Kazakhstan

Executive Summary

Kazakhstan's Baa1/BBB/BBB- investment-grade sovereign credit profile reflects a distinctive combination of substantial fiscal buffers and persistent structural vulnerabilities characteristic of hydrocarbon-dependent emerging markets. The sovereign benefits from exceptionally strong balance sheet fundamentals, with the National Fund of Kazakhstan and foreign exchange reserves collectively exceeding 50% of GDP and public debt maintained at a conservative 23.7% of GDP as of 2024. These substantial sovereign assets provide meaningful shock-absorption capacity against external volatility, whilst the country's strategic geographic position between China, Russia, and Europe offers diversification opportunities for trade and investment flows. However, the credit profile remains constrained by pronounced hydrocarbon dependency—with oil accounting for approximately 20% of GDP and over 50% of exports—alongside institutional weaknesses, export route concentration through Russia, and elevated inflation that has persistently exceeded the central bank's 5% target, reaching 8.6% in 2024.

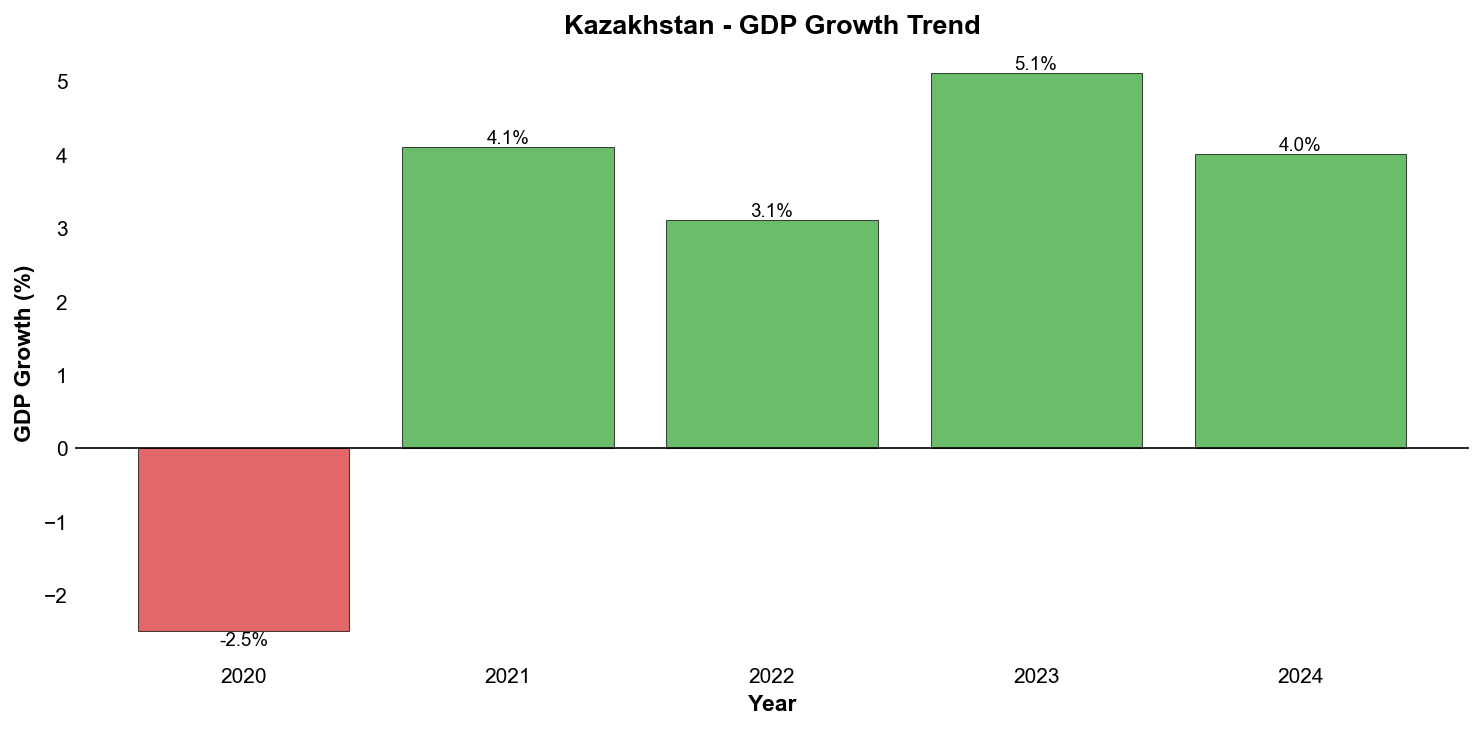

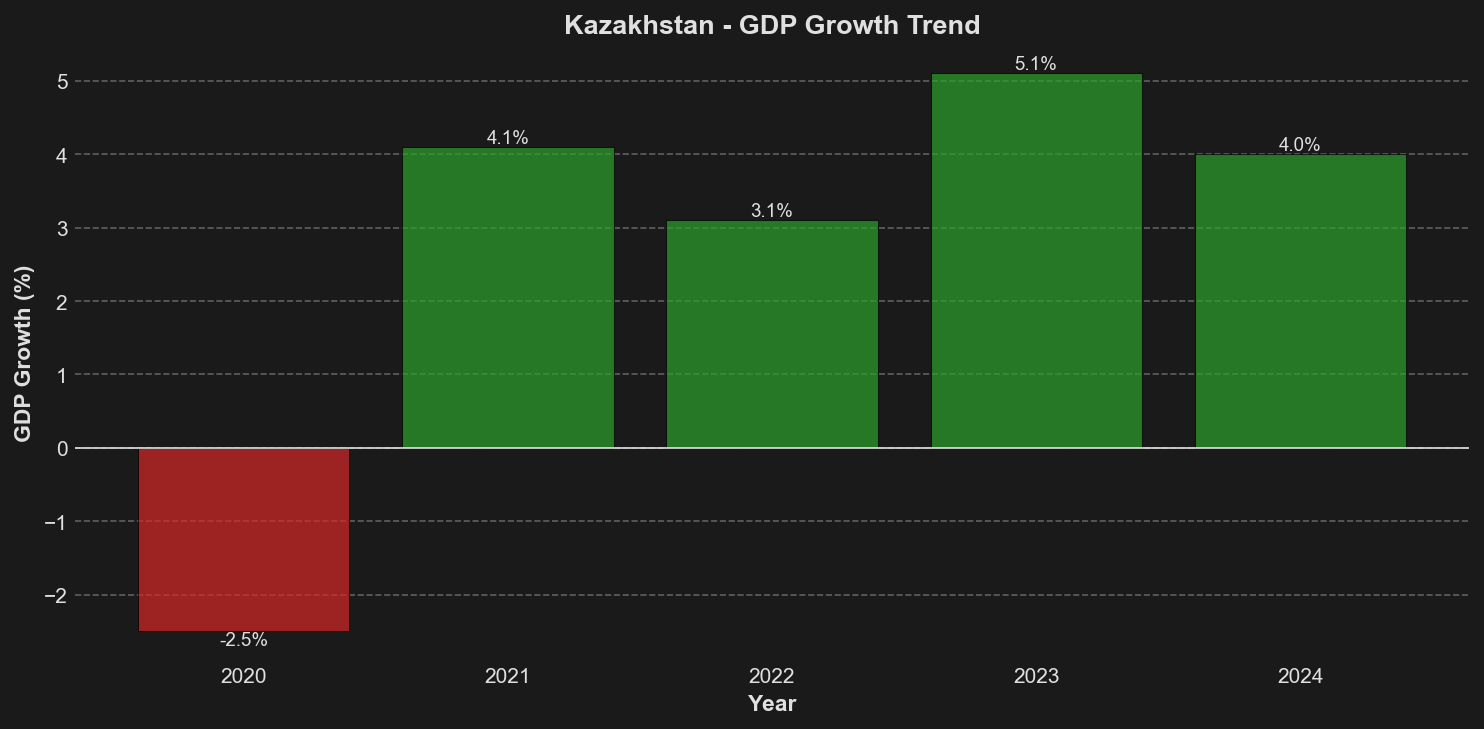

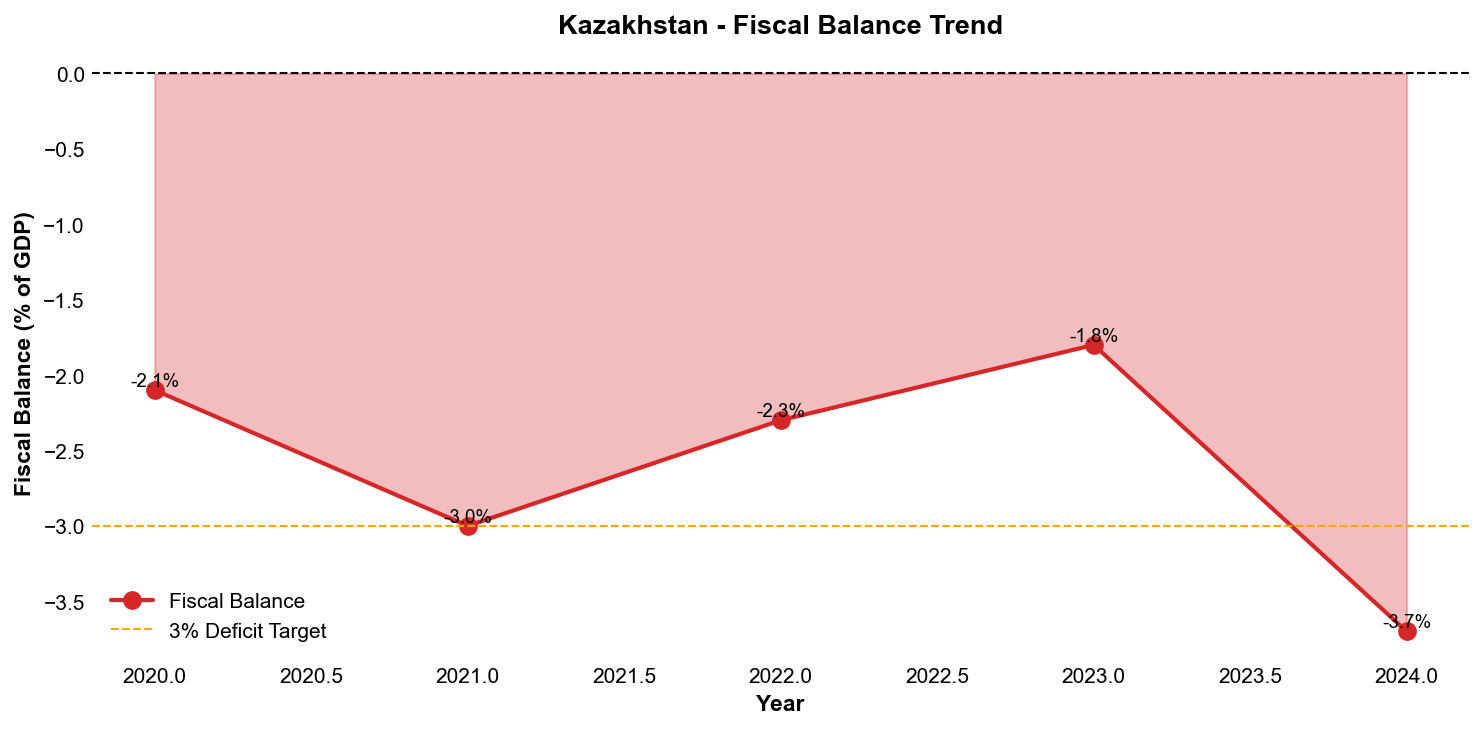

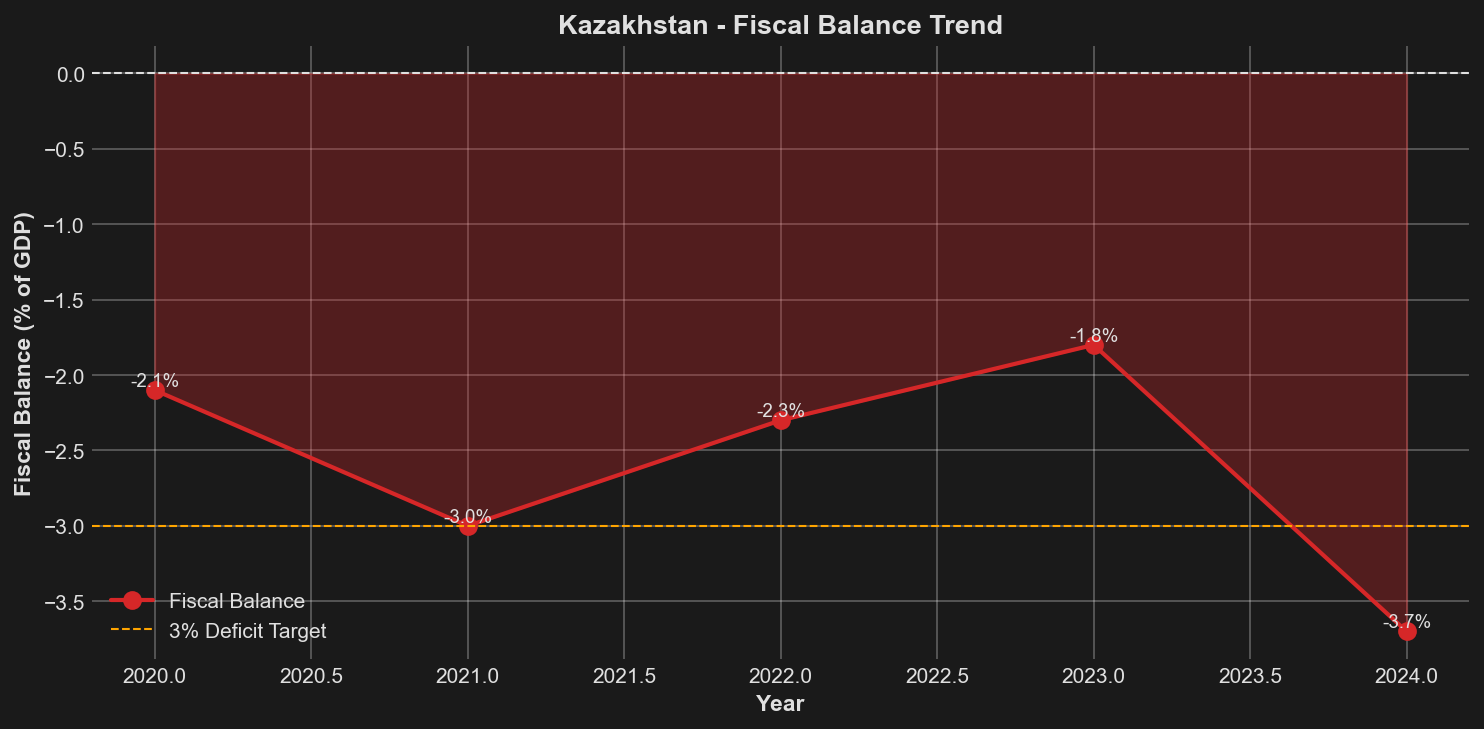

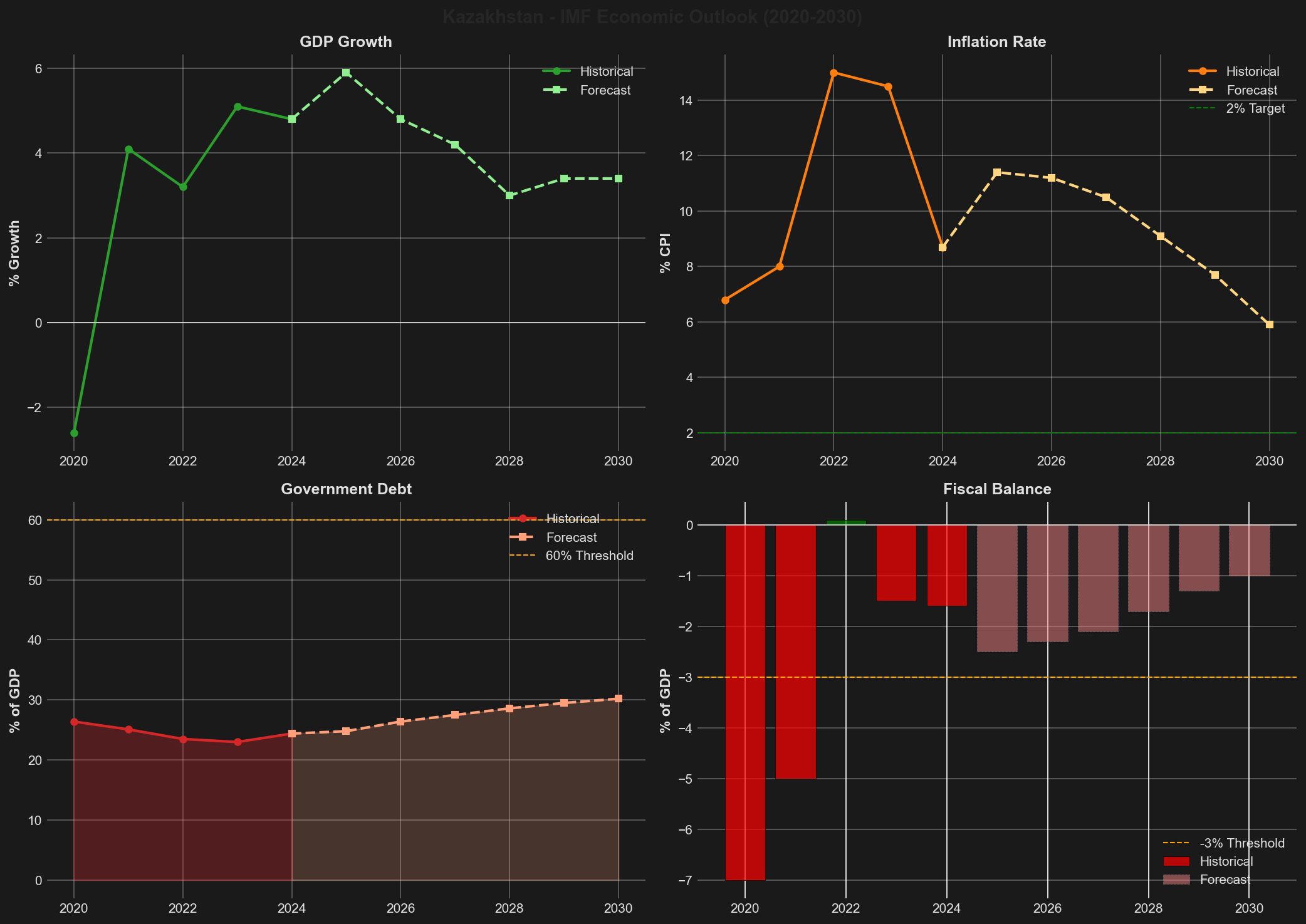

The Kazakhstani economy has demonstrated resilience in recent years, rebounding from a 2.5% contraction in 2020 to achieve 5.1% growth in 2023, before moderating to 4.0% in 2024. Growth prospects for 2025 remain constructive at 4-5%, supported by the anticipated Tengiz oilfield expansion which should bolster hydrocarbon production and export revenues. Foreign direct investment surged to a post-Soviet record of $15.7 billion in 2024, representing an 88% year-on-year increase, though extractive industries remain the primary destination. The fiscal position has shown some deterioration, with the deficit widening to 3.7% of GDP in 2024 due to expansionary fiscal policy and infrastructure investments, whilst the current account has fluctuated in line with global oil price movements. Foreign exchange reserves strengthened notably to $45.8 billion in 2024, providing approximately seven months of import coverage and reinforcing external resilience.

