Hungary

Executive Summary

Hungary maintains investment-grade sovereign credit ratings at the lowest tier (BBB-/Baa2/BBB), with two of three major rating agencies assigning negative outlooks that signal elevated downgrade risk. The country's credit profile reflects a fundamental tension between robust economic fundamentals—including exceptional banking sector capitalisation (20.5% capital adequacy ratio), a healthy current account surplus (2.3% of GDP), and substantial foreign exchange reserves (€46.3 billion)—and systematic governance failures that have triggered unprecedented punitive measures from the European Union. Hungary ranks as the EU's most corrupt member state for the third consecutive year, with a Transparency International score of 41/100 placing it alongside Morocco and Tanzania globally. This governance deficit has resulted in €19 billion in frozen EU funds representing 34.8% of 2023 government revenue, whilst the country permanently forfeited €1 billion in EU funds in January 2025, marking the first such loss in EU history.

The Hungarian economy faces acute near-term headwinds from multiple directions. Growth has stagnated over the past three years with cumulative real expansion near zero, whilst escalating US trade tariffs averaging 18.8% on Hungarian exports threaten to reduce GDP by 1.4-2.3% in 2025. The automotive sector, which represents 40% of exports to the United States and employs tens of thousands domestically, confronts particularly severe pressure from 25% vehicle tariffs. These external shocks compound domestic fiscal challenges, with interest costs projected to exceed 4% of GDP in 2025—representing 11.9% of government revenues—whilst pre-election spending ahead of the 2026 parliamentary elections is expected to push the fiscal deficit to 4.5% of GDP, well above government targets. Hungary's strategic pivot towards Chinese investment, now comprising 80% of new foreign direct investment, offers partial mitigation of Western funding constraints but introduces new dependencies and further complicates relations with traditional European and transatlantic partners.

The forward outlook remains contingent on Hungary's ability to navigate competing pressures from governance reform requirements, trade policy developments, and domestic political dynamics. Rating agencies project modest recovery in 2026, with growth estimates ranging from 1.9% to 3.0%, predicated on easing trade tensions and potential policy shifts following the 2026 elections. However, Hungary faces the imminent risk of losing substantial Recovery and Resilience Facility resources—equivalent to 5% of GDP—if it fails to meet 27 super-conditions before the end-2026 deadline, a prospect that agencies view with considerable scepticism given the country's track record on governance reforms. The combination of constrained fiscal space, elevated interest burdens, frozen EU funds, and external demand weakness creates a challenging environment for sustainable growth acceleration, whilst the negative outlooks from Standard & Poor's and Moody's underscore the material risk of downgrade to sub-investment grade should fiscal consolidation falter or governance deterioration continue.

Ratings Summary

Hungary maintains investment-grade status across all three major rating agencies, positioned at the lowest tier with ratings of BBB-/Baa2/BBB, though deteriorating outlooks signal mounting downgrade risk. Standard & Poor's rates Hungary at BBB- with a negative outlook as of April 2025, placing the sovereign just one notch above speculative grade. The agency revised its outlook from stable to negative in April 2025, citing concerns about pre-election fiscal spending ahead of the 2026 parliamentary elections, with projected deficits of 4.5% of GDP exceeding government targets and interest costs projected to surpass 4% of GDP in 2025—representing 11.9% of government revenues. Moody's Investors Service assigns a Baa2 rating with negative outlook, having revised its assessment in November 2024 driven by institutional and governance weaknesses alongside the elevated risk of losing substantial EU grants and loans totalling approximately 5% of GDP if Hungary fails to meet conditions for accessing Recovery and Resilience Facility resources. The agency also highlights Hungary's vulnerability to weak German economic performance, which poses particular risks to the vehicle industry heavily integrated into German supply chains. Only Fitch Ratings maintains a stable outlook with its BBB rating, having upgraded from negative in December 2024 based on the government's fiscal consolidation efforts and strong employment levels. The divergence in agency outlooks reflects different weighting of Hungary's near-term fiscal pressures versus medium-term institutional challenges, with two of three agencies signalling heightened concern about the sovereign's credit trajectory.

