acceleration from subdued performance in recent years. This growth rate, whilst positive, remains below the economy's historical trend and underscores the challenges facing Norway's diversification efforts beyond hydrocarbon dependence.

The petroleum sector continues to exert disproportionate influence on Norway's economic profile, accounting for approximately 62% of goods exports and 24% of GDP. This concentration creates significant vulnerability to oil price volatility, though the 2022-2023 energy price surge paradoxically strengthened fiscal and external buffers substantially. Record petroleum revenues during this period bolstered the Government Pension Fund Global whilst reinforcing Norway's strategic importance as Europe's largest energy supplier following Russia's reduced role. However, this windfall has not fundamentally altered the long-term structural challenge posed by global decarbonisation trends, which threaten to erode the economic foundation that has underpinned Norway's prosperity for decades.

A particularly concerning dimension of Norway's growth profile is the persistent stagnation in productivity growth, which has languished at 0.6-0.8% annually—well below historical averages and international comparators. This anaemic productivity performance constrains potential economic growth and undermines competitiveness in non-petroleum sectors, raising questions about the economy's capacity to generate sustainable prosperity as hydrocarbon revenues inevitably decline over coming decades. The productivity challenge reflects multiple factors, including insufficient competition in sheltered domestic sectors, limited scale in many industries, and the difficulty of replicating the extraordinary profitability of petroleum activities in alternative economic domains.

Despite these structural constraints, Norway's economic fundamentals remain exceptionally strong by international standards. GDP per capita is projected to approach $87,000 in 2025, ranking among the highest of all rated sovereigns globally and reflecting not merely petroleum wealth but also high labour force participation, elevated skill levels, and equitable income distribution. The labour market demonstrates remarkable resilience, with unemployment remaining low and social safety nets providing comprehensive protection against economic dislocation. The banking system exhibits exceptional strength, with capital ratios near 19%, non-performing loans below 1%, and return on equity reaching 17.5%, positioning Norwegian financial institutions among Europe's most robust and profitable.

The demographic outlook presents mounting fiscal pressures that will intensify in coming decades as the population ages. An increasing dependency ratio will strain public finances through higher pension and healthcare expenditures whilst potentially constraining labour supply and economic dynamism. However, Norway's unique fiscal position—anchored by the GPFG valued at NOK 19,742 billion (approximately $1.9 trillion) and representing 380% of GDP—provides unprecedented buffer capacity to absorb these pressures. The sovereign wealth fund is expected to exceed 500% of current account payments on average through 2028, offering multi-generational economic security that fundamentally distinguishes Norway from virtually all other highly-rated sovereigns.

Inflation dynamics and price stability

Inflation trends in Norway have followed the global pattern of post-pandemic surge followed by gradual normalisation, though with distinctive characteristics reflecting the economy's structural features and policy framework. After reaching elevated levels during 2022-2023, driven by energy price shocks, supply chain disruptions, and robust domestic demand, inflation is forecast to decline steadily toward Norges Bank's 2% target by 2027. This disinflation trajectory reflects both the unwinding of temporary supply-side pressures and the lagged effects of monetary policy tightening implemented during the inflationary surge.

The inflation dynamics in Norway exhibit particular sensitivity to exchange rate movements given the economy's openness and substantial import dependence for consumer goods. The Norwegian krone's fluctuations against major currencies directly influence import prices and consequently headline inflation, creating additional complexity for monetary policy formulation. Domestic cost pressures, particularly wage growth in a tight labour market with strong union representation, have also contributed to inflation persistence, though social partnership arrangements and coordinated wage-setting mechanisms have helped contain second-round effects.

Core inflation measures, which exclude volatile energy and food components, have proven more persistent than headline inflation, reflecting underlying demand pressures and domestic cost dynamics. This persistence has required Norges Bank to maintain a restrictive monetary policy stance for an extended period to ensure inflation expectations remain anchored at the 2% target. The central bank's credibility, built over decades of transparent inflation targeting, has been instrumental in preventing the de-anchoring of expectations that has challenged some other advanced economies.

