India

Executive Summary

India maintains a solid investment-grade sovereign credit profile underpinned by its position as the world's fastest-growing major economy, though this achievement is tempered by persistent fiscal vulnerabilities and elevated debt levels relative to emerging market peers. The country reached a significant milestone in August 2024 when S&P upgraded its rating to BBB from BBB-, marking the first upgrade in 18 years, whilst Moody's maintains its Baa3 rating and Fitch holds at BBB-. India's credit strengths derive from a large and diversified economic base, favourable demographic dynamics, successful digital infrastructure transformation, and a substantially improved banking sector with non-performing assets declining to historic lows of 2.6%. Real GDP growth of 6.5% in FY 2024-25, with projections to maintain similar momentum through FY 2025-26, demonstrates exceptional economic resilience amid global uncertainties. The nation's strategic positioning amid US-China geopolitical tensions creates opportunities for manufacturing relocation and export diversification, though risks from potential US tariffs and global trade fragmentation require careful navigation.

The current economic situation reflects sustained momentum across key indicators, with fiscal consolidation efforts progressing towards a targeted deficit of 4.9% of GDP in FY 2024-25, down from the pandemic peak of 9.2%. Infrastructure investment remains a central pillar of the government's growth strategy, with ₹11.11 trillion allocated for FY 2024-25, supporting both near-term demand and long-term productive capacity. The successful implementation of production-linked incentive schemes, particularly in electronics where iPhone production reached $10 billion in the first seven months of FY25, demonstrates India's growing manufacturing capabilities and integration into global supply chains. Foreign exchange reserves of $653.7 billion provide robust external buffers, whilst the current account deficit has narrowed to a manageable 0.7% of GDP, reflecting improved external resilience. Inflation has moderated to 4.85% with core inflation at 3.1%, allowing the Reserve Bank of India to adopt a neutral monetary policy stance that balances growth support with price stability objectives.

Significant challenges persist that constrain India's credit profile and limit the scope for near-term rating upgrades. Government debt levels, whilst showing improvement, remain elevated relative to BBB-rated peers, with debt affordability metrics constrained by substantial interest payment obligations. Infrastructure gaps continue to require massive investment across transport, energy, and urban development, placing ongoing demands on public finances. The transition to coalition governance under Prime Minister Modi's third term introduces new political dynamics that may moderate the pace of contentious structural reforms, though broad policy continuity appears assured. Weak debt affordability, reflected in high interest-to-revenue ratios, remains a key constraint highlighted by rating agencies, particularly Moody's. Additionally, India must navigate external headwinds including potential shifts in global trade policy, commodity price volatility, and tightening global financial conditions that could affect capital flows and external financing costs.

Looking ahead, India's sovereign credit trajectory appears cautiously positive, supported by sustained fiscal consolidation efforts, continued infrastructure-led growth, and structural reforms in manufacturing and digital governance. The government's commitment to reducing the fiscal deficit below 4.5% of GDP by FY 2025-26 provides a credible anchor for debt stabilisation, whilst tax reforms and improved compliance should support revenue enhancement. India's demographic dividend, with a median age of 28 years, offers substantial long-term growth potential if accompanied by investments in education, skills development, and job creation. The successful scaling of digital public infrastructure, including the Unified Payments Interface processing over 100 billion transactions annually, demonstrates India's capacity for transformative innovation. However, the pace of future rating upgrades will depend critically on demonstrable progress in fiscal consolidation, debt reduction, and the implementation of structural reforms that enhance productivity and competitiveness whilst managing the political economy constraints inherent in coalition governance.

Ratings Summary

India's sovereign credit profile reflects a consensus investment-grade assessment across the three major rating agencies, though with notable divergence in positioning within the BBB category. Standard & Poor's delivered a landmark upgrade in August 2024, raising India's rating to BBB from BBB- with a stable outlook—the first upgrade in 18 years—citing exceptional growth performance averaging 8.8% from FY22-FY24, the highest in the Asia-Pacific region. The agency emphasised India's sustained fiscal consolidation commitment, improved quality of public spending focused on infrastructure development, and strengthened corporate and financial balance sheets as key factors underpinning the upgrade decision. Fitch Ratings maintained its BBB- rating with stable outlook in August 2024, acknowledging India's strong medium-term growth prospects whilst expressing concerns about elevated fiscal deficits and high debt burden relative to BBB-range peers, noting that coalition politics may constrain major economic reforms but recognising positive momentum from infrastructure-driven growth and nascent manufacturing investment. Moody's Investors Service maintains the most conservative stance at Baa3, having last affirmed its rating in August 2023, acknowledging India's rapid economic growth and strengthened financial sector whilst citing persistent concerns about high debt burden, weak debt affordability, and rising domestic political risks. All three agencies identify continued fiscal consolidation progress and debt reduction as critical factors for potential future upgrades, with S&P projecting 6.5% GDP growth in FY26 and growth averaging 6.8% over the next three years supporting its more constructive view.