| Rating Agency | Current Rating | Outlook | Last Action Date |

|---|---|---|---|

| S&P Global Ratings | BBB- | Negative | April 11, 2025 |

| Moody's Investors Service | Baa2 | Negative | November 29, 2024 |

| Fitch Ratings | BBB | Stable | June 6, 2025 |

Economic Indicators

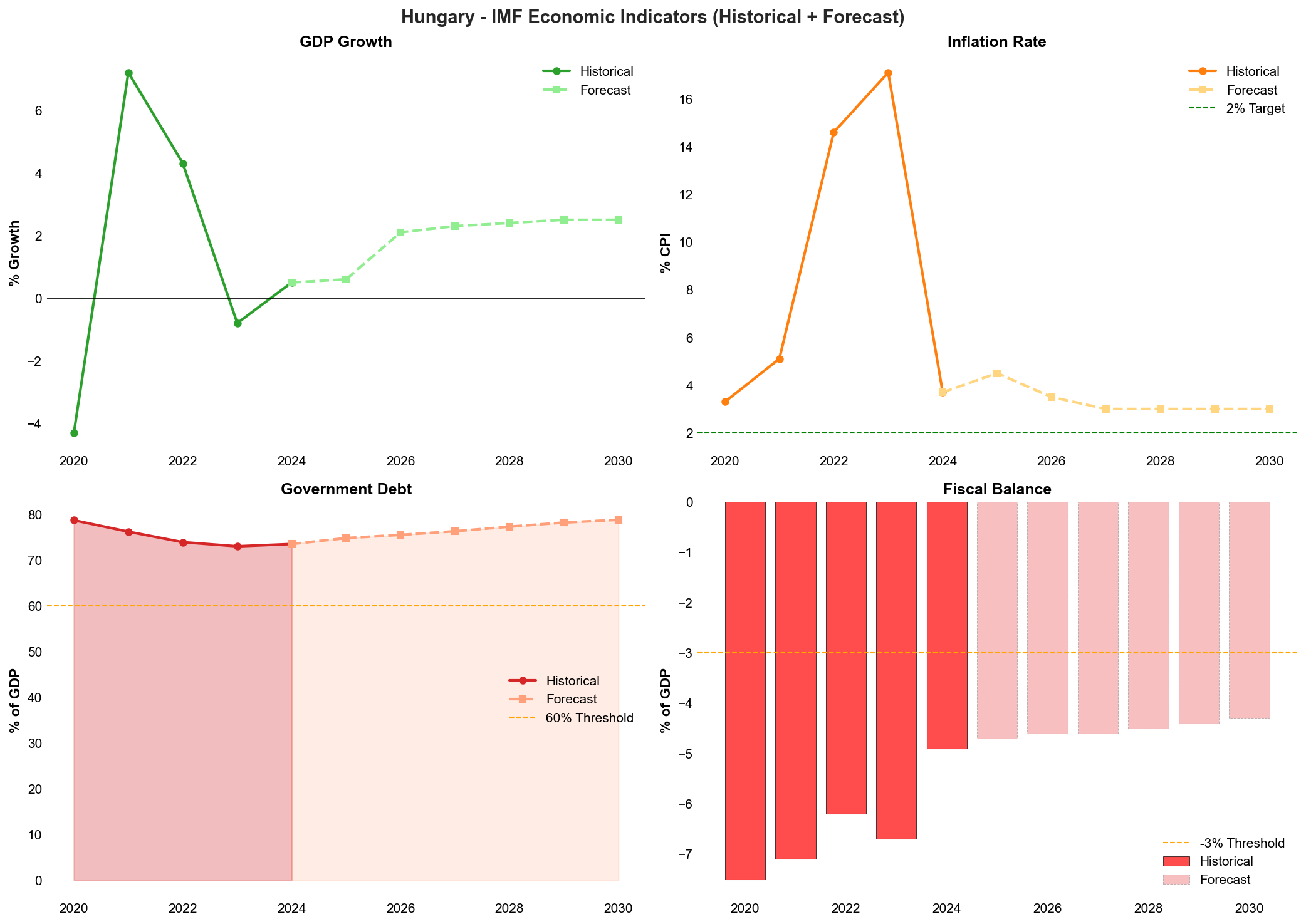

Hungary's economic performance has been characterised by pronounced stagnation over the 2022-2024 period, with cumulative real growth approaching zero as the economy grappled with elevated inflation, weak external demand, and policy uncertainty. The contraction of 0.9% in 2023 represented the nadir of this challenging cycle, driven by deteriorating consumer confidence, restrictive monetary policy to combat inflation exceeding 17% in 2023, and weakening demand from key trading partners, particularly Germany. The modest recovery to 0.8% growth in 2024 reflects tentative stabilisation rather than robust expansion, with domestic consumption constrained by real wage erosion and investment dampened by frozen EU funds and geopolitical tensions. Looking forward, the IMF projects a gradual acceleration to 2.5% growth by 2030, contingent upon normalisation of trade relations, potential governance reforms following the 2026 elections, and successful absorption of EU Recovery and Resilience Facility resources before the end-2026 deadline.

| Indicator | 2022 | 2023 | 2024 | 2025 | 2026 | 2030 |

|---|---|---|---|---|---|---|

| Real GDP Growth (%) | 4.6 | -0.9 | 0.8 | 1.5-1.9 | 3.0 | 2.5 |

| Inflation (%) | 14.5 | 17.0 | 3.7 | 4.5 | 3.5 | 3.0 |

| Unemployment Rate (%) | 3.6 | 4.1 | 4.5 | 4.2 | 4.0 | 3.8 |

| Current Account (% GDP) | -7.8 | -1.2 | 2.3 | 2.5 | 3.0 | 5.5 |

| Fiscal Balance (% GDP) | -6.2 | -6.7 | -4.7 | -4.5 | -3.7 | -4.3 |

| Government Debt (% GDP) | 73.5 | 73.3 | 73.9 | 75.0 | 76.5 | 78.8 |

| GDP per Capita (USD) | 18,728 | 20,539 | 23,292 | — | — | — |

The dramatic improvement in Hungary's current account position represents one of the most significant positive developments in the country's macroeconomic profile, with the balance swinging from a deficit of 7.8% of GDP in 2022 to a surplus of 2.3% in 2024. This nine-percentage-point adjustment reflects both cyclical and structural factors, including import compression during the economic slowdown, improved terms of trade as energy prices normalised following the initial shock of Russia's invasion of Ukraine, and strong export performance from newly operational automotive manufacturing facilities. The IMF projects further strengthening to 5.5% of GDP by 2030, supported by continued expansion of export-oriented manufacturing capacity, particularly in electric vehicle production, and sustained tourism receipts. This robust external position provides critical insulation against external shocks and reduces vulnerability to sudden stops in capital flows, partially offsetting concerns about governance-related risks and frozen EU funds.

