France

Executive Summary

France confronts an unprecedented convergence of fiscal deterioration and political fragmentation that has fundamentally weakened its sovereign credit profile. All three major rating agencies downgraded or revised France's outlook in autumn 2025, with Fitch and S&P stripping the country of its double-A status through downgrades to A+ in September and October respectively, whilst Moody's maintained its Aa3 rating but revised the outlook to negative in October. The rating actions followed the collapse of three governments within twelve months, culminating in Prime Minister François Bayrou's ouster via no-confidence vote and his successor Sébastien Lecornu's politically expedient suspension of the 2023 pension reform until 2028. France now carries the highest fiscal deficit in the European Union at 5.8% of GDP, with public debt projected to reach 121% of GDP by 2027-2028 absent significant corrective measures. French 10-year bond yields have widened to 80 basis points above German Bunds—approaching Italian levels—whilst the country now offers higher yields than Spain despite historically stronger fundamentals, signalling material erosion in market confidence.

The economic backdrop reflects stagnation rather than crisis, with growth decelerating sharply from post-pandemic recovery rates to a projected 0.6-0.8% in 2025—the weakest performance since 2020. Fiscal consolidation of approximately 1% of GDP, combined with elevated political uncertainty, has depressed business investment and consumer confidence, whilst weak external demand from Germany constrains export-led recovery. France's labour market provides a notable counterpoint to this weakness, with the employment rate reaching a historic high of 69.3% in Q1 2025, whilst inflation has moderated to 0.9-1.2% in 2025 following France's relatively successful navigation of the 2022-2023 energy shock through limited Russian gas dependence and aggressive price controls. The current account has returned to marginal surplus after years of deficit, reflecting weak domestic demand rather than improved competitiveness.

The central challenge facing France is whether its institutional strengths can overcome political dysfunction before market confidence deteriorates further. The country must reduce its deficit by 2.8 percentage points by 2029 under European Union oversight through a €120 billion consolidation plan, yet legislative fragmentation has rendered the National Assembly effectively ungovernable, with no coalition commanding a stable majority. All three rating agencies identified similar downgrade triggers: further evidence of durably weakened legislative institutions, continued difficulties implementing fiscal consolidation measures, pension reform reversal, and debt-to-GDP approaching 125%. The suspension of pension reform until 2028—reversing the increase in retirement age to 64—represents precisely the type of structural backsliding that agencies warned would precipitate further downgrades, whilst the collapse of three governments in rapid succession demonstrates the fragility of France's current political equilibrium.

The forward outlook hinges on France's capacity to restore fiscal credibility through a credible, politically sustainable consolidation path whilst preserving the structural reforms that underpin long-term growth potential. France retains significant economic resilience through diversified industrial champions spanning aerospace, luxury goods, and pharmaceuticals, a robust banking sector with limited sovereign exposure, and Europe's strongest labour market dynamics. Moody's negative outlook provides a 12-24 month window for stabilisation before France loses its last double-A rating, creating urgency for political actors to forge consensus on fiscal adjustment. However, the combination of a deeply fragmented National Assembly, entrenched opposition to expenditure restraint across the political spectrum, and the approaching 2027 presidential election creates substantial implementation risk for any consolidation programme. Absent a durable political settlement that enables sustained fiscal adjustment, France faces the prospect of further rating downgrades, widening sovereign spreads, and potential loss of its status as a core eurozone credit.

Ratings Summary

France's creditworthiness deteriorated sharply in the final quarter of 2025, with all three major rating agencies either downgrading the sovereign or revising their outlook to negative. Fitch Ratings initiated the downgrades on 12 September 2025, cutting France from AA- to A+ with a Stable outlook following the collapse of Prime Minister François Bayrou's government via no-confidence vote. This action stripped France of its double-A status for the first time in the Fifth Republic's history. S&P Global Ratings followed on 18 October with an unscheduled downgrade to A+ with Stable outlook, brought forward by six weeks after Prime Minister Sébastien Lecornu survived two no-confidence votes only by suspending the 2023 pension reform until 2028. Moody's Investors Service affirmed its Aa3 rating on 25 October but revised the outlook from Stable to Negative, signalling potential downgrade within 12 to 24 months. The convergence of rating actions reflects unprecedented concern about France's ability to implement fiscal consolidation amidst profound political fragmentation, with all three agencies now effectively assessing France at single-A equivalent levels—the lowest creditworthiness in modern French history. Moody's negative outlook provides a critical window for stabilisation before France loses its last remaining double-A rating, though the agency has explicitly warned that further evidence of durably weakened legislative institutions, continued difficulties implementing fiscal measures, pension reform reversal, or debt-to-GDP approaching 125% would trigger downgrade. French 10-year bond yields widened to 80 basis points above German Bunds during the crisis, approaching Italian levels and trading above Spanish yields despite France's historically stronger economic fundamentals.

Credit Ratings and Outlook

France experienced unprecedented credit deterioration during the third and fourth quarters of 2025 as acute political instability compounded persistent fiscal challenges. The sovereign endured a rapid succession of rating actions across all three major agencies, culminating in the loss of its double-A status and marking the lowest creditworthiness assessment in modern French history. Fitch Ratings initiated the downgrade cycle on 12 September, reducing France from AA- to A+ following the collapse of Prime Minister François Bayrou's government through a no-confidence vote. This action stripped France of its double-A rating for the first time in the Fifth Republic's history. S&P Global Ratings followed with an unscheduled downgrade to A+ on 18 October, bringing forward its review by six weeks after PM Sébastien Lecornu narrowly survived two no-confidence motions only by suspending the politically contentious 2023 pension reform until 2028. Moody's Investors Service affirmed its Aa3 rating on 25 October but revised the outlook from stable to negative, signalling potential downgrade within twelve to twenty-four months. All three agencies now effectively rate France at single-A equivalent levels.

The rating actions revealed striking convergence in analytical themes. Fitch Ratings projects French government debt rising from 113.2% of GDP to 121% by 2027, noting explicitly that there exists "no clear horizon for debt stabilisation" under current policy trajectories. The agency emphasised that the fiscal deficit will remain above 5% of GDP through the 2026-2027 period despite official government consolidation targets. S&P Global Ratings highlighted that "political uncertainty will affect the French economy by dragging on investment activity," projecting debt reaching 121% of GDP by 2028 absent significant additional fiscal measures beyond those currently legislated. Moody's assessment focused particularly on institutional degradation, warning of "increased risk that fragmentation of the country's political landscape will continue to impair the functioning of France's legislative institutions." The agency specifically cautioned against sustained rollback of structural reforms, particularly the pension system increase to age 64, which it views as essential to long-term fiscal sustainability.