The sovereign faces several medium-term challenges that will influence its credit trajectory. Persistent inflationary pressures, stemming from both domestic demand dynamics and external spillovers, complicate monetary policy management and erode real incomes. The concentration of export routes through Russia creates geopolitical vulnerability, particularly relevant given regional tensions and Western sanctions regimes. The global energy transition poses a structural threat to the hydrocarbon-dependent economic model, necessitating accelerated diversification efforts. President Tokayev has consolidated political authority since 2022 and introduced governance reforms; however, implementation remains limited, creating uncertainty regarding the pace and depth of institutional strengthening.

The stable outlook across all three major rating agencies reflects a balanced assessment of Kazakhstan's credit fundamentals. Upside potential exists should the authorities successfully implement structural reforms to reduce hydrocarbon dependency, strengthen institutional frameworks, and diversify the economic base beyond extractive industries. Conversely, downside risks include sustained low oil prices, escalation of geopolitical tensions affecting export routes, failure to contain inflation within target ranges, or fiscal deterioration stemming from undisciplined National Fund withdrawals. The banking sector's strong capitalisation and liquidity provide additional systemic stability, though credit growth dynamics warrant continued monitoring. Kazakhstan's rating trajectory will ultimately depend on the authorities' ability to translate ambitious diversification initiatives into tangible structural transformation whilst maintaining the fiscal discipline that has characterised sovereign debt management to date.

Ratings Summary