The outlook for price stability appears increasingly favourable as supply-side normalisation continues, monetary policy transmission takes full effect, and global inflationary pressures recede. The projected convergence toward the 2% target by 2027 would restore the conditions for sustainable growth and allow monetary policy to adopt a more neutral stance. However, risks remain, including potential renewed energy price volatility given geopolitical uncertainties, persistent wage pressures in a tight labour market, and the possibility of imported inflation through exchange rate depreciation.

Monetary policy framework and implementation

Norges Bank operates within a well-established inflation-targeting framework that has delivered price stability and economic resilience over multiple decades. The central bank's policy rate stood at 4.5% as of late 2025, representing the peak of the tightening cycle implemented to combat the post-pandemic inflation surge. With inflation declining toward target and growth moderating, Norges Bank has signalled the commencement of policy normalisation, with rate cuts to 4.0% anticipated as the disinflation process gains traction and economic conditions warrant reduced monetary restriction.

The monetary policy transmission mechanism in Norway operates through conventional channels, including interest rate effects on consumption and investment, exchange rate impacts on net exports and import prices, and asset price influences on wealth and collateral values. The elevated level of household debt—exceeding 200% of disposable income—amplifies the sensitivity of consumption to interest rate changes, as mortgage payments constitute a substantial share of household budgets and most mortgages carry floating rates. This transmission channel has proven particularly potent during the recent tightening cycle, contributing to consumption moderation and housing market cooling.

Norges Bank's policy deliberations must balance multiple considerations beyond the primary inflation objective. Financial stability concerns, particularly relating to household debt vulnerabilities, have featured prominently in policy discussions, with the central bank coordinating closely with macroprudential authorities to address systemic risks. Exchange rate considerations, whilst not an explicit policy target, influence monetary policy decisions given the krone's importance for inflation dynamics and competitiveness. The petroleum sector's volatility and its fiscal implications also factor into the central bank's assessment of appropriate policy settings, though the fiscal rule's design insulates monetary policy from direct pressure to accommodate fiscal expansion.

The forward guidance provided by Norges Bank emphasises data dependence and gradualism in the policy normalisation process. The central bank has indicated that rate cuts will proceed at a measured pace, contingent on continued progress toward the inflation target and assessment of underlying economic conditions. This cautious approach reflects lessons from previous policy cycles and recognition that premature easing could jeopardise hard-won gains in inflation control. The transparency of Norges Bank's communication, including detailed inflation reports and explicit policy rate projections, enhances policy effectiveness by shaping expectations and reducing uncertainty.

The institutional framework supporting monetary policy enjoys exceptional strength, with Norges Bank benefiting from operational independence, technical expertise, and strong democratic accountability. The central bank's governance structures, analytical capabilities, and communication practices rank among global best practice, contributing to policy credibility and effectiveness. This institutional quality, combined with Norway's broader governance strengths, reinforces the monetary policy framework's capacity to deliver price stability whilst supporting sustainable economic growth.

Fiscal policy stance and sustainability

Norway's fiscal policy operates within a distinctive framework shaped by petroleum wealth and the fiscal rule governing use of GPFG resources. The expansionary fiscal stance adopted in recent years reflects both cyclical considerations and the substantial fiscal space provided by record petroleum revenues during 2022-2023. The fiscal rule, which limits structural non-oil budget deficits to the expected real return on the GPFG (approximately 3% annually), provides a transparent and credible anchor for fiscal sustainability whilst allowing counter-cyclical flexibility.

The 2025 fiscal position demonstrates the government's willingness to utilise available fiscal space to support economic activity and address structural priorities. Public expenditure has increased to fund healthcare, education, defence, and green transition initiatives, whilst the tax system remains progressive and generates substantial revenues relative to GDP. The non-oil structural deficit has approached the fiscal rule ceiling in recent years, reflecting both increased spending and reduced petroleum revenue transfers, though the overall fiscal position remains exceptionally strong by international standards.