Current Rating Positions

| Agency | Rating | Outlook | Last Action | Previous Rating |

|---|---|---|---|---|

| Fitch Ratings | A+ | Stable | 12 September 2025 (Downgrade) | AA- |

| S&P Global Ratings | A+ | Stable | 18 October 2025 (Downgrade) | AA- |

| Moody's Investors Service | Aa3 | Negative | 25 October 2025 (Outlook revision) | Aa3 (Stable) |

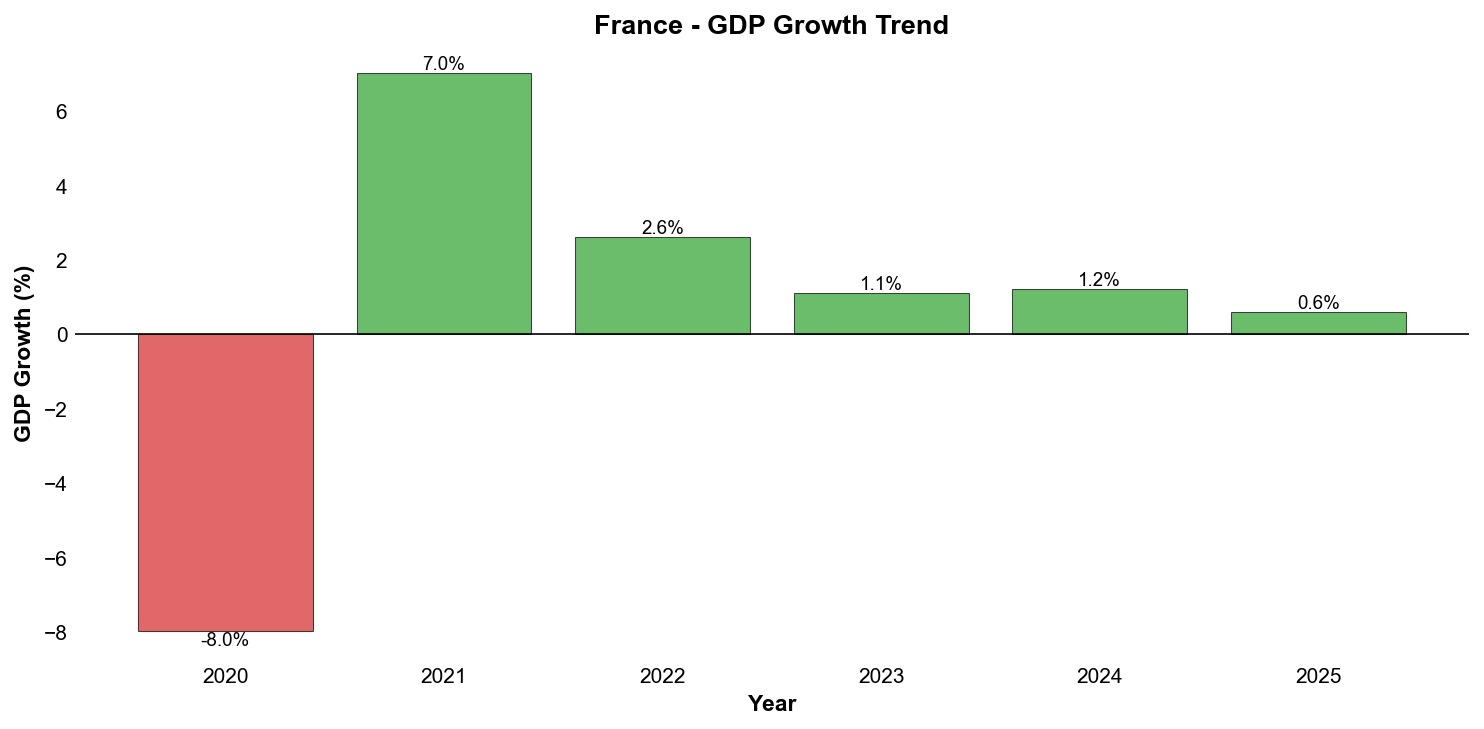

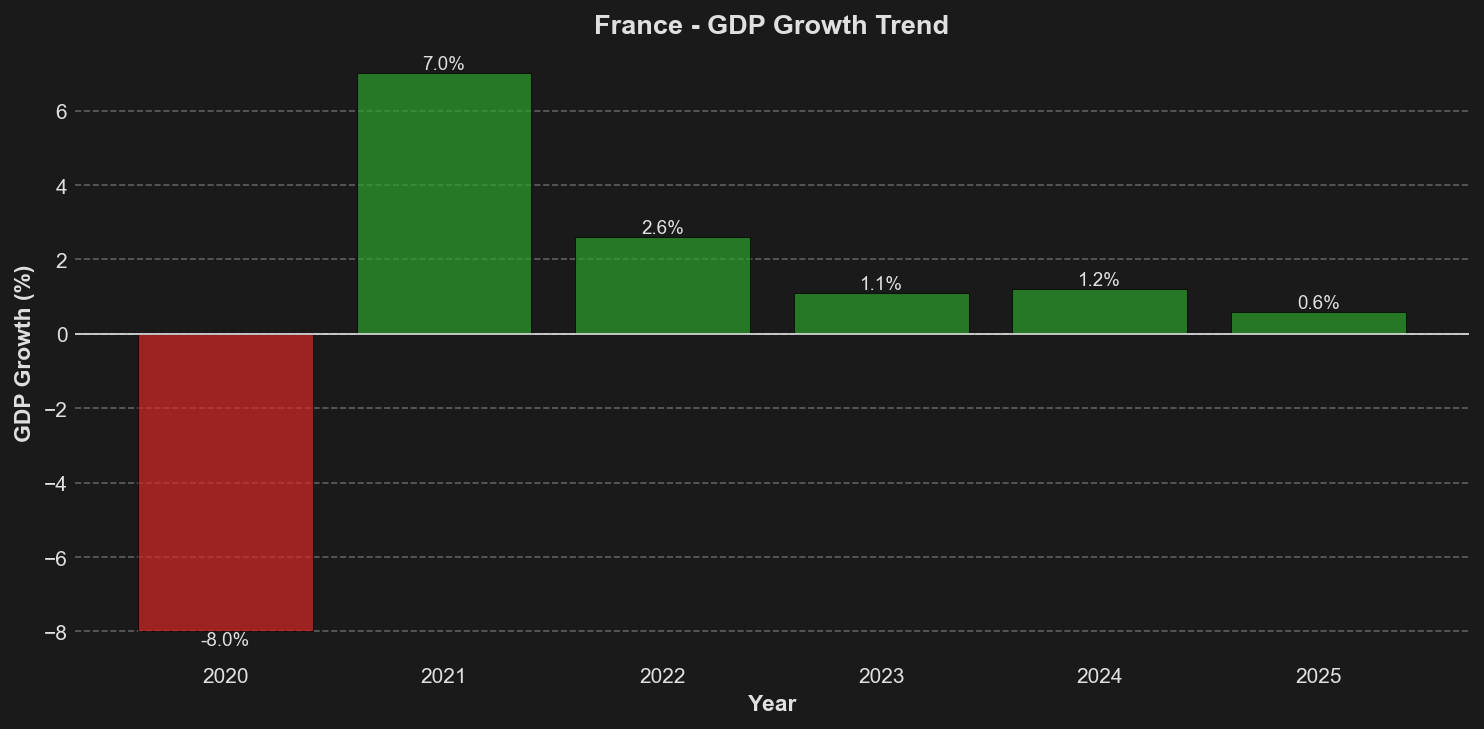

*Historical GDP growth trends showing annual percentage changes, with color coding for positive (green) and negative (red) growth periods.*

