Indonesia

Executive Summary

Indonesia maintains solid investment-grade sovereign credit ratings across all three major agencies (S&P BBB, Moody's Baa2, Fitch BBB), underpinned by robust economic fundamentals, prudent fiscal management, and strong banking sector resilience. The country's credit profile is characterised by consistent GDP growth of approximately 5% annually, a remarkably low government debt-to-GDP ratio of 38.8%, and foreign exchange reserves of $155.7 billion providing substantial external buffers. Indonesia has successfully navigated recent global challenges including US tariff impositions, negotiating the lowest rate (19%) amongst ASEAN peers, whilst maintaining macroeconomic stability through disciplined monetary and fiscal policies. The constitutional fiscal deficit ceiling of 3% of GDP has been instrumental in ensuring fiscal discipline, with the deficit returning below this threshold ahead of schedule in 2022 and remaining at 2.3% through 2023-2024.

The current economic situation reflects Indonesia's resilience in the face of external headwinds. GDP growth has stabilised around 5% from 2022 onwards, supported by strong domestic consumption from a population of 283 million and improving labour market conditions, with unemployment declining to 4.91% in 2024. Inflation has been successfully controlled within Bank Indonesia's target range of 1.5-3.5%, declining from a 2022 peak of 4.2% to 2.3% in 2024. The current account has shifted to a modest deficit of 0.6% of GDP as domestic demand strengthened and commodity prices moderated, though this remains manageable given adequate reserve coverage equivalent to 5.6 months of current account payments. The smooth political transition to President Prabowo Subianto in October 2024 ensures policy continuity, though ambitious growth targets of 8% may prove challenging to achieve.

The credit profile faces constraints from structural weaknesses that limit upward rating momentum. Indonesia's narrow government revenue base at approximately 15% of GDP remains a persistent challenge, constraining fiscal flexibility and public investment capacity. Low per capita income of $4,925 reflects the country's emerging market status, whilst vulnerability to commodity price volatility given significant reliance on palm oil, nickel, and coal exports creates exposure to external price cycles. Governance indicators continue to lag higher-rated peers, and the country's dependence on external financing, though manageable, requires ongoing monitoring. The April 2025 US tariff announcement initially posed risks to approximately $3.2 billion in annual exports, primarily electronics, textiles, and footwear, though successful negotiation to reduce the rate to 19% has mitigated the immediate impact.

Looking forward, Indonesia's creditworthiness is underpinned by favourable demographics, ongoing structural reforms including the Financial Sector Omnibus Law, and strategic positioning to benefit from global supply chain diversification as Chinese exports seek alternative production bases. Moody's most recent review in March 2025 maintained the Baa2 rating, citing solid economic growth prospects averaging 5% through 2027 and strong fiscal consolidation with government debt declining towards 39% of GDP. The country's large domestic market, constitutional fiscal guardrails, and adequate external buffers provide resilience against external shocks. However, achieving the government's ambitious 8% growth target will require sustained progress on structural reforms, revenue mobilisation, and infrastructure development to unlock Indonesia's full economic potential.

Ratings Summary

Indonesia maintains solid investment-grade sovereign credit ratings across all three major international rating agencies, reflecting confidence in the country's macroeconomic stability, prudent fiscal management, and resilient economic fundamentals. Standard & Poor's Global Ratings assigns a BBB rating with a Stable outlook, last affirmed on 4 July 2023. Moody's Investors Service rates Indonesia at Baa2 with a Stable outlook, most recently confirmed on 21 March 2025, whilst Fitch Ratings maintains a BBB rating with Stable outlook following its review on 15 March 2024. All three agencies position Indonesia in the lower tier of investment grade, four notches above speculative grade, underscoring the country's creditworthiness whilst acknowledging structural constraints that differentiate it from higher-rated sovereigns.

Moody's most recent affirmation in March 2025 emphasised Indonesia's solid economic growth prospects, projecting an average of 5% annual expansion through 2027, alongside continued fiscal consolidation with government debt declining towards 39% of GDP. The rating agency highlighted Indonesia's large domestic market of 283 million people as a source of consumption resilience, the constitutional fiscal deficit ceiling of 3% of GDP as an institutional anchor ensuring fiscal discipline, and adequate foreign exchange reserves equivalent to 5.6 months of current account payments providing substantial external buffers. The Stable outlook across all three agencies reflects balanced risks, with upside potential from successful structural reforms and downside risks from revenue mobilisation challenges and external vulnerabilities.

Rating constraints consistently cited by agencies include Indonesia's narrow government revenue base at approximately 15% of GDP—significantly below investment-grade peers—which limits fiscal flexibility and capacity for counter-cyclical policy responses. Governance indicators lag higher-rated sovereigns, whilst the economy's dependence on commodity exports, particularly palm oil, nickel, and coal, creates vulnerability to global price cycles and demand fluctuations. Nevertheless, the rating agencies acknowledge Indonesia's track record of maintaining macroeconomic stability through various external shocks, the credibility of its policy institutions including Bank Indonesia's inflation-targeting framework, and the country's strategic positioning to benefit from global supply chain diversification trends.