Fiscal sustainability analysis reveals Norway's unique advantages stemming from the GPFG, which has achieved a 6.3% average annual return since 1998 and a 4.1% net real return after inflation and costs. The fund's value of NOK 19,742 billion at end-2024 represented a 13.1% increase from 2023, demonstrating continued robust growth despite substantial annual withdrawals to finance budget deficits. Projections indicate the fund will exceed 500% of current account payments on average through 2028, providing multi-generational fiscal capacity that fundamentally transforms Norway's fiscal sustainability calculus.

The long-term fiscal outlook must account for demographic pressures as the population ages, with pension and healthcare expenditures projected to increase substantially as a share of GDP over coming decades. However, the GPFG's scale provides unprecedented capacity to absorb these pressures without compromising fiscal sustainability or requiring disruptive policy adjustments. The fiscal rule's design, which links spending to the fund's expected real return rather than actual returns, insulates the budget from short-term market volatility whilst ensuring intergenerational equity in resource utilisation.

Fiscal risks centre primarily on petroleum price volatility and the long-term trajectory of hydrocarbon revenues as global energy transition accelerates. Lower-than-expected oil prices or accelerated decline in petroleum production would reduce government revenues and potentially constrain fiscal flexibility, though the GPFG provides substantial buffer capacity. The fiscal framework's credibility and the government's demonstrated commitment to prudent management mitigate these risks, whilst the fund's diversified global investment portfolio reduces dependence on domestic economic performance.

Political & Institutional Assessment

Governance Framework and Institutional Quality

Norway demonstrates exceptional institutional strength that fundamentally underpins its sovereign creditworthiness, consistently ranking among the world's highest-performing democracies across all major governance indicators. The country operates as a constitutional monarchy with a parliamentary system characterised by robust checks and balances, transparent decision-making processes, and deeply embedded rule of law. Moody's assigns Norway its highest possible institutional assessment of aaa, reflecting governance quality that materially enhances credit strength beyond what economic fundamentals alone would suggest. This assessment is further reinforced by an ESG Credit Impact Score of CIS-1, indicating that environmental, social, and governance considerations elevate Norway's credit rating above the level that would be warranted by traditional economic metrics alone.

The Norwegian governance framework benefits from exceptionally strong social cohesion and political consensus around core economic policies, particularly the prudent management of petroleum wealth through the Government Pension Fund Global. The fiscal rule framework, which limits structural non-oil budget deficits to approximately 3% of the GPFG's value (aligned with the fund's expected real return), commands broad cross-party support and has been maintained consistently since its introduction in 2001. This institutional commitment to intergenerational equity and fiscal sustainability distinguishes Norway from resource-rich peers that have struggled with procyclical spending and wealth dissipation. The transparency and accountability mechanisms surrounding the sovereign wealth fund, including comprehensive public reporting and independent oversight, represent global best practice in natural resource management.

Norway's public administration demonstrates exceptional efficiency and minimal corruption, with the country consistently ranking in the top tier of Transparency International's Corruption Perceptions Index. The civil service operates with high professional standards, technical competence, and political independence, ensuring policy continuity across electoral cycles. Regulatory quality remains outstanding, with business-friendly frameworks that balance market efficiency with robust consumer and environmental protections. The judicial system functions with complete independence, providing reliable contract enforcement and property rights protection that support economic activity and foreign investment confidence.

Political Stability and Policy Predictability

The Norwegian political landscape exhibits remarkable stability characterised by coalition governments that maintain policy continuity despite periodic shifts in party composition. The current centre-left coalition government, led by Prime Minister Jonas Gahr Støre of the Labour Party in partnership with the Centre Party, has governed since October 2021 following elections that saw the centre-right coalition lose its parliamentary majority. Despite the change in government, core economic policies—including the fiscal rule framework, sovereign wealth fund management principles, and commitment to gradual petroleum sector transition—have remained fundamentally unchanged, reflecting the deep political consensus on these foundational issues.