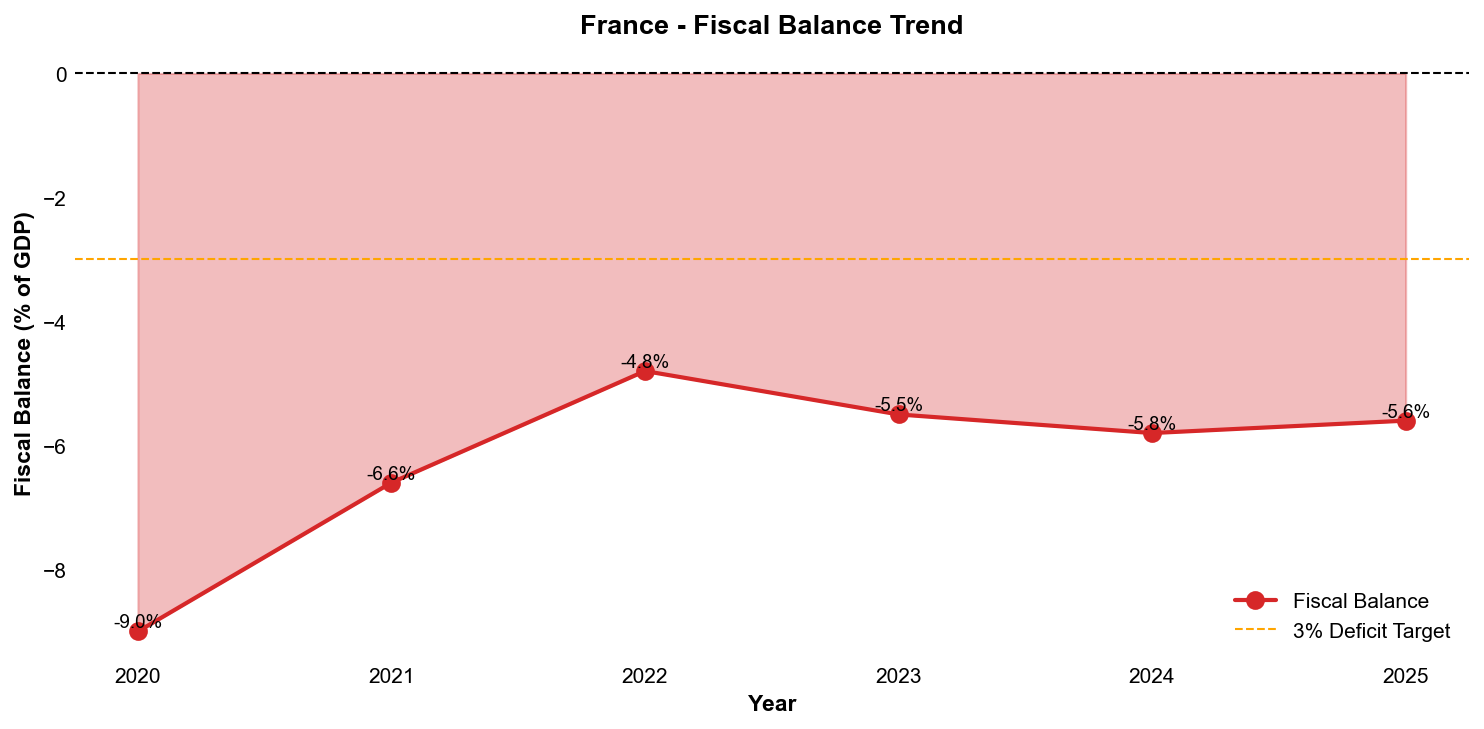

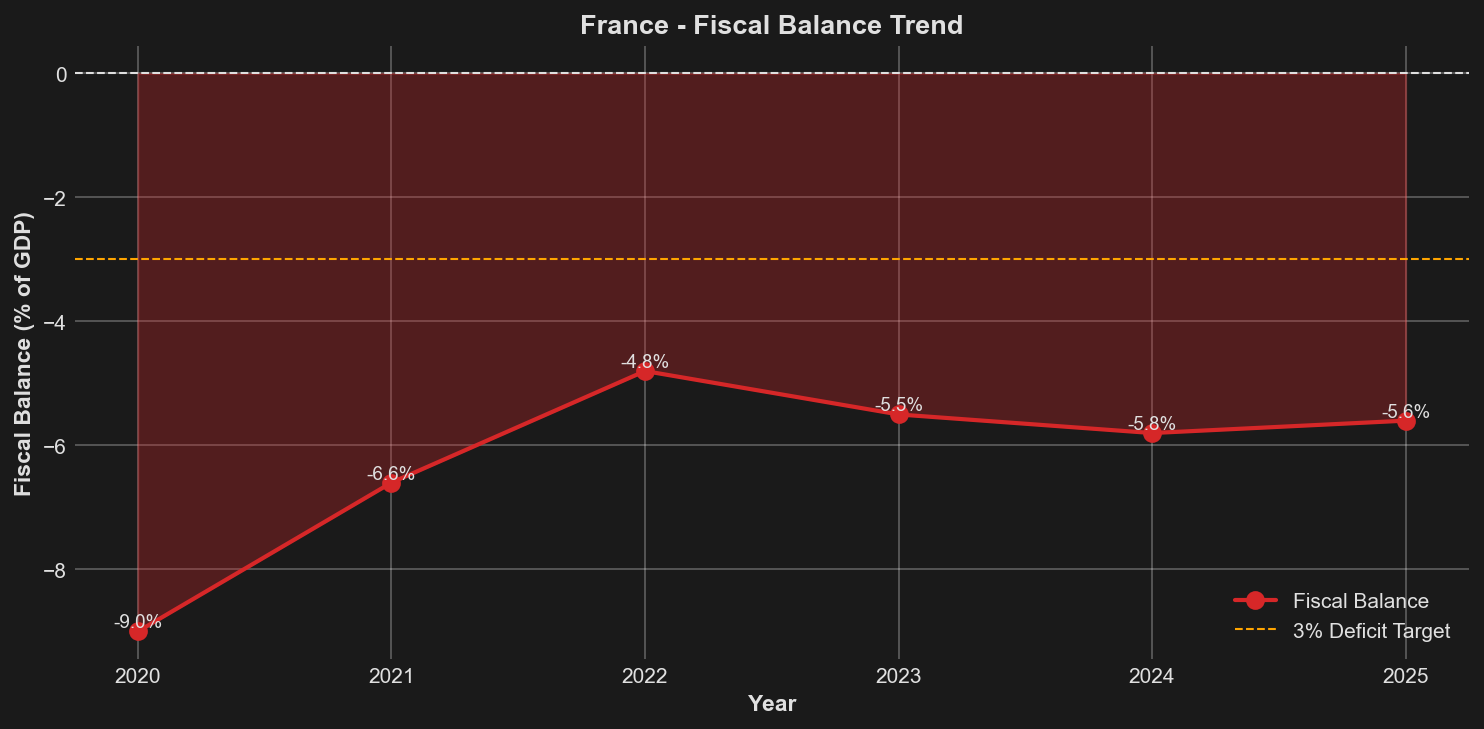

*Fiscal balance as percentage of GDP, showing government surplus (positive) or deficit (negative) positions over time.*