Kazakhstan maintains investment-grade ratings from all three major credit rating agencies, with Moody's positioning the sovereign at Baa1, S&P at BBB-, and Fitch at BBB, all carrying stable outlooks. Moody's upgraded Kazakhstan to Baa1 in September 2024, citing improved governance frameworks and progress on economic diversification initiatives. The stable outlooks across agencies reflect a balanced assessment of credit fundamentals, wherein substantial sovereign wealth assets and low public indebtedness provide robust buffers against external shocks, whilst hydrocarbon dependency and institutional weaknesses constrain the ratings. Rating agencies consistently emphasise Kazakhstan's considerable sovereign wealth assets, comprising approximately $60 billion in the National Fund alongside foreign exchange reserves, and a low public debt burden of 23.7% of GDP as principal credit strengths. Conversely, key rating constraints include the economy's structural dependence on hydrocarbons, with oil accounting for 20% of GDP and exceeding 50% of exports, creating vulnerability to commodity price volatility. Additional concerns centre on export route concentration through Russia, persistent inflation running above the central bank's 5% target at 8.6% in 2024, and the widening fiscal deficit to 4.3% of GDP. Fitch has specifically highlighted concerns regarding the absence of formal limits on National Fund transfers, which could potentially erode fiscal buffers over time.

| Rating Agency | Current Rating | Outlook | Last Action Date |

|---|---|---|---|

| S&P | BBB- | Stable | 21 February 2024 |

| Moody's | Baa1 | Stable | 9 September 2024 |

| Fitch | BBB | Stable | 17 May 2024 |

Economic Indicators

| Indicator | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

| GDP Growth (annual %) | -2.5% | 4.1% | 3.1% | 5.1% | 4.0%* |

| Inflation Rate (%) | 6.7% | 8.0% | 14.7% | 9.8% | 8.6% |

| Debt-to-GDP Ratio (%) | 23.7% | 22.4% | 24.4% | 21.7% | 23.7%* |

| Fiscal Balance (% of GDP) | -2.1% | -3.0% | -2.3% | -1.8% | -3.7%* |

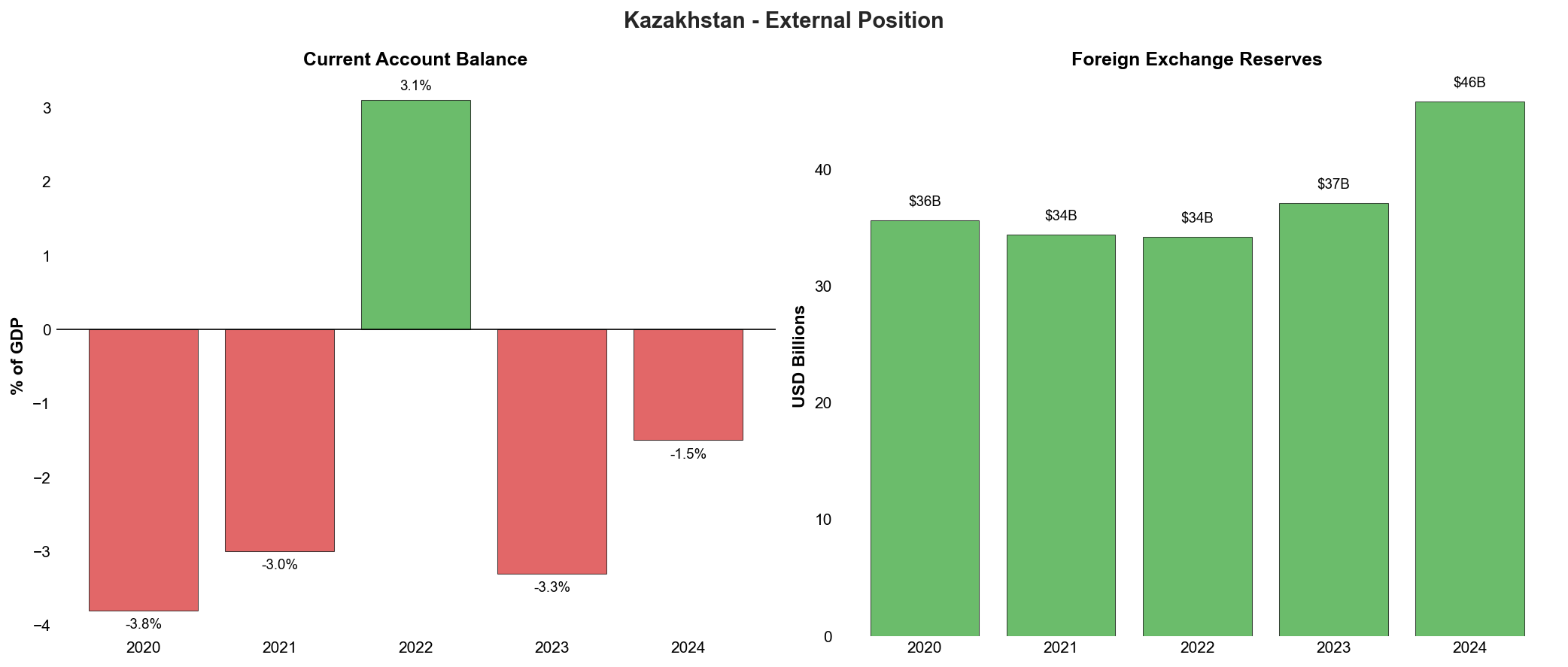

| Current Account Balance (% of GDP) | -3.8% | -3.0% | 3.1% | -3.3% | -1.5%* |

| Foreign Exchange Reserves (USD billions) | 35.6 | 34.4 | 34.2 | 37.1 | 45.8* |

| Oil Production (million barrels per day) | 1.47 | 1.55 | 1.77 | 1.57 | 1.75* |

| Unemployment Rate (%) | 4.9% | 5.6% | 4.9% | 4.8% | 4.6% |

| FDI (USD billions) | 7.2 | 4.6 | 6.1 | 8.4 | 15.7* |

*Note: 2024 figures include actual data and projections/estimates for the full year