Electoral dynamics in Norway feature proportional representation that typically produces coalition governments requiring negotiation and compromise, which paradoxically enhances policy stability by preventing dramatic shifts in direction. The next parliamentary elections scheduled for September 2025 may produce changes in government composition, but the structural features of Norwegian politics ensure that any new coalition will operate within the established framework of fiscal prudence and long-term economic planning. Opinion polling suggests continued fragmentation across the political spectrum, with no single party positioned to command a majority, reinforcing the likelihood of coalition governance and centrist policy outcomes.

Political debate in Norway increasingly centres on the pace and nature of energy transition away from petroleum dependence, with tensions between environmental ambitions and the economic realities of continued hydrocarbon revenues. However, these discussions occur within parameters of broad agreement on climate commitments and the need for managed transition rather than abrupt disruption. The government's climate action plan targets 55% emissions reduction by 2030 relative to 1990 levels, whilst acknowledging that petroleum production will continue for decades as global demand persists. This pragmatic approach reflects political maturity in balancing competing priorities whilst maintaining the fiscal discipline that has characterised Norwegian economic management for over two decades.

Geopolitical Position and Security Considerations

Norway's geopolitical position has gained heightened significance following Russia's invasion of Ukraine in February 2022, transforming the country's role as Europe's most important energy supplier outside Russia. The proximity to Russian territory, including a 196-kilometre land border in the Arctic and extensive maritime boundaries, creates security considerations that have intensified amid deteriorating relations between Russia and Western nations. Norway's membership in NATO since its founding in 1949 provides collective security guarantees, whilst the country's substantial defence capabilities and strategic Arctic presence contribute meaningfully to Alliance deterrence posture in the High North.

The security environment has prompted increased defence spending and closer coordination with NATO allies, particularly the United States and United Kingdom, on Arctic security and energy infrastructure protection. Norway has committed to meeting NATO's 2% of GDP defence spending target, with budgets trending upward from historical levels around 1.5-1.7% of GDP. The government has prioritised modernisation of naval and air capabilities suited to Arctic operations, whilst enhancing surveillance and intelligence infrastructure to monitor Russian military activity in adjacent waters and airspace. These security investments, whilst representing fiscal costs, simultaneously reinforce Norway's strategic value to Western allies and strengthen its negotiating position on energy and economic matters.

Norway's energy supplier role has paradoxically strengthened its geopolitical position despite increased security risks, as European nations seek to reduce dependence on Russian hydrocarbons. Norwegian natural gas exports to Europe increased substantially following the Nord Stream pipeline sabotage in September 2022, with the country now supplying approximately 25-30% of European gas demand. This strategic importance provides Norway with enhanced political influence within European forums despite remaining outside the European Union, whilst generating substantial economic benefits through elevated energy prices and increased production volumes. The government has demonstrated willingness to leverage this position responsibly, increasing production where feasible whilst maintaining long-term resource management principles and avoiding opportunistic exploitation of European energy vulnerability.

The country's relationship with the European Union, characterised by membership in the European Economic Area whilst remaining outside the political union, reflects a carefully calibrated balance that commands broad domestic support. This arrangement provides access to the single market for goods, services, capital, and labour whilst preserving sovereignty over key sectors including fisheries, agriculture, and petroleum resources. The EEA framework has proven durable across multiple decades and changing governments, suggesting continued stability in Norway's European integration model despite periodic tensions over regulatory alignment and financial contributions to EU programmes.

Banking Sector & Financial Stability

Overview of the Norwegian banking system

The Norwegian banking system demonstrates exceptional resilience and stability, positioning it among the strongest financial sectors in Europe. As of the most recent assessment period, the banking sector maintains capital ratios approaching 19%, substantially above regulatory minimums and reflecting robust capitalisation that provides significant buffers against potential shocks. Non-performing loans remain remarkably low at below 1% of total loans, indicating strong asset quality and effective credit risk management across the sector. Profitability metrics are equally impressive, with return on equity reaching 17.5%, demonstrating the sector's ability to generate sustainable returns whilst maintaining prudent risk management practices.