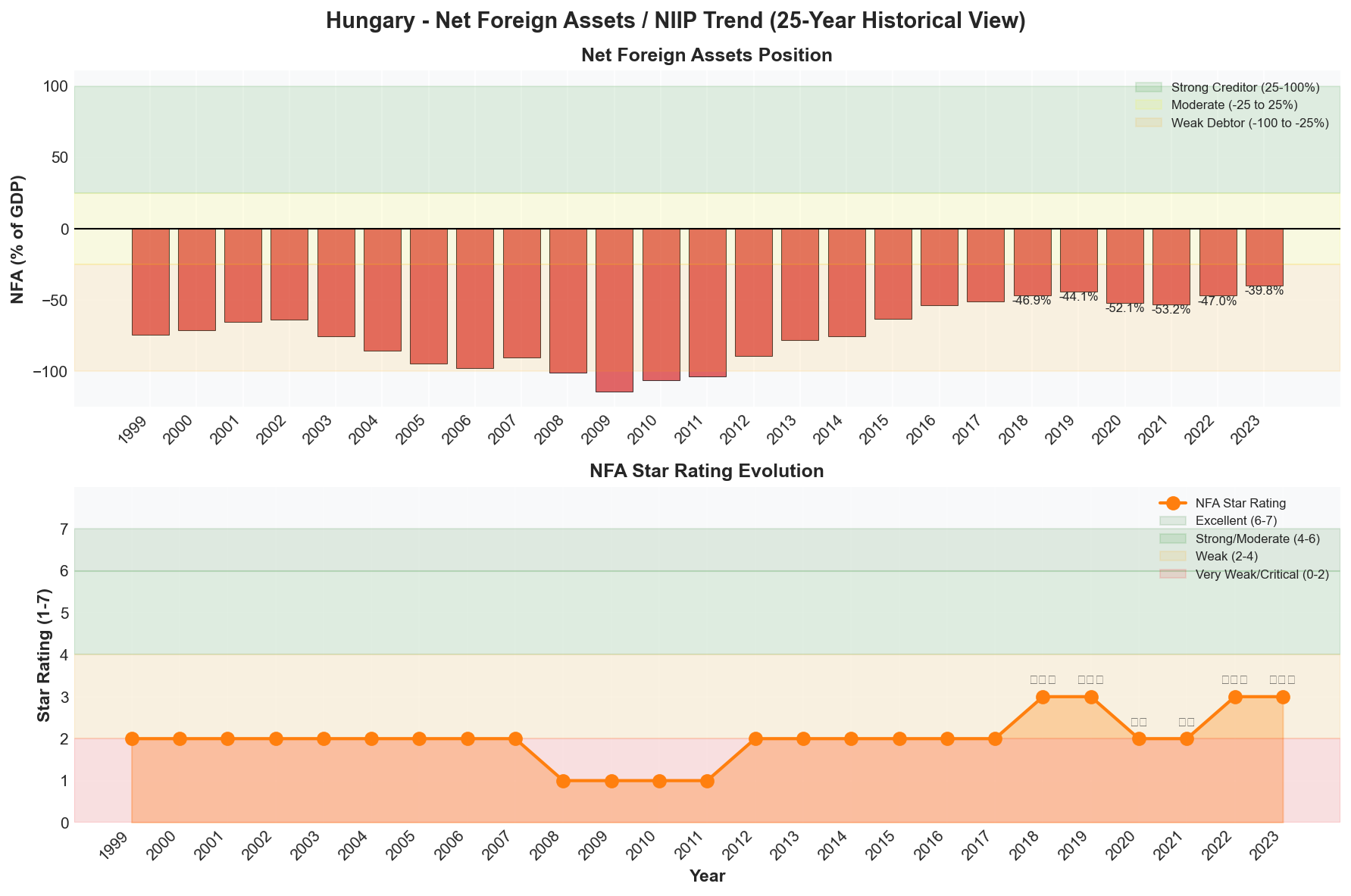

Hungary's net foreign asset position has shown notable improvement from its weakest point in 2021, when the net international investment position reached negative 53.2% of GDP, to negative 39.8% in 2023. This 13.4-percentage-point improvement over two years reflects both current account adjustment and valuation effects, lifting Hungary from a "Very Weak" debtor position (⭐⭐) to a "Weak" classification (⭐⭐⭐) in the External Wealth of Nations assessment framework. Whilst the country remains a net debtor with notable external liabilities, the trajectory of improvement and the current level of negative 39.8% of GDP place Hungary in a more manageable position relative to its 2020-2021 nadir. The combination of sustained current account surpluses and continued FDI inflows—albeit increasingly concentrated from Chinese sources—should support further gradual improvement in the net foreign asset position over the medium term, enhancing external resilience.

Fiscal consolidation has proceeded more slowly than initially targeted, with the government deficit declining from 6.7% of GDP in 2023 to an estimated 4.7% in 2024, but remaining well above the 3% Maastricht criterion. Standard & Poor's projects deficits of 4.5% of GDP in 2025, driven by pre-election spending pressures ahead of the 2026 parliamentary elections, with the agency expressing scepticism about the government's ability to achieve its more ambitious consolidation targets. The IMF's projection of a 4.3% deficit persisting through 2030 suggests structural fiscal challenges that extend beyond the electoral cycle, reflecting both revenue constraints from frozen EU funds and expenditure pressures from an ageing population, elevated interest costs exceeding 4% of GDP, and necessary infrastructure investment. Government debt is projected to rise gradually from 73.9% of GDP in 2024 to 78.8% by 2030, a trajectory that remains manageable but leaves limited fiscal space for responding to adverse shocks, particularly given Hungary's exclusion from significant EU funding streams.

The inflation trajectory illustrates both the severity of the 2022-2023 shock and the effectiveness of subsequent monetary tightening, with consumer price inflation peaking at 17.0% in 2023 before declining sharply to 3.7% in 2024. Standard & Poor's projects inflation averaging 4.5% in 2025, above the central bank's 3% target, before converging towards the IMF's 3.0% forecast for 2030. The persistence of above-target inflation reflects both external factors—including potential second-round effects from US tariffs on imported goods—and domestic pressures from tight labour markets and administered price adjustments. The unemployment rate has remained exceptionally low by European standards, fluctuating between 3.6% and 4.5% over the 2022-2024 period, with the IMF projecting further decline to 3.8% by 2030. This tight labour market supports household incomes and consumption but constrains monetary policy flexibility and may contribute to wage-price spiral risks if productivity growth remains subdued.

Net Foreign Assets & External Position

Hungary's external position reflects a persistent but gradually improving debtor status, with net foreign assets standing at -39.8% of GDP in 2023—a marked improvement from the -53.2% trough recorded in 2021 but still indicative of substantial external liabilities that constrain sovereign creditworthiness. The country's net international investment position (NIIP) has strengthened by 13.4 percentage points over the past two years, driven primarily by robust current account surpluses, favourable valuation effects from forint depreciation on foreign-currency assets, and sustained foreign direct investment inflows concentrated in the automotive and battery manufacturing sectors. Despite this positive trajectory, Hungary's external position remains classified as "weak" with a three-star rating on a seven-point scale, placing it in the -50% to -25% NFA/GDP range that signals notable external vulnerabilities requiring careful monitoring. The improvement trajectory is encouraging, yet the country's negative NIIP leaves it exposed to external financing shocks and limits fiscal policy flexibility during periods of market stress.

The five-year trend in Hungary's net foreign asset position reveals a clear inflection point following the pandemic-induced deterioration. From 2019 through 2021, Hungary's NIIP weakened substantially, declining from -44.1% to -53.2% of GDP as the country absorbed external financing to support pandemic response measures and maintain economic activity during lockdowns. This deterioration pushed Hungary temporarily into "very weak" territory with a two-star rating, reflecting heightened external vulnerability at a time of global economic uncertainty. The subsequent recovery beginning in 2022 has been sustained and significant, with the NIIP improving to -47.0% in 2022 and further to -39.8% in 2023, restoring the three-star "weak" classification. This improvement of 13.4 percentage points over two years represents one of the stronger NIIP recoveries among Central European peers and reflects both cyclical factors—including strong export performance in automotive and electronics sectors—and structural shifts in Hungary's external financing profile.

The composition of Hungary's external liabilities warrants particular attention, as the country's negative NIIP is heavily weighted toward foreign direct investment rather than debt instruments, providing a more stable financing structure than headline figures might suggest. FDI liabilities constitute approximately 60% of Hungary's gross external liabilities, reflecting decades of foreign investment in manufacturing, particularly automotive production facilities established by Mercedes-Benz, BMW, Audi, and more recently battery manufacturing plants from Chinese firms including CATL and BYD. This FDI-heavy liability structure is considerably less vulnerable to sudden stops or capital flight compared to portfolio debt or banking sector liabilities, as direct investment represents long-term commitments tied to physical assets and integrated supply chains. However, the recent shift toward Chinese FDI—now comprising 80% of new foreign investment—introduces new considerations for external stability, as these investments are concentrated in sectors facing potential overcapacity concerns and are subject to evolving geopolitical dynamics between China and Western economies.

Hungary's current account position has emerged as a significant strength supporting external stability, with the country recording a surplus of 2.3% of GDP in recent periods and IMF projections indicating this surplus will expand substantially to 5.5% of GDP by 2030. This represents a remarkable transformation from the current account deficits that characterised Hungary's pre-2008 economic model and reflects both structural improvements in export competitiveness and cyclical factors including compressed domestic demand. The automotive sector remains the primary driver of export performance, with vehicle and parts exports generating substantial trade surpluses despite facing headwinds from US tariffs averaging 25% on finished vehicles. The current account surplus provides a natural hedge against external financing pressures, generating foreign exchange inflows that reduce reliance on capital markets and support gradual NIIP improvement. The IMF's projection of a 5.5% surplus by 2030 appears optimistic given potential headwinds from US trade policy and weakening German demand, but even more conservative surplus projections of 2-3% of GDP would support continued NIIP strengthening over the medium term.