Kazakhstan's economy has demonstrated considerable resilience following the sharp 2.5% contraction in 2020 precipitated by the COVID-19 pandemic and associated disruptions to global commodity markets. Growth rebounded robustly to 4.1% in 2021 and maintained positive momentum through subsequent years, accelerating to 5.1% in 2023 before moderating to 4.0% in 2024. This growth trajectory reflects the economy's continued dependence on hydrocarbon extraction, with oil production recovering to 1.75 million barrels per day in 2024, approaching the elevated levels achieved in 2022. The Tengiz oilfield expansion project, which commenced production increases in 2024, is expected to support medium-term growth prospects, with IMF forecasts projecting GDP growth of 3.4% by 2030 as the economy matures and hydrocarbon production plateaus.

Persistent inflation remains a significant macroeconomic challenge and a key constraint on Kazakhstan's sovereign credit profile. Consumer price inflation peaked at 14.7% in 2022, driven by global supply chain disruptions, elevated commodity prices, and substantial spillover effects from Russia's invasion of Ukraine, including currency depreciation pressures and trade disruptions. Whilst inflation has moderated to 8.6% in 2024, it remains well above the National Bank of Kazakhstan's 5% target corridor, reflecting structural price pressures in food and utilities, currency pass-through effects, and accommodative fiscal policy. The IMF projects inflation to decline gradually to 5.9% by 2030, contingent upon continued monetary policy tightening and reduced fiscal stimulus, though this trajectory faces risks from external shocks and domestic wage pressures.

The fiscal position has exhibited notable fluctuations over the review period, with the deficit widening to 3.7% of GDP in 2024 due to expansionary fiscal policy measures, increased infrastructure investments, and social spending commitments following the political unrest in January 2022. This represents a deterioration from the relatively contained deficit of 1.8% in 2023 and contrasts with the government's stated consolidation objectives. Despite these recurring deficits, Kazakhstan maintains a remarkably low debt-to-GDP ratio of 23.7% in 2024, providing substantial fiscal headroom relative to investment-grade peers. The IMF forecasts a gradual fiscal consolidation to a deficit of 1.0% of GDP by 2030, supported by revenue measures and expenditure restraint, though implementation risks remain considerable given political pressures for continued social spending. The government's fiscal position is further buttressed by the National Fund of Kazakhstan, which held approximately $60 billion in assets as of 2024, though rating agencies have expressed concerns regarding the absence of formal limits on transfers from the Fund to the budget.

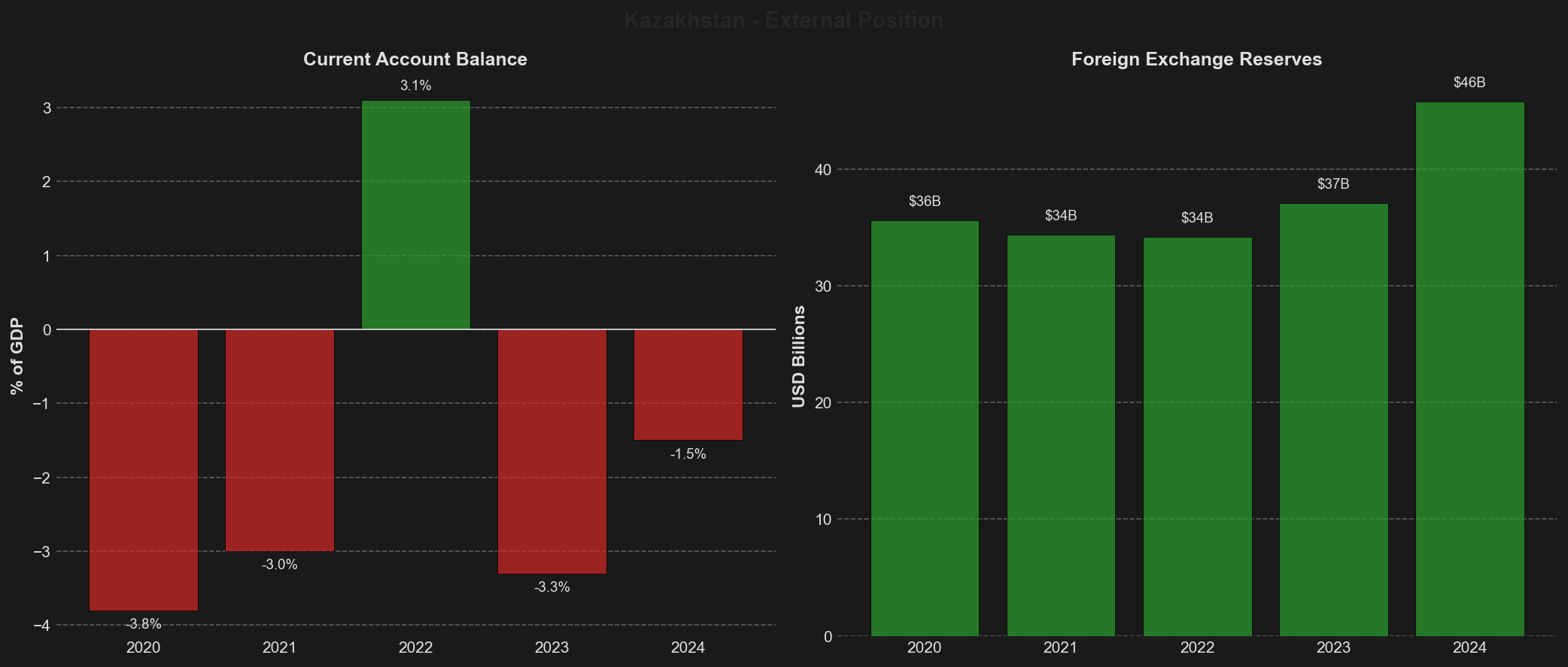

The external position presents a mixed picture, with the current account balance fluctuating between deficit and surplus primarily in response to oil price movements and production volumes. The notable surplus of 3.1% of GDP in 2022 reflected elevated hydrocarbon prices during the initial phase of the Russia-Ukraine conflict, whilst the return to deficit in 2023 and 2024 reflected normalising commodity prices and robust import growth driven by infrastructure investment and consumer demand. The IMF projects a substantial widening of the current account deficit to 11.3% of GDP by 2030, reflecting declining hydrocarbon revenues as global energy transition accelerates, increased profit repatriation by foreign investors in the extractive sector, and sustained import demand. This deteriorating external position represents a medium-term credit concern, particularly given Kazakhstan's already weak net foreign asset position of negative 33.3% of GDP in 2023, which has improved from negative 56.9% in 2020 but remains in the "Weak" category, indicating notable external liabilities and vulnerability to capital flow reversals.

Foreign exchange reserves increased substantially to $45.8 billion in 2024, representing approximately seven months of import coverage and providing a meaningful buffer against external shocks. This reserve accumulation reflects central bank intervention to manage tenge volatility, current account surpluses in 2022, and National Fund transfers. Combined with the National Fund's assets, Kazakhstan's total sovereign liquid assets exceed 50% of GDP, representing a key rating strength and providing substantial capacity to manage external financing pressures. Foreign direct investment surged to a post-Soviet record of $15.7 billion in 2024, representing an 88% year-on-year increase, though extractive industries remain the primary destination, underscoring the ongoing challenge of economic diversification. The unemployment rate has remained relatively stable at 4.6% in 2024, though this figure likely understates labour market slack given substantial informal employment and underemployment in rural areas.