| Rating Agency | Current Rating | Outlook | Last Action Date |

|---|---|---|---|

| Standard & Poor's | BBB | Stable | 14 August 2024 |

| Moody's | Baa3 | Stable | 18 August 2023 |

| Fitch Ratings | BBB- | Stable | 29 August 2024 |

Economic Indicators

| Indicator | 2020 | 2021 | 2022 | 2023 | 2024 | 2025* | 2026* |

|---|---|---|---|---|---|---|---|

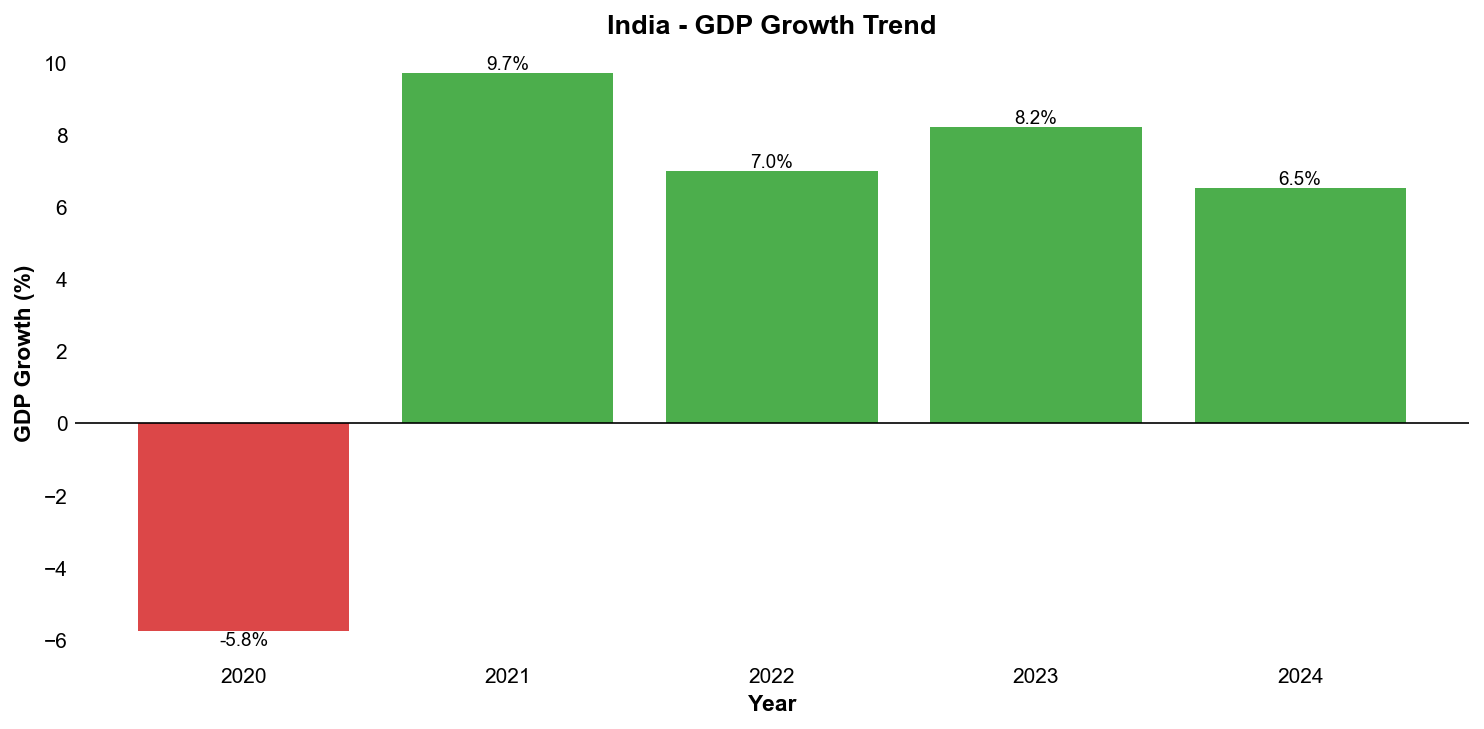

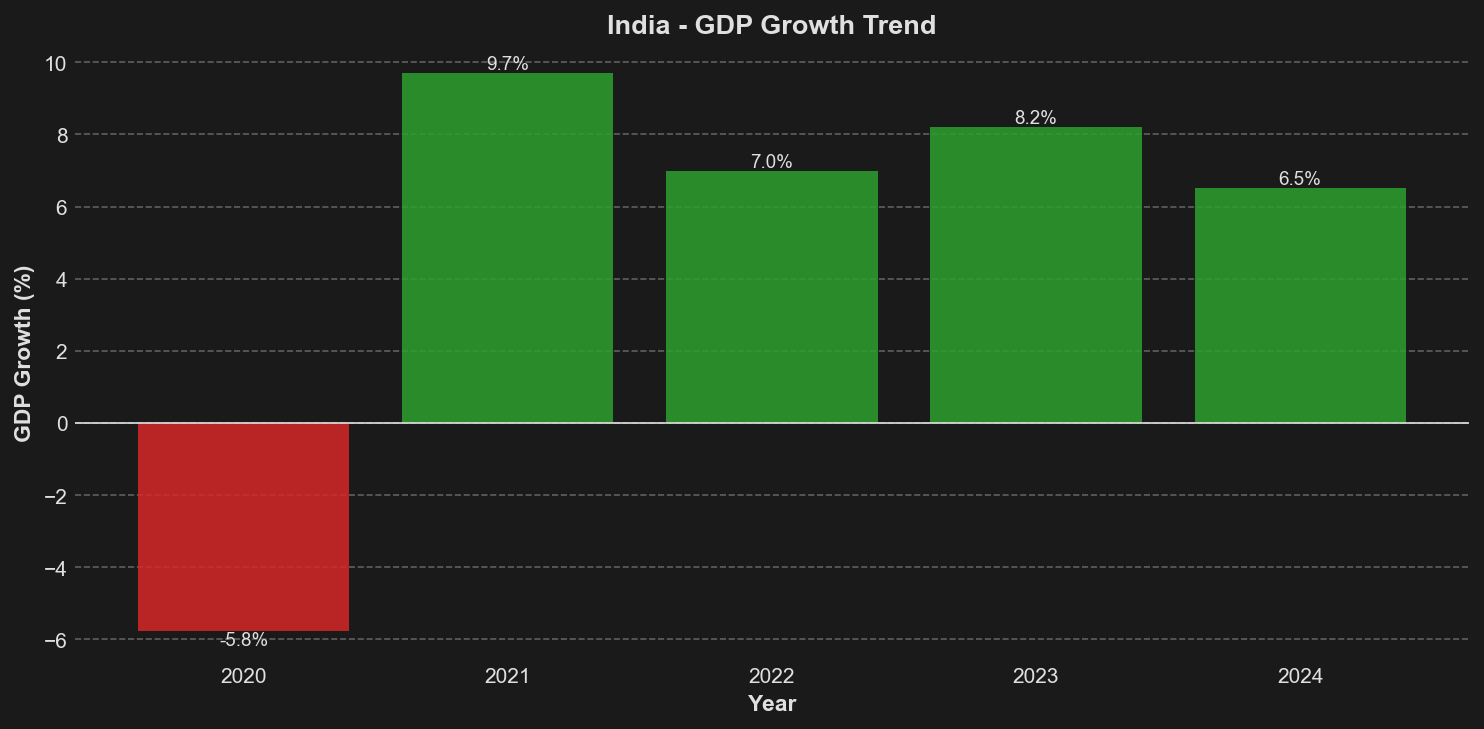

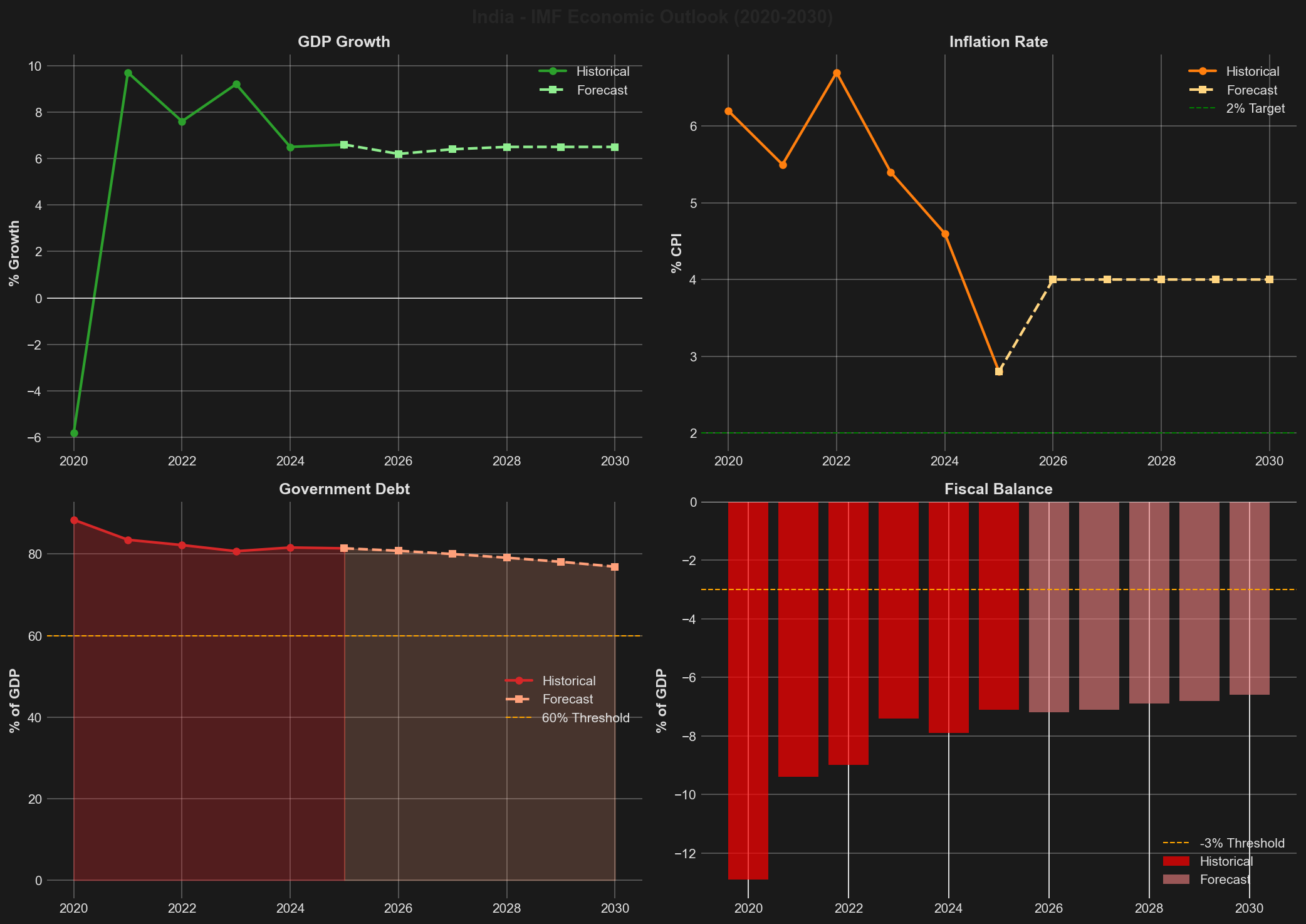

| GDP Growth (%) | -5.78 | 9.69 | 6.99 | 8.2 | 6.5 | 6.5 | 6.5 |

| Inflation (%) | 6.62 | 5.13 | 6.5 | 5.36 | 4.85 | 4.2 | 4.0 |

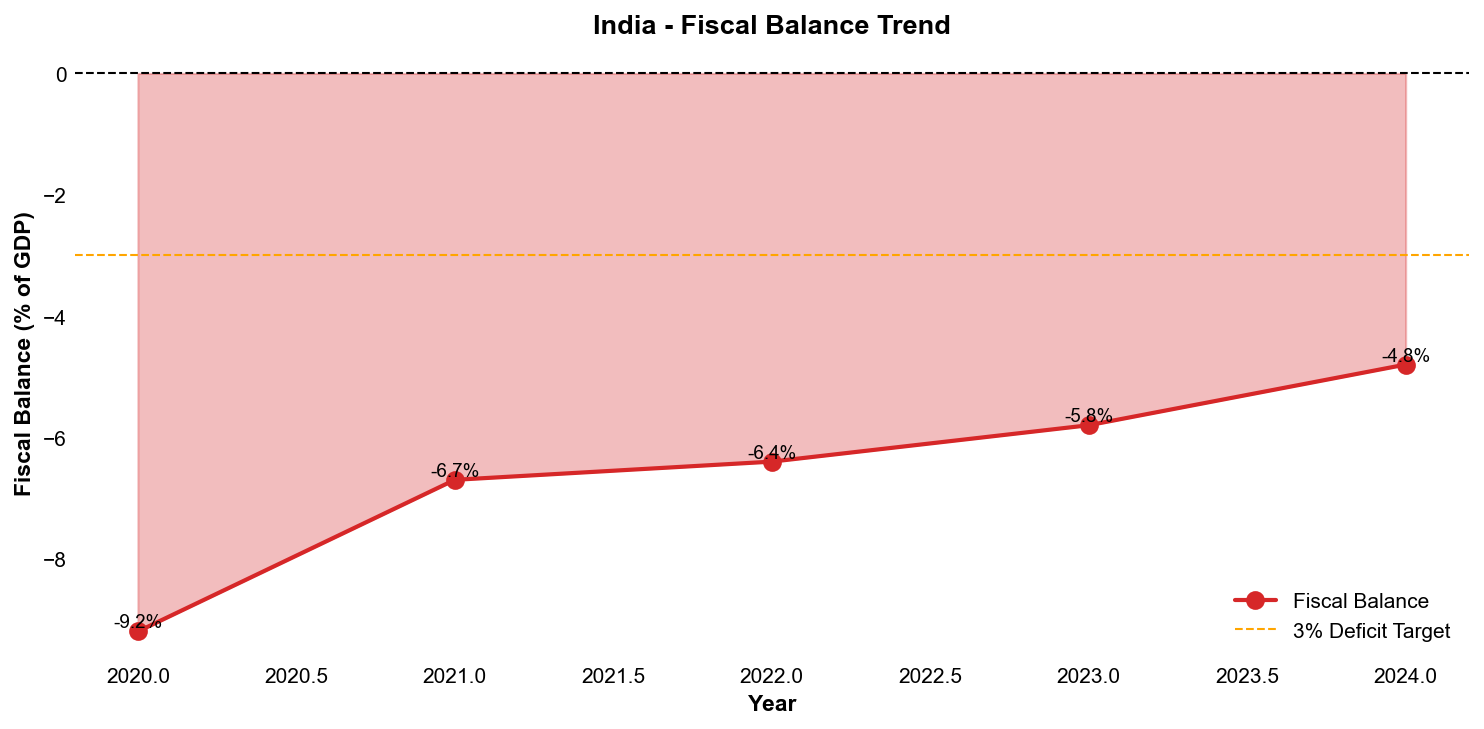

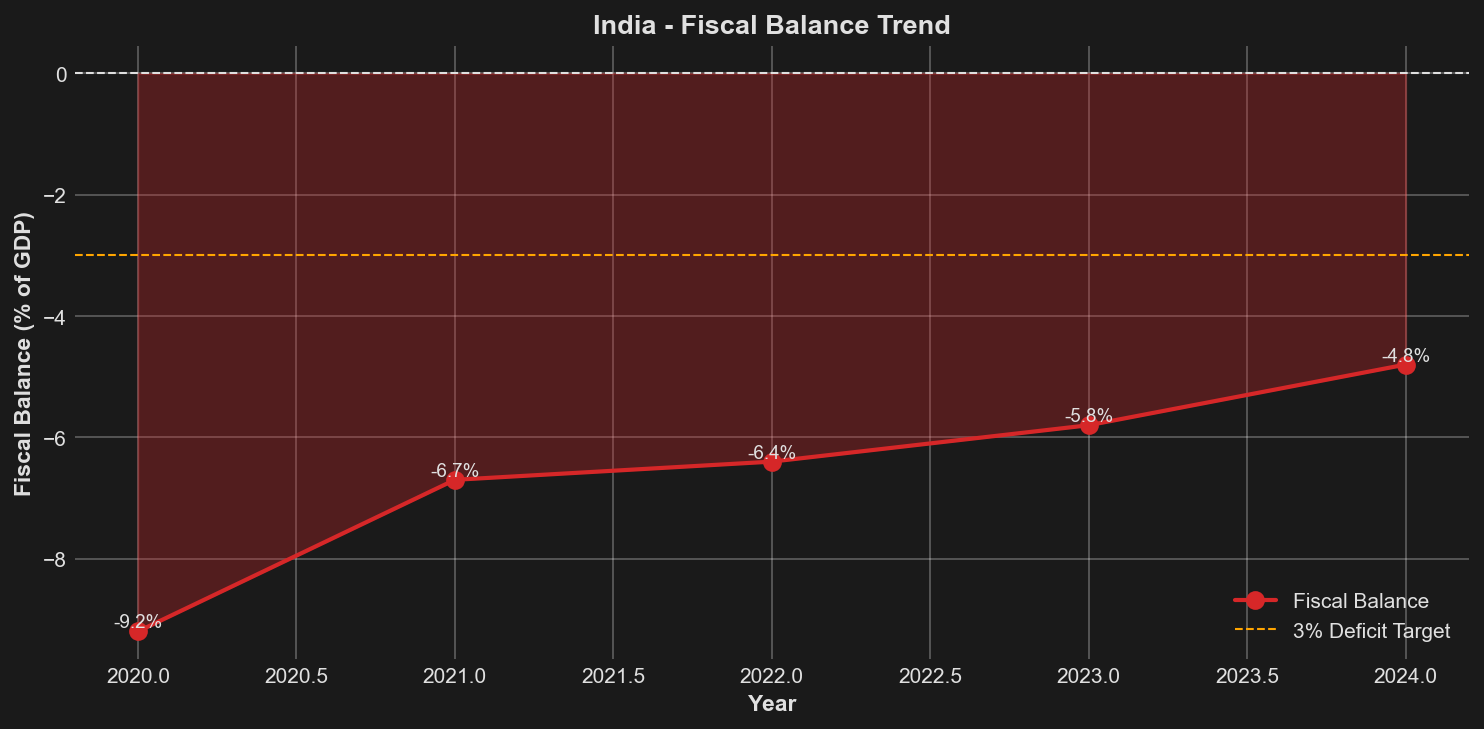

| Fiscal Balance (% GDP) | -9.2 | -6.7 | -6.4 | -5.8 | -4.8 | -5.5 | -6.0 |

| Government Debt (% GDP) | 89.5 | 85.0 | 83.0 | 81.6 | 81.2 | 79.5 | 78.0 |

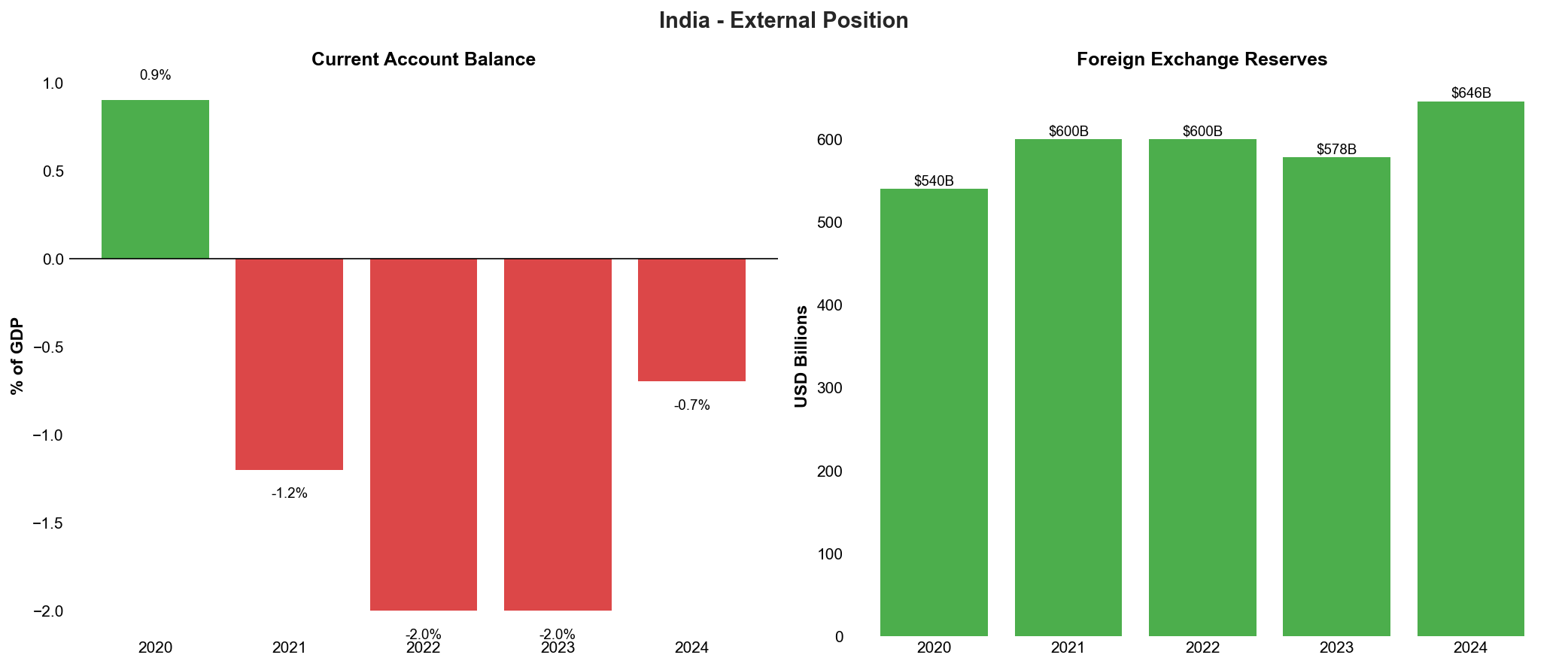

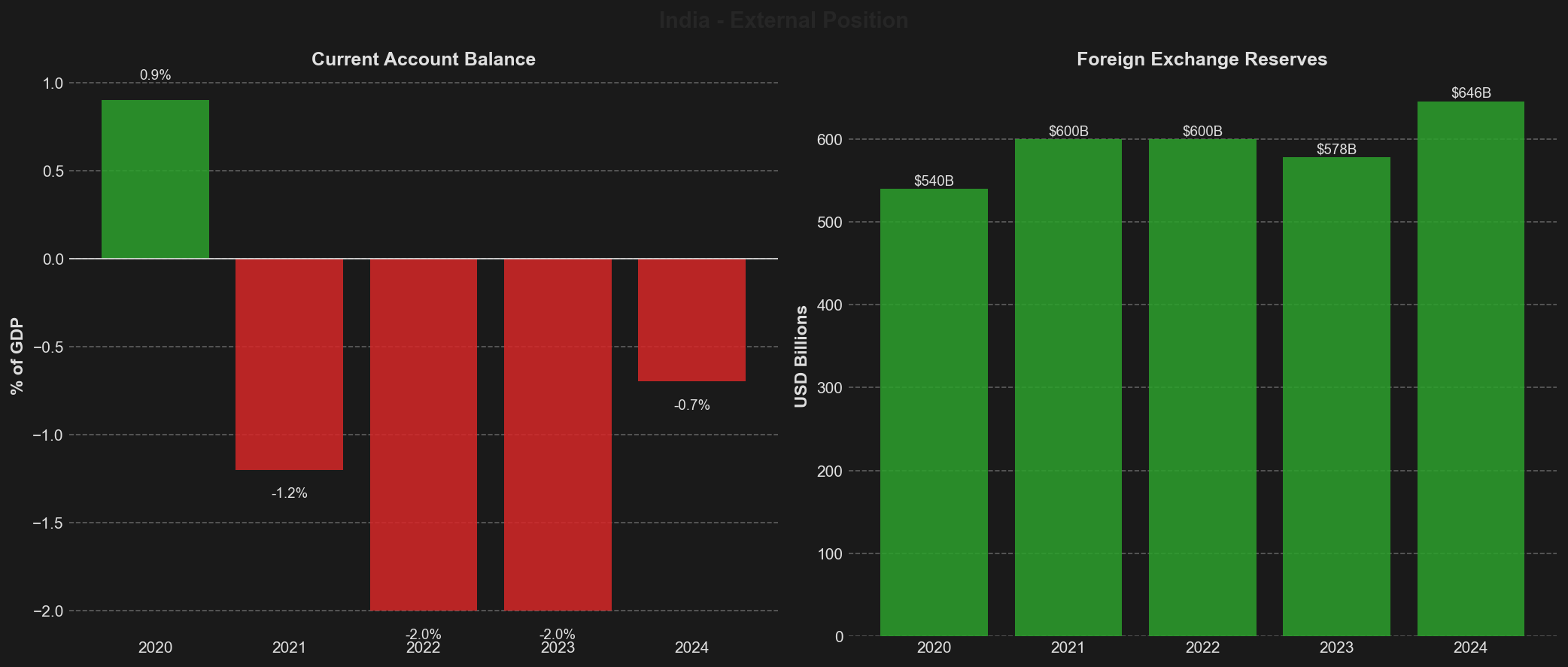

| Current Account (% GDP) | 0.9 | -1.2 | -2.0 | -2.0 | -0.7 | -1.2 | -1.5 |

*IMF forecast/estimate

India's economic indicators demonstrate a robust recovery trajectory following the pandemic-induced contraction of 2020, with GDP growth rebounding sharply to 9.69% in 2021 and subsequently stabilising at elevated levels averaging above 7% through 2023. The economy's resilience is particularly noteworthy given the challenging global environment characterised by geopolitical tensions, supply chain disruptions, and monetary tightening across major economies. Real GDP growth of 6.5% in FY 2024-25 positions India as the world's fastest-growing major economy, with the IMF projecting sustained growth at this level through 2026, underpinned by strong domestic demand, infrastructure investment, and nascent manufacturing sector expansion.