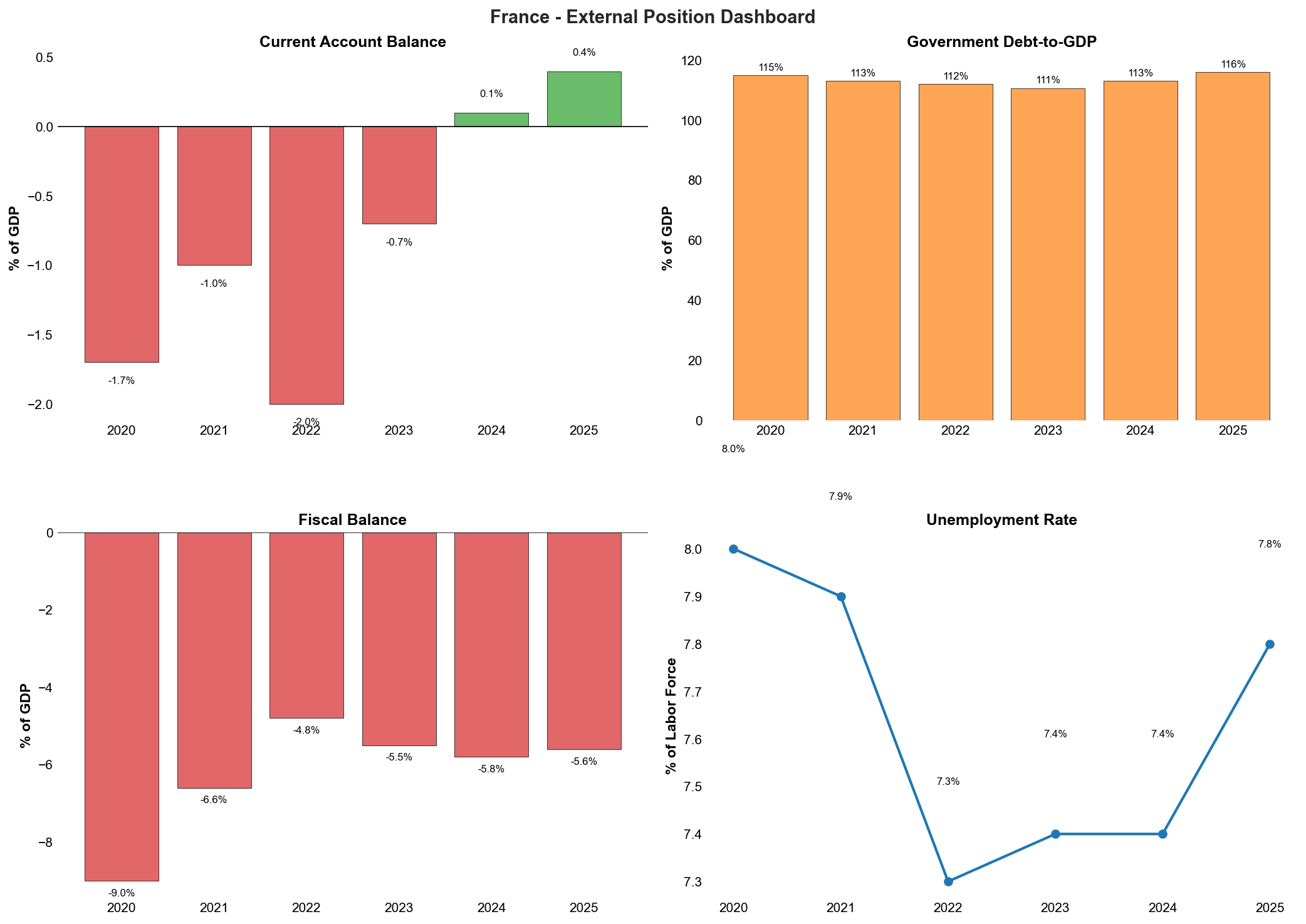

*Comprehensive external position dashboard showing foreign exchange reserves, current account balance, and unemployment trends.*

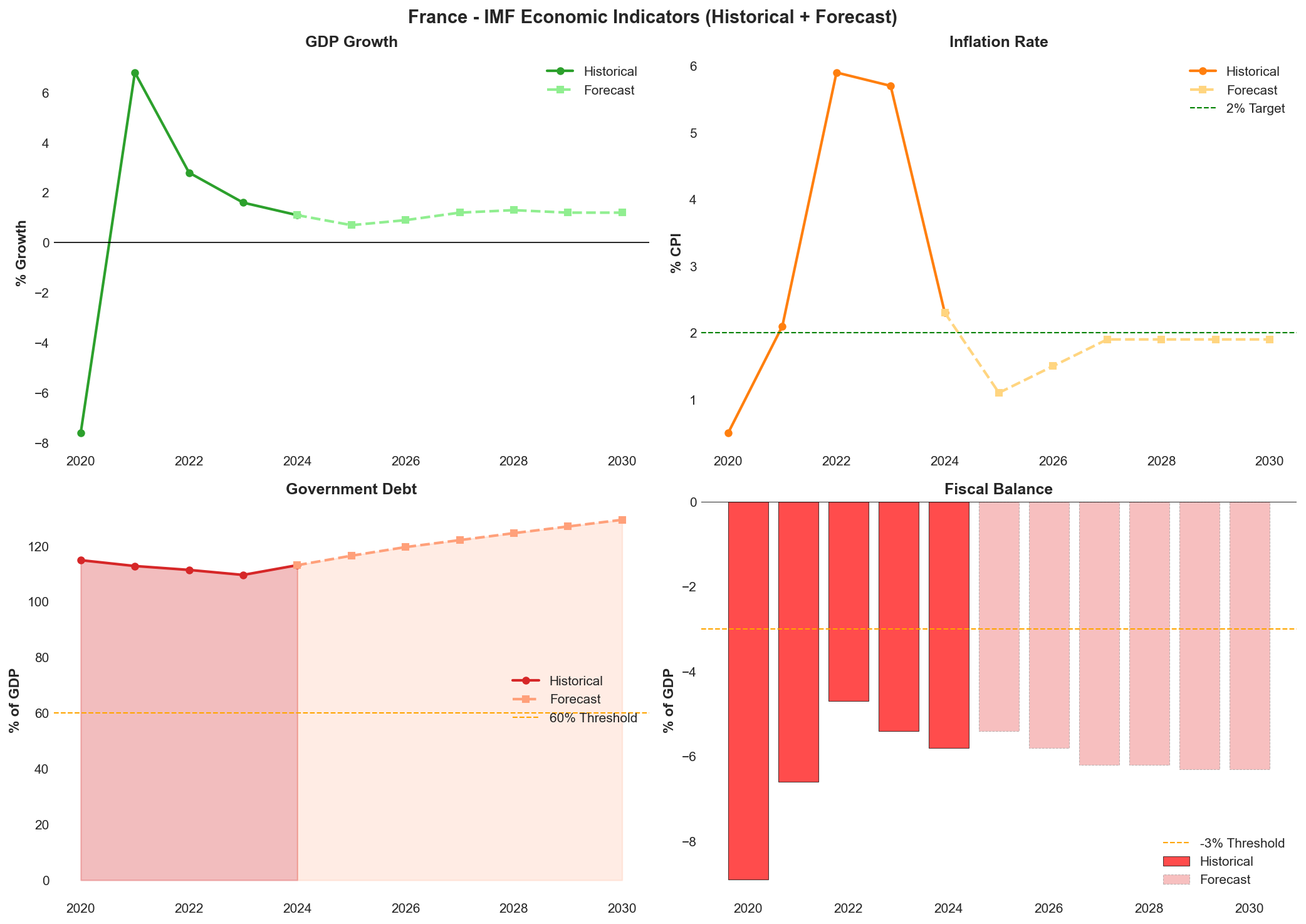

*Comprehensive view of key macroeconomic indicators from IMF data, showing historical trends (2020-2024) and medium-term forecasts through 2030 for GDP growth, inflation, government debt, and fiscal balance.*

All three agencies articulated similar downgrade triggers in their rating rationales. These include further evidence of durably weakened legislative institutions that prevent effective governance, continued difficulties implementing the fiscal consolidation measures required under the EU's Excessive Deficit Procedure, reversal of the 2023 pension reform that would materially worsen long-term fiscal projections, and government debt-to-GDP ratios approaching 125%. The market response to these rating actions proved severe. French ten-year government bond yields widened to 80 basis points above German Bunds, approaching spreads historically associated with Italian sovereign debt despite France's substantially stronger economic fundamentals. France now offers higher yields than Spain across the maturity curve, representing a significant inversion of traditional eurozone credit hierarchies.