The structural composition of Norway's banking sector reflects a well-diversified landscape combining large domestic institutions, regional savings banks, and branches of foreign banks. DNB Bank ASA, the country's largest financial institution, holds a dominant market position whilst smaller regional banks serve local communities and specialised market segments. This diversification contributes to financial system stability by preventing excessive concentration risk, though the largest institutions remain systemically important and subject to enhanced regulatory oversight and capital requirements.

Norwegian banks benefit from a supportive operating environment characterised by strong macroeconomic fundamentals, transparent regulatory frameworks, and a sophisticated financial infrastructure. The sector has successfully navigated recent periods of global financial stress, including the COVID-19 pandemic and subsequent inflationary pressures, without requiring government support or experiencing systemic distress. This track record reinforces confidence in the sector's resilience and the effectiveness of Norway's macroprudential policy framework.

Household debt and financial stability concerns

Despite the banking sector's overall strength, elevated household indebtedness represents the most significant financial stability concern facing Norwegian authorities. Household debt exceeds 200% of disposable income, ranking amongst the highest levels in developed economies and reflecting decades of sustained borrowing growth driven by rising property prices, low interest rates, and cultural preferences for homeownership. This concentration of debt in the household sector creates potential vulnerabilities should economic conditions deteriorate, unemployment rise, or interest rates increase substantially beyond current expectations.

The composition of household debt is heavily weighted toward mortgage lending, with residential property serving as collateral for the vast majority of household borrowing. Norwegian property prices have experienced sustained appreciation over multiple decades, supported by supply constraints in urban centres, population growth, and favourable financing conditions. Whilst this collateralisation provides banks with security against potential defaults, it also creates feedback mechanisms whereby property price corrections could amplify financial stress through wealth effects, reduced consumption, and increased loan impairments.

Norwegian authorities have implemented comprehensive macroprudential measures to address household debt vulnerabilities and strengthen borrower resilience. These measures include loan-to-value limits, debt-service-to-income requirements, and stress-testing obligations that require banks to assess borrowers' ability to service debt under adverse scenarios including interest rate increases. The effectiveness of these measures is evident in the banking sector's continued strong asset quality metrics, though the elevated debt stock remains a structural vulnerability requiring ongoing monitoring and potential policy adjustments.

The low unemployment environment and robust social safety nets provide important mitigating factors against household debt risks. Norway's unemployment rate remains amongst the lowest in Europe, supported by a flexible labour market, active employment policies, and strong economic fundamentals. The comprehensive welfare system, including unemployment insurance, housing support, and debt counselling services, provides households with buffers during periods of financial stress. These institutional strengths reduce the probability of widespread household defaults even during economic downturns, though they cannot entirely eliminate risks associated with the elevated debt burden.

Regulatory framework and supervision

Norway's financial regulatory framework adheres to international best practices and incorporates stringent capital, liquidity, and risk management requirements that exceed minimum Basel III standards. Finanstilsynet, the Norwegian Financial Supervisory Authority, maintains rigorous oversight of banks and other financial institutions through comprehensive on-site examinations, continuous off-site monitoring, and stress-testing exercises that assess resilience under adverse scenarios. The regulatory approach emphasises forward-looking risk assessment, early intervention when vulnerabilities emerge, and transparent communication with supervised institutions and the public.

The implementation of countercyclical capital buffers demonstrates Norway's proactive approach to macroprudential policy. Authorities adjust buffer requirements in response to evolving financial stability risks, requiring banks to build additional capital during periods of credit expansion and potentially releasing buffers during downturns to support lending capacity. This dynamic framework enhances the banking sector's ability to absorb shocks whilst maintaining credit provision to the real economy, contributing to both financial stability and macroeconomic resilience.

Norwegian banks are subject to comprehensive liquidity requirements including the Liquidity Coverage Ratio and Net Stable Funding Ratio, ensuring institutions maintain sufficient high-quality liquid assets to withstand funding stress and structural liquidity mismatches. The banking sector's strong deposit base, dominated by stable retail and corporate deposits, provides a solid funding foundation that reduces reliance on wholesale funding markets. This funding structure enhances resilience against potential market disruptions and reduces vulnerability to external funding shocks.