The fiscal consolidation path reveals credible commitment to restoring budgetary discipline following the pandemic-related fiscal expansion. The general government fiscal deficit has improved steadily from its peak of 9.2% of GDP in 2020 to 4.8% in 2024, reflecting both revenue buoyancy driven by economic recovery and expenditure rationalisation. However, the IMF projects a modest widening of the fiscal deficit to 5.5% in 2025 and 6.0% in 2026, suggesting challenges in maintaining the consolidation momentum amid competing demands for social spending, defence expenditure, and infrastructure investment. The government's commitment to achieving a fiscal deficit target of 4.5% of GDP by FY 2025-26 represents an ambitious objective that will require sustained revenue mobilisation efforts and expenditure discipline.

Government debt dynamics show gradual improvement, with the debt-to-GDP ratio declining from 89.5% in 2020 to 81.2% in 2024, reflecting the combined effects of nominal GDP growth, primary deficit reduction, and improved debt management. The IMF forecasts continued debt reduction to 78.0% by 2026, though this trajectory remains contingent upon sustained fiscal consolidation and robust economic growth. India's debt burden remains elevated relative to BBB-rated peers, representing a key constraint on sovereign creditworthiness and limiting fiscal space to respond to potential economic shocks. The composition of debt, predominantly domestic and rupee-denominated, mitigates refinancing and currency risks, though rising interest payments absorb approximately 20% of central government revenues, constraining developmental expenditure.