France retains one critical advantage in this deteriorated rating environment. Moody's negative outlook provides a twelve to twenty-four month observation window before the agency would likely proceed with a downgrade, offering French policymakers a defined timeframe to demonstrate fiscal and political stabilisation. Loss of the Aa3 rating would leave France rated single-A across all three major agencies, a threshold that could trigger mechanical selling by investment mandates restricted to double-A or higher sovereigns and further complicate debt management for a sovereign issuing approximately €260 billion annually.

2. Economic Performance and Indicators

France's economic trajectory reflects the tension between underlying resilience and mounting fiscal constraints that increasingly weigh on growth prospects. Real GDP contracted 8.0% in 2020 before rebounding strongly at 7.0% in 2021, but growth decelerated sharply to 2.6% in 2022, 1.1% in 2023, and 1.2% in 2024. The 2025 consensus projects just 0.6-0.8% growth—the weakest performance since the pandemic—as fiscal consolidation of approximately 1% of GDP combines with political uncertainty to depress business investment and consumer confidence. The IMF, OECD, and European Commission all project subdued recovery to 0.9-1.3% in 2026, constrained by fiscal headwinds and weak external demand from Germany. Looking further ahead, the IMF's medium-term projections show growth stabilising at 1.2% by 2030, suggesting France faces an extended period of below-potential expansion as fiscal adjustment continues to constrain domestic demand.

| Indicator | 2021 | 2022 | 2023 | 2024 | 2025F | 2026F |

|---|---|---|---|---|---|---|

| GDP Growth (%) | 6.8 | 2.8 | 1.6 | 1.1 | 0.7 | 0.9 |

| Inflation (%) | 2.1 | 5.9 | 5.7 | 2.3 | 1.1 | 1.5 |

| Debt-to-GDP (%) | 112.8 | 111.4 | 109.6 | 113.1 | 116.5 | 119.6 |

| Fiscal Balance (%) | -6.6 | -4.7 | -5.4 | -5.8 | -5.4 | -5.8 |

| Current Account (%) | 0.3 | -1.4 | -1.0 | 0.1 | -0.1 | -0.2 |

| Unemployment (%) | 7.9 | 7.3 | 7.3 | 7.4 | 7.6 | 7.5 |

Source: IMF World Economic Outlook Database (January 2026)

Inflation dynamics proved favourable relative to European peers during the energy crisis. France weathered the 2022-2023 energy shock with peak inflation of 4.9-5.2%—below the eurozone average—thanks to limited Russian gas dependence and aggressive price controls on electricity and gas. Inflation moderated to 2.3% in 2024 and is projected at just 0.9-1.2% in 2025, undershooting the ECB's 2% target. The IMF projects inflation returning to 1.9% by 2030, consistent with the ECB's medium-term objective. This disinflationary environment provides monetary policy space as the ECB continues rate cuts, though France's predominance of fixed-rate lending limits transmission compared to variable-rate markets.

The fiscal trajectory presents the most acute concern for France's creditworthiness. The deficit widened from 5.5% of GDP in 2023 to 5.8% in 2024—the highest in the European Union—driven by revenue shortfalls and continued spending pressures. Despite government commitments to reduce the deficit to 5.6% in 2025, implementation risks remain elevated given political fragmentation. More troubling is the medium-term outlook: the IMF projects the fiscal deficit deteriorating to 6.3% of GDP by 2030, suggesting France's consolidation efforts will fall substantially short of EU requirements. This persistent deficit trajectory drives debt-to-GDP from 113.0% in 2024 to a projected 116.0% in 2025, with the IMF forecasting further deterioration to 129.4% by 2030. This places France on an unsustainable debt path absent significant policy correction, approaching the 125% threshold identified by rating agencies as a potential downgrade trigger.

The labour market represents a genuine bright spot amidst fiscal challenges. The employment rate reached 69.3% in Q1 2025—a historic high—whilst unemployment held steady at 7.4% through 2024. The IMF projects unemployment declining to 7.0% by 2030, reflecting structural improvements from past labour market reforms. However, near-term projections show unemployment rising modestly to 7.8% in 2025 as fiscal consolidation and weak growth weigh on job creation. The current account balance has improved markedly, swinging from deficits of 1.7-2.0% of GDP in 2020-2022 to near-balance or modest surplus of 0.1-0.4% in 2024, though a return to deficit of 0.6% is projected for 2025. The IMF's medium-term forecast shows the current account strengthening to a surplus of 1.6% of GDP by 2030, suggesting improved external competitiveness as domestic demand remains constrained by fiscal adjustment.

3. Net Foreign Assets and External Position

France's external position presents a paradox: structural deterioration in net foreign assets alongside near-term current account stabilisation that masks underlying competitiveness challenges. The country's net international investment position (NIIP) deteriorated from -21.4% of GDP in 2019 to approximately -28% by end-2024, reflecting persistent current account deficits during 2020-2023 and valuation losses on foreign assets. This places France amongst the weaker external positions in the eurozone core, though well above peripheral economies and cushioned by the country's reserve currency status and deep capital markets.

The current account trajectory reveals cyclical improvement masking structural weakness. After widening to -2.0% of GDP in 2022—driven by energy import costs following Russia's invasion of Ukraine—the deficit narrowed sharply to -0.7% in 2023 and swung to a modest surplus of +0.1% to +0.4% in 2024 as energy prices normalised and tourism revenues recovered to record levels. However, this improvement proves fragile: consensus forecasts project a return to deficit of -0.6% in 2025 as weak domestic demand constrains imports whilst export growth remains anaemic. The IMF's medium-term projection of a +1.6% surplus by 2030 appears optimistic absent significant competitiveness gains, relying heavily on assumptions of sustained energy price moderation and robust services exports.

France's goods trade balance remains structurally challenged, with the deficit hovering near €100 billion annually despite cyclical improvements. The country has lost export market share in key manufacturing sectors—particularly automobiles and machinery—to German and Asian competitors, whilst high labour costs and regulatory complexity constrain industrial competitiveness. The services surplus of approximately €50-60 billion provides partial offset, driven by tourism (France remains the world's leading destination by arrivals), business services, and intellectual property receipts. Yet this services strength proves vulnerable to global economic slowdown and faces intensifying competition from Southern European destinations.

The composition of France's external liabilities warrants careful monitoring. Gross external debt reached approximately 240% of GDP in 2024, though this figure reflects France's role as a major financial centre with substantial inter-company lending and banking sector positions rather than sovereign vulnerability per se. Non-resident holdings of French government debt stood at approximately 50% of outstanding OATs in mid-2025—down from 55% in 2022 as domestic banks absorbed issuance—providing some insulation from external funding shocks whilst maintaining sufficient foreign participation to ensure market liquidity. The recent widening of French-German spreads to 80 basis points, however, signals growing foreign investor discrimination that could accelerate should fiscal consolidation falter.

France benefits from several mitigating factors that reduce external vulnerability despite the negative NIIP. The country issues debt in its own currency within the eurozone framework, eliminating direct currency mismatch risk whilst retaining ECB backstop credibility through potential Transmission Protection Instrument activation. French multinational corporations and banks maintain substantial foreign assets—approximately €8 trillion gross—providing natural hedges and repatriation capacity in stress scenarios. The current account deficit remains modest in absolute terms and readily financeable through normal capital market channels, with no evidence of sudden stop risk.