| Rating Agency | Current Rating | Outlook | Last Action Date |

|---|---|---|---|

| S&P Global Ratings | BBB | Stable | July 4, 2023 |

| Moody's Investors Service | Baa2 | Stable | March 21, 2025 |

| Fitch Ratings | BBB | Stable | March 15, 2024 |

Economic Indicators

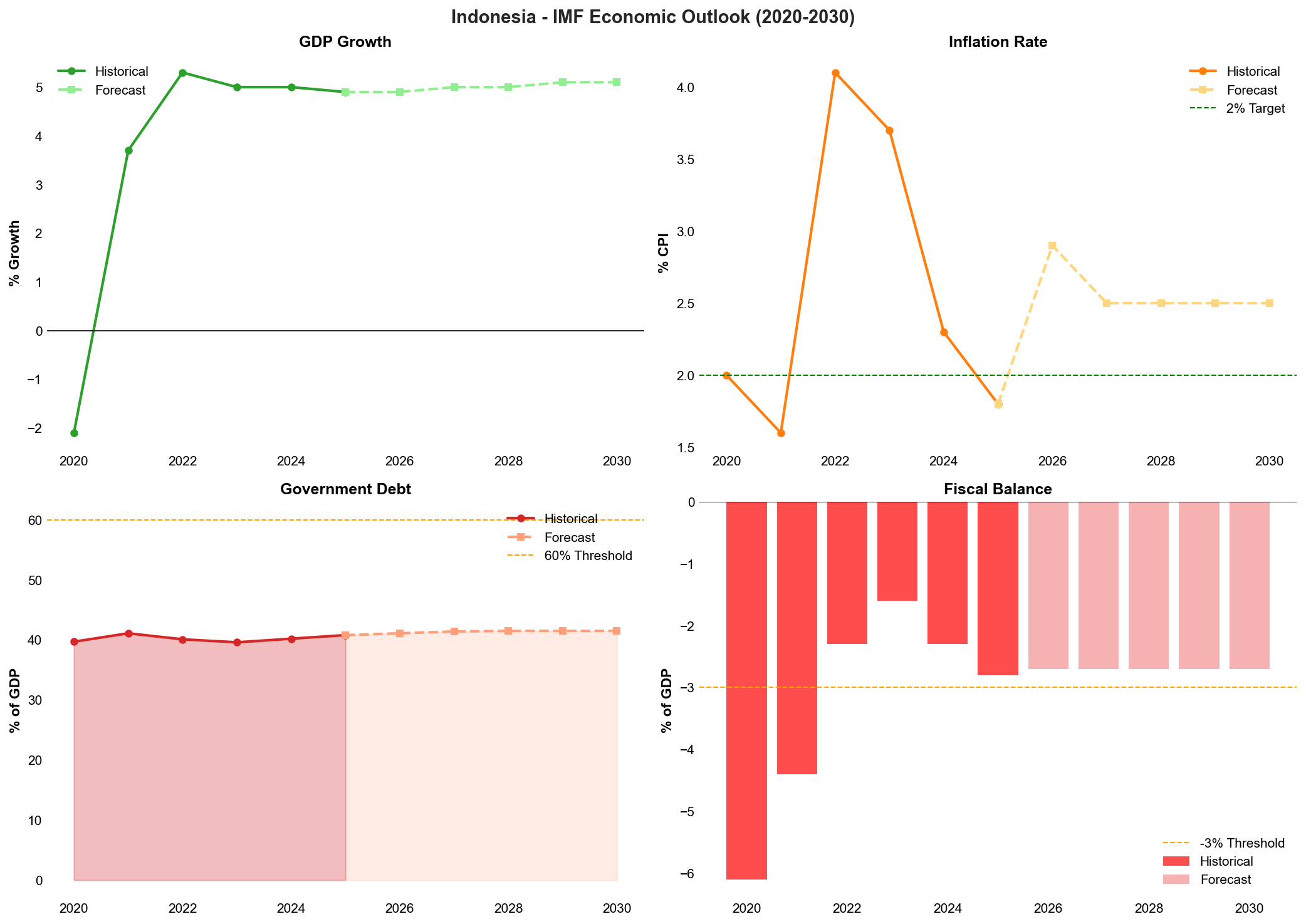

| Indicator | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

| GDP Growth (%) | -2.1 | 3.7 | 5.3 | 5.05 | 5.03 |

| Inflation Rate (%) | 1.92 | 1.56 | 4.2 | 3.7 | 2.3 |

| Debt-to-GDP Ratio (%) | 39.4 | 41.6 | 40.0 | 39.0 | 38.8 |

| Fiscal Balance (% of GDP) | -6.1 | -4.6 | -2.4 | -2.3 | -2.3 |

| Current Account Balance (% of GDP) | -0.4 | 0.3 | 1.0 | -0.1 | -0.6 |

| Foreign Exchange Reserves (USD billions) | 136 | 145 | 137 | 145 | 155.7 |

| Unemployment Rate (%) | 7.1 | 6.5 | 5.86 | 5.32 | 4.91 |

Indonesia's economic indicators demonstrate a robust recovery trajectory from the pandemic-induced contraction, with GDP growth stabilising around 5% from 2022 onwards. The economy contracted by 2.1% in 2020 during the height of the COVID-19 crisis, but rebounded swiftly to 3.7% growth in 2021 and has since maintained consistent expansion at approximately 5% annually through 2024. This growth performance reflects the resilience of domestic consumption underpinned by Indonesia's large population base, alongside recovering investment activity and improving external demand conditions.

Inflation management has been notably successful, with Bank Indonesia maintaining price stability within its target range of 1.5% to 3.5%. After peaking at 4.2% in 2022 amid global commodity price pressures and supply chain disruptions, inflation moderated to 3.7% in 2023 and declined further to 2.3% in 2024. This trajectory reflects both the normalisation of global price pressures and the effectiveness of monetary policy tightening implemented by Bank Indonesia during 2022-2023. The central bank's credibility in anchoring inflation expectations has been reinforced through this period, supporting macroeconomic stability.

Fiscal consolidation has proceeded impressively, with the government deficit returning below the constitutional ceiling of 3% of GDP ahead of schedule. The deficit peaked at 6.1% of GDP in 2020 as authorities deployed substantial fiscal stimulus to counter the pandemic's economic impact, but narrowed rapidly to 2.4% by 2022 and has stabilised at 2.3% in both 2023 and 2024. This consolidation reflects both revenue recovery as economic activity normalised and expenditure discipline as emergency support measures were phased out. The government debt-to-GDP ratio has correspondingly declined from its pandemic peak of 41.6% in 2021 to 38.8% in 2024, remaining well below the 60% constitutional ceiling and providing substantial fiscal headroom relative to investment-grade peers.