Inflation has moderated significantly from elevated levels of 6.5% in 2022 to 4.85% in 2024, with core inflation declining to 3.1%, reflecting the lagged effects of monetary tightening by the Reserve Bank of India and normalisation of global commodity prices. The IMF projects further disinflation to 4.0% by 2026, consistent with the RBI's medium-term inflation target of 4%. This benign inflation outlook provides scope for monetary policy normalisation, supporting credit growth and investment activity. However, risks to the inflation trajectory include volatile food prices, which constitute a significant component of the consumer price index, and potential external shocks from geopolitical developments or commodity market disruptions.

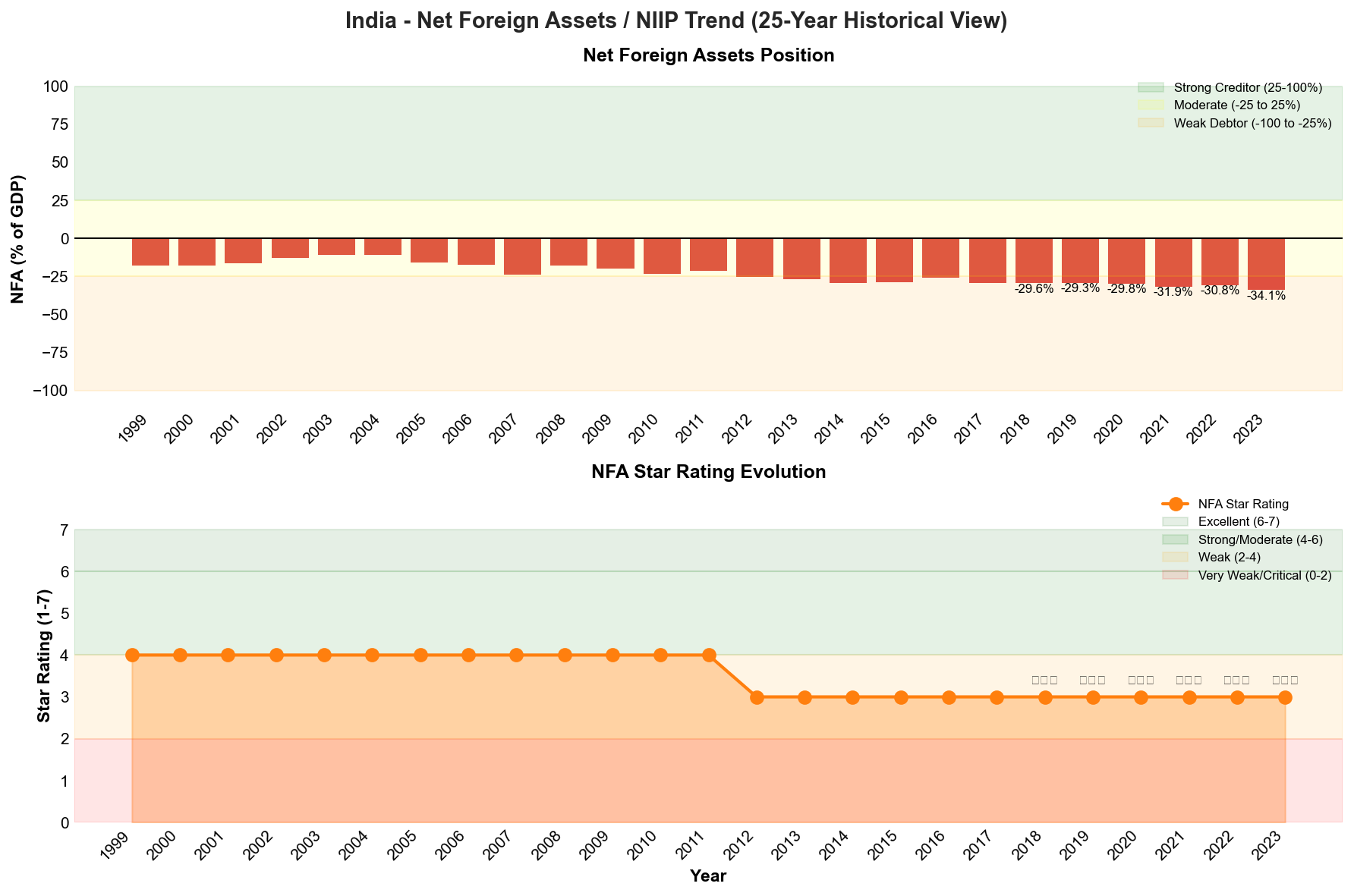

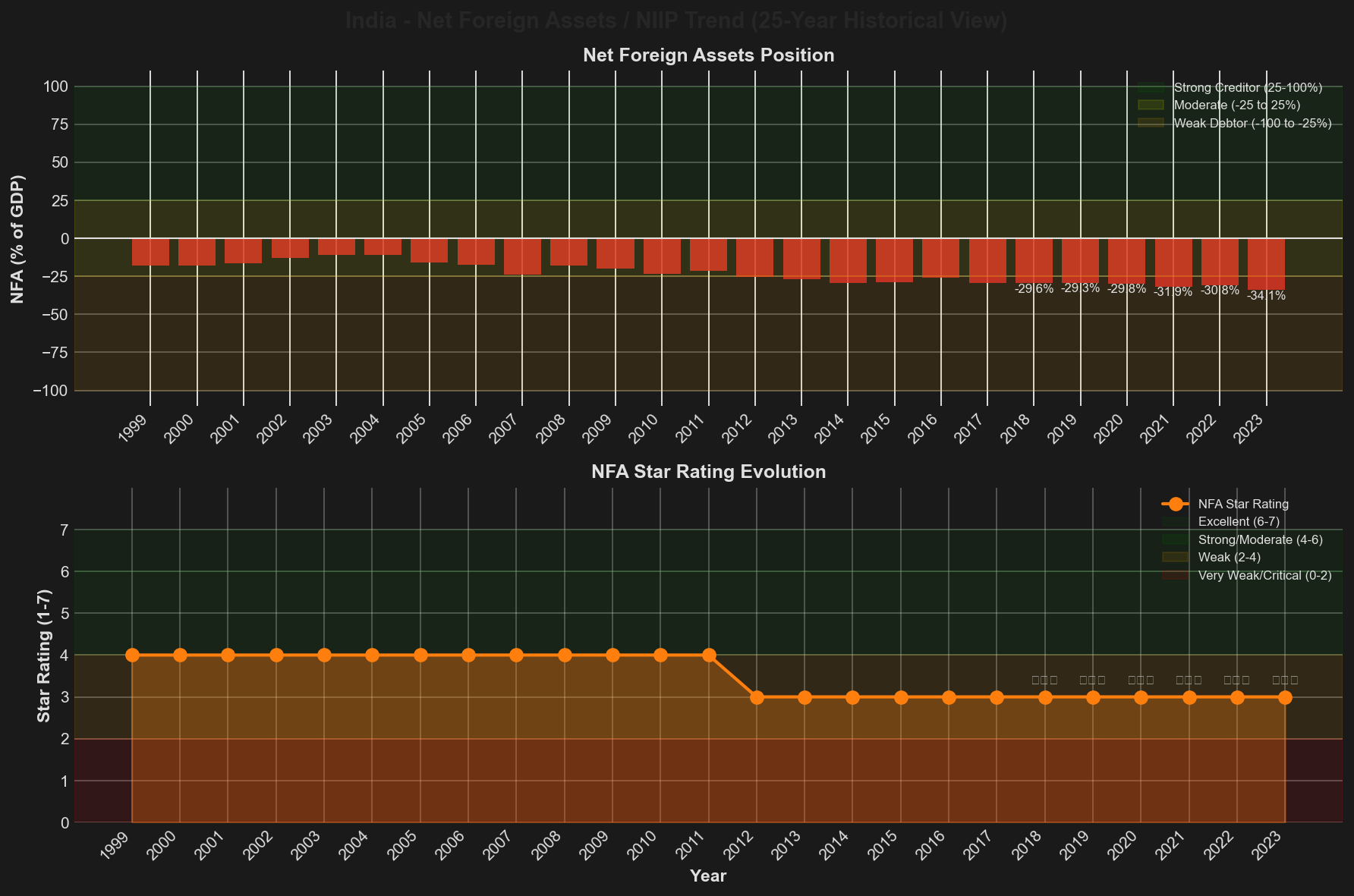

The current account balance has demonstrated considerable volatility, swinging from a surplus of 0.9% of GDP in 2020, driven by pandemic-related import compression, to deficits of 2.0% in 2022-2023 as domestic demand recovered and commodity prices surged. The narrowing of the current account deficit to 0.7% of GDP in 2024 reflects moderation in global energy prices, robust services exports, and resilient remittance inflows. The IMF projects a gradual widening to 1.5% of GDP by 2026 as import demand strengthens with economic expansion and investment activity accelerates. India's net foreign assets position stood at -34.1% of GDP in 2023, representing a weak debtor position that has deteriorated from -29.3% in 2019, reflecting cumulative current account deficits and valuation effects. This external liability position, whilst manageable given India's large domestic financing base and substantial foreign exchange reserves of $646 billion, represents a structural vulnerability that warrants monitoring, particularly in scenarios of capital flow reversals or external financing stress.

Net Foreign Assets & External Position

India's external position reflects the characteristics of a large emerging market economy with substantial financing needs to support its development trajectory, manifesting in a persistent net debtor position that has deepened modestly in recent years. As of 2023, India's net international investment position (NIIP) stood at -34.1% of GDP, representing a weak debtor position according to External Wealth of Nations database classifications, with the country maintaining a three-star rating (⭐⭐⭐) on a seven-point scale. This external liability position, whilst notable in absolute terms, remains manageable within the context of India's large and diversified economy, robust foreign exchange reserves, and the predominantly stable composition of external liabilities weighted towards foreign direct investment and concessional official financing rather than volatile portfolio flows or short-term debt.

The trajectory of India's net foreign asset position over the five-year period from 2019 to 2023 reveals a gradual deterioration, with the NIIP declining from -29.3% of GDP in 2019 to -34.1% in 2023, representing an approximate 4.8 percentage point weakening. This trend reflects India's sustained current account deficits during much of this period, particularly the elevated deficits of 2.0% of GDP recorded in both 2022 and 2023, driven by elevated commodity prices following Russia's invasion of Ukraine and strong domestic demand during the post-pandemic recovery phase. The deepening of the net debtor position accelerated notably between 2020 and 2021, when the NIIP deteriorated by 2.1 percentage points, coinciding with the economic recovery that drove import demand whilst export growth lagged. However, the external position has demonstrated resilience through maintaining its three-star rating throughout this period, indicating that whilst the debtor position has widened, it has remained within the "weak" category (-50% to -25% of GDP) without deteriorating into more concerning territory.