Net Foreign Assets & External Position

Kazakhstan's external position reflects a persistent structural imbalance characteristic of resource-rich emerging markets with substantial foreign investment in extractive industries. The sovereign's net international investment position (NIIP) stood at -33.3% of GDP in 2023, representing a weak debtor position with notable external liabilities, though demonstrating meaningful improvement from the -56.9% trough recorded in 2020. This negative NIIP primarily reflects accumulated foreign direct investment in the hydrocarbon sector rather than excessive external borrowing, with the composition weighted towards equity liabilities rather than debt instruments. The external position assessment carries a three-star rating on a seven-point scale, positioning Kazakhstan in the "weak" category but showing a constructive trajectory of gradual strengthening over the medium term.

The five-year trend in Kazakhstan's net foreign assets reveals a notable improvement trajectory following the pandemic-induced deterioration. The NIIP weakened sharply from -46.7% of GDP in 2019 to -56.9% in 2020 as the denominator effect of GDP contraction and currency depreciation amplified the negative position. Subsequently, the external balance has strengthened consistently, improving to -51.7% in 2021, -39.2% in 2022, and -33.3% in 2023. This 23.6 percentage point improvement since the 2020 nadir reflects multiple factors: robust GDP growth averaging 4.1% over the recovery period, elevated commodity prices supporting current account dynamics, and substantial foreign exchange reserve accumulation. The progression from a "very weak" two-star rating in 2020-2021 to a "weak" three-star assessment in 2022-2023 indicates meaningful progress, though Kazakhstan remains a net external debtor requiring continued vigilance.

Reserve Adequacy and External Buffers

Kazakhstan maintains substantial external buffers that significantly mitigate vulnerabilities associated with its negative NIIP. Foreign exchange reserves reached $45.8 billion in 2024, representing approximately seven months of import coverage and providing a robust first line of defence against external shocks. When combined with the National Fund of Kazakhstan's assets of approximately $60 billion, total sovereign liquid external assets exceed 50% of GDP, creating an exceptional buffer relative to most emerging market peers. This substantial reserve position more than offsets the negative NIIP from a liquidity perspective, though the structural debtor position remains a rating constraint. The central bank has demonstrated prudent reserve management, with holdings increasing by $8.7 billion between 2023 and 2024 despite periodic interventions to manage tenge volatility during periods of regional stress.

Current Account Dynamics and Sustainability

The current account balance has exhibited considerable volatility, fluctuating between a 3.1% of GDP surplus in 2022 during peak oil prices and deficits of 3.8% in 2020 and 3.3% in 2023. The deficit narrowed to an estimated 1.5% of GDP in 2024, reflecting improved terms of trade and the commencement of production from the expanded Tengiz oilfield. However, IMF projections indicate a substantial widening of the current account deficit to 11.3% of GDP by 2030, raising medium-term sustainability concerns. This projected deterioration reflects multiple factors: declining oil production from mature fields absent major new developments, increasing profit repatriation by foreign investors in the hydrocarbon sector, and rising import demand driven by infrastructure investment and consumption growth. The composition of the current account reveals structural vulnerabilities, with the income balance persistently negative due to profit remittances from foreign-owned extractive operations, whilst the services balance remains in deficit.

External Debt Profile and Vulnerabilities

Kazakhstan's external debt position remains manageable despite the negative NIIP, with government external debt comprising a modest portion of the 23.7% debt-to-GDP ratio. The external debt stock is predominantly denominated in foreign currency, creating exchange rate sensitivity, though the substantial reserve buffers provide considerable protection. Private sector external debt, concentrated in the banking and hydrocarbon sectors, warrants monitoring but remains serviceable given corporate cash flows and banking sector capitalisation. The maturity profile of external obligations is relatively favourable, with limited near-term refinancing concentrations, though the sovereign maintains regular access to international capital markets. External financing requirements remain modest relative to reserve holdings, with debt service obligations comfortably covered by export receipts and reserve assets.

Structural Vulnerabilities and Geopolitical Considerations

The external position faces structural vulnerabilities beyond the headline NIIP metric. Export route concentration through Russia creates significant geopolitical risk, with the majority of oil exports transiting Russian territory via the Caspian Pipeline Consortium. Sanctions risks and potential transit disruptions represent material external vulnerabilities not fully captured in traditional balance of payments metrics. The hydrocarbon dependency, with oil accounting for over 50% of exports, creates substantial terms of trade sensitivity and exposes the external position to global energy transition risks over the longer term. Currency risk remains elevated despite the flexible exchange rate regime, with periodic tenge depreciation episodes reflecting regional spillovers and commodity price movements. The projected widening of the current account deficit to double-digit percentages by 2030 raises questions about external sustainability absent successful economic diversification, though the substantial sovereign asset base provides considerable time to address structural imbalances. The banking sector's external funding position remains stable, with foreign currency liquidity adequate and cross-border exposures manageable, supporting overall external resilience despite the negative NIIP.

Credit Strengths & Vulnerabilities

Strengths

Kazakhstan's sovereign credit profile is underpinned by exceptionally strong fiscal buffers that distinguish it from regional peers. The National Fund of Kazakhstan holds approximately $60 billion in assets, complemented by foreign exchange reserves of $45.8 billion as of 2024, collectively representing more than 50% of GDP. This substantial sovereign wealth provides a critical cushion against external shocks and commodity price volatility. The government's debt position remains remarkably conservative, with public debt at just 23.7% of GDP—well below most investment-grade sovereigns—affording considerable fiscal flexibility for countercyclical policy responses.

The economy demonstrates resilience through diversified commodity exports and strategic geographic positioning. Whilst hydrocarbon dependency remains significant, Kazakhstan has developed substantial mineral resources including uranium, copper, and chromium, reducing reliance on oil price movements alone. The nation's location at the crossroads of China, Russia, and Europe positions it as a natural transit corridor for trade flows, particularly as China's Belt and Road Initiative expands westward connectivity. The banking sector exhibits robust fundamentals with strong capitalisation ratios and adequate liquidity buffers, having weathered previous commodity cycles without systemic stress.

Foreign direct investment reached a post-Soviet record of $15.7 billion in 2024, representing an 88% year-on-year increase that signals growing international confidence. The Tengiz oilfield expansion project, one of the world's largest oil developments, is expected to boost production capacity significantly and support 4-5% GDP growth through 2025. Unemployment remains relatively contained at 4.6%, whilst the government has maintained macroeconomic stability despite regional turbulence from Russia's invasion of Ukraine and subsequent sanctions regimes.

Vulnerabilities

Hydrocarbon dependency constitutes the most significant structural weakness in Kazakhstan's credit profile. Oil accounts for approximately 20% of GDP and over 50% of export revenues, creating acute vulnerability to global energy price fluctuations and long-term demand uncertainty. This concentration risk extends beyond direct fiscal impacts to affect employment, investment flows, and broader economic activity. The government's budget remains heavily reliant on oil revenues, with the fiscal deficit widening to 3.7% of GDP in 2024 partly reflecting lower-than-anticipated commodity receipts.

Persistent inflation represents a chronic macroeconomic challenge that constrains policy flexibility. Consumer price growth peaked at 14.7% in 2022 following global supply chain disruptions and spillover effects from the Ukraine conflict, but remained elevated at 8.6% in 2024—substantially above the central bank's 5% target. This persistent price pressure reflects structural factors including limited domestic competition, supply chain inefficiencies, and exchange rate pass-through effects. The National Bank of Kazakhstan faces difficult trade-offs between supporting growth and anchoring inflation expectations, particularly given external pressures on the tenge.

Export route concentration through Russia creates significant geopolitical risk. The majority of Kazakhstan's oil exports transit Russian territory via the Caspian Pipeline Consortium, whilst rail and road connections to European markets similarly depend on Russian infrastructure. Western sanctions on Russia have complicated payment systems and logistics, whilst the risk of transit disruptions—whether from technical issues, political tensions, or deliberate interference—represents a material vulnerability. Alternative routes through the Caspian Sea and China face capacity constraints and higher costs.

Institutional weaknesses persist despite recent reform initiatives. Governance indicators remain below investment-grade medians, with concerns regarding rule of law, regulatory predictability, and corruption. President Tokayev's consolidation of power since 2022 and announced governance reforms have yet to translate into substantial institutional strengthening. The lack of formal limits on National Fund transfers, as highlighted by Fitch, raises concerns about fiscal discipline and the potential for politically motivated drawdowns. Implementation capacity for structural reforms remains limited, whilst vested interests often resist changes that threaten established rent-seeking arrangements.