Foreign exchange reserves provide a substantial buffer against external shocks, with holdings of €46.3 billion (approximately 23% of GDP) offering considerable protection against balance of payments pressures or sudden capital outflows. These reserves are managed by the Magyar Nemzeti Bank and have been accumulated through periods of current account surplus and central bank foreign exchange purchases designed to limit forint appreciation. The reserve position compares favourably to traditional adequacy metrics, covering approximately 5.5 months of imports and exceeding 100% of short-term external debt by remaining maturity. This reserve cushion proved valuable during the 2022 energy crisis and forint volatility, when the central bank deployed reserves to support currency stability without requiring external assistance. However, the adequacy of reserves must be assessed against Hungary's substantial gross external financing requirements, which include both maturing external debt and potential portfolio outflows during risk-off episodes. The country's EU membership provides an additional safety net through access to Balance of Payments assistance mechanisms, though recourse to such facilities would likely trigger rating downgrades and signal acute distress.

External vulnerabilities remain concentrated in three primary areas that could reverse recent NIIP improvements and pressure sovereign creditworthiness. First, Hungary's deep integration into German automotive supply chains creates asymmetric exposure to German economic performance, with weak demand from Germany—Hungary's largest trading partner accounting for 25% of exports—capable of generating substantial trade balance deterioration. The German automotive sector faces its own structural challenges including electrification transition costs and Chinese competition, potentially transmitting weakness to Hungarian suppliers and assembly operations. Second, the maturity profile of external debt, while manageable, requires continuous market access to refinance maturing obligations, leaving Hungary vulnerable to sudden shifts in investor sentiment or global financial conditions. Approximately 15% of GDP in external debt matures within one year, necessitating regular market engagement that could prove challenging if governance concerns intensify or rating downgrades materialise. Third, the concentration of new FDI in Chinese battery manufacturing creates sector-specific risks, as global electric vehicle demand has proven more volatile than anticipated and potential overcapacity in battery production could lead to facility closures or reduced capacity utilisation, undermining the FDI stability that has historically anchored Hungary's external position.

The forward trajectory of Hungary's external position depends critically on sustaining current account surpluses while managing external debt refinancing and maintaining FDI inflows despite governance concerns. The IMF's projection of a 5.5% current account surplus by 2030 would, if realised, support continued NIIP improvement toward the -25% threshold that would elevate Hungary to "moderate" external position status with a four-star rating. However, this optimistic scenario requires successful navigation of US trade policy uncertainty, sustained German economic recovery, and continued competitiveness in automotive and electronics exports despite rising wage pressures and infrastructure constraints from frozen EU funds. A more conservative scenario incorporating modest trade policy headwinds and slower German growth would likely see current account surpluses of 2-3% of GDP, still sufficient to support gradual NIIP improvement but at a slower pace. The risk scenario involves a combination of sharp German recession, escalating US tariffs, and FDI reversal that could reverse recent gains and push the NIIP back toward -50% of GDP, though the probability of such an adverse confluence appears moderate given Hungary's diversified export base and EU integration benefits.

Credit Strengths & Vulnerabilities

Strengths

Hungary's credit profile is anchored by several robust structural features that provide meaningful resilience against external shocks. The banking sector demonstrates exceptional capitalisation, with a capital adequacy ratio of 20.5% that substantially exceeds both regulatory minimums and regional peers, creating a significant buffer against potential financial stress. This strong capitalisation reflects both prudent regulatory oversight and the sector's profitability, positioning Hungarian banks to support economic activity even during periods of heightened uncertainty.

The external position provides another pillar of strength, with Hungary maintaining a current account surplus of 2.3% of GDP—a marked improvement from historical deficits and a reflection of export competitiveness despite recent headwinds. Foreign exchange reserves stand at €46.3 billion, providing substantial coverage against external financing needs and offering monetary authorities considerable flexibility in managing exchange rate pressures. This reserve position, combined with the current account surplus, significantly reduces vulnerability to sudden stops in capital flows or external financing disruptions.

Hungary's deep integration within European Union structures, despite recent tensions, continues to provide fundamental economic benefits through market access, regulatory alignment, and institutional frameworks. The country's position within EU supply chains, particularly in the automotive sector, has driven significant foreign direct investment and technology transfer over the past two decades. Even with current fund freezes, Hungary's EU membership provides access to the single market and benefits from monetary policy coordination with the European Central Bank, factors that underpin long-term economic stability.

Vulnerabilities

Governance deterioration represents the most significant structural vulnerability in Hungary's credit profile, with the country ranking as the EU's most corrupt member state for the third consecutive year. Transparency International's score of 41 out of 100 places Hungary alongside Morocco and Tanzania globally, reflecting systematic weaknesses in institutional quality, rule of law, and public sector integrity. This governance deficit has triggered unprecedented consequences, with EU fund freezes totaling €19 billion—equivalent to 34.8% of 2023 government revenue. The permanent forfeiture of €1 billion in EU funds in January 2025 marked the first such loss in EU history, establishing a concerning precedent and constraining fiscal space for infrastructure investment and economic modernisation.

Fiscal pressures have intensified as interest costs are projected to exceed 4% of GDP in 2025, representing 11.9% of government revenues. This substantial debt service burden limits policy flexibility precisely when external headwinds require countercyclical support. The fiscal deficit is projected at 4.5% of GDP in 2025, exceeding government targets and raising concerns about pre-election spending ahead of the 2026 parliamentary elections. The combination of elevated deficits, high interest costs, and frozen EU funds creates a challenging fiscal environment that constrains the government's ability to respond to economic shocks or invest in productivity-enhancing infrastructure.

Economic stagnation over the past three years, with cumulative real growth near zero, reflects both cyclical and structural challenges. Weak external demand, particularly from Germany—Hungary's largest trading partner—has weighed heavily on the export-oriented manufacturing sector. The automotive industry, which represents 40% of exports to the United States and employs tens of thousands, faces acute pressure from 25% tariffs on vehicles. Overall, US trade tariffs averaging 18.8% on Hungarian exports, combined with indirect effects through German supply chains, threaten to reduce GDP by 1.4-2.3% in 2025. Persistent inflation, expected to average 4.5% in 2025, further erodes purchasing power and complicates monetary policy management.

Opportunities

The nascent economic recovery projected for 2026 offers potential for improved credit metrics if external conditions stabilise. Rating agencies forecast growth accelerating to an average of 3% in 2026-2028, driven by new electric vehicle production facilities coming online and potential easing of trade tensions. Should Hungary successfully navigate the 2026 elections and implement governance reforms, access to frozen EU funds could be restored, providing substantial fiscal resources for infrastructure investment and economic modernisation. The Recovery and Resilience Facility resources, if accessed before the end-2026 deadline, would represent approximately 5% of GDP and could catalyse private investment through improved infrastructure and business environment.

Hungary's pivot toward Chinese investment, now comprising 80% of new foreign direct investment, provides alternative capital sources at a time when Western investment has become more cautious. Major Chinese investments in electric vehicle manufacturing and battery production offer potential for industrial upgrading and export diversification, though these opportunities come with strategic dependencies. The development of new manufacturing capacity in emerging technologies could position Hungary favourably for future growth sectors, particularly if global supply chains continue to diversify away from concentrated production locations.