India's external vulnerability metrics present a mixed but broadly manageable picture, with substantial foreign exchange reserves providing a critical buffer against potential shocks. As of 2024, India's foreign exchange reserves stood at USD 646 billion, having recovered from the drawdown to USD 578 billion in 2023 when the Reserve Bank of India intervened to stabilise the rupee amid global monetary tightening and capital outflows. The 2024 reserve level represents approximately 11 months of import cover and exceeds 100% of external debt, providing comfortable liquidity buffers by conventional adequacy metrics. The current account deficit has narrowed substantially to 0.7% of GDP in 2024 from the elevated levels of 2.0% in the preceding two years, reflecting moderation in commodity prices, particularly crude oil, and resilient services exports driven by India's information technology and business process outsourcing sectors. This improvement in the current account balance, if sustained, should moderate the pace of NIIP deterioration going forward.

Composition and Quality of External Liabilities

The composition of India's external liabilities significantly mitigates risks associated with the net debtor position, with foreign direct investment representing the largest and most stable component of external financing. FDI inflows have remained robust, supported by India's large domestic market, improving ease of doing business rankings, and production-linked incentive schemes that have attracted manufacturing investment, particularly in electronics and renewable energy sectors. Portfolio investment flows, whilst more volatile, have stabilised following the turbulence of 2022-2023 when global monetary tightening triggered emerging market outflows. India's inclusion in global bond indices, including JP Morgan's emerging market bond index from June 2024, is expected to attract sustained portfolio inflows into government securities, providing a more stable investor base. External debt, whilst substantial in absolute terms at approximately USD 630 billion, remains moderate at roughly 19% of GDP, with the majority comprising longer-term obligations and a significant proportion denominated in rupees, reducing currency mismatch vulnerabilities.

Forward-Looking External Position Assessment

Looking ahead to 2025 and 2026, India's external position faces both supportive factors and emerging challenges that will shape the trajectory of the NIIP. The IMF projects India's current account deficit to remain contained, supported by sustained services export growth, remittance inflows that consistently exceed USD 100 billion annually, and government initiatives to boost merchandise exports through infrastructure improvements and trade agreements. However, the IMF's longer-term projections indicate fiscal deficits persisting at elevated levels, with the fiscal balance forecast at -6.6% of GDP by 2030, which may necessitate continued external financing and could constrain NIIP improvement. The government debt trajectory, projected to reach 76.9% of GDP by 2030 according to IMF forecasts, suggests that public sector external borrowing requirements may remain substantial, potentially limiting the pace of external position strengthening.

Structural factors provide grounds for cautious optimism regarding India's external sustainability despite the weak NIIP position. The country's demographic dividend, with a median age of 28 years, supports a high domestic savings rate that finances the majority of investment needs domestically, limiting dependence on external capital. The digital infrastructure transformation, exemplified by the Unified Payments Interface processing over 10 billion transactions monthly, enhances economic efficiency and supports services export competitiveness. Manufacturing sector development under production-linked incentive schemes, demonstrated by iPhone production reaching USD 10 billion in the first seven months of FY25, promises to diversify the export base beyond traditional services and reduce structural current account pressures over the medium term. Nevertheless, India's external position remains vulnerable to global risk-off episodes, commodity price shocks given continued energy import dependence, and potential capital flow reversals should global monetary conditions tighten unexpectedly or domestic reform momentum falter under coalition government dynamics.

The external financing environment presents both opportunities and risks as India navigates an increasingly fragmented global economic landscape. Geopolitical tensions between the United States and China create opportunities for India to attract supply chain diversification investments, potentially boosting FDI inflows and supporting current account improvement through enhanced manufacturing exports. However, the threat of increased US tariffs under protectionist policies and broader trade fragmentation could constrain export growth and complicate external financing. India's strategic balancing act, maintaining relationships with both Western economies and Russia whilst pursuing autonomous foreign policy objectives, provides diplomatic flexibility but introduces uncertainties regarding market access and investment flows. The country's strong foreign exchange reserves, equivalent to approximately 20% of GDP, provide substantial insurance against external shocks and afford policymakers time to implement adjustments should external conditions deteriorate, supporting the assessment that whilst India's net foreign asset position reflects structural weaknesses, the overall external position remains resilient and sustainable over the credit horizon.

Credit Strengths & Vulnerabilities

Strengths

India's sovereign credit profile is underpinned by a large and diversified economy that has demonstrated exceptional resilience and growth momentum. The country's position as the world's fastest-growing major economy reflects deep structural strengths, with real GDP growth averaging 8.8% from FY22-FY24, the highest performance in the Asia-Pacific region. This robust economic expansion is supported by a favourable demographic dividend, with a median age of 28 years providing a substantial and growing workforce that enhances long-term growth potential and supports domestic consumption dynamics.

The successful transformation of India's digital infrastructure represents a fundamental credit strength, with the implementation of unified payment interfaces, digital identity systems through Aadhaar, and widespread financial inclusion initiatives creating efficiency gains across the economy. This digital ecosystem has facilitated improved tax collection, reduced leakages in government transfers, and enhanced the business environment, contributing to sustained productivity improvements. The banking sector has undergone significant strengthening, with non-performing assets declining to historic lows of 2.6%, reflecting improved asset quality, enhanced regulatory oversight, and successful resolution mechanisms that have restored financial sector stability.

India's external position provides substantial resilience against global shocks, with foreign exchange reserves of $653.7 billion as of 2024 offering robust buffers equivalent to approximately one year of import cover. The current account deficit has narrowed considerably to a manageable 0.7% of GDP, supported by resilient services exports, particularly in information technology and business process outsourcing, alongside growing remittance inflows. The government's demonstrated commitment to fiscal consolidation, evidenced by the steady reduction in the fiscal deficit from pandemic peaks of 9.2% to a targeted 4.9% in FY 2024-25, reflects credible policy discipline that has been recognised by rating agencies, culminating in S&P's historic upgrade in August 2024.

The substantial infrastructure investment programme, with ₹11.11 trillion allocated for FY 2024-25, addresses critical bottlenecks whilst supporting near-term growth and enhancing long-term productive capacity. The successful implementation of production-linked incentive schemes has begun to demonstrate tangible results, particularly in electronics manufacturing where iPhone production reached $10 billion in the first seven months of FY25, signalling India's growing competitiveness in global manufacturing value chains. Strong corporate and financial balance sheets, improved following post-pandemic deleveraging and restructuring, provide a solid foundation for private sector investment and credit growth.

Vulnerabilities

Despite considerable strengths, India's sovereign credit profile faces persistent vulnerabilities centred on elevated government debt levels that remain high relative to peer emerging markets. Whilst fiscal consolidation efforts have progressed, the debt-to-GDP ratio, though showing improvement, continues to constrain fiscal flexibility and absorbs a significant portion of government revenues through debt service obligations. The quality of fiscal data and variations in measurement methodologies across different sources introduce uncertainty regarding the precise magnitude of public sector liabilities, particularly when considering off-balance-sheet obligations and contingent liabilities from state-owned enterprises.

Debt affordability remains a concern, with interest payments consuming a substantial share of government revenues, limiting resources available for critical development spending in health, education, and social protection. This constraint is particularly acute given India's low per capita income levels and substantial infrastructure gaps that require sustained public investment. The fiscal deficit, whilst on a declining trajectory, remains elevated compared to investment-grade peers, and the government's ability to maintain consolidation momentum faces challenges from competing spending pressures, including subsidies, defence expenditure, and social welfare programmes.

Infrastructure deficiencies persist across transport, power, urban services, and digital connectivity, requiring massive investment estimated at several trillion dollars over the coming decade. These gaps constrain productivity growth, increase logistics costs, and limit the economy's ability to fully capitalise on manufacturing opportunities. The banking sector, despite significant improvements, continues to face challenges from concentrated exposures, governance issues in some public sector banks, and potential asset quality pressures from highly leveraged corporate borrowers and stressed sectors.

Income inequality and regional disparities remain pronounced, with significant variations in development outcomes across states creating social tensions and complicating policy implementation. Labour market rigidities, land acquisition challenges, and regulatory complexities continue to impede business operations and foreign investment, despite reform efforts. The transition to coalition governance under Modi's third term introduces new political dynamics that may constrain the pace and scope of contentious structural reforms, particularly in areas such as labour laws, land reforms, and privatisation of state-owned enterprises.

Opportunities

India's strategic positioning amid evolving global trade dynamics presents substantial opportunities for economic advancement. The reconfiguration of supply chains driven by US-China tensions and the "China plus one" strategy adopted by multinational corporations creates scope for manufacturing relocation and export growth. India's large domestic market, improving business environment, and competitive labour costs position the country favourably to capture a greater share of global manufacturing, particularly in sectors such as electronics, pharmaceuticals, textiles, and automotive components.

The production-linked incentive schemes, if successfully scaled across additional sectors, could accelerate industrial development and employment generation whilst enhancing export competitiveness. The government's focus on infrastructure development, including the National Infrastructure Pipeline and dedicated freight corridors, promises to reduce logistics costs and improve connectivity, addressing long-standing constraints on manufacturing competitiveness. Continued digitalisation offers opportunities to enhance government service delivery, improve tax compliance, reduce corruption, and foster innovation in financial services and e-commerce.

Demographic advantages provide a sustained growth tailwind, with a young and increasingly educated workforce supporting consumption growth and offering potential for productivity gains through skill development initiatives. The expanding middle class, projected to grow substantially over the coming decade, creates opportunities for domestic market-oriented industries and services. India's strength in services exports, particularly technology services, business process outsourcing, and increasingly high-value professional services, offers diversified sources of foreign exchange earnings and employment generation for skilled workers.

The energy transition presents opportunities for India to leapfrog traditional development pathways through renewable energy deployment, with ambitious targets for solar and wind capacity offering potential for reduced energy import dependence and improved environmental outcomes. Financial sector deepening, including expanded credit penetration, development of corporate bond markets, and growth of institutional investors, could enhance resource mobilisation and allocation efficiency. Potential rating upgrades from Moody's and Fitch, following S&P's lead, would reduce borrowing costs and attract additional foreign investment flows.

Threats

India's credit outlook faces threats from multiple sources, both domestic and external. Global economic uncertainties, including potential recessions in advanced economies, could dampen export demand and foreign investment flows, whilst tightening global financial conditions may increase borrowing costs and trigger capital outflows from emerging markets. The threat of increased protectionism, particularly potential US tariffs under changing American trade policy, could disrupt India's export growth trajectory and complicate efforts to integrate into global manufacturing value chains.

Geopolitical tensions in the region, including border disputes and security challenges, necessitate elevated defence spending that constrains fiscal resources available for development priorities. Climate change poses significant risks through increased frequency and severity of extreme weather events, including droughts, floods, and heatwaves, which threaten agricultural productivity, infrastructure, and livelihoods, particularly for vulnerable populations. India's dependence on energy imports, despite growing renewable capacity, leaves the economy exposed to oil price volatility that can widen the current account deficit and fuel inflationary pressures.