Financial sector resilience and risk assessment

Stress-testing exercises conducted by Norges Bank and Finanstilsynet consistently demonstrate the Norwegian banking sector's capacity to withstand severe adverse scenarios including sharp property price corrections, significant increases in unemployment, and substantial interest rate rises. These assessments indicate that even under tail-risk scenarios, the banking system would maintain capital ratios above regulatory minimums, though profitability would deteriorate and credit losses would increase materially. The results reinforce confidence in systemic resilience whilst highlighting the importance of maintaining robust capital buffers and prudent risk management practices.

The banking sector's exposure to the petroleum sector represents a concentrated risk given the industry's importance to the Norwegian economy and its vulnerability to oil price volatility and energy transition dynamics. Norwegian banks have developed sophisticated expertise in petroleum lending and maintain conservative underwriting standards for this sector, though a severe and sustained downturn in oil and gas activity would inevitably impact asset quality and profitability. Diversification efforts by both banks and the broader economy aim to reduce this concentration over time, though the petroleum sector will remain systemically important for the foreseeable future.

Operational risks including cybersecurity threats have gained prominence as Norwegian banks increasingly digitalise their operations and customer interfaces. The sector has invested substantially in information technology infrastructure, security systems, and incident response capabilities to address these evolving threats. Regulatory authorities maintain heightened focus on operational resilience, requiring banks to demonstrate robust business continuity arrangements, third-party risk management, and cyber defence capabilities. Whilst no major incidents have compromised systemic stability, the dynamic nature of cyber threats requires continuous vigilance and investment.

The Norwegian banking sector's strong performance metrics, robust regulatory framework, and demonstrated resilience through multiple stress episodes support the assessment that financial stability risks are well-managed despite the structural vulnerability posed by elevated household debt. The combination of high capital ratios, strong asset quality, prudent supervision, and comprehensive macroprudential policies provides multiple layers of defence against potential shocks. This financial sector strength reinforces Norway's exceptional sovereign credit profile and contributes to the stable outlooks maintained by all major rating agencies.

Outlook & Scenarios

Short-Term Outlook (12 months)

Norway's near-term economic trajectory through 2026 reflects a gradual normalisation following the exceptional petroleum revenue windfall of 2022-2023, with mainland GDP growth expected to stabilise around 1.5% as the economy transitions from elevated energy prices to more sustainable fundamentals. The monetary policy cycle has entered an easing phase, with Norges Bank implementing measured rate reductions from the 4.5% peak towards 4.0% as inflation converges towards the 2% target, providing modest support to household consumption and business investment whilst maintaining vigilance against financial stability risks associated with elevated household indebtedness exceeding 200% of disposable income. The labour market demonstrates continued resilience with unemployment remaining below 4%, though wage growth moderation and productivity constraints continue to weigh on competitiveness in the non-petroleum tradeable sector.

Fiscal policy maintains an expansionary stance supported by record petroleum revenues and the Government Pension Fund Global's robust performance, with the sovereign wealth fund's value approaching NOK 20 trillion providing unparalleled capacity to absorb economic shocks whilst adhering to the fiscal rule framework that limits structural non-oil deficits to approximately 3% of fund assets. The external position remains exceptionally strong with current account surpluses projected to persist in the 15-17% of GDP range, driven by sustained energy exports to European markets seeking alternatives to Russian supply, though volumes face gradual decline as North Sea fields mature. The banking sector's exceptional capitalisation near 19% and minimal non-performing loans below 1% position financial institutions to maintain credit provision through any near-term volatility, whilst housing market dynamics warrant continued monitoring given elevated household leverage ratios.