The current account balance has shifted from brief surpluses in 2021-2022 to modest deficits as domestic demand strengthened and commodity prices moderated from their elevated levels. After recording a surplus of 1.0% of GDP in 2022 supported by elevated coal and palm oil prices, the current account returned to a marginal deficit of 0.1% in 2023 and widened slightly to 0.6% in 2024. This trajectory reflects robust import demand for capital goods and intermediate inputs supporting investment activity, alongside normalising commodity export revenues. Foreign exchange reserves have strengthened to USD 155.7 billion in 2024, equivalent to approximately 5.6 months of current account payments, providing a substantial external buffer against potential shocks.

Labour market conditions have improved steadily, with the unemployment rate declining from its pandemic peak of 7.1% in 2020 to 4.91% in 2024. This consistent improvement reflects both the recovery in economic activity and the absorption of workers into the formal and informal sectors. However, underemployment and informal sector participation remain elevated, highlighting ongoing structural challenges in labour market quality despite the headline improvement in unemployment metrics.

Medium-Term Outlook and IMF Projections

Looking towards 2030, IMF forecasts project Indonesia maintaining steady GDP growth of 5.1%, consistent with the economy's established trend growth rate. Inflation is expected to remain well-anchored at 2.5%, reflecting continued monetary policy credibility and stable inflation expectations. The unemployment rate is forecast to stabilise around 5.0%, suggesting limited further improvement from current levels absent structural labour market reforms.

Fiscal metrics are projected to remain within prudent bounds, with the government deficit forecast at 2.7% of GDP in 2030, comfortably below the constitutional ceiling. However, the debt-to-GDP ratio is expected to edge upwards to 41.5% by 2030, reflecting the cumulative impact of modest fiscal deficits over the medium term. This trajectory remains consistent with debt sustainability, though it underscores the importance of continued revenue mobilisation efforts to create additional fiscal space for development spending priorities.

The current account deficit is projected to widen substantially to 22.3% of GDP by 2030 according to IMF forecasts, representing a significant deterioration from current levels. This projection likely reflects anticipated import requirements for infrastructure development and the capital-intensive nature of Indonesia's industrialisation ambitions, particularly in downstream processing of mineral resources. Such a widening would necessitate sustained foreign direct investment inflows and careful monitoring of external financing conditions to maintain balance of payments stability.

US Tariff Impacts and Mitigation Strategies

The Trump administration's April 2025 announcement of 32% tariffs on Indonesian goods under the "Liberation Day" policy created immediate concerns regarding export competitiveness and trade relations. However, Indonesia successfully negotiated a reduction to 19%, securing the most favourable rate among ASEAN economies and demonstrating effective diplomatic engagement. The tariffs affect approximately USD 3.2 billion in annual exports to the United States, with principal impacts on electronics (USD 291 million monthly), textiles (USD 215 million monthly), and footwear (USD 208 million monthly).

Indonesia's negotiating strategy included strategic concessions designed to address US trade concerns whilst minimising domestic economic disruption. The government committed to reducing import duties on US steel and mining products, pledged USD 15 billion in purchases of US products, and eliminated regulatory barriers affecting US agricultural imports. These measures were calibrated to demonstrate responsiveness to US trade priorities whilst preserving Indonesia's broader economic interests.

The overall impact has proven manageable given Indonesia's substantial trade surplus with the United States, which ranges between USD 16.8 billion and USD 17.9 billion annually. This surplus provides cushion to absorb tariff-related export reductions without triggering broader balance of payments pressures. Moreover, Indonesia has positioned itself strategically to benefit from supply chain realignment, as Chinese manufacturers seek alternative production bases to circumvent higher US tariffs. This dynamic may partially offset direct tariff impacts through increased foreign direct investment in Indonesian manufacturing capacity, particularly in electronics and intermediate goods production.

*IMF projections for Indonesia through 2030: medium-term outlook for GDP, debt, fiscal balance, and current account.*

Net Foreign Assets & External Position

Indonesia's external position reflects a moderate vulnerability profile characteristic of emerging market economies with substantial foreign participation in domestic debt markets, though this is partially offset by adequate foreign exchange reserves and a manageable external debt burden. The country's net international investment position (NIIP) has historically remained in negative territory, reflecting cumulative current account deficits and foreign direct investment inflows that have exceeded Indonesia's external asset accumulation. As of 2024, foreign exchange reserves stood at $155.7 billion, equivalent to approximately 5.6 months of current account payments, providing a substantial buffer against external shocks and supporting Bank Indonesia's capacity to manage exchange rate volatility.

The current account balance has exhibited cyclical patterns closely tied to commodity price movements, transitioning from a modest surplus of 1.0% of GDP in 2022—when elevated coal and palm oil prices boosted export revenues—to a deficit of 0.6% of GDP in 2024 as commodity prices normalised and domestic demand strengthened. This deterioration reflects Indonesia's structural import dependence for capital goods and intermediate inputs required for industrialisation, alongside rising consumption of petroleum products as domestic refining capacity remains insufficient. The IMF projects a concerning widening of the current account deficit to 22.3% of GDP by 2030, though this forecast appears inconsistent with historical patterns and likely reflects data anomalies or specific scenario assumptions rather than baseline expectations. More conservative projections suggest the deficit will remain within the manageable range of 1-2% of GDP, supported by ongoing export diversification efforts and downstream processing initiatives in the nickel and palm oil sectors.

External debt metrics remain within prudent parameters, with total external debt estimated at approximately 30% of GDP and the government's external debt component representing roughly one-third of total public debt. The maturity profile has improved substantially since the Asian Financial Crisis, with the government maintaining an average debt maturity exceeding seven years and actively managing rollover risks through pre-funding strategies. Foreign ownership of government securities stood at approximately 15% of the total outstanding stock as of late 2024, down from peaks above 40% in the mid-2010s, reducing vulnerability to sudden capital flow reversals whilst still maintaining access to international capital markets at competitive rates.