Political transition following the 2026 elections could catalyse governance improvements and restore relations with EU institutions. A change in government approach toward rule of law, judicial independence, and anti-corruption measures could unlock frozen funds and improve Hungary's standing with Western partners. Even incremental progress on the "27 super-conditions" for accessing Recovery and Resilience Facility resources would signal positive momentum and potentially stabilise rating agency outlooks.

Threats

Downgrade to sub-investment grade represents the most immediate threat to Hungary's credit profile, with two of three major rating agencies maintaining negative outlooks. A downgrade would trigger forced selling by institutional investors with investment-grade mandates, potentially disrupting government bond markets and increasing borrowing costs. The loss of investment-grade status would also complicate private sector access to international capital markets and likely accelerate capital outflows, creating broader financial stability risks.

Escalating trade tensions pose severe downside risks to growth projections, particularly given Hungary's heavy dependence on automotive exports and integration into German supply chains. US tariffs averaging 18.8% on Hungarian exports could reduce GDP by up to 2.3%, whilst weak German economic performance would transmit directly through supply chain linkages. New electric vehicle production facilities may operate below capacity due to weak external demand, undermining the expected contribution to growth and employment. Should trade tensions intensify further or expand to additional sectors, the economic impact could significantly exceed current projections.

The permanent loss of additional EU funds remains a substantial risk if Hungary fails to meet conditionality requirements before deadlines expire. Beyond the €1 billion already forfeited, substantial Recovery and Resilience Facility resources totaling approximately 5% of GDP face an end-2026 deadline. The government's ability to implement required reforms whilst managing pre-election political pressures appears increasingly constrained, raising the probability of further fund losses. Such an outcome would not only deprive Hungary of critical investment resources but would also signal deepening institutional divergence from EU norms, potentially triggering broader economic and financial consequences.

Geopolitical isolation from Western partners introduces strategic vulnerabilities that could manifest through reduced investment, technology transfer restrictions, or exclusion from security and economic cooperation frameworks. Hungary's increasingly close alignment with China and Russia, whilst providing short-term economic benefits, complicates relations with NATO allies and EU partners. Should geopolitical tensions escalate, Hungary could face difficult choices between competing alliances, with significant economic and security implications regardless of the path chosen.

Economic Analysis

Hungary's economic trajectory reflects a protracted period of stagnation punctuated by mounting external pressures that threaten the nascent recovery anticipated for 2026. The economy has effectively flatlined over the past three years, with cumulative real growth approaching zero—a performance that places Hungary among the weakest performers in the Central European region. This extended period of economic malaise stems from a confluence of factors including elevated inflation that has eroded household purchasing power, weak external demand from key trading partners, and the constraining effects of frozen EU funds on public investment capacity. The growth outlook for 2025 remains subdued, with consensus forecasts clustering around 1.5-1.9%, though projections for 2026 and beyond suggest a potential acceleration contingent upon resolution of trade tensions and possible governance reforms following parliamentary elections.

Growth dynamics reveal structural vulnerabilities and external dependencies

The Hungarian economy's growth performance has deteriorated markedly from the robust expansion witnessed in earlier years, with structural weaknesses becoming increasingly apparent. Standard & Poor's revised its 2025 GDP growth forecast downward to 1.5%, a substantial reduction from the 3% previously anticipated, citing weak external demand and the lingering effects of persistent inflation. Moody's projects marginally stronger growth of 1.9% for 2025, rising to an average of 3% over the 2026-2028 period, though this optimistic medium-term outlook carries significant conditionality. The growth deceleration reflects both cyclical headwinds and structural challenges that constrain Hungary's economic potential.

External demand weakness constitutes a primary drag on Hungarian economic activity, with the country's export-oriented growth model proving vulnerable to deteriorating conditions in key markets. Germany, Hungary's largest trading partner and the destination for a substantial portion of manufactured exports, has experienced its own economic difficulties that reverberate through Hungarian supply chains. The automotive sector, which represents 40% of Hungarian exports to the United States and forms a critical component of the industrial base, faces particularly acute pressure from the imposition of 25% tariffs on vehicles. These direct tariff effects combine with indirect impacts transmitted through German automotive manufacturers, with whom Hungarian producers maintain deep integration, to create a compounding negative shock. Analysts estimate that US tariffs averaging 18.8% on Hungarian exports, when combined with these indirect transmission channels, could reduce GDP by between 1.4% and 2.3% in 2025—a material headwind that substantially undermines growth prospects.

Domestic demand has similarly failed to provide compensatory momentum, constrained by elevated inflation that has compressed real household incomes and dampened consumption. The prolonged period of above-target inflation has eroded purchasing power, whilst elevated interest rates maintained to combat price pressures have increased borrowing costs and discouraged investment. Public investment, traditionally a significant growth driver in Hungary, has been curtailed by the freeze on €19 billion in EU funds—resources that would ordinarily finance infrastructure development and economic modernisation. The permanent forfeiture of €1 billion in EU cohesion funds in January 2025 represents not merely a fiscal loss but a tangible reduction in productive investment that would have supported medium-term growth potential.

The nascent recovery projected for 2026 rests upon several critical assumptions that introduce considerable uncertainty into the outlook. Easing trade tensions, particularly resolution of US tariff policies, would remove a significant constraint on export performance and restore confidence in the automotive sector. Potential governance reforms following the 2026 parliamentary elections could facilitate the unlocking of frozen EU funds, though this outcome depends upon political developments that remain highly uncertain. The establishment of new electric vehicle production facilities offers promise for future export capacity, yet Moody's cautions that these facilities may operate below capacity due to weak external demand—a concern that underscores the vulnerability of Hungary's growth model to conditions beyond domestic policy control.

Inflation persistence complicates monetary policy normalisation

Hungary has grappled with elevated inflation that has proven more persistent than initially anticipated, complicating the central bank's efforts to normalise monetary policy whilst supporting economic recovery. Standard & Poor's projects inflation will average 4.5% in 2025, substantially above the Magyar Nemzeti Bank's 3% target and indicative of underlying price pressures that have resisted monetary tightening. This inflation persistence reflects both external factors, including energy price volatility and supply chain disruptions, and domestic dynamics such as wage growth in a tight labour market and the pass-through effects of forint depreciation.

The inflation trajectory has significant implications for household welfare and economic performance. Real wage growth has been constrained by price increases that have outpaced nominal wage gains, reducing disposable income and dampening consumption. The erosion of purchasing power has been particularly acute for lower-income households that allocate larger budget shares to food and energy—categories that have experienced above-average price increases. This distributional impact of inflation has contributed to social pressures that complicate fiscal policy choices, as the government faces demands for compensatory measures even as it attempts fiscal consolidation.