Domestic political risks have increased with the transition to coalition governance, potentially constraining policy flexibility and complicating the implementation of necessary but politically sensitive reforms. Social tensions, including communal divisions and regional disparities, could escalate and disrupt economic activity whilst diverting policy attention from growth-enhancing measures. The risk of policy slippage on fiscal consolidation remains present, particularly in the face of electoral pressures, economic shocks, or demands for increased social spending.

Financial sector vulnerabilities, whilst reduced, persist in the form of concentrated exposures, governance challenges in public sector banks, and potential stress in non-banking financial companies. A sharp economic slowdown could trigger asset quality deterioration and impair credit growth, creating negative feedback loops. Regulatory uncertainties and retrospective policy changes have historically deterred foreign investment and could resurface, undermining investor confidence. The challenge of generating sufficient formal sector employment for India's growing workforce remains acute, with inadequate job creation potentially leading to social instability and constraining consumption growth. Implementation risks surrounding ambitious infrastructure and manufacturing initiatives could result in cost overruns, delays, and suboptimal outcomes that fail to deliver anticipated productivity gains.

Economic Analysis

Growth Dynamics and Structural Transformation

India's economic growth trajectory demonstrates remarkable resilience and structural strength, positioning the nation as the world's fastest-growing major economy despite challenging global conditions. The economy's performance through the mid-2020s reflects a fundamental shift from pandemic recovery to sustained expansion driven by domestic demand, infrastructure investment, and emerging manufacturing capabilities. Real GDP growth of 6.5% in FY 2024-25 represents a moderation from the exceptional 8.8% average achieved during FY22-FY24, yet remains substantially above both global averages and peer emerging market economies. This deceleration reflects a natural normalisation following the post-pandemic rebound rather than underlying weakness in economic fundamentals.

The composition of growth reveals increasingly balanced contributions across sectors, with services maintaining their traditional dominance whilst manufacturing demonstrates nascent but significant momentum. The successful implementation of production-linked incentive schemes has catalysed substantial manufacturing investment, particularly in electronics where iPhone production reached $10 billion in the first seven months of FY25, exemplifying India's growing integration into global supply chains. This manufacturing renaissance, whilst still in early stages, represents a critical diversification away from services-led growth and addresses longstanding concerns about employment generation and export competitiveness.

Infrastructure investment continues to serve as a primary growth engine, with the government allocating ₹11.11 trillion for FY 2024-25, representing approximately 3.4% of GDP. This sustained capital expenditure programme generates multiplier effects throughout the economy, enhancing productivity, reducing logistics costs, and creating conditions for private sector expansion. The quality of public spending has improved markedly, with greater emphasis on productive capital formation rather than current expenditure, a shift explicitly recognised by S&P in their August 2024 upgrade decision.

India's demographic dividend remains a fundamental structural advantage, with a median age of approximately 28 years providing a growing workforce and expanding consumer base. However, realising this potential requires continued focus on education, skill development, and employment generation, particularly in labour-intensive manufacturing and services sectors. The digital infrastructure transformation, exemplified by the Unified Payments Interface processing billions of transactions monthly, has created new economic opportunities and enhanced financial inclusion, supporting both consumption and entrepreneurship.

The transition to coalition governance under Modi's third term introduces new political dynamics that may influence the pace and nature of economic reforms. Whilst broad policy continuity appears assured, the need for coalition management may moderate the implementation of contentious structural reforms, particularly those affecting agricultural markets or labour regulations. Nevertheless, the fundamental commitment to fiscal consolidation, infrastructure investment, and manufacturing promotion appears intact across the political spectrum, providing reasonable confidence in policy stability.

Inflation Dynamics and Price Stability

India's inflation trajectory through 2024 and into 2025 reflects successful monetary policy management and favourable supply-side developments, with headline inflation moderating to 4.85% in 2024 from elevated levels experienced during 2022-23. This deceleration brings inflation comfortably within the Reserve Bank of India's target band of 2-6%, with the midpoint target of 4% increasingly within reach. Core inflation, excluding volatile food and fuel components, has declined more substantially to 3.1%, indicating diminishing demand-side pressures and well-anchored inflation expectations.

Food price dynamics, which constitute approximately 46% of the consumer price index, remain the primary source of inflation volatility given India's exposure to monsoon variability and agricultural supply shocks. The 2024 monsoon season delivered near-normal rainfall, supporting agricultural production and moderating food price pressures. However, structural vulnerabilities in agricultural supply chains, storage infrastructure, and distribution networks continue to generate periodic price spikes, particularly in perishable commodities. Government interventions through buffer stock management, minimum support prices, and targeted subsidies help moderate extreme price movements but introduce fiscal costs and potential market distortions.

Energy price transmission represents another critical inflation channel, with India importing approximately 85% of its crude oil requirements. Global oil price moderation through 2024, combined with the government's strategic petroleum reserve management and retail pricing mechanisms, has contributed to inflation deceleration. Nevertheless, India remains vulnerable to external energy price shocks, with potential implications for both inflation and the current account balance. The government's medium-term strategy emphasises renewable energy expansion and energy efficiency improvements to reduce this structural vulnerability.

Inflation expectations, as measured by household surveys and market-based indicators, have declined alongside actual inflation, reflecting credibility in the RBI's monetary policy framework. This anchoring of expectations provides the central bank with greater flexibility in policy response and reduces the output costs of maintaining price stability. The successful navigation of the 2022-23 inflation surge, when global commodity prices spiked following geopolitical disruptions, demonstrated the effectiveness of India's monetary policy framework and enhanced institutional credibility.

Monetary Policy Framework and Financial Conditions

The Reserve Bank of India's monetary policy stance has evolved substantially through 2024, transitioning from a prolonged tightening cycle to a neutral stance as inflation pressures moderated and growth concerns emerged. The policy repo rate, raised cumulatively by 250 basis points during 2022-23 to combat elevated inflation, has been maintained at restrictive levels through much of 2024, with the RBI prioritising inflation control over growth support. This disciplined approach, whilst imposing near-term growth costs, has successfully anchored inflation expectations and preserved monetary policy credibility.

The shift to a neutral policy stance in late 2024 reflects the RBI's assessment that inflation risks have diminished sufficiently to allow greater focus on growth support, particularly given signs of moderating domestic demand and global economic uncertainties. This recalibration provides scope for gradual policy rate reduction through 2025-26, supporting credit growth and investment activity whilst maintaining vigilance against inflation resurgence. The pace and magnitude of potential rate cuts will depend critically on inflation trajectory, global financial conditions, and exchange rate stability considerations.

Liquidity management has become increasingly sophisticated, with the RBI employing a range of instruments including open market operations, variable rate repo auctions, and standing facilities to maintain appropriate monetary conditions. The banking system has generally operated in modest liquidity deficit through 2024, consistent with the RBI's operational framework, with periodic liquidity injections ensuring smooth functioning of money markets. The development of deep and liquid government securities markets facilitates effective monetary policy transmission and provides the central bank with operational flexibility.

Credit growth to the commercial sector has moderated from elevated levels, reflecting both demand-side factors including higher interest rates and supply-side considerations including banks' risk management practices. Nevertheless, credit expansion remains supportive of economic activity, with particular strength in retail lending, infrastructure financing, and working capital provision to manufacturing enterprises. The banking sector's improved health, with non-performing assets declining to historic lows of 2.6%, enhances credit intermediation capacity and reduces financial stability risks that previously constrained monetary policy effectiveness.

Exchange rate management reflects the RBI's approach of allowing market determination whilst intervening to prevent excessive volatility and maintain adequate foreign exchange reserves. The rupee has experienced modest depreciation pressures through 2024, reflecting India's inflation differential with trading partners and periodic capital flow volatility. However, foreign exchange reserves of $653.7 billion, equivalent to approximately 11 months of imports, provide substantial buffers against external shocks and enhance confidence in exchange rate stability. The RBI's intervention strategy balances reserve accumulation objectives with avoiding excessive currency appreciation that might undermine export competitiveness.

The monetary policy framework's credibility has been reinforced by the RBI's operational independence, transparent communication, and consistent focus on its inflation mandate. The Monetary Policy Committee's regular assessments and forward guidance provide markets with clarity regarding policy intentions, reducing uncertainty and enhancing transmission effectiveness. This institutional strength represents a critical asset for India's macroeconomic management and sovereign credit profile, distinguishing the country from emerging market peers with less developed monetary frameworks.

Political & Institutional Assessment

India's political landscape has entered a new phase following the June 2024 general elections, which resulted in Prime Minister Narendra Modi securing a historic third consecutive term whilst simultaneously marking a significant shift in the country's governance structure. The Bharatiya Janata Party (BJP) fell short of an outright majority for the first time since 2014, securing 240 seats in the 543-member Lok Sabha, necessitating reliance on coalition partners within the National Democratic Alliance (NDA) to form government. This transition from single-party dominance to coalition governance introduces new political dynamics that carry implications for policy formulation, reform implementation, and the pace of structural transformation.

The coalition arrangement, whilst maintaining overall policy continuity, has introduced constraints on the government's ability to pursue contentious reforms that may face resistance from regional allies. Key coalition partners, including the Telugu Desam Party and Janata Dal (United), possess sufficient leverage to influence policy priorities, particularly on issues affecting their respective states. This political recalibration has manifested in a more consultative approach to governance, with the government demonstrating increased sensitivity to regional concerns and opposition viewpoints. The moderation in political approach may slow the implementation of ambitious structural reforms, particularly those requiring constitutional amendments or politically sensitive measures such as labour law reforms, land acquisition changes, or agricultural market liberalisation.

Despite these constraints, the Modi administration has maintained its core economic policy framework, with continued emphasis on infrastructure development, manufacturing promotion through production-linked incentive schemes, and digital transformation initiatives. The government's commitment to fiscal consolidation remains intact, as evidenced by the FY 2024-25 budget's deficit target of 4.9% of GDP, representing a measured reduction from the previous year's 5.6%. The administration has successfully navigated the coalition dynamics to secure parliamentary approval for key budgetary measures and maintain investor confidence in policy stability.

India's institutional framework demonstrates considerable strengths that underpin sovereign creditworthiness, though areas of concern persist. The Reserve Bank of India maintains operational independence and credibility in monetary policy formulation, having successfully anchored inflation expectations whilst supporting growth objectives. The central bank's inflation-targeting framework, established in 2016, has proven effective in maintaining price stability, with inflation moderating to 4.85% in 2024 from elevated levels in previous years. The RBI's shift to a neutral monetary policy stance in October 2024, followed by a 25-basis-point rate cut in February 2025, reflects its data-driven approach and responsiveness to evolving economic conditions.

The banking sector has undergone substantial strengthening, with non-performing asset ratios declining to historic lows of 2.6% as of September 2024, down from peaks exceeding 11% in 2018. This improvement reflects the success of the government's comprehensive approach to addressing legacy asset quality issues through the Insolvency and Bankruptcy Code, recapitalisation of public sector banks, and enhanced regulatory oversight. The financial sector's improved health provides a more robust foundation for credit intermediation and economic growth, reducing contingent liability risks to the sovereign balance sheet.