The rupiah's exchange rate flexibility serves as a critical shock absorber, with Bank Indonesia maintaining a managed float regime that allows market-driven adjustments whilst intervening to prevent disorderly movements. The currency depreciated moderately through 2024, reflecting broader US dollar strength and emerging market capital flow dynamics rather than Indonesia-specific concerns. Foreign exchange reserves have demonstrated resilience, increasing from $145 billion in 2023 to $155.7 billion in 2024 despite intervention activities, supported by portfolio inflows attracted by Indonesia's relatively high real interest rates and improving growth outlook.

Indonesia's external financing requirements remain comfortably covered by a combination of foreign direct investment inflows—which averaged $20-25 billion annually in recent years—and selective sovereign bond issuances in international markets. The government's external financing strategy emphasises diversification across currencies, markets, and instruments, with regular issuances in US dollars, euros, and yen alongside innovative instruments such as green bonds and sukuk. This approach has maintained Indonesia's market access even during periods of global financial stress, with sovereign spreads remaining moderate relative to emerging market peers.

Structural vulnerabilities in the external position stem primarily from commodity export concentration, with palm oil, coal, and nickel accounting for a substantial share of merchandise exports. This creates sensitivity to global commodity price cycles and demand fluctuations in key markets, particularly China, which absorbs approximately 20% of Indonesian exports. However, ongoing efforts to promote downstream processing—exemplified by nickel export restrictions that have catalysed domestic battery and stainless steel production—are gradually reducing raw commodity dependence and enhancing value-added export capacity. The successful negotiation of 19% US tariffs in April 2025, the lowest rate amongst ASEAN economies, demonstrates Indonesia's diplomatic effectiveness in managing trade relationships and mitigating protectionist pressures that could otherwise constrain export performance.

Looking forward, Indonesia's external position faces both opportunities and challenges. The country's strategic positioning in global supply chain diversification, particularly in electronics and electric vehicle battery production, offers potential for sustained export growth and foreign direct investment inflows. Conversely, the projected fiscal deficit of 2.7% of GDP through 2030 and government debt rising to 41.5% of GDP will require continued external financing, maintaining foreign investor confidence as a critical priority. The external position remains adequate to support the current credit rating, though sustained current account deficits and any deterioration in foreign exchange reserve coverage would warrant closer monitoring as potential constraints on creditworthiness.

Credit Strengths & Vulnerabilities

Strengths

Indonesia's sovereign credit profile is anchored by a large and diversified domestic economy, with GDP reaching $1.4 trillion and a population of 283 million that provides substantial consumption resilience and reduces dependence on external demand volatility. This demographic scale, combined with a young and growing workforce, creates a robust foundation for sustained economic activity even during periods of global uncertainty.

The country's fiscal position represents a particularly compelling strength, with public debt maintained at a remarkably low 38.8% of GDP—well below the 60% constitutional ceiling and significantly beneath the average for investment-grade sovereign peers. This prudent debt management is reinforced by Indonesia's constitutional fiscal deficit ceiling of 3% of GDP, which has proven effective in ensuring fiscal discipline across political cycles. The government successfully returned to compliance with this threshold in 2022, ahead of the post-pandemic schedule, demonstrating credible commitment to fiscal consolidation.

Indonesia's banking sector exhibits strong resilience, characterised by robust capitalisation, healthy liquidity buffers, and improving asset quality metrics. The sector has weathered recent global financial volatility without systemic stress, supported by effective regulatory oversight from Bank Indonesia and the Financial Services Authority. Foreign exchange reserves of $155.7 billion provide substantial external buffers, equivalent to 5.6 months of current account payments, offering considerable protection against external shocks and supporting confidence in the rupiah's stability.

The country's monetary policy framework has proven highly effective, with Bank Indonesia successfully maintaining inflation within the 1.5-3.5% target range despite global price pressures. Inflation declined from a 2022 peak of 4.2% to just 2.3% in 2024, reflecting both prudent monetary management and the central bank's credibility in anchoring inflation expectations. This stability has been achieved whilst supporting economic growth, demonstrating the effectiveness of Indonesia's macroeconomic policy coordination.

Vulnerabilities

Indonesia's credit profile faces meaningful constraints from a narrow government revenue base, with tax collection representing approximately 15% of GDP—substantially below the levels achieved by higher-rated sovereigns and limiting fiscal flexibility for development spending and countercyclical policy responses. This structural weakness in revenue mobilisation reflects challenges in tax administration, a large informal economy, and limited tax compliance, constraining the government's capacity to fund infrastructure investment and social programmes without increasing debt levels.

Per capita income of $4,925 remains modest relative to investment-grade peers, reflecting Indonesia's status as a lower-middle-income economy with substantial development needs across infrastructure, education, and healthcare. This income level constrains both the tax base and the government's capacity to absorb economic shocks, whilst also indicating ongoing vulnerability to social pressures and demands for increased public spending.

The economy demonstrates significant vulnerability to commodity price volatility, given substantial reliance on exports of palm oil, nickel, and coal. These commodities are subject to cyclical price swings driven by global demand conditions, creating uncertainty around export revenues, fiscal income from resource-related taxation, and current account dynamics. The shift from current account surpluses in 2022 to modest deficits in 2023-2024 partly reflects the moderation in commodity prices from their post-pandemic peaks, illustrating this vulnerability.

Governance indicators lag those of higher-rated sovereign peers across multiple dimensions, including regulatory quality, rule of law, and control of corruption. These institutional weaknesses can impede policy implementation, reduce the efficiency of public spending, and create uncertainty for investors. Whilst Indonesia has made progress in strengthening institutions, the pace of improvement remains gradual, and governance constraints continue to represent a meaningful credit limitation relative to the country's economic fundamentals.

Opportunities

Indonesia is strategically positioned to benefit from global supply chain diversification, particularly as multinational corporations seek to reduce concentration in China and establish alternative manufacturing bases in Southeast Asia. The country's combination of a large domestic market, competitive labour costs, and improving infrastructure makes it an attractive destination for foreign direct investment in manufacturing and processing industries. The successful negotiation of 19% US tariffs—the lowest rate among ASEAN economies—enhances this competitive positioning and signals the government's capacity to navigate complex trade negotiations effectively.