Nevertheless, the external position trajectory compounds fiscal concerns in rating agency assessments. The combination of rising government debt—projected by the IMF to reach 129.4% of GDP by 2030—and deteriorating NIIP creates a twin deficit dynamic that constrains policy flexibility. Should political dysfunction prevent fiscal consolidation, France faces the prospect of simultaneous sovereign and external financing pressures that could trigger non-linear market reactions. The country's external position thus represents a latent rather than immediate vulnerability: manageable under baseline scenarios but capable of amplifying stress should domestic political crisis erode the institutional credibility that currently anchors foreign investor confidence.

3. Credit Strengths and Vulnerabilities

Strengths

France retains formidable structural advantages that distinguish it from peripheral eurozone economies despite acute near-term challenges. The country operates the eurozone's most resilient labour market, with the employment rate reaching a historic 69.3% in Q1 2025—substantially above the European average and reflecting two decades of structural reforms. This labour market strength underpins consumption resilience even as business investment falters, providing a stabilising force during political turbulence. Unemployment at 7.4-7.8% remains elevated by northern European standards but represents significant improvement from the 10% levels that prevailed through much of the 2010s, demonstrating the cumulative impact of training programmes, apprenticeship expansion, and labour market flexibility measures implemented since the Macron presidency began in 2017.

The French economy benefits from exceptional diversification across high-value sectors. Industrial champions span aerospace (Airbus, Safran), luxury goods (LVMH, Kering, Hermès), pharmaceuticals (Sanofi), energy (TotalEnergies, EDF), and defence (Dassault, Thales), providing export resilience and technological depth that few European economies can match. This industrial base generated a current account surplus of 0.1-0.4% of GDP in 2024—a marked improvement from the 2.0% deficit in 2022—as energy import costs normalised following the Russia-Ukraine shock. France's limited dependence on Russian gas proved strategically advantageous, enabling the country to weather the energy crisis with peak inflation of just 4.9-5.2% compared to double-digit rates in several European peers.

The banking sector emerged from the 2020 pandemic shock with enhanced resilience. French banks maintain robust capitalisation with Common Equity Tier 1 ratios consistently above regulatory requirements, whilst non-performing loan ratios remain contained below 3%. The sector's diversification across retail banking, corporate finance, and insurance—combined with significant international operations—provides earnings stability even during domestic economic weakness. Deposit funding remains stable, and the predominance of fixed-rate mortgages insulates household balance sheets from interest rate volatility, reducing financial stability risks compared to variable-rate markets.

Institutional quality represents a fundamental strength despite current political dysfunction. France's civil service tradition ensures policy continuity across government changes, whilst the Banque de France maintains rigorous oversight of financial institutions. The country's legal framework, property rights protection, and regulatory predictability support long-term investment, even as short-term political uncertainty weighs on business confidence. France's position as a core eurozone member provides implicit backstops through ECB liquidity facilities and European Stability Mechanism access, though these safety nets remain untested for a G7 economy.

Vulnerabilities

France confronts its most severe fiscal crisis since the Fifth Republic's founding, with the general government deficit reaching 5.8% of GDP in 2024—the highest in the European Union and more than double the Stability and Growth Pact's 3% ceiling. This deficit reflects not merely cyclical weakness but structural imbalances, as government spending reached 57.3% of GDP—the highest ratio among advanced economies—whilst tax revenues at 48.1% of GDP already represent near-maximum extraction capacity. The deficit persisted at elevated levels even during the 2021-2022 recovery, demonstrating that France's fiscal challenges transcend economic cycles. Both Fitch and S&P project debt rising from 113.0% of GDP in 2024 to 121% by 2027-2028 under current policies, with Fitch explicitly stating there is "no clear horizon for debt stabilization" absent substantial additional measures.

Political fragmentation has rendered France effectively ungovernable under current institutional arrangements. Three governments collapsed within twelve months—an unprecedented frequency in Fifth Republic history—as the National Assembly fractured into three irreconcilable blocs: the left-wing Nouveau Front Populaire, President Macron's centrist coalition, and Marine Le Pen's Rassemblement National. Prime Minister François Bayrou fell to a no-confidence vote in August 2025, whilst successor Sébastien Lecornu survived two such votes in October only by suspending the 2023 pension reform until 2028—a concession that directly contradicts fiscal consolidation requirements. This political paralysis places France's €120 billion consolidation plan at severe implementation risk, as rating agencies explicitly warned. Moody's noted "increased risk that fragmentation of the country's political landscape will continue to impair the functioning of France's legislative institutions," whilst S&P emphasised that "political uncertainty will affect the French economy by dragging on investment activity."

The pension reform reversal exemplifies how political constraints undermine fiscal sustainability. The 2023 legislation raising the retirement age from 62 to 64 was projected to save €17.7 billion annually by 2030—equivalent to 0.6% of GDP—yet this measure now stands suspended until 2028 as the price of government survival. France's pension system already operates at a deficit, and demographic pressures intensify as the population ages. The dependency ratio continues deteriorating, with the proportion of over-65s projected to rise from 21% in 2024 to 26% by 2040, placing inexorable pressure on both pension and healthcare expenditures. Absent the retirement age increase, France faces either substantial tax increases—politically toxic given already-record tax burdens—or deeper cuts to other spending categories.

Market confidence has deteriorated markedly, with tangible financial consequences. French 10-year bond yields widened to 80 basis points above German Bunds—approaching Italian levels despite France's historically stronger fundamentals and core eurozone status. France now offers higher yields than Spain, a reversal of traditional risk hierarchies that reflects investor concern about political dysfunction rather than economic fundamentals alone. Credit default swap spreads similarly widened, whilst equity market performance lagged European peers as uncertainty depressed valuations of domestically-focused companies. The rating downgrades by Fitch and S&P to A+ levels—stripping France of double-A status—increase borrowing costs and reduce the investor base, as certain institutional mandates restrict holdings below specified rating thresholds.

Structural competitiveness challenges persist beneath near-term political drama. France's unit labour costs remain elevated relative to Germany, constraining export competitiveness in price-sensitive sectors. Business investment growth has consistently underperformed European peers, reflecting regulatory complexity, high corporate taxation despite recent reforms, and labour market rigidities that persist despite improvements. The country's innovation performance, whilst strong in specific sectors like aerospace and pharmaceuticals, lags leaders like Germany and Sweden in broader measures of research intensity and patent output. Youth unemployment at 17-18%—more than double the overall rate—indicates persistent skills mismatches and labour market segmentation that constrain long-term growth potential.

Opportunities

The European Union's fiscal framework revision provides France with a structured pathway to restore credibility if political conditions permit implementation. Under the reformed Stability and Growth Pact, France must reduce its deficit by 2.8 percentage points by 2029—a demanding but achievable target that would bring the deficit to 3.0% of GDP and stabilise debt dynamics. The EU's shift towards country-specific adjustment paths rather than uniform rules offers flexibility to phase consolidation in ways that minimise growth damage, potentially concentrating measures in years of stronger cyclical performance. Successfully executing this plan would demonstrate that France's institutional capacity can overcome political fragmentation, potentially triggering rating upgrades as agencies reward credible fiscal adjustment.

Monetary policy easing by the European Central Bank provides cyclical support as France navigates fiscal consolidation. With inflation undershooting the 2% target at just 0.9-1.2% in 2025, the ECB continues reducing policy rates from their 2023 peaks, lowering debt service costs and supporting economic activity. France's predominance of fixed-rate mortgages means households benefit from lower rates primarily through refinancing rather than immediate payment reductions, but corporate borrowing costs decline more directly. This monetary accommodation creates space for fiscal tightening without triggering recession, provided consolidation is implemented gradually rather than through front-loaded austerity.