India's regulatory environment has evolved considerably, with significant improvements in ease of doing business metrics, though implementation challenges persist at state and local levels. The Goods and Services Tax, implemented in 2017, has matured into a more stable revenue framework, though compliance burdens and rate structure complexities continue to generate business concerns. The government's digital infrastructure initiatives, particularly the Unified Payments Interface and digital identity systems, have transformed service delivery and financial inclusion, demonstrating institutional capacity for large-scale technological implementation.

Governance challenges remain evident in several dimensions. Corruption perceptions, whilst improved from historical levels, continue to constrain India's institutional assessment relative to higher-rated peers. The World Bank's governance indicators place India in the 40th-50th percentile range across most dimensions, reflecting ongoing challenges in regulatory quality, rule of law, and control of corruption. Judicial system capacity constraints result in significant case backlogs, with over 45 million pending cases across various court levels, impeding contract enforcement and dispute resolution efficiency.

The federal structure of India's governance introduces complexity in policy implementation, with significant variation in institutional quality and reform progress across states. High-performing states such as Gujarat, Maharashtra, and Tamil Nadu demonstrate strong governance capacity and business-friendly environments, whilst several states lag considerably in infrastructure quality, regulatory efficiency, and fiscal management. This heterogeneity creates uneven investment climates and complicates national-level reform implementation, particularly in areas requiring state-level cooperation such as land acquisition, labour regulations, and agricultural marketing.

Political stability considerations extend beyond the immediate coalition dynamics to encompass longer-term questions about policy continuity beyond the current administration's tenure. The BJP's organisational strength and Prime Minister Modi's personal popularity provide reasonable assurance of political stability through the current term ending in 2029. However, the erosion of the party's electoral dominance and strengthening of opposition forces introduce greater uncertainty regarding the post-2029 political landscape and potential policy shifts.

India's strategic positioning in the evolving global geopolitical environment carries both opportunities and risks for sovereign credit assessment. The country's participation in multilateral forums such as the Quad and its growing strategic partnership with the United States reflect its rising international influence. Simultaneously, India maintains pragmatic engagement with Russia and pursues independent foreign policy positions, as evidenced by its approach to the Ukraine conflict. This strategic autonomy provides flexibility but occasionally generates tensions with major partners.

The government's institutional capacity for crisis management has been tested through the COVID-19 pandemic, during which India implemented one of the world's largest vaccination programmes, administering over 2.2 billion doses. This demonstrated significant logistical and administrative capabilities, though the second wave's severity in 2021 also revealed healthcare system vulnerabilities and coordination challenges. The experience has prompted increased focus on healthcare infrastructure investment and pandemic preparedness frameworks.

Looking forward, the political and institutional trajectory appears broadly supportive of sovereign creditworthiness, with established democratic institutions, policy continuity, and gradual institutional strengthening offsetting concerns about coalition constraints and governance challenges. The government's ability to maintain fiscal discipline whilst pursuing growth-supportive policies within the coalition framework will prove critical for sustaining positive credit momentum. Further institutional reforms addressing judicial efficiency, regulatory streamlining, and governance quality improvements would strengthen India's institutional assessment and support potential rating upgrades over the medium term.

Banking Sector & Financial Stability

India's banking sector has undergone a remarkable transformation over the past five years, emerging from a protracted period of asset quality stress to demonstrate robust health characterised by strong capitalisation, improved profitability, and historically low non-performing assets. The sector's resilience forms a critical pillar supporting India's investment-grade sovereign credit profile, with the financial system's stability providing essential foundations for sustained economic growth and credit intermediation to the productive economy.

The most striking indicator of the banking sector's recovery is the dramatic decline in non-performing assets, which reached historic lows of 2.6% of total advances as of March 2024, down from peaks exceeding 11% in 2018. This improvement reflects the combined impact of aggressive resolution efforts under the Insolvency and Bankruptcy Code, enhanced provisioning practices, strengthened underwriting standards, and robust economic growth facilitating corporate deleveraging. Public sector banks, which bore the brunt of the previous NPA cycle, have demonstrated particularly impressive asset quality improvements, with their gross NPA ratios declining to 3.9% from double-digit levels just five years prior. Private sector banks maintained their superior asset quality metrics with NPAs below 2%, whilst also expanding market share through aggressive retail lending and digital banking initiatives.

Capital adequacy across the Indian banking system remains comfortably above regulatory requirements, with the overall Capital Adequacy Ratio standing at 16.8% as of September 2024, well above the Basel III minimum of 11.5% including the capital conservation buffer. Public sector banks, following substantial government recapitalisation totalling over ₹3.5 trillion between 2017 and 2021, now maintain CAR levels averaging 14.6%, providing adequate buffers to support credit growth whilst absorbing potential shocks. The improved capitalisation has been complemented by enhanced profitability, with the banking sector's return on assets improving to 1.1% and return on equity reaching 13.2%, reflecting operating efficiency gains, lower credit costs, and improved net interest margins in a rising rate environment.

Credit growth has accelerated meaningfully, with bank lending expanding at approximately 16% year-on-year as of December 2024, driven by robust retail credit demand, working capital requirements from manufacturing sector expansion, and infrastructure financing aligned with government capital expenditure programmes. The composition of credit growth reflects healthy diversification, with retail loans growing at 18%, services sector credit at 15%, and industrial credit showing signs of revival at 9% growth after years of stagnation. Mortgage lending continues to dominate retail credit expansion, supported by favourable demographics, urbanisation trends, and government housing initiatives, though regulators have implemented prudential measures including increased risk weights on unsecured personal loans and credit card exposures to moderate exuberance in certain segments.

The Reserve Bank of India's supervisory framework has strengthened considerably, incorporating enhanced stress testing protocols, climate risk assessments, and cyber security requirements alongside traditional prudential oversight. The central bank's proactive approach to emerging risks is evidenced by targeted regulatory interventions, including restrictions on certain non-bank financial company activities, enhanced governance requirements for systemically important institutions, and guidelines on digital lending practices to protect consumer interests whilst fostering innovation. The RBI's macroprudential toolkit has expanded to include countercyclical capital buffers and sectoral exposure limits, providing flexibility to address potential vulnerabilities before they crystallise into systemic risks.

Non-bank financial companies, which experienced significant stress during 2018-2020 following the IL&FS default and subsequent liquidity crisis, have stabilised considerably with improved funding profiles, enhanced regulatory oversight, and selective consolidation that has strengthened the sector's overall resilience. The NBFC sector's asset quality metrics have normalised, with gross NPAs declining to 4.6%, whilst capital adequacy ratios have improved to 26.8% for deposit-taking NBFCs and 25.4% for systemically important non-deposit taking NBFCs. Regulatory reforms including scale-based supervision, enhanced governance standards, and liquidity risk management frameworks have addressed previous vulnerabilities, though the sector's interconnectedness with banks through funding channels requires continued supervisory vigilance.

Digital transformation represents a defining characteristic of India's financial sector evolution, with the Unified Payments Interface processing over 11 billion transactions monthly valued at ₹17 trillion as of December 2024, demonstrating unprecedented financial inclusion and transaction efficiency. The digital public infrastructure encompassing UPI, Aadhaar-based authentication, and the Account Aggregator framework has fundamentally altered financial services delivery, reducing transaction costs, expanding credit access to previously underserved segments, and fostering fintech innovation. Whilst digitalisation enhances efficiency and inclusion, it simultaneously introduces new risks including cyber security vulnerabilities, operational resilience challenges, and potential for rapid contagion during stress events, necessitating continuous regulatory adaptation and investment in technological safeguards.

Financial inclusion metrics have improved substantially, with 80% of adults now holding bank accounts compared to 35% a decade ago, facilitated by the Pradhan Mantri Jan Dhan Yojana and digital payment infrastructure. However, meaningful financial inclusion extending beyond basic account ownership to encompass credit access, insurance penetration, and investment participation remains incomplete, particularly in rural areas and among lower-income households. The government's continued focus on deepening financial inclusion through initiatives including credit guarantee schemes for micro and small enterprises, digital lending platforms, and financial literacy programmes supports both social objectives and financial sector development.

Looking forward, the banking sector faces several challenges that warrant careful monitoring despite its current strength. Rapid credit growth, particularly in unsecured retail segments, raises concerns about potential asset quality deterioration should economic conditions weaken or interest rates remain elevated for extended periods. Concentration risks persist, with exposure to certain sectors including commercial real estate and infrastructure requiring ongoing assessment. The transition to expected credit loss provisioning under Indian Accounting Standards convergent with IFRS 9 will test banks' risk management capabilities and potentially impact reported profitability. Climate-related financial risks, whilst not yet material, require proactive assessment and integration into risk management frameworks as India pursues its net-zero commitments whilst maintaining energy security during the transition period.

Nevertheless, the Indian banking sector's fundamental health represents a significant sovereign credit strength, contrasting favourably with the asset quality crises that constrained growth during 2015-2019. The sector's capacity to intermediate savings into productive investment, support government financing requirements, and withstand potential shocks provides essential underpinning for India's economic development trajectory and sovereign creditworthiness. Continued supervisory vigilance, prudent risk management practices, and gradual regulatory evolution to address emerging challenges should sustain the sector's resilience whilst supporting the financial intermediation necessary for India's growth ambitions.

Outlook & Scenarios

Short-Term Outlook (12 months)

India's near-term credit trajectory through early 2027 remains anchored by resilient economic fundamentals and sustained policy continuity, though navigating an increasingly complex global environment. Real GDP growth is projected to moderate to approximately 6.5% in FY 2025-26, reflecting the natural deceleration from the exceptional post-pandemic rebound whilst maintaining India's position as the fastest-growing major economy globally. This growth profile continues to be underpinned by robust domestic consumption supported by favourable demographics, steady infrastructure investment execution, and nascent manufacturing sector expansion through production-linked incentive schemes. The government's commitment to fiscal consolidation remains credible, with the FY 2025-26 budget targeting a deficit of 4.4% of GDP, representing continued progress towards the medium-term objective of sub-4.5% deficits. However, execution risks persist given the coalition government dynamics and potential pressures from state-level fiscal slippage.

Inflation dynamics present a balanced picture, with headline CPI inflation expected to remain within the Reserve Bank of India's tolerance band of 2-6%, averaging approximately 4.5% through 2026. The RBI's neutral monetary policy stance provides flexibility to respond to evolving domestic and external conditions, though global commodity price volatility and potential rupee depreciation pressures warrant close monitoring. The external sector position remains comfortable, with foreign exchange reserves maintaining adequate coverage of approximately 11 months of imports, providing substantial buffers against external shocks. The current account deficit is projected to widen modestly to 1.2-1.5% of GDP as domestic demand strengthens and commodity imports increase, though this remains well within sustainable thresholds. Capital flows continue to benefit from India's structural growth story and inclusion in global bond indices, though volatility associated with US monetary policy trajectory and geopolitical tensions introduces periodic pressure on the rupee.