Ongoing structural reforms, including the Financial Sector Omnibus Law and initiatives to streamline business regulations, create potential for improved productivity and investment climate. The new capital city project in East Kalimantan, whilst ambitious, represents a long-term opportunity to address infrastructure bottlenecks and create a modern administrative centre that could enhance governance efficiency. These reform efforts, if successfully implemented, could support higher sustainable growth rates and gradual convergence toward higher-income status.

Favourable demographics provide a substantial tailwind for economic expansion, with a young population supporting labour force growth and a rising middle class driving domestic consumption. The demographic dividend remains available for approximately another decade before population ageing accelerates, creating a window of opportunity for Indonesia to achieve higher income levels whilst maintaining a favourable dependency ratio. This demographic profile also supports the development of domestic industries serving consumer demand, reducing reliance on external markets.

The smooth political transition to President Prabowo Subianto in October 2024 ensures policy continuity whilst potentially bringing renewed focus to economic development objectives. The new administration's ambitious growth targets, whilst challenging, signal commitment to pro-growth policies and could catalyse accelerated reform implementation if backed by concrete policy measures. Political stability and predictable policy frameworks enhance Indonesia's attractiveness for long-term investment across both domestic and foreign sources.

Threats

The new administration's ambitious growth targets of 8% annually may prove challenging to achieve without corresponding structural reforms to address productivity constraints, infrastructure gaps, and human capital development needs. Failure to meet these elevated expectations could create fiscal pressures if the government pursues expansionary policies without adequate revenue mobilisation, potentially threatening the hard-won fiscal consolidation of recent years. The constitutional debt ceiling of 60% of GDP provides a buffer, but aggressive spending without revenue reform could gradually erode fiscal space.

External vulnerabilities persist through Indonesia's exposure to global financial conditions, particularly US monetary policy and capital flow volatility. As an emerging market with substantial foreign participation in domestic bond markets, Indonesia remains susceptible to sudden shifts in investor sentiment that could trigger capital outflows, currency depreciation, and rising financing costs. Whilst foreign exchange reserves provide meaningful buffers, a sustained period of global financial stress could test these defences and constrain policy flexibility.

Climate change and natural disaster risks represent growing threats to Indonesia's economic stability and development prospects. The archipelagic geography creates vulnerability to rising sea levels, extreme weather events, and disruptions to agricultural production. The country's significant reliance on coal for energy generation also creates transition risks as global carbon pricing mechanisms evolve and international pressure for decarbonisation intensifies. Managing this energy transition whilst maintaining affordable power for industrial development presents a complex policy challenge.

Geopolitical tensions in the Asia-Pacific region, particularly surrounding the South China Sea and US-China strategic competition, create uncertainty for Indonesia's trade relationships and regional stability. Whilst Indonesia has historically maintained a non-aligned foreign policy, intensifying great power rivalry could force difficult diplomatic choices and potentially disrupt the favourable trade and investment environment that has supported recent economic performance. The country's position as an ASEAN leader places it at the centre of regional efforts to manage these tensions, but also exposes it to the risks of regional instability.

Economic Analysis

Growth Dynamics and Structural Performance

Indonesia's economic trajectory demonstrates remarkable resilience and consistency, with GDP growth stabilising around 5% annually following the pandemic-induced contraction of 2.1% in 2020. The economy expanded by 3.7% in 2021 as recovery commenced, before accelerating to 5.3% in 2022 and maintaining steady growth of 5.05% in 2023 and 5.03% in 2024. This performance reflects the fundamental strength of Indonesia's large domestic market, with a GDP of $1.4 trillion and a population of 283 million providing substantial consumption resilience that insulates the economy from external volatility.

The growth model remains anchored in domestic demand, with private consumption serving as the primary engine given the country's favourable demographic profile and expanding middle class. Investment activity has been supported by ongoing infrastructure development and structural reforms designed to improve the business environment. However, the economy faces structural constraints that limit its potential growth trajectory, most notably a narrow revenue base constraining public investment capacity and relatively low per capita income of $4,925, which positions Indonesia in the lower-middle-income category despite its investment-grade sovereign ratings.

The new administration under President Prabowo Subianto, which assumed office in October 2024, has articulated ambitious growth targets of 8% annually. Whilst policy continuity has been maintained following the smooth political transition, achieving such elevated growth rates would require substantial acceleration beyond recent trends and successful implementation of comprehensive structural reforms. The government's ability to mobilise additional revenue, enhance infrastructure quality, and improve human capital development will prove critical determinants of whether Indonesia can shift to a higher growth trajectory whilst maintaining macroeconomic stability.

Inflation Trends and Price Stability

Indonesia has demonstrated commendable success in maintaining price stability, with inflation declining from a peak of 4.2% in 2022 to 2.3% in 2024. This performance reflects effective monetary policy management by Bank Indonesia, which has successfully navigated the global inflationary pressures that emerged following the pandemic and were subsequently exacerbated by commodity price volatility and supply chain disruptions. The central bank's inflation target range of 1.5% to 3.5% has provided a credible anchor for expectations, and inflation outcomes have remained well-controlled within this corridor.

The inflation trajectory shows a marked deceleration from the elevated levels of 2022, when global commodity prices surged and domestic demand recovered strongly. The moderation to 3.7% in 2023 and further decline to 2.3% in 2024 reflects both the normalisation of global supply conditions and the effectiveness of monetary policy tightening implemented during the previous cycle. Core inflation has remained relatively stable, suggesting that underlying price pressures have been contained despite periodic volatility in food and energy components.

Looking forward, inflation dynamics will be influenced by several factors including domestic demand conditions, global commodity price movements, and exchange rate developments. Indonesia's position as both a producer and consumer of key commodities creates complex transmission channels for external price shocks. The country's significant exports of palm oil, nickel, and coal mean that commodity price cycles affect both the terms of trade and domestic cost structures. Bank Indonesia's continued commitment to price stability, supported by appropriate fiscal coordination, should enable inflation to remain anchored within the target range, though vigilance will be required given Indonesia's vulnerability to commodity price volatility.