Structural reform momentum could accelerate if political circumstances shift. The 2017-2022 Macron presidency demonstrated that France can implement significant reforms—labour market flexibility, corporate tax reductions, apprenticeship expansion—when executive authority aligns with legislative support. Should the 2027 presidential and legislative elections produce a clearer governing majority, the reform agenda could resume with measures to enhance competitiveness, reduce regulatory burdens, and modernise public services. France's civil service capacity enables rapid policy implementation once political decisions are taken, as demonstrated by the swift deployment of pandemic support programmes in 2020.

France's industrial policy positioning offers medium-term growth opportunities. The country secured substantial allocations under the EU's NextGenerationEU recovery programme, with funds designated for green transition, digitalisation, and industrial modernisation. Strategic sectors like electric vehicles, renewable energy, and advanced manufacturing benefit from both EU support and domestic initiatives such as the France 2030 investment plan. The reshoring trend in European supply chains following pandemic and geopolitical disruptions favours France's diversified industrial base and skilled workforce, potentially attracting investment that had previously migrated to lower-cost locations.

Threats

The most immediate threat involves further political deterioration triggering additional rating downgrades and market stress. Moody's negative outlook signals potential downgrade to A1 within 12-24 months if fiscal consolidation stalls or institutional dysfunction persists, which would leave France rated single-A by all three major agencies. Such downgrades could trigger non-linear market reactions, as certain institutional investors face mandate restrictions on sub-AA holdings, forcing portfolio reallocation and potentially creating self-reinforcing dynamics where higher borrowing costs worsen fiscal metrics. The precedent of Italy's 2011 crisis—where political uncertainty catalysed market panic despite manageable fundamentals—demonstrates that core eurozone members are not immune to confidence shocks.

The 2027 electoral cycle introduces profound uncertainty with potential for radical policy shifts. Marine Le Pen's Rassemblement National leads opinion polls for the presidential election, whilst the left-wing Nouveau Front Populaire commands substantial parliamentary support. Both formations advocate policies—pension reform reversal, wealth tax restoration, increased public spending—that directly contradict fiscal consolidation requirements and would likely trigger immediate rating downgrades and market turbulence. Even if centrist forces prevail, the election campaign will constrain policy action through 2026-2027, compressing the timeline for implementing the €120 billion consolidation plan and increasing the risk of abrupt, growth-damaging measures if adjustment is delayed.

Debt sustainability risks intensify as the maturity wall approaches. France must refinance substantial debt volumes in coming years whilst simultaneously funding ongoing deficits, creating vulnerability to interest rate volatility. The debt-to-GDP ratio trajectory towards 121% by 2027-2028 approaches the 125% threshold that rating agencies identified as a downgrade trigger, leaving minimal margin for adverse shocks. Each percentage point increase in average borrowing costs adds approximately €30 billion to annual debt service—equivalent to 1% of GDP—creating a vicious cycle where higher rates worsen fiscal metrics and justify further rate increases. France's core eurozone status provides some insulation, but the widening spread to German Bunds demonstrates that market discipline is tightening.

External economic headwinds could derail France's fragile growth trajectory. Germany—France's largest trading partner—faces structural challenges in its automotive and industrial sectors, constraining demand for French exports. Potential trade tensions following the 2024 US presidential election threaten European exports, particularly in aerospace and luxury goods where France maintains strong positions. A broader eurozone slowdown would reduce French growth through both trade and confidence channels, worsening fiscal metrics and complicating consolidation efforts. The global economic environment offers limited support, with China's recovery disappointing and geopolitical tensions elevated.

Banking sector vulnerabilities could emerge if sovereign stress intensifies. French banks hold substantial domestic government debt, creating sovereign-bank linkages that proved destabilising during the eurozone crisis. Whilst current bank capitalisation appears adequate, a sharp widening of French spreads would impose mark-to-market losses on bond portfolios and potentially constrain lending capacity. The predominance of fixed-rate mortgages protects household debt service capacity but reduces banks' net interest margins in a rising rate environment, pressuring profitability. Any perception of banking sector weakness could trigger deposit flight or wholesale funding stress, forcing intervention and potentially creating fiscal contingent liabilities that worsen sovereign metrics.

Economic Performance and Indicators

France's economic trajectory reflects the tension between underlying resilience and mounting headwinds from fiscal consolidation and political uncertainty. Real GDP contracted 8.0% in 2020 during the pandemic before rebounding strongly at 7.0% in 2021, but growth decelerated sharply to 2.6% in 2022, 1.1% in 2023, and 1.2% in 2024. The 2025 consensus projects just 0.6-0.8% growth—the weakest performance since the pandemic—as fiscal consolidation of approximately 1% of GDP combines with political uncertainty to depress business investment and consumer confidence. The IMF, OECD, and European Commission all project subdued recovery to 0.9-1.3% in 2026, constrained by ongoing fiscal headwinds and weak external demand from Germany.

| Indicator | 2021 | 2022 | 2023 | 2024 | 2025F | 2026F |

|---|---|---|---|---|---|---|

| GDP Growth (%) | 6.8 | 2.8 | 1.6 | 1.1 | 0.7 | 0.9 |

| Inflation (%) | 2.1 | 5.9 | 5.7 | 2.3 | 1.1 | 1.5 |

| Debt-to-GDP (%) | 112.8 | 111.4 | 109.6 | 113.1 | 116.5 | 119.6 |

| Fiscal Balance (%) | -6.6 | -4.7 | -5.4 | -5.8 | -5.4 | -5.8 |

| Current Account (%) | 0.3 | -1.4 | -1.0 | 0.1 | -0.1 | -0.2 |

| Unemployment (%) | 7.9 | 7.3 | 7.3 | 7.4 | 7.6 | 7.5 |

Source: IMF World Economic Outlook Database (January 2026)

Growth Dynamics and Structural Factors

The deceleration in French growth reflects both cyclical and structural factors. Domestic demand has weakened as households face real income pressures despite moderating inflation, whilst business investment has stalled amid political uncertainty surrounding tax policy and structural reforms. The collapse of three governments within twelve months has created a policy vacuum that discourages capital expenditure decisions, particularly in sectors sensitive to regulatory frameworks. External demand provides limited support given Germany's industrial recession and broader eurozone weakness, constraining France's export-oriented manufacturing sectors.

Nevertheless, France retains structural advantages that prevent deeper contraction. The economy benefits from diversified industrial champions across aerospace, pharmaceuticals, luxury goods, and energy, providing resilience against sector-specific shocks. The services sector, which accounts for approximately 70% of GDP, has demonstrated relative stability despite manufacturing weakness. Tourism revenues remain robust, supported by France's position as the world's leading destination by visitor numbers. These factors establish a floor beneath growth even as political dysfunction weighs on sentiment and investment.

Inflation Trajectory and Price Dynamics

Inflation dynamics proved favourable relative to European peers throughout the energy crisis period. France weathered the 2022-2023 energy shock with peak inflation of 4.9-5.2%—below the eurozone average of approximately 8-10%—thanks to limited dependence on Russian gas and aggressive government-imposed price controls on electricity and gas tariffs. The "tariff shield" policy capped energy price increases for households and small businesses, absorbing fiscal costs estimated at €45 billion over 2022-2023 but preventing the wage-price spirals observed in other major economies.