Opportunities

Economic diversification initiatives present pathways to reduce hydrocarbon dependency over the medium term. The government has prioritised development of non-oil sectors including agriculture, logistics, tourism, and manufacturing through targeted incentives and infrastructure investments. Kazakhstan's substantial renewable energy potential—particularly wind and solar resources—offers opportunities to develop green hydrogen production and position the country as a clean energy exporter as global markets transition. The Astana International Financial Centre aims to establish Kazakhstan as a regional financial hub, attracting capital flows and expertise.

Geopolitical realignment creates potential trade and investment opportunities. Western companies seeking to reduce exposure to Russia and China have identified Kazakhstan as an alternative destination for investment and sourcing. The Middle Corridor transport route connecting China to Europe via the Caspian Sea and Caucasus has gained prominence as businesses diversify away from Russian transit routes, with Kazakhstan positioned as a key node. Strengthening ties with the European Union, including the recently enhanced Partnership and Cooperation Agreement, could facilitate technology transfer and market access.

Demographic advantages support long-term growth potential. Kazakhstan's population of approximately 20 million is relatively young compared to regional peers, with a median age below 30 years providing a growing labour force. Educational investments and digital infrastructure development could enhance human capital quality, whilst urbanisation trends support productivity gains. The government's emphasis on attracting the Kazakh diaspora and skilled migrants could further strengthen the talent pool.

Threats

The global energy transition poses an existential challenge to Kazakhstan's economic model. Accelerating decarbonisation efforts, particularly in Europe and China—Kazakhstan's key export markets—threaten long-term demand for fossil fuels. Peak oil demand scenarios could materialise within the next decade, potentially stranding hydrocarbon assets and eroding the fiscal base before economic diversification achieves critical mass. Whilst the Tengiz expansion will boost near-term production, the project's multi-decade payback period faces demand uncertainty. Carbon border adjustment mechanisms and other climate policies could further disadvantage hydrocarbon exports.

Geopolitical tensions surrounding Russia create multifaceted risks. Kazakhstan must navigate complex relationships with Moscow whilst maintaining ties to Western partners and China, a balancing act that becomes increasingly difficult as great power competition intensifies. Russian pressure to align with Moscow's positions on sanctions and foreign policy could trigger Western countermeasures, whilst excessive accommodation of Western interests risks Russian retaliation through export route disruptions or political interference. The precedent of Russian military intervention in neighbouring states, combined with Kazakhstan's significant ethnic Russian minority (approximately 18% of the population), creates latent security concerns.

Domestic political stability faces medium-term uncertainties. Whilst President Tokayev has consolidated control following the January 2022 unrest, underlying grievances regarding inequality, corruption, and limited political participation remain unaddressed. The government's legitimacy rests substantially on delivering economic prosperity, making it vulnerable to commodity price downturns or reform-induced disruptions. Succession planning remains opaque, creating uncertainty about policy continuity. Regional disparities between resource-rich western provinces and the rest of the country fuel social tensions.

Climate change and water scarcity present growing environmental risks. Kazakhstan faces increasing temperatures, changing precipitation patterns, and glacier retreat that threaten agricultural productivity and water availability. The Aral Sea disaster demonstrates the country's vulnerability to environmental mismanagement, whilst competition with downstream neighbours over transboundary water resources could escalate. Extreme weather events, including droughts and floods, have become more frequent, imposing economic costs and potentially triggering social unrest in affected regions.

Economic Analysis

Growth Dynamics and Structural Composition

Kazakhstan's economic trajectory demonstrates considerable resilience amidst a challenging external environment, though the growth profile remains intrinsically linked to hydrocarbon sector performance. The economy's recovery from the pandemic-induced contraction has been sustained, with growth averaging approximately 4% annually since 2021. The acceleration to 5.1% in 2023 represented the strongest expansion in recent years, driven by robust oil production increases and elevated commodity prices, before moderating to 4.0% in 2024 as global energy markets normalised.

The hydrocarbon sector's dominance continues to shape Kazakhstan's growth dynamics, with oil accounting for approximately 20% of GDP and constituting over 50% of total exports. This concentration creates significant vulnerability to global energy price fluctuations and demand patterns, a structural weakness that rating agencies consistently identify as a key constraint on the sovereign's creditworthiness. The Tengiz oilfield expansion project, one of the world's largest oil production facilities, is expected to provide meaningful support to growth prospects through 2025 and beyond, with production capacity increases anticipated to reach 260,000 barrels per day upon completion. Oil production recovered to 1.75 million barrels per day in 2024, approaching the 2022 peak of 1.77 million barrels per day, reflecting both the Tengiz expansion and broader sectoral investments.

Beyond hydrocarbons, the non-oil economy has demonstrated moderate growth, supported by construction activity, services sector expansion, and agricultural production. The government's ambitious diversification initiatives aim to reduce commodity dependence through targeted support for manufacturing, agribusiness, and digital economy development. However, implementation of these structural reforms remains uneven, with institutional weaknesses and governance challenges constraining the pace of economic transformation. The surge in foreign direct investment to $15.7 billion in 2024—an 88% year-on-year increase and a post-Soviet record—signals growing investor confidence, though extractive industries continue to dominate capital inflows, underscoring the persistent challenge of achieving meaningful economic diversification.

Inflation Dynamics and Price Stability Challenges

Persistent inflationary pressures represent a significant macroeconomic vulnerability and a key rating constraint for Kazakhstan. Inflation has remained stubbornly elevated since 2021, consistently exceeding the National Bank of Kazakhstan's 5% target corridor. The inflation trajectory peaked at 14.7% in 2022, driven by a confluence of factors including global supply chain disruptions, surging commodity prices, and substantial spillover effects from Russia's invasion of Ukraine and subsequent Western sanctions. Whilst inflation has moderated from this peak, declining to 9.8% in 2023 and 8.6% in 2024, the pace of disinflation has been slower than anticipated, reflecting both external pressures and domestic structural factors.

Several structural elements contribute to Kazakhstan's inflation persistence. The economy's substantial import dependence, particularly for consumer goods and manufactured products, creates vulnerability to external price shocks and exchange rate fluctuations. The tenge's depreciation against major currencies has transmitted imported inflation into domestic prices, particularly affecting food and non-food consumer goods. Additionally, Kazakhstan's geographic position and trade linkages with Russia mean that economic disruptions in neighbouring countries rapidly transmit through cross-border trade channels, complicating domestic price stability efforts.

Food price inflation has been particularly pronounced, reflecting both global agricultural commodity price increases and domestic supply constraints. The government has implemented various administrative measures to contain food price pressures, including export restrictions on certain agricultural products and price monitoring mechanisms, though these interventions have had limited sustained impact. Housing and utilities costs have also contributed meaningfully to headline inflation, driven by construction sector dynamics and regulated tariff adjustments. The persistence of inflation above target erodes real incomes, constrains household purchasing power, and complicates monetary policy formulation, representing a medium-term challenge to macroeconomic stability.

Monetary Policy Framework and Central Bank Response

The National Bank of Kazakhstan has maintained a relatively tight monetary policy stance in response to persistent inflationary pressures, though policy effectiveness has been constrained by structural factors and external shocks. The central bank operates under an inflation-targeting framework with a medium-term target of 5%, though actual inflation has consistently exceeded this objective since 2021. The policy rate has been adjusted upwards in multiple steps to combat inflation, though the transmission mechanism remains imperfect given the banking sector's structure and the economy's dollarisation characteristics.

Exchange rate management represents a critical dimension of Kazakhstan's monetary policy framework. The National Bank transitioned to a floating exchange rate regime in 2015, allowing greater exchange rate flexibility to absorb external shocks. However, the central bank continues to intervene in foreign exchange markets to smooth excessive volatility and maintain orderly market conditions, drawing on substantial foreign exchange reserves that reached $45.8 billion in 2024. These reserves, equivalent to approximately seven months of import coverage, provide considerable capacity to defend the currency during periods of stress, though persistent current account deficits and capital flow volatility periodically test this buffer.

The monetary policy transmission mechanism faces structural impediments that limit the central bank's ability to influence inflation outcomes. The banking sector's relatively high dollarisation—with foreign currency deposits and loans comprising a significant share of total banking system assets and liabilities—reduces the effectiveness of domestic interest rate adjustments. Additionally, administered prices for utilities and certain essential goods, which are set by government decree rather than market forces, account for a meaningful portion of the consumer price index, limiting the scope for monetary policy to influence headline inflation. The central bank's credibility has been tested by the prolonged period of above-target inflation, though its commitment to price stability and operational independence remain broadly intact, supporting confidence in the monetary policy framework despite implementation challenges.