Monetary Policy Framework and Financial Conditions

Bank Indonesia has maintained a prudent and responsive monetary policy stance, adjusting policy settings to balance growth support with price stability objectives. The central bank's policy framework combines interest rate management with foreign exchange intervention and macroprudential measures to maintain financial stability. This multi-instrument approach has proven effective in navigating external shocks whilst preserving the rupiah's stability and ensuring adequate liquidity conditions for credit growth.

The accumulation of foreign exchange reserves to $155.7 billion by 2024, equivalent to 5.6 months of current account payments, provides substantial buffers against external volatility and enhances the central bank's capacity to smooth exchange rate fluctuations. This reserve adequacy has been a critical factor supporting Indonesia's investment-grade ratings, as it demonstrates the country's ability to meet external obligations and maintain confidence during periods of capital flow volatility. The reserves position compares favourably to regional peers and exceeds conventional adequacy metrics.

Financial sector resilience has been strengthened through ongoing regulatory reforms, including the Financial Sector Omnibus Law, which aims to deepen capital markets, enhance financial inclusion, and improve the regulatory architecture. The banking sector maintains solid capitalisation levels, manageable non-performing loan ratios, and adequate provisioning buffers. Credit growth has been supportive of economic activity without generating concerning imbalances, and the sector's exposure to external funding vulnerabilities remains limited given the predominantly domestic deposit base. These financial sector strengths provide an important foundation for sustained economic growth and enhance Indonesia's capacity to absorb potential shocks whilst maintaining macroeconomic stability.

Political and Institutional Assessment

Indonesia's political and institutional framework demonstrates considerable stability underpinned by well-established democratic processes and constitutional safeguards, though governance effectiveness remains constrained by structural weaknesses characteristic of emerging market economies. The smooth presidential transition in October 2024 to Prabowo Subianto, following his decisive electoral victory with 58.6% of the vote, reinforces the country's track record of peaceful democratic transfers of power since the reformasi era began in 1998. This continuity is particularly significant for sovereign creditworthiness, as President Prabowo has retained key economic policymakers from the previous Jokowi administration, including Finance Minister Sri Mulyani Indrawati, whose decade-long tenure has been instrumental in maintaining fiscal discipline and advancing revenue mobilisation reforms.

The institutional architecture supporting macroeconomic stability is robust, anchored by constitutional provisions that impose a fiscal deficit ceiling of 3% of GDP and a public debt limit of 60% of GDP. These constraints have proven effective in maintaining fiscal prudence even during crisis periods, with Indonesia successfully consolidating its deficit from the pandemic peak of 6.1% in 2020 to 2.3% by 2024, returning below the constitutional threshold ahead of schedule. Bank Indonesia operates with considerable independence, successfully navigating the challenging monetary policy environment of recent years by maintaining inflation within its 1.5-3.5% target range whilst preserving exchange rate stability through judicious foreign exchange interventions supported by reserves of $155.7 billion.

The legislative environment has demonstrated capacity for meaningful structural reform, evidenced by the passage of the Financial Sector Omnibus Law which consolidates regulatory oversight and strengthens the macroprudential framework. Parliament's approval of the new capital city project in Nusantara, alongside supporting infrastructure investments, reflects political consensus around long-term development priorities. However, the ambitious nature of President Prabowo's growth targets—aiming for 8% annual GDP expansion compared to the historical 5% trend—introduces policy execution risks, particularly given the substantial fiscal resources required for planned infrastructure, defence, and social programmes whilst maintaining deficit discipline.

Governance indicators present a mixed picture that constrains Indonesia's credit profile relative to higher-rated sovereigns. Whilst the country scores reasonably well on political stability and regulatory quality dimensions, perceptions of corruption and bureaucratic efficiency lag investment-grade peers in Northeast Asia and parts of Latin America. The decentralised administrative structure, whilst promoting local autonomy, creates coordination challenges for policy implementation and revenue collection. Government revenue mobilisation remains the most significant institutional weakness, with the tax-to-GDP ratio persistently around 10-11%, contributing to total government revenue of approximately 15% of GDP—substantially below the emerging market median of 25-30%. This narrow fiscal base limits the government's capacity to fund development priorities and respond to economic shocks, despite ongoing efforts to broaden the tax base through improved administration and compliance measures.

The legal and regulatory environment for business has improved incrementally through reforms such as the Omnibus Law on Job Creation, which streamlined investment procedures and labour regulations, though implementation challenges persist at subnational levels. Indonesia's strategic positioning within ASEAN and its active participation in multilateral forums including the G20 provide institutional anchors for policy credibility. The country's successful navigation of US tariff negotiations in 2025, securing the most favourable 19% rate among ASEAN economies through strategic concessions and diplomatic engagement, demonstrates sophisticated trade policy management and the government's capacity to protect national economic interests whilst maintaining constructive international relationships.

Looking forward, institutional capacity will be tested by the administration's ambitious development agenda, including the capital relocation project, downstream industrialisation initiatives in the nickel and palm oil sectors, and expansion of social protection programmes. The government's ability to mobilise additional revenues through tax reform, maintain fiscal discipline within constitutional constraints, and execute complex infrastructure projects will be critical determinants of Indonesia's medium-term credit trajectory. Political consensus around economic orthodoxy remains strong across major parties, providing reasonable confidence in policy continuity beyond the current administration's term through 2029.

Banking Sector & Financial Stability

Indonesia's banking sector demonstrates robust fundamentals that provide critical support to the sovereign credit profile, characterised by strong capitalisation, improving asset quality, and effective regulatory oversight. The sector has proven resilient through multiple stress episodes, including the pandemic-induced economic contraction and subsequent global monetary tightening, whilst maintaining its intermediation function to support economic growth.