Monetary policy navigates competing imperatives

The Magyar Nemzeti Bank confronts the challenging task of calibrating monetary policy to address persistent inflation whilst avoiding excessive constraint on an already fragile economic recovery. The central bank has maintained elevated interest rates to anchor inflation expectations and defend the forint, yet this stance imposes costs on economic activity through higher borrowing costs and reduced credit availability. The policy dilemma is compounded by external factors beyond the central bank's control, including US Federal Reserve policy that influences global financial conditions and European Central Bank decisions that affect regional monetary dynamics.

The forint's exchange rate performance adds complexity to monetary policy implementation. Currency depreciation, whilst potentially supporting export competitiveness, generates inflationary pressure through higher import costs—particularly problematic for an economy dependent upon imported energy and intermediate goods. The central bank must therefore balance the competing objectives of maintaining exchange rate stability, controlling inflation, and supporting growth—a trilemma that admits no easy resolution in the current environment. The substantial foreign exchange reserves of €46.3 billion provide a buffer against currency volatility and enhance the credibility of monetary policy, yet reserves alone cannot insulate Hungary from the fundamental tensions inherent in its economic position.

The path toward monetary policy normalisation depends critically upon inflation dynamics and external conditions. A sustained decline in inflation toward the 3% target would create space for interest rate reductions that could support economic recovery, yet premature easing risks reigniting price pressures or triggering currency depreciation. The central bank's policy trajectory will therefore likely remain cautious and data-dependent, with the pace of normalisation contingent upon clear evidence of inflation moderation and stabilisation of external conditions. This gradualist approach, whilst prudent from a monetary stability perspective, implies that the supportive effects of easier monetary policy on growth will materialise slowly and may prove insufficient to offset other headwinds facing the economy.

Political & Institutional Assessment

Hungary's political and institutional framework presents significant credit challenges, characterised by systematic governance deficiencies that have triggered unprecedented punitive measures from the European Union and contributed to the country's isolation within Western institutional structures. The nation ranks as the EU's most corrupt member state for the third consecutive year, with a Transparency International score of 41/100, positioning it alongside Morocco and Tanzania in global comparisons. This governance deficit extends beyond corruption metrics to encompass broader concerns about institutional independence, rule of law adherence, and democratic backsliding that have fundamentally altered Hungary's relationship with its traditional European partners.

The tangible consequences of these institutional weaknesses manifest most acutely in the unprecedented freezing of EU funds totalling €19 billion, representing 34.8% of 2023 government revenue. This figure encompasses both cohesion policy funds and resources from the Recovery and Resilience Facility, with access contingent upon Hungary meeting 27 super-conditions related to judicial independence, anti-corruption measures, and public procurement reforms. The severity of the EU's response reached a historic milestone in January 2025 when Hungary permanently forfeited €1 billion in cohesion funds—the first such forfeiture in EU history—underscoring the depth of institutional concerns and the EU's willingness to enforce conditionality mechanisms. The loss of these funds constrains fiscal space and infrastructure investment capacity at a critical juncture when the economy faces multiple external headwinds.

The political calendar introduces additional uncertainty, with parliamentary elections scheduled for 2026 creating incentives for pre-election fiscal expansion that may compromise consolidation efforts. Standard & Poor's outlook revision to negative in April 2025 explicitly cited concerns about pre-election spending pressures, projecting deficits of 4.5% of GDP that exceed government targets. The electoral cycle thus intersects with Hungary's already constrained fiscal position, potentially exacerbating tensions with EU institutions and rating agencies alike. Whilst the 2026 elections could theoretically provide an opportunity for governance reforms that might unlock frozen EU funds, the entrenched nature of current political arrangements suggests limited near-term prospects for the institutional changes required to satisfy EU conditionality.

Hungary's geopolitical positioning further complicates its institutional profile, with the government's pivot toward Chinese investment and maintenance of closer relations with Russia than other EU member states creating strategic tensions with Western partners. Chinese investment now comprises 80% of new foreign direct investment inflows, representing a dramatic reorientation of economic dependencies that introduces new vulnerabilities whilst partially offsetting reduced Western engagement. This geopolitical stance, combined with systematic governance deficiencies, has contributed to Hungary's increasing isolation within EU decision-making structures and complicated its ability to advocate effectively for national interests within European institutions. The resulting institutional fragility represents a structural credit weakness that constrains policy flexibility and amplifies vulnerability to external shocks, particularly given Hungary's high degree of economic integration with EU markets and dependence on EU funding flows for fiscal sustainability.

Banking Sector & Financial Stability

Hungary's banking sector represents a notable bright spot in the country's credit profile, demonstrating exceptional capitalisation, robust profitability, and resilient asset quality that provide a critical buffer against macroeconomic headwinds. The sector's capital adequacy ratio stands at 20.5% as of December 2024, substantially exceeding both the regulatory minimum of 8% and the EU average of approximately 15%. This strong capitalisation reflects conservative risk management practices, regulatory requirements implemented following the 2008 financial crisis, and sustained profitability that has enabled banks to retain earnings and build capital buffers. The sector's return on equity averaged 15.2% in 2024, amongst the highest in the European Union, whilst non-performing loan ratios remained contained at 2.8%—well below the 3.5% threshold typically associated with systemic stress.

The banking sector's strength derives partly from structural reforms implemented over the past decade that have transformed its ownership composition and operational framework. Following a period of aggressive nationalisation between 2013 and 2015, domestic ownership now accounts for approximately 50% of banking sector assets, with the state-owned MKB Bank, Takarékbank, and Budapest Bank forming the core of the domestic banking system. Foreign-owned institutions, predominantly Austrian, German, and Italian banks, comprise the remainder and continue to provide important links to European capital markets and expertise. This mixed ownership structure has proven resilient, combining the stability of well-capitalised foreign parents with domestic institutions' deeper understanding of local market dynamics and closer relationships with small and medium-sized enterprises.

Profitability in the Hungarian banking sector has benefited significantly from the high interest rate environment that prevailed through 2023 and much of 2024, with the National Bank of Hungary's base rate reaching 13% in October 2023 before declining to 6.5% by December 2024. This elevated rate environment expanded net interest margins, particularly for banks with substantial retail deposit bases, whilst fee income from transaction services and asset management remained robust. However, the sector faces emerging pressures from several directions. The government's introduction of a windfall tax on banks in 2022, subsequently extended through 2024, extracted approximately HUF 200 billion (€500 million) annually from the sector, constraining capital accumulation and lending capacity. Whilst this levy was reduced in 2025, it established a precedent for discretionary taxation that introduces uncertainty into long-term planning.

Asset quality metrics warrant careful monitoring despite their current strength. The 2.8% non-performing loan ratio masks some underlying vulnerabilities, particularly in the corporate loan portfolio where exposure to struggling manufacturing firms and small businesses affected by weak domestic demand could deteriorate if economic conditions worsen. The automotive supply chain, which employs tens of thousands and faces acute pressure from US tariffs and weak European demand, represents a concentrated risk given many suppliers' reliance on bank financing for working capital and investment. Similarly, the commercial real estate sector shows signs of stress, with vacancy rates in Budapest office properties rising and valuations under pressure from higher interest rates and reduced demand. Banks' exposure to these sectors, whilst manageable at present, could generate losses if the projected economic recovery fails to materialise or if trade tensions intensify.