Political & Institutional Assessment

Kazakhstan's political landscape has undergone significant transformation since President Kassym-Jomart Tokayev consolidated power following the January 2022 civil unrest, which resulted in over 200 deaths and exposed deep-seated social tensions. The crisis prompted Tokayev to accelerate political reforms whilst simultaneously strengthening his control over the security apparatus and reducing the influence of former President Nursultan Nazarbayev, who had maintained considerable behind-the-scenes authority since his 2019 resignation. This power consolidation has created a more centralised governance structure, reducing factional competition within the elite but concentrating decision-making authority.

The government has introduced a series of constitutional and institutional reforms aimed at addressing public grievances and improving governance standards. A June 2022 constitutional referendum approved changes including presidential term limits, enhanced parliamentary powers, and the abolition of the death penalty. Subsequent parliamentary elections in March 2023 saw increased representation for opposition parties, though the ruling Amanat party retained a commanding majority. These reforms represent meaningful steps towards political liberalisation, yet implementation remains constrained by entrenched interests and weak institutional capacity. The judiciary continues to lack independence, corruption remains pervasive across government institutions, and civil society faces restrictions on political activity.

Governance indicators reflect these persistent institutional weaknesses. Kazakhstan ranks in the 42nd percentile globally for government effectiveness and the 35th percentile for control of corruption according to World Bank governance metrics. Regulatory quality and rule of law indicators similarly place the country in the middle range of emerging markets, substantially below investment-grade peers in Central Europe but ahead of regional neighbours in Central Asia. The business environment has improved incrementally, with Kazakhstan ranking 25th in the World Bank's Ease of Doing Business index prior to its discontinuation, though contract enforcement and property rights protection remain problematic.

The political system remains fundamentally authoritarian despite reform rhetoric, with power concentrated in the presidency and limited checks on executive authority. Media freedom is constrained, with state influence over major outlets and periodic harassment of independent journalists. Civil society organisations operate under restrictive legislation that limits their activities and funding sources. These institutional deficiencies create uncertainty around policy implementation and increase the risk of social instability, particularly given persistent income inequality and regional development disparities between the prosperous oil-producing west and less developed southern regions.

Tokayev's reform agenda includes ambitious economic diversification initiatives and anti-corruption measures, yet progress has been uneven. High-profile corruption prosecutions have targeted some officials, but systemic reforms to strengthen institutional accountability remain incomplete. The president has sought to balance competing interests amongst elite factions whilst maintaining stability, a delicate equilibrium that could prove fragile under economic stress or external shocks. The 2022 unrest demonstrated the potential for rapid escalation of social tensions, particularly around issues of economic inequality and perceived elite corruption.

Geopolitical positioning significantly influences Kazakhstan's institutional development and policy autonomy. The country maintains a multi-vector foreign policy, balancing relationships with Russia, China, the European Union, and the United States. This approach has provided diplomatic flexibility but also creates vulnerabilities, particularly regarding Russia's expectations of political alignment. Kazakhstan has carefully navigated Western sanctions on Russia following the Ukraine invasion, maintaining economic ties with Moscow whilst avoiding actions that would trigger secondary sanctions. This balancing act requires sophisticated diplomatic management and creates ongoing policy uncertainty.

The medium-term political outlook remains stable but subject to meaningful risks. Tokayev's consolidation of power has reduced elite competition and created clearer lines of authority, supporting policy continuity. However, the lack of genuine political pluralism and weak institutions create vulnerabilities to social unrest, particularly if economic conditions deteriorate or inflation remains elevated. Succession planning remains opaque, and the absence of established mechanisms for political transition represents a structural weakness. The government's ability to implement lasting institutional reforms and address corruption will prove critical to maintaining social stability and supporting sustainable economic development beyond the hydrocarbon sector.

Banking Sector & Financial Stability

Kazakhstan's banking sector has demonstrated considerable resilience following the comprehensive restructuring undertaken after the 2017–2018 banking crisis, which necessitated substantial government intervention and consolidation. The sector now exhibits strong capitalisation metrics and adequate liquidity buffers, though the legacy of non-performing loans and concentrated ownership structures continue to warrant supervisory attention. The National Bank of Kazakhstan has maintained a proactive regulatory stance, implementing Basel III standards and strengthening macroprudential frameworks to enhance systemic stability.

The sector's capitalisation remains robust, with the aggregate capital adequacy ratio standing at approximately 20% as of mid-2024, well above the regulatory minimum of 10.5%. Tier 1 capital ratios similarly exceed regulatory requirements, providing substantial loss-absorption capacity. Liquidity indicators have improved markedly, with the liquid assets ratio maintained above 40% across the system, reflecting both regulatory requirements and banks' cautious approach to balance sheet management following previous stress episodes. Return on equity has recovered to approximately 15–17% for the sector, though profitability remains concentrated amongst the largest institutions.

Asset quality metrics have shown gradual improvement, with the non-performing loan ratio declining to approximately 5–6% of total loans by late 2024, down from double-digit levels in the immediate aftermath of the 2017–2018 crisis. However, this improvement partly reflects regulatory forbearance measures and loan restructurings rather than purely organic credit quality enhancement. Provisioning coverage has strengthened, with provisions covering approximately 80–85% of non-performing exposures, though significant variation exists across institutions. Credit growth has accelerated to approximately 12–15% annually, driven primarily by retail lending and corporate working capital facilities, raising questions about underwriting standards in an environment of persistent inflation and currency volatility.

The sector remains highly concentrated, with the five largest banks accounting for approximately 60% of total assets. State ownership remains significant, with the government maintaining controlling or substantial stakes in several systemically important institutions, including Halyk Bank and Kazkommertsbank. This ownership structure creates potential contingent liabilities for the sovereign, though the government has demonstrated willingness to provide support when necessary. Foreign bank participation has diminished following the crisis period, with several international institutions reducing their presence or exiting the market entirely.

Dollarisation presents an ongoing structural vulnerability, with foreign currency loans comprising approximately 30–35% of total lending and foreign currency deposits representing a similar proportion of funding. This currency mismatch creates exchange rate risk for both banks and unhedged borrowers, particularly given the tenge's historical volatility. The National Bank has implemented measures to discourage dollarisation, including differentiated reserve requirements and lending restrictions, though progress has been gradual. The central bank's foreign exchange reserves and the National Fund's assets provide substantial buffers to manage currency pressures, but rapid depreciation could nonetheless strain borrowers' repayment capacity and crystallise credit losses.

The regulatory and supervisory framework has been strengthened considerably, with the National Bank enhancing its stress-testing capabilities, implementing risk-based supervision, and improving resolution frameworks. Deposit insurance coverage has been expanded to 20 million tenge (approximately $42,000), providing protection for the vast majority of retail depositors. However, institutional capacity constraints and governance weaknesses in some supervised entities continue to challenge effective oversight. The authorities have made progress in addressing anti-money laundering and combating the financing of terrorism concerns, though Kazakhstan remains on the Financial Action Task Force's enhanced monitoring list, reflecting ongoing implementation challenges.

Looking forward, the banking sector faces several key challenges that could affect both financial stability and the sovereign's contingent liability exposure. Rapid credit growth in an inflationary environment raises concerns about asset quality deterioration, particularly if monetary tightening proves necessary to anchor inflation expectations. The concentration of lending to commodity-related sectors creates vulnerability to oil price shocks and global energy transition dynamics. Cyber security risks have increased as digitalisation accelerates, requiring continued investment in technological infrastructure and risk management capabilities. Nevertheless, the sector's improved capitalisation, enhanced regulatory framework, and the sovereign's demonstrated capacity to provide support if necessary underpin a stable assessment of financial sector risks to the sovereign credit profile.

Outlook & Scenarios

Short-Term Outlook (12 months)

Kazakhstan's near-term credit profile is expected to remain stable through 2026, underpinned by robust sovereign buffers and continued hydrocarbon export revenues. The economy is projected to sustain growth momentum of 4-5%, driven primarily by the Tengiz oilfield expansion, which is anticipated to add approximately 260,000 barrels per day to production capacity. This expansion represents a significant boost to export revenues and fiscal receipts, providing the government with enhanced capacity to finance infrastructure investments and social spending commitments. The National Bank of Kazakhstan faces ongoing challenges in anchoring inflation expectations, with price pressures likely to persist above the 5% target through the first half of 2026, reflecting structural factors including food price volatility, currency depreciation pressures, and administered price adjustments in utilities and transport.

The fiscal position is expected to remain in moderate deficit, likely in the range of 2.5-3.5% of GDP, as the government balances infrastructure investment priorities against revenue constraints. Continued transfers from the National Fund of Kazakhstan will be necessary to finance the deficit, though the fund's substantial asset base of approximately $60 billion provides ample capacity to support fiscal operations without threatening medium-term sustainability. Foreign exchange reserves are projected to remain robust at around $45-48 billion, maintaining comfortable import coverage of six to seven months. The current account is likely to record a modest deficit of 1-2% of GDP, reflecting the balance between strong hydrocarbon exports and elevated imports of capital goods and consumer products.