The banking system's capital position remains well above regulatory requirements, with the aggregate Capital Adequacy Ratio standing at 26.8% as of December 2024, substantially exceeding the 8% Basel III minimum and Bank Indonesia's enhanced requirement of 10-14% depending on bank classification. This capital buffer provides significant loss absorption capacity and enables continued lending expansion to support the government's growth objectives. The sector's profitability has remained healthy, with Return on Assets averaging 2.3% and Return on Equity at 14.2% through 2024, reflecting efficient operations and disciplined risk management practices.

Asset quality metrics have shown consistent improvement following the pandemic-related deterioration. The Non-Performing Loan ratio declined to 2.1% by end-2024 from a peak of 3.2% in 2021, supported by economic recovery, corporate debt restructuring programmes, and proactive provisioning by banks. The Loan-to-Deposit Ratio has stabilised at approximately 78%, indicating balanced credit growth relative to deposit mobilisation and providing liquidity headroom for future lending expansion. Banks have maintained conservative provisioning practices, with coverage ratios exceeding 150%, which positions the sector well to absorb potential credit losses from economic volatility or external shocks.

Bank Indonesia's regulatory and supervisory framework has strengthened considerably over the past decade, incorporating macroprudential tools to address systemic risks and implementing Basel III standards ahead of many emerging market peers. The central bank has demonstrated effective crisis management capabilities, deploying targeted liquidity facilities and regulatory forbearance measures during the pandemic whilst maintaining financial stability. The Financial Sector Omnibus Law enacted in 2024 further enhances the regulatory architecture by consolidating oversight functions, strengthening resolution frameworks, and improving coordination between Bank Indonesia and the Financial Services Authority (OJK).

The banking sector's foreign currency exposure remains manageable, with aggregate net open positions well within prudential limits. Banks have reduced reliance on external wholesale funding, with foreign liabilities representing less than 10% of total funding, thereby limiting vulnerability to global financial market volatility. The sector's direct exposure to commodity-related lending, whilst significant given Indonesia's export structure, is diversified across multiple commodities and counterparties, with enhanced monitoring frameworks in place to manage concentration risks.

Digital transformation of the banking sector has accelerated, with mobile and internet banking penetration expanding rapidly and supporting financial inclusion objectives. This technological advancement enhances operational efficiency and revenue diversification whilst introducing new risks related to cybersecurity and operational resilience, which regulators are addressing through updated prudential standards. The emergence of financial technology companies has increased competition but also created partnership opportunities that extend banking services to previously underserved segments of the population.

Looking forward, the banking sector faces challenges from potential credit quality pressures if economic growth disappoints, interest rate volatility affecting net interest margins, and the need for continued investment in technology and human capital. However, the sector's strong fundamentals, prudent regulatory environment, and demonstrated adaptability position it as a continuing source of strength for Indonesia's sovereign credit profile, capable of supporting economic development objectives whilst maintaining financial stability through evolving domestic and external conditions.

Outlook & Scenarios

Short-Term Outlook (12 months)

Indonesia's credit profile is expected to remain stable through 2026, supported by continued economic expansion in the 5.0-5.3% range and sustained fiscal discipline. The government's commitment to maintaining the fiscal deficit below the 3% constitutional ceiling provides a strong anchor for debt sustainability, with the debt-to-GDP ratio projected to stabilise around 38-39% of GDP. Bank Indonesia's credible monetary policy framework should keep inflation within the 1.5-3.5% target range despite potential external price pressures from commodity markets and currency fluctuations. The central bank's foreign exchange reserves of $155.7 billion provide adequate buffers against short-term external shocks, equivalent to approximately 5.6 months of current account payments.

The negotiated 19% US tariff rate, whilst creating headwinds for specific export sectors, represents a manageable challenge given Indonesia's diversified export base and substantial trade surplus with the United States. The immediate impact on electronics, textiles, and footwear exports totalling approximately $8.5 billion annually will be partially offset by Indonesia's strategic positioning to capture manufacturing relocations from China. Domestic consumption, which accounts for approximately 55% of GDP, will continue to provide economic resilience alongside recovering investment activity. The government's infrastructure development programme and efforts to attract foreign direct investment through regulatory streamlining under the Financial Sector Omnibus Law should support growth momentum.

Key risks to the short-term outlook include potential volatility in global commodity prices, particularly for palm oil, nickel, and coal which constitute significant export revenues. A sharper-than-expected slowdown in China's economy could dampen demand for Indonesian commodities and reduce tourism receipts. Domestically, the new administration's ambitious spending plans must be carefully calibrated to avoid breaching fiscal targets, whilst implementation capacity for structural reforms will be tested as policy initiatives move from planning to execution phases.

Medium-Term Outlook (1-3 years)

Over the medium term, Indonesia's sovereign credit strength will be determined by progress on structural reforms addressing revenue mobilisation and institutional capacity constraints. The government's ability to broaden the tax base beyond the current narrow 15% of GDP will be critical for financing development needs whilst maintaining fiscal sustainability. Successful implementation of tax administration reforms and reduction of the informal economy could gradually lift revenue collection towards 16-17% of GDP by 2028, providing fiscal space for infrastructure investment and human capital development without compromising debt dynamics.

Economic growth is projected to average 5.0-5.3% annually through 2027-2028, supported by favourable demographics with a working-age population that continues to expand and urbanisation trends that drive productivity gains. The government's target of 8% growth appears optimistic given structural constraints including infrastructure gaps, skills mismatches in the labour market, and regulatory complexities that continue to affect the ease of doing business. More realistic growth outcomes in the 5-5.5% range would still support gradual income convergence, with GDP per capita rising from the current $4,925 towards $6,000-6,500 by 2028.

Indonesia's strategic positioning in global supply chain reconfiguration presents significant opportunities over this timeframe. The country's abundant natural resources, particularly nickel for electric vehicle batteries, position it favourably in the energy transition. Government policies promoting downstream processing and value addition in commodity sectors could enhance export sophistication and reduce vulnerability to price volatility. However, realising these opportunities requires continued improvements in infrastructure quality, regulatory predictability, and human capital development to compete effectively with regional peers for foreign investment.