The banking sector's health continues to improve, with non-performing asset ratios declining further from the historic lows of 2.6% achieved in 2024, supported by robust economic growth, improved credit underwriting standards, and resolution of legacy stressed assets. Credit growth remains healthy at 11-13%, supporting productive investment whilst maintaining prudent risk management. The coalition government's policy agenda demonstrates broad continuity with previous priorities, focusing on infrastructure development, manufacturing promotion, and digital public infrastructure expansion, though the pace of contentious structural reforms may moderate given the need for broader political consensus. Key near-term risks include potential escalation of global trade tensions, particularly regarding US tariff policies that could impact India's export competitiveness, domestic political uncertainties as coalition dynamics evolve, and weather-related disruptions to agricultural output affecting rural incomes and inflation.

Medium-Term Outlook (1-3 years)

India's medium-term sovereign credit profile through 2029 is characterised by sustained economic expansion, gradual fiscal consolidation, and structural transformation of the manufacturing base, positioning the economy for potential rating upgrades if key fiscal metrics continue improving. Real GDP growth is projected to average 6.5-7.0% annually over the three-year horizon, supported by several structural drivers including demographic dividends with a median age of 28 years, continued urbanisation creating consumption and investment opportunities, digital infrastructure enabling productivity gains across sectors, and manufacturing sector deepening through production-linked incentives and supply chain diversification. The government's ambitious infrastructure investment programme, averaging approximately ₹11-12 trillion annually, serves as both a near-term growth catalyst and medium-term productivity enhancer, improving logistics efficiency and reducing business costs. The successful scaling of electronics manufacturing, particularly in smartphones and components, demonstrates India's capacity to integrate into global value chains, with potential expansion into semiconductors, electric vehicles, and renewable energy equipment manufacturing.

Fiscal consolidation remains the critical determinant of India's rating trajectory over the medium term. The government's commitment to reducing the fiscal deficit below 4.5% of GDP by FY 2025-26 and further towards 3.0-3.5% by the end of the decade represents a credible path, though execution requires sustained discipline amidst competing expenditure pressures. The quality of fiscal adjustment matters significantly, with continued emphasis on capital expenditure over revenue spending supporting growth potential whilst improving long-term debt sustainability. General government debt-to-GDP ratios are projected to decline gradually from current levels towards 80% by 2029, contingent upon maintaining nominal GDP growth above effective interest rates and adhering to deficit targets. However, India's debt burden remains elevated relative to similarly-rated peers, with debt affordability metrics constrained by relatively low revenue mobilisation at approximately 17-18% of GDP. Tax reforms including GST rate rationalisation and base broadening, alongside disinvestment proceeds and improved tax compliance through digitalisation, provide avenues for revenue enhancement without compromising growth.

The external sector outlook remains manageable despite modest current account deficits projected at 1.5-2.0% of GDP through the medium term. India's services exports, particularly in information technology, business services, and tourism, provide substantial offsetting inflows, whilst remittances from the Indian diaspora contribute approximately $100-110 billion annually. Foreign direct investment flows targeting manufacturing, digital infrastructure, and renewable energy sectors are expected to remain robust, supported by India's large domestic market, improving ease of doing business, and geopolitical positioning as companies diversify supply chains. External debt metrics remain comfortable with external debt-to-GDP ratios below 20% and predominantly long-term in nature, limiting rollover risks. The rupee's exchange rate trajectory reflects India's inflation differential with trading partners and evolving terms of trade, with gradual depreciation pressures balanced by capital inflows and RBI intervention maintaining orderly market conditions.

Rating Scenarios

India's sovereign rating trajectory over the next 12-36 months presents asymmetric possibilities, with greater probability of maintaining current ratings than either upgrade or downgrade scenarios, though the positive momentum from S&P's 2024 upgrade creates potential for further rating actions if fiscal consolidation accelerates beyond current projections.

An upgrade scenario, with probability estimated at 25-30% over the medium term, would require demonstrable progress on several fronts simultaneously. Most critically, sustained fiscal consolidation delivering general government deficits below 4.0% of GDP and placing the debt-to-GDP ratio on a firm downward trajectory towards 75% would address rating agencies' primary concern regarding India's elevated debt burden relative to peers. This would necessitate revenue mobilisation improvements through tax reforms, expenditure rationalisation particularly in subsidies, and maintaining capital expenditure discipline whilst avoiding populist spending pressures. Additionally, an upgrade scenario would benefit from continued strong GDP growth averaging above 7.0% annually, demonstrating India's capacity to grow out of its debt burden whilst creating fiscal space. Successful implementation of structural reforms including land and labour market liberalisation, further financial sector strengthening, and manufacturing sector deepening would enhance medium-term growth potential and economic resilience. Improved governance indicators, reduced political polarisation, and strengthened institutional frameworks would address concerns about policy predictability and implementation capacity. The sequencing of potential upgrades would likely see Moody's moving first from Baa3 to Baa2, aligning with S&P and Fitch, before any further upgrades across agencies.

The baseline scenario, with probability estimated at 60-65%, assumes continued rating affirmation at current levels with stable outlooks maintained across all three major agencies. This scenario incorporates steady fiscal consolidation progress towards the 4.4-4.5% deficit target, real GDP growth moderating to 6.5-6.8% range as the economy matures, inflation remaining within the RBI's target band allowing accommodative monetary policy when needed, and external sector stability with manageable current account deficits and adequate reserve buffers. The baseline assumes policy continuity under coalition governance with infrastructure investment maintained and gradual progress on manufacturing initiatives, though without breakthrough reforms. Banking sector health continues improving with NPAs remaining below 3.0% and credit growth supporting economic expansion. Global conditions in this scenario feature moderate growth, contained trade tensions, and gradual normalisation of monetary policies in advanced economies without triggering emerging market stress. This scenario reflects rating agencies' current assessment that India's credit strengths including robust growth, large diversified economy, and improving financial sector balance the weaknesses of elevated debt burden and modest revenue mobilisation.

A downgrade scenario, with probability estimated at 10-15%, would require significant deterioration across multiple dimensions or materialisation of severe external shocks. Fiscal slippage represents the primary downgrade trigger, particularly if deficits remain persistently above 5.5% of GDP due to populist spending pressures, revenue shortfalls, or state-level fiscal deterioration, placing the debt-to-GDP ratio on an upward trajectory. Sharp economic growth deceleration below 5.0% annually, whether from domestic policy missteps, financial sector stress, or global recession, would undermine debt sustainability and fiscal consolidation capacity. External sector stress manifesting through current account deficits widening beyond 3.0% of GDP, capital flow reversals, or significant reserve depletion would raise concerns about external vulnerability. Banking sector deterioration with NPAs rising above 5.0% due to credit quality problems or economic slowdown would threaten financial stability and require fiscal support. Severe political instability, policy paralysis, or reversal of economic reforms would undermine investor confidence and growth prospects. Global risk factors including major trade wars directly impacting India's exports, oil price spikes significantly widening the current account deficit, or emerging market contagion from crises elsewhere could trigger reassessment of India's resilience. The downgrade path would likely begin with outlook revisions to negative before actual rating actions, providing policy authorities opportunity to implement corrective measures.

Critical factors that rating agencies will monitor closely over the coming quarters include monthly fiscal deficit data and adherence to budgeted targets, quarterly GDP growth releases and sectoral composition, inflation trends and monetary policy responses, current account balance evolution and reserve adequacy, banking sector asset quality indicators and credit growth patterns, progress on structural reforms including privatisation and labour market changes, political developments affecting policy continuity and reform momentum, and global economic conditions including trade policy changes and commodity prices. The government's budget presentations for FY 2026-27 and beyond will provide crucial signals regarding medium-term fiscal strategy and commitment to consolidation. State election outcomes and coalition management will influence reform capacity and spending discipline. External developments including US-China relations, global trade architecture evolution, and advanced economy monetary policies will shape India's external environment and capital flow dynamics.

Conclusion

India's sovereign credit profile reflects a compelling narrative of structural transformation underpinned by robust economic fundamentals, though tempered by persistent fiscal vulnerabilities that constrain its rating trajectory. The country's investment-grade status, reinforced by S&P's historic upgrade to BBB in August 2024, recognises the exceptional growth performance that has positioned India as the world's fastest-growing major economy. With real GDP growth projected to sustain at 6.5% through FY 2025-26 and averaging 6.8% over the medium term, India demonstrates remarkable economic resilience that distinguishes it from both advanced and emerging market peers.

The credit strengths supporting India's rating are multifaceted and deeply embedded in the economy's structural characteristics. The large and diversified economic base, with nominal GDP exceeding $3.7 trillion, provides inherent stability and reduces vulnerability to sector-specific shocks. The demographic dividend, characterised by a median age of 28 years and a workforce that continues to expand, offers sustained potential for productivity gains and consumption-driven growth. India's digital infrastructure transformation, exemplified by the Unified Payments Interface processing over 100 billion transactions annually, has fundamentally altered the efficiency of economic transactions whilst enhancing financial inclusion. The banking sector's rehabilitation, with non-performing assets declining to historic lows of 2.6%, represents a critical achievement that strengthens the financial system's capacity to support economic expansion.

However, material credit constraints persist and warrant careful monitoring. The fiscal deficit, whilst on a consolidation path targeting 4.9% of GDP in FY 2024-25, remains elevated relative to rating category peers. Government debt levels, though subject to measurement variations across sources, constitute a significant burden that limits fiscal flexibility and absorbs substantial resources for debt servicing. Infrastructure deficiencies, despite the ambitious ₹11.11 trillion allocation for FY 2024-25, continue to constrain productivity and require sustained investment over multiple years. The transition to coalition governance under Modi's third term introduces political dynamics that may moderate the pace of contentious structural reforms, though broad policy continuity appears assured.

India's external position provides a robust buffer against global volatility, with foreign exchange reserves of $653.7 billion offering substantial import cover and the current account deficit compressed to a manageable 0.7% of GDP. The strategic positioning amid US-China geopolitical tensions creates opportunities for manufacturing relocation, evidenced by iPhone production reaching $10 billion in the first seven months of FY25 under production-linked incentive schemes. Nevertheless, risks from potential US tariffs, global trade fragmentation, and commodity price volatility require vigilant policy responses.

The sovereign credit trajectory appears constructive over the medium term, contingent upon sustained fiscal consolidation, continued infrastructure investment, and successful implementation of manufacturing and digital governance reforms. Progress towards reducing the debt-to-GDP ratio and improving debt affordability metrics remains critical for potential rating upgrades from Moody's and Fitch. The successful execution of fiscal targets, maintenance of macroeconomic stability, and navigation of coalition governance dynamics will determine whether India can build upon S&P's upgrade momentum and achieve broader rating recognition of its economic transformation. Whilst challenges remain substantial, India's fundamental credit strengths and demonstrated policy commitment provide a solid foundation for maintaining and potentially enhancing its investment-grade sovereign credit profile.