Geopolitical considerations stemming from regional tensions and Norway's enhanced strategic importance as Europe's primary energy supplier create both opportunities and risks, with sustained demand for Norwegian hydrocarbons supporting fiscal revenues whilst simultaneously exposing the economy to potential supply disruptions or security concerns. The short-term outlook remains firmly anchored by the sovereign's unmatched fiscal buffers and institutional strength, with rating stability assured barring extraordinary external shocks that would likely affect multiple highly-rated sovereigns simultaneously.

Medium-Term Outlook (1-3 years)

The medium-term horizon through 2028-2029 presents a more complex landscape as Norway navigates structural transitions in the global energy system whilst confronting domestic demographic and productivity challenges that will increasingly constrain potential growth. Mainland GDP growth is projected to converge towards 1.5-2.0% annually, reflecting the economy's mature development stage and persistent productivity growth stagnation at 0.6-0.8%—substantially below historical averages and peer country performance—which fundamentally limits competitiveness gains outside the petroleum sector. The energy transition trajectory poses mounting strategic questions for an economy deriving approximately 62% of goods exports and 24% of GDP from hydrocarbons, as accelerating global decarbonisation efforts and renewable energy deployment gradually erode long-term demand for fossil fuels, though the timeline remains sufficiently extended to permit orderly adjustment supported by the GPFG's diversification.

Demographic pressures will intensify as population ageing accelerates, with the old-age dependency ratio rising and placing increasing demands on healthcare and pension systems, though Norway's exceptional fiscal position provides multi-generational capacity to absorb these costs without threatening debt sustainability. The Government Pension Fund Global is projected to exceed 500% of current account payments through 2028, with continued prudent management and diversified global equity and fixed income holdings generating average annual returns near 6% since inception, ensuring the fund's real value preservation despite gradual increases in fiscal withdrawals to support mainland economic activity. Monetary policy is expected to normalise towards neutral rates in the 3.0-3.5% range as inflation stabilises durably at target, though the policy stance will remain sensitive to household debt dynamics and housing market developments that represent the primary domestic financial stability concern.

The banking sector's robust capitalisation and profitability metrics position institutions to support economic diversification efforts and maintain credit provision through the structural transition, whilst regulatory frameworks and macroprudential tools provide authorities with instruments to address emerging vulnerabilities. Norway's external position will remain exceptionally strong despite gradual petroleum production declines, with the massive net international investment position and sovereign wealth fund returns generating substantial investment income flows that increasingly supplement trade surpluses. The medium-term outlook remains fundamentally supportive of the AAA/Aaa rating, contingent upon continued adherence to the fiscal rule framework, successful navigation of energy transition challenges, and maintenance of the institutional quality and governance standards that distinguish Norway amongst global sovereigns.

Rating Scenarios

Norway's AAA/Aaa rating with stable outlook reflects an exceptionally high threshold for downward pressure given the sovereign's unparalleled fiscal buffers and institutional strengths, with rating agencies consistently emphasising that vulnerabilities are substantially mitigated by the Government Pension Fund Global's scale and the policy framework's credibility. An upgrade scenario is precluded by Norway's position at the highest possible rating level, though the stable outlook could theoretically shift to positive if the sovereign demonstrated materially accelerated economic diversification away from petroleum dependence whilst simultaneously achieving sustained productivity growth improvements that fundamentally enhanced long-term competitiveness—outcomes that appear unlikely within the foreseeable rating horizon given structural constraints and the mature economy's characteristics.

Downgrade scenarios, whilst remote in probability, would require a confluence of adverse developments that materially eroded Norway's core credit strengths across multiple dimensions simultaneously. A negative outlook could emerge if fiscal policy discipline deteriorated significantly through sustained breaches of the fiscal rule framework, with structural non-oil deficits persistently exceeding 3% of GPFG assets without offsetting revenue measures or expenditure restraint, particularly if accompanied by imprudent sovereign wealth fund management that generated sustained negative real returns or inappropriate risk-taking that threatened capital preservation. A precipitous and permanent collapse in petroleum revenues substantially exceeding current baseline decline projections—whether through accelerated energy transition dynamics, major technological disruptions rendering hydrocarbon assets stranded, or geopolitical developments severing European energy markets—could pressure the rating if economic diversification efforts proved insufficient to offset the sectoral contraction.