The banking sector's resilience, with non-performing loan ratios below 3% and strong capitalisation, provides a stable foundation for credit intermediation supporting private sector growth. Continued financial sector deepening through implementation of the Financial Sector Omnibus Law should enhance access to finance for small and medium enterprises whilst maintaining prudential standards. External vulnerabilities remain manageable given the modest current account deficit projected at 0.5-1.0% of GDP, adequate foreign exchange reserves, and a diversified external funding base with lengthening debt maturity profiles.

Rating Scenarios

Upward rating pressure could emerge over the medium term if Indonesia demonstrates sustained progress on structural reforms that address current constraints. Specifically, successful revenue mobilisation efforts that lift government revenues above 16% of GDP on a sustained basis would enhance fiscal flexibility and reduce vulnerability to economic shocks. Meaningful improvements in governance indicators and institutional quality, as measured by World Bank and Transparency International metrics, would align Indonesia more closely with higher-rated investment-grade peers. Additionally, continued diversification of the export base towards higher value-added manufacturing and services, reducing dependence on commodity price cycles, would strengthen external resilience. Achievement of GDP growth consistently above 5.5% accompanied by rising GDP per capita towards $6,500-7,000 would support income convergence with higher-rated sovereigns.

Downward rating pressure would likely result from fiscal slippage that breaches the 3% constitutional deficit ceiling on a sustained basis or leads to a reversal in debt consolidation trends. A deterioration in the debt-to-GDP ratio above 42-43% of GDP, particularly if driven by revenue shortfalls rather than counter-cyclical measures, would raise sustainability concerns. Significant external shocks such as a sharp decline in commodity prices combined with capital outflow pressures that materially erode foreign exchange reserves below $130 billion would weaken external buffers. Policy missteps including reversal of structural reforms, weakening of central bank independence, or implementation of populist measures that undermine macroeconomic stability would also pressure the ratings. A pronounced slowdown in economic growth below 4% for an extended period, whether due to domestic policy failures or severe external headwinds, would constrain debt affordability and fiscal flexibility.

The stable outlook reflects the balanced assessment that upward and downward pressures are broadly matched over the next 12-18 months. The government's track record of fiscal discipline, credible monetary policy framework, and demonstrated capacity to navigate external challenges provide confidence in maintaining current credit quality. However, structural constraints including narrow revenue base, governance gaps, and commodity dependence limit near-term upside potential. The ratings could be affirmed with stable outlooks through 2026-2027 assuming continued policy discipline and steady progress on reform implementation, even if ambitious growth targets prove elusive.

Conclusion

Indonesia's sovereign credit profile reflects a balanced assessment of robust macroeconomic fundamentals tempered by structural constraints that limit upward rating momentum. The country's investment-grade status across all three major rating agencies, most recently reaffirmed by Moody's in March 2025, rests on a foundation of consistent economic performance, prudent fiscal management, and demonstrated resilience to external shocks. The stabilisation of GDP growth at approximately 5% annually, combined with a remarkably low government debt-to-GDP ratio of 38.8%, positions Indonesia favourably within its rating category and provides substantial policy flexibility to navigate future challenges.

The sovereign's creditworthiness is underpinned by several enduring strengths. Indonesia's large domestic economy, with GDP of $1.4 trillion and a population of 283 million, generates consumption-driven growth that reduces vulnerability to external demand fluctuations. The constitutional fiscal deficit ceiling of 3% of GDP has proven an effective anchor for fiscal discipline, whilst foreign exchange reserves of $155.7 billion, equivalent to 5.6 months of current account payments, provide adequate buffers against balance of payments pressures. The banking sector's strong capitalisation and limited exposure to foreign currency risks further enhance financial stability. Indonesia's successful navigation of US tariff negotiations, securing the lowest rate of 19% among ASEAN peers, demonstrates effective economic diplomacy and the government's capacity to manage trade tensions whilst maintaining strategic relationships.

Nevertheless, persistent structural weaknesses constrain the rating and limit prospects for near-term upgrades. The narrow government revenue base, at approximately 15% of GDP, remains significantly below investment-grade peers and restricts the state's capacity to fund infrastructure development and social programmes essential for long-term growth. Per capita income of $4,925 reflects Indonesia's lower-middle-income status and highlights the substantial development challenges ahead. The economy's dependence on commodity exports, particularly palm oil, nickel, and coal, creates vulnerability to global price cycles and complicates macroeconomic management. Governance indicators continue to lag higher-rated sovereigns, whilst infrastructure gaps and regulatory complexity impede private investment and productivity gains.

Looking forward, Indonesia's credit trajectory will be shaped by the government's ability to address these structural constraints whilst preserving macroeconomic stability. The smooth political transition to President Prabowo Subianto in October 2024 ensures policy continuity, though ambitious growth targets of 8% appear challenging given current capacity constraints and the global economic environment. Ongoing structural reforms, including implementation of the Financial Sector Omnibus Law and efforts to broaden the tax base, represent positive developments that could gradually strengthen the credit profile. Indonesia's strategic positioning to benefit from global supply chain diversification offers opportunities for export growth and foreign direct investment inflows, particularly in manufacturing sectors seeking alternatives to China-centric production networks.

The stable outlook assigned by all three rating agencies reflects expectations that Indonesia will maintain its current credit fundamentals over the medium term. Upward rating pressure would require sustained progress on revenue mobilisation, continued fiscal consolidation, and structural reforms that enhance productivity and reduce commodity dependence. Conversely, downside risks include fiscal slippage from ambitious spending programmes, external financing pressures from widening current account deficits, or policy missteps that undermine investor confidence. On balance, Indonesia's sovereign credit profile remains solid within the investment-grade spectrum, supported by prudent macroeconomic management and a large, diversified economy, whilst acknowledging that meaningful rating progression will require addressing deep-seated structural challenges through sustained reform implementation.