The household lending portfolio presents a more benign picture, supported by strong employment levels (unemployment at 4.3% in December 2024) and wage growth that has outpaced inflation since mid-2024. Mortgage lending, which comprises approximately 40% of household credit, benefits from relatively conservative loan-to-value ratios averaging 60-65% and the prevalence of fixed-rate products that insulate borrowers from interest rate volatility. Consumer lending growth has moderated from the rapid expansion seen in 2021-2022, reflecting both tighter monetary conditions and banks' more cautious approach to unsecured lending. Household debt service ratios remain manageable at approximately 12% of disposable income, well below levels that typically signal systemic stress.

Liquidity conditions in the banking sector remain comfortable, with the loan-to-deposit ratio standing at 78% in December 2024, indicating substantial deposit funding that reduces reliance on wholesale markets. Hungarian banks maintain liquid asset buffers equivalent to approximately 25% of total assets, comprising primarily government securities and central bank deposits. This liquidity cushion provides resilience against potential deposit outflows or disruptions to wholesale funding markets. However, the sector's substantial holdings of Hungarian government debt—estimated at HUF 12 trillion (€30 billion) or approximately 20% of total assets—creates a sovereign-bank nexus that could amplify stress if Hungary's credit rating were downgraded or if government bond yields spiked. This exposure reflects both regulatory requirements for liquid asset holdings and banks' search for yield in a market with limited high-quality domestic alternatives.

The National Bank of Hungary has demonstrated competent supervision and crisis management capabilities, implementing macroprudential measures to contain risks whilst supporting financial stability. The central bank's willingness to deploy foreign exchange reserves to stabilise the forint during periods of market stress, combined with its communication strategy and coordination with European authorities, has helped maintain confidence in the banking system. Regulatory stress tests conducted in 2024 indicated that major banks could withstand severe adverse scenarios, including a 3% GDP contraction, 200 basis point increase in interest rates, and 30% depreciation of the forint, whilst maintaining capital ratios above regulatory minima.

Looking forward, the banking sector's resilience will be tested by Hungary's challenging macroeconomic environment and the potential for renewed currency volatility if trade tensions escalate or if relations with the European Union deteriorate further. The sector's strong starting position provides meaningful capacity to absorb losses and continue supporting the real economy, but sustained economic stagnation, fiscal deterioration, or a sovereign rating downgrade could erode this buffer and constrain banks' ability to extend credit. The government's fiscal pressures may also tempt authorities to impose additional levies on the banking sector, further constraining profitability and capital accumulation at a time when economic conditions argue for strengthening rather than weakening financial buffers.

Outlook & Scenarios

Short-Term Outlook (12 months)

Hungary's near-term credit trajectory faces considerable headwinds as the country navigates a confluence of external shocks and domestic policy challenges through 2026. The immediate outlook centres on three critical pressure points: the impact of US trade tariffs on export-dependent sectors, pre-election fiscal expansion ahead of the April 2026 parliamentary elections, and the continued freeze of substantial EU funding streams. The automotive sector, which represents 40% of exports to the United States and employs tens of thousands of workers, confronts particularly acute stress from 25% tariffs on vehicles, with broader indirect effects transmitted through weakened German demand given Hungary's deep integration into German supply chains. These trade disruptions are projected to reduce GDP growth to between 1.5% and 1.9% in 2025, representing a significant downward revision from earlier forecasts of 3% growth.

Fiscal dynamics present mounting concern as the government pursues expansionary policies in the run-up to elections. Standard & Poor's projects the general government deficit will reach 4.5% of GDP in 2025, exceeding official government targets and raising questions about fiscal discipline. Interest costs are expected to surpass 4% of GDP, consuming 11.9% of government revenues and constraining policy flexibility at a juncture when infrastructure investment and social spending face competing demands. Inflation persistence compounds these challenges, with consumer price growth anticipated to average 4.5% through 2025—well above the central bank's target and eroding real incomes despite strong employment levels. The Magyar Nemzeti Bank faces a delicate balancing act between supporting economic activity through accommodative monetary policy and maintaining price stability, with limited room for manoeuvre given external financing requirements.

The frozen EU funds totalling €19 billion—equivalent to 34.8% of 2023 government revenue—represent the most significant structural constraint on near-term prospects. Hungary faces a critical deadline of end-2026 to access Recovery and Resilience Facility resources by meeting 27 super-conditions related to governance reforms, judicial independence, and anti-corruption measures. The permanent forfeiture of €1 billion in cohesion funds in January 2025 marked an unprecedented development in EU history and signals Brussels' hardening stance on conditionality enforcement. Without meaningful progress on governance reforms, Hungary risks losing additional tranches of funding that would otherwise finance critical infrastructure upgrades, education system improvements, and green transition investments. The government's ability to navigate these conditionalities whilst maintaining its domestic political positioning will largely determine whether the nascent economic recovery projected for late 2026 materialises or whether the country slides into a more protracted period of stagnation.

Medium-Term Outlook (1-3 years)

The medium-term credit outlook for Hungary hinges critically on the outcome of the April 2026 parliamentary elections and subsequent policy trajectory, particularly regarding EU relations and governance reforms. A scenario in which the current government retains power but moderates its approach to Brussels—potentially driven by fiscal necessity and the imperative to access frozen funds—could enable gradual improvement in Hungary's credit profile. Conversely, continued deterioration in EU relations and permanent loss of substantial funding streams would entrench structural weaknesses and elevate downgrade risk. Moody's projects average GDP growth of 3% for the 2026-2028 period, contingent on resolution of trade tensions, normalisation of EU fund flows, and sustained external demand recovery. However, this baseline scenario incorporates significant execution risk, particularly regarding the government's capacity to implement the governance reforms required to unlock EU resources whilst maintaining domestic political support.

Hungary's strategic pivot toward Chinese investment introduces both opportunities and vulnerabilities over the medium term. Chinese foreign direct investment now comprises 80% of new FDI inflows, financing major projects including battery manufacturing facilities and the Budapest-Belgrade railway upgrade. Whilst this capital partially offsets constrained EU funding and supports employment in advanced manufacturing sectors, it creates new dependencies that complicate Hungary's geopolitical positioning within NATO and the European Union. The concentration of investment in electric vehicle supply chains exposes Hungary to demand volatility in the global EV market, which has experienced significant turbulence with weakening consumer adoption rates in key markets. New production facilities may operate below capacity if external demand remains subdued, limiting the employment and fiscal revenue benefits anticipated from these investments.

The banking sector's exceptional resilience provides crucial stability through this transition period. With a capital adequacy ratio of 20.5%—substantially above regulatory minimums and peer country averages—Hungarian banks possess robust buffers to absorb potential credit losses from economic slowdown or corporate distress in export-oriented sectors. Non-performing loan ratios remain contained, and the sector's profitability has recovered following earlier challenges related to foreign currency lending legacy issues. This financial sector strength, combined with Hungary's substantial foreign exchange reserves of €46.3 billion and persistent current account surplus of 2.3% of GDP, provides critical external financing capacity and reduces vulnerability to sudden stops in capital flows. However, these buffers cannot indefinitely compensate for weak productivity growth, demographic headwinds from population decline and ageing, and the structural competitiveness challenges posed by inadequate infrastructure investment resulting from frozen EU funds.