Severe financial stability events stemming from disorderly housing market corrections combined with household debt distress that overwhelmed banking sector capital buffers and required substantial public sector intervention would represent a material credit negative, particularly if coinciding with broader economic recession that strained fiscal resources. Institutional deterioration through governance failures, corruption scandals, or political instability that undermined policy credibility and transparency—outcomes that appear highly improbable given Norway's consistent top-tier rankings in global governance assessments—would fundamentally challenge the rating's foundations. Geopolitical shocks including direct military conflict affecting Norwegian territory or critical energy infrastructure, whilst currently assessed as low probability, could trigger rating pressure through economic disruption and fiscal demands, though Norway's NATO membership and strategic importance provide substantial security assurances.

The rating agencies' consistent messaging emphasises that Norway's vulnerabilities would need to intensify dramatically and simultaneously across petroleum dependence, household debt, and productivity dimensions whilst the sovereign wealth fund's buffering capacity diminished materially before downgrade consideration became warranted. The stable outlook reflects the assessment that Norway's exceptional fiscal flexibility, institutional quality, and policy framework credibility provide substantial resilience against foreseeable adverse scenarios, with the GPFG representing approximately 380% of GDP ensuring multi-generational capacity to absorb shocks and manage structural transitions whilst preserving debt sustainability and macroeconomic stability that underpin the AAA/Aaa rating.

Conclusion

Norway's AAA/Aaa credit ratings with stable outlooks reflect a sovereign credit profile of exceptional strength, distinguished by fiscal and external positions that are unparalleled among rated sovereigns globally. The Government Pension Fund Global, valued at NOK 19,742 billion and representing approximately 380% of GDP, provides multi-generational fiscal flexibility that fundamentally differentiates Norway's creditworthiness from all other highly-rated peers. This extraordinary buffer capacity, combined with GDP per capita approaching $87,000, robust democratic institutions ranked amongst the world's finest, and a banking system demonstrating capital ratios near 19% with non-performing loans below 1%, establishes a credit foundation of remarkable resilience. The sovereign's net external creditor position, supported by persistent current account surpluses averaging 15-17% of GDP, further reinforces this assessment of exceptional financial strength.

Nevertheless, Norway's credit profile incorporates structural vulnerabilities that warrant careful monitoring, even as they remain substantially mitigated by the sovereign's formidable fiscal resources. The petroleum sector's dominance—accounting for approximately 62% of goods exports and 24% of GDP—creates meaningful exposure to hydrocarbon price volatility and long-term energy transition risks as global decarbonisation accelerates. Household indebtedness exceeding 200% of disposable income represents a persistent financial stability concern, whilst productivity growth stagnation at 0.6-0.8% annually constrains potential economic expansion and competitiveness relative to historical performance. Demographic pressures from an ageing population will intensify fiscal demands in coming decades, and geopolitical proximity to Russia introduces security considerations, though this has paradoxically enhanced Norway's strategic importance as Europe's largest energy supplier after Russia.

The near-term economic outlook demonstrates resilience amid global uncertainty, with mainland GDP growth forecast at 1.5% in 2025 and inflation trajectory declining towards the 2% target by 2027, enabling Norges Bank to pursue gradual policy normalisation through rate reductions from 4.5% to 4.0%. The expansionary fiscal stance, underpinned by record petroleum revenues and prudent sovereign wealth fund management adhering to the established fiscal rule, positions Norway to absorb near-term economic shocks whilst pursuing gradual diversification away from hydrocarbon dependence. The unanimous affirmation of top-tier ratings by all three major agencies reflects the assessment that Norway's structural challenges, whilst material, are comprehensively offset by unparalleled fiscal flexibility, exceptional institutional quality, and the sovereign wealth fund's capacity to provide economic security across multiple generations. This combination of extraordinary strengths and well-managed vulnerabilities supports Norway's position amongst the world's most creditworthy sovereigns.