Geopolitical considerations will remain prominent in the short-term outlook, particularly regarding export route diversification. Kazakhstan's dependence on Russian pipeline infrastructure for the majority of oil exports creates ongoing vulnerability to transit disruptions, as demonstrated by periodic technical issues at the Caspian Pipeline Consortium terminal. The government's efforts to expand alternative routes, including the Trans-Caspian International Transport Route and increased rail shipments to China, will progress incrementally but are unlikely to materially reduce Russian route concentration within the twelve-month horizon. Political stability under President Tokayev's consolidated leadership is expected to be maintained, though implementation of governance reforms will likely remain gradual, with limited near-term impact on institutional quality metrics.

Medium-Term Outlook (1-3 years)

Over the medium term, Kazakhstan's credit trajectory will be determined by the interplay between its substantial fiscal and external buffers and the pace of structural reform implementation. The government's ambitious diversification agenda, articulated in various strategic documents, aims to reduce hydrocarbon dependency and develop non-extractive sectors including agriculture, logistics, and manufacturing. However, historical experience suggests that implementation will be gradual and uneven, constrained by institutional capacity limitations, vested interests in the hydrocarbon sector, and the challenge of creating competitive advantages in non-resource industries. The Tengiz expansion will provide a window of enhanced fiscal space through 2027-2028, which could be leveraged for productive investments in infrastructure, education, and governance systems, though there remains significant risk that windfall revenues will be absorbed by current expenditure rather than transformational reforms.

Inflation dynamics over the medium term will be critical to macroeconomic stability and living standards. Achieving sustained convergence towards the 5% target will require not only appropriate monetary policy settings but also structural measures to enhance competition, improve supply chain efficiency, and strengthen the transmission mechanism of monetary policy. The National Bank's credibility and operational independence will be tested by potential political pressures to maintain accommodative policy settings to support growth objectives. The banking sector is expected to remain resilient, with strong capitalisation ratios and adequate liquidity buffers, though credit growth to the corporate and household sectors will require careful monitoring to prevent the accumulation of vulnerabilities.

The medium-term fiscal outlook presents both opportunities and risks. On one hand, the low public debt stock provides substantial headroom for countercyclical policy and strategic investments. On the other hand, the absence of clear fiscal rules governing National Fund transfers creates uncertainty about fiscal discipline and the long-term preservation of sovereign wealth. The government's ability to broaden the non-hydrocarbon revenue base through tax administration improvements and economic diversification will be crucial to reducing dependence on volatile commodity revenues. External vulnerabilities related to export route concentration are likely to persist, though incremental progress on alternative corridors may modestly reduce Russian transit dependency from current levels exceeding 80% to perhaps 70-75% by 2028.

Geopolitical positioning between China, Russia, and Europe will continue to shape Kazakhstan's economic and political landscape. The country's participation in China's Belt and Road Initiative provides opportunities for infrastructure development and market access, whilst maintaining pragmatic relations with Russia remains essential given geographic proximity and extensive economic linkages. Balancing these relationships whilst pursuing closer engagement with European markets and institutions will require sophisticated diplomacy. The global energy transition poses a long-term structural challenge to Kazakhstan's hydrocarbon-dependent model, though the impact over the three-year medium-term horizon is likely to be limited, with oil demand remaining robust and natural gas potentially benefiting from its role as a transition fuel.

Rating Scenarios

Kazakhstan's sovereign ratings could experience upward pressure under a scenario characterised by sustained implementation of structural reforms, meaningful economic diversification, and strengthened institutional frameworks. Specific catalysts for a positive rating action would include a demonstrable reduction in hydrocarbon dependency, with non-oil sectors contributing an increasing share of GDP growth and fiscal revenues; successful diversification of export routes, reducing reliance on Russian infrastructure to below 60-65% of oil exports; adoption and adherence to a credible fiscal framework that limits National Fund transfers and ensures long-term wealth preservation; and sustained inflation convergence towards the 5% target, reflecting enhanced monetary policy credibility and structural improvements in price formation mechanisms. Additionally, tangible progress on governance indicators, including reduced corruption perceptions, strengthened rule of law, and improved regulatory quality, would support a positive rating trajectory. Moody's upgrade to Baa1 in September 2024 suggests the rating agency perceives progress on these dimensions, and further advancement could position Kazakhstan for additional upgrades from S&P and Fitch.

Conversely, downward rating pressure could emerge from several adverse scenarios. A sustained decline in oil prices below $60 per barrel for an extended period would significantly compress fiscal and external buffers, potentially necessitating substantial National Fund drawdowns and threatening the low public debt profile if the government resorts to external borrowing. Major disruptions to oil export routes, whether due to geopolitical tensions, infrastructure failures, or deliberate transit restrictions, could severely impact export revenues and foreign exchange earnings. A marked deterioration in the regional security environment, including spillover effects from conflicts in neighbouring countries or domestic political instability, would undermine investor confidence and economic performance. Failure to control inflation, particularly if price pressures become entrenched above 10% for a sustained period, would erode real incomes, complicate monetary policy, and signal broader macroeconomic management challenges. Additionally, a reversal of governance reforms, increased state intervention in the economy, or deterioration in the business environment could trigger negative rating actions. The banking sector, whilst currently resilient, could become a source of vulnerability if rapid credit expansion leads to asset quality deterioration, requiring government support that strains fiscal resources.

A stable rating scenario, which appears most probable given the current outlooks from all three major agencies, would involve Kazakhstan maintaining its existing policy trajectory with incremental progress on diversification and reforms, but without transformational breakthroughs. Under this scenario, oil prices would remain in a moderate range of $70-85 per barrel, supporting adequate fiscal and external balances; the National Fund would continue to provide fiscal support whilst maintaining its asset base above $50 billion; inflation would gradually moderate towards 6-7%, remaining above target but avoiding a return to double digits; and the government would implement selective reforms in priority areas whilst broader institutional transformation remains gradual. Export route concentration would decline modestly through incremental capacity additions on alternative corridors, and the political environment would remain stable under consolidated executive authority, with limited but steady progress on governance metrics. This scenario would preserve Kazakhstan's investment-grade status and substantial sovereign buffers whilst acknowledging persistent structural vulnerabilities that constrain upward rating momentum.

Conclusion

Kazakhstan's investment-grade sovereign credit profile reflects a delicate equilibrium between substantial fiscal strengths and persistent structural vulnerabilities. The country's Baa1/BBB/BBB- ratings, with stable outlooks across all three major agencies, are fundamentally anchored by exceptional sovereign wealth buffers—with the National Fund and foreign exchange reserves collectively exceeding 50% of GDP—and a remarkably low public debt burden of 23.7%. These financial cushions provide considerable capacity to absorb external shocks and maintain macroeconomic stability, distinguishing Kazakhstan favourably within its rating category.

The economy's near-term growth trajectory appears robust, with 4-5% expansion anticipated in 2025, supported by the Tengiz oilfield expansion and record foreign direct investment inflows of $15.7 billion in 2024. The banking sector demonstrates resilience through strong capitalisation and liquidity metrics, whilst the country's strategic geographic position between major economic powers—China, Russia, and Europe—offers potential diversification opportunities. Moody's September 2024 upgrade to Baa1 acknowledged tangible progress in governance frameworks and economic diversification efforts under President Tokayev's consolidated leadership.

However, these strengths are counterbalanced by significant structural constraints that limit upward rating momentum. Hydrocarbon dependency remains acute, with oil representing 20% of GDP and over 50% of exports, creating pronounced vulnerability to commodity price volatility and long-term energy transition risks. Export route concentration through Russia introduces geopolitical risk that recent events have brought into sharp relief. Persistent inflation at 8.6%—substantially above the central bank's 5% target—and a widening fiscal deficit of 3.7% of GDP in 2024 signal ongoing macroeconomic management challenges. Perhaps most critically, whilst governance reforms have been announced, implementation remains limited, and institutional weaknesses continue to constrain the investment climate and economic efficiency.

The stable outlook across rating agencies reflects this balanced assessment: substantial buffers provide downside protection, whilst structural vulnerabilities cap upside potential. Kazakhstan's medium-term credit trajectory will ultimately depend on the authorities' ability to translate diversification ambitions into tangible economic transformation, strengthen institutional frameworks beyond rhetorical commitments, and navigate the dual challenges of global energy transition and regional geopolitical complexity. Without meaningful progress on these structural reforms, the sovereign's investment-grade status, whilst secure in the near term, may struggle to advance beyond its current positioning.