Rating Scenarios

Hungary's rating trajectory over the next 12 to 18 months will be determined primarily by fiscal consolidation credibility, progress on EU fund access, and the severity of trade-related economic disruption. The current BBB-/Baa2 ratings with predominantly negative outlooks signal elevated downgrade risk, with the country positioned just one to two notches above sub-investment grade status. A downgrade scenario would likely be triggered by a combination of factors: fiscal deficits persistently exceeding 5% of GDP without credible consolidation measures, permanent loss of substantial additional EU funding beyond the €1 billion already forfeited, and GDP growth remaining below 2% through 2026 due to sustained trade tensions and weak external demand. Standard & Poor's has explicitly highlighted concerns about pre-election spending and scepticism regarding Hungary's ability to draw down Recovery and Resilience Facility resources before the end-2026 deadline, suggesting the agency may move first if these risks materialise.

A rating affirmation scenario requires demonstration of fiscal discipline following the April 2026 elections, with deficits declining toward 3% of GDP by 2027 through a combination of revenue measures and expenditure restraint. Critically, Hungary would need to achieve meaningful progress on governance reforms sufficient to unlock at least a substantial portion of frozen EU funds, signalling to rating agencies that the country can maintain access to this vital financing source. Resolution or significant easing of US trade tariffs—whether through bilateral negotiations or broader trade policy shifts—would remove a major downside risk to growth projections and support the nascent recovery anticipated for late 2026. Under this scenario, agencies with negative outlooks would likely revise to stable, reducing near-term downgrade pressure whilst maintaining Hungary at the lower end of investment grade.

An upgrade scenario appears remote over the medium term given the depth of governance challenges and the structural nature of Hungary's institutional weaknesses. Fitch Ratings, which maintains a stable outlook, has indicated that upward rating momentum would require sustained fiscal consolidation with debt-to-GDP declining below 70%, comprehensive governance reforms that restore Hungary's standing within EU institutions, and consistent GDP growth above 3% driven by productivity improvements rather than cyclical factors. Such an outcome would likely require political change or fundamental policy reorientation following the 2026 elections, combined with normalisation of the external environment including resolution of trade tensions and recovery in key export markets. Even under optimistic scenarios, rating agencies would require several years of demonstrated performance before considering upgrades, given Hungary's track record of policy unpredictability and the erosion of institutional quality over the past decade. The country's ranking as the EU's most corrupt member state for three consecutive years represents a reputational burden that cannot be reversed quickly, requiring sustained commitment to transparency, judicial independence, and anti-corruption enforcement that extends well beyond electoral cycles.

Conclusion

Hungary's BBB-/Baa2 sovereign credit rating reflects a precarious equilibrium between robust macroeconomic fundamentals and profound governance challenges that increasingly constrain the country's fiscal flexibility and growth potential. The nation occupies the lowest tier of investment grade, with two of three major rating agencies maintaining negative outlooks that signal material downgrade risk over the medium term. This positioning underscores the fragility of Hungary's credit standing as it navigates an exceptionally challenging external environment characterised by frozen EU funds, escalating trade tensions with the United States, and systematic institutional weaknesses that have isolated it from traditional Western partners.

The credit profile's principal strengths derive from Hungary's well-capitalised banking sector, with a capital adequacy ratio of 20.5% providing substantial buffers against financial shocks, and its persistent current account surplus of 2.3% of GDP supported by foreign exchange reserves totalling €46.3 billion. These fundamentals offer meaningful protection against external financing pressures and distinguish Hungary from more vulnerable emerging market peers. The country's deep integration into European supply chains, particularly in the automotive sector, has historically generated substantial export revenues and employment, whilst EU membership provides institutional anchors and market access that underpin economic stability.

However, these strengths are increasingly overshadowed by governance deterioration that has triggered unprecedented financial consequences. Hungary's ranking as the EU's most corrupt member state for three consecutive years, with a Transparency International score of 41/100, has precipitated the permanent forfeiture of €1 billion in EU funds in January 2025—the first such loss in EU history—and the freezing of an additional €19 billion representing 34.8% of 2023 government revenue. This governance deficit directly constrains fiscal capacity at a juncture when infrastructure investment and economic diversification are critical to long-term competitiveness. The risk of losing substantial Recovery and Resilience Facility resources, estimated at 5% of GDP, if Hungary fails to meet 27 super-conditions by the end-2026 deadline, represents a material fiscal cliff that could necessitate abrupt consolidation or further ratings pressure.

The external environment compounds these domestic vulnerabilities. US tariffs averaging 18.8% on Hungarian exports, with particularly severe 25% levies on vehicles that constitute 40% of exports to the United States, threaten to reduce GDP by 1.4-2.3% in 2025. Indirect effects through Germany, Hungary's largest trading partner accounting for substantial automotive supply chain integration, amplify these headwinds. The economy's stagnation over the past three years, with cumulative real growth near zero, reflects both cyclical weakness in European demand and structural constraints from underinvestment and governance failures. Interest costs projected to exceed 4% of GDP in 2025, representing 11.9% of government revenues, further limit fiscal space for countercyclical measures or growth-enhancing expenditure.

Hungary's strategic pivot toward Chinese investment, now comprising 80% of new foreign direct investment, offers partial mitigation of Western funding constraints but introduces new dependencies that complicate geopolitical positioning and may generate additional tensions with EU and NATO partners. This reorientation reflects pragmatic adaptation to frozen EU funds but carries long-term risks to institutional alignment and strategic autonomy. The government's fiscal consolidation efforts, whilst acknowledged by Fitch Ratings' stable outlook, face credibility challenges given pre-election spending pressures ahead of the 2026 parliamentary elections and projected deficits of 4.5% of GDP that exceed official targets.

The credit trajectory over the next 12-24 months hinges critically on three factors: the government's ability to implement governance reforms sufficient to unlock frozen EU funds, the evolution of US-EU trade relations and their impact on Hungary's export-dependent economy, and fiscal discipline in the context of electoral pressures. A nascent recovery projected for 2026, contingent on easing trade tensions and potential post-election governance improvements, offers a constructive scenario, but execution risks remain substantial. The negative outlooks from S&P and Moody's indicate that downgrade to sub-investment grade represents a material risk if governance failures persist, EU fund access remains blocked, or external shocks prove more severe than currently anticipated. Conversely, meaningful progress on institutional reforms, successful navigation of trade headwinds, and credible fiscal consolidation could stabilise the rating and potentially support outlook revisions to stable over the medium term. Hungary's credit standing thus remains highly contingent on policy choices and external developments that will unfold over the coming quarters, with limited margin for adverse surprises given the country's position at the investment grade threshold.