Inflation moderated to 2.3% in 2024 and is projected at just 0.9-1.2% in 2025, undershooting the European Central Bank's 2% target. This disinflationary trend reflects normalising energy prices, weak domestic demand, and the lagged effects of previous monetary tightening. Core inflation has similarly declined, indicating limited second-round effects from the energy shock. The subdued inflation environment provides monetary policy space as the ECB continues its rate-cutting cycle, though France's predominance of fixed-rate mortgage lending limits transmission mechanisms compared to variable-rate markets such as Spain or Ireland.

Monetary Policy Environment and Financial Conditions

French monetary conditions are determined by European Central Bank policy, with the ECB having raised its deposit facility rate from -0.5% in mid-2022 to a peak of 4.0% in September 2023 before commencing rate cuts in mid-2024. The ECB reduced rates by 25 basis points in June, September, and December 2024, bringing the deposit rate to 3.25% by year-end, with market expectations of further cuts to approximately 2.0-2.25% by end-2025 as eurozone inflation converges towards target.

The transmission of monetary policy to the French economy differs from eurozone peers due to structural characteristics of the mortgage market. Approximately 95% of French residential mortgages carry fixed rates, typically with 15-25 year terms, insulating existing borrowers from rate increases but reducing the immediate impact of rate cuts on household disposable income. New mortgage origination has declined sharply since 2022 as higher rates reduced affordability, contributing to housing market cooling but avoiding the payment shock experienced in variable-rate markets.

Credit conditions for corporates have tightened moderately, with bank lending surveys indicating stricter standards and weaker demand. However, French banks remain well-capitalised and liquid, maintaining credit supply to viable businesses. The sovereign-bank nexus presents manageable risks despite rating downgrades, as French banks hold substantial sovereign debt but maintain diversified balance sheets and strong capital ratios above regulatory minimums. Widening sovereign spreads increase funding costs incrementally but have not triggered systemic stress given the absence of acute market dysfunction.

3. Political and Institutional Assessment

France confronts an unprecedented crisis of governability that threatens the Fifth Republic's institutional foundations. The collapse of three governments within twelve months—those of Prime Ministers Gabriel Attal, François Bayrou, and the near-collapse of Sébastien Lecornu's administration—represents the most severe political fragmentation since the constitution's adoption in 1958. This instability directly undermines France's capacity to implement the fiscal consolidation required under EU oversight, with the €120 billion deficit reduction plan facing severe implementation risk despite the country's historically robust institutional framework.

Parliamentary Fragmentation and Governance Paralysis

The June 2024 legislative elections produced a tripartite deadlock that has proven structurally ungovernable. The National Assembly fractured into three roughly equal blocs: the left-wing Nouveau Front Populaire coalition commanding approximately 193 seats, President Macron's centrist Ensemble alliance holding 166 seats, and Marine Le Pen's Rassemblement National with 143 seats in the 577-member chamber. No bloc approaches the 289-seat absolute majority required for stable governance, whilst ideological polarisation prevents coalition formation across the left-right divide. The centre-left Socialists refuse formal alliance with Macron's government, whilst the centre-right Les Républicains—holding the potential balance of power with approximately 45 seats—remain internally divided between cooperation and opposition.

This fragmentation has rendered France's constitutional mechanisms for executive authority increasingly precarious. Prime Minister Lecornu's government survived dual no-confidence motions in October 2025 only through an extraordinary political compromise: suspending the 2023 pension reform that raised the retirement age from 62 to 64 until after the 2027 presidential election. This represented a fundamental reversal of structural reform explicitly cited by rating agencies as essential for long-term fiscal sustainability. Lecornu subsequently invoked Article 49.3 of the constitution—which allows passage of legislation without parliamentary vote—to advance the 2026 budget, the fourth consecutive year this emergency provision has been deployed for fiscal legislation. Whilst constitutionally permissible, repeated use of Article 49.3 exposes each budget to immediate no-confidence votes, creating a quarterly cycle of political brinkmanship that prevents medium-term policy planning.

The structural nature of this deadlock distinguishes the current crisis from previous periods of cohabitation in French politics. Presidential elections are not scheduled until April-May 2027, whilst constitutional provisions prevent dissolution of the National Assembly before June 2025—one year after the previous election. France therefore faces a minimum eighteen-month period of minority government with no clear mechanism for resolution. Opinion polling suggests the 2027 elections may reproduce or intensify current fragmentation, with Marine Le Pen leading first-round presidential polling at 33-35%, followed by a centrist candidate at 22-25% and left-wing candidates collectively at 28-32%. The prospect of a Le Pen presidency—which would likely pursue significant departures from current fiscal and European policy—adds medium-term uncertainty to immediate governance challenges.

Fiscal Governance and EU Oversight

France's fiscal position has deteriorated to the most severe in the European Union, triggering formal excessive deficit procedures that impose binding consolidation requirements. The 2024 deficit reached 5.8% of GDP—the highest in the EU and more than double the Maastricht Treaty's 3% threshold—driven by a combination of pandemic-era spending that was never fully unwound, energy crisis support measures, and structural revenue weakness. Public debt stood at 113.0% of GDP in 2024, having reversed the modest decline achieved between 2020 and 2023. Under the EU's revised fiscal framework, France must reduce its deficit by 2.8 percentage points by 2029, requiring sustained annual consolidation of approximately 0.6-0.7% of GDP.

The government's fiscal strategy centres on a €120 billion consolidation plan spanning 2025-2029, with approximately two-thirds derived from expenditure restraint and one-third from revenue measures. The 2025-2026 component targets €60 billion in savings through public sector efficiency gains, subsidy reductions, and temporary tax increases on large corporations and high-income households. However, implementation faces severe political obstacles. The suspension of pension reform removes an estimated €8-10 billion in annual savings from 2028 onwards, whilst parliamentary opposition has already forced modifications to proposed spending cuts in healthcare, local government transfers, and education. The European Commission's autumn 2025 assessment noted "significant risks to fiscal targets" and warned that France may require additional measures beyond those currently proposed.

France's fiscal institutions provide some counterweight to political dysfunction. The Haut Conseil des Finances Publiques—an independent fiscal council—issues binding assessments of budget forecasts and has consistently warned that government projections rely on optimistic growth assumptions. The Cour des Comptes, France's supreme audit institution, maintains rigorous oversight of public expenditure and has documented systematic underperformance against fiscal targets since 2020. These institutions enhance transparency and constrain the most egregious forms of fiscal manipulation, yet they cannot compel parliamentary action when political will is absent. The contrast with Germany's constitutional debt brake or Switzerland's fiscal rules—which impose automatic corrections—highlights the limitations of advisory rather than binding fiscal frameworks.

Institutional Resilience and Administrative Capacity

Despite political turbulence, France retains significant institutional strengths that distinguish it from other fiscally stressed European sovereigns. The French civil service—particularly the elite corps of inspecteurs des finances and énarques trained at the École Nationale d'Administration's successor institutions—provides continuity and technical competence across government transitions. This administrative capacity enables policy implementation even during political instability, as evidenced by the successful deployment of pandemic support programmes and energy price controls despite concurrent governmental crises. France's prefectoral system, which embeds central government authority in regional administration, ensures policy execution independent of local political variations.

The French judiciary and regulatory framework demonstrate independence and effectiveness. The Conseil Constitutionnel exercises meaningful constitutional review, having struck down multiple provisions of recent budgets for procedural irregularities or violations of constitutional principles. Financial sector regulation through the Autorité de Contrôle Prudentiel et de Résolution maintains standards aligned with European Banking Authority requirements, whilst the Autorité des Marchés Financiers ensures capital market integrity. France scores in the 88th percentile globally on the World Bank's Government Effectiveness Index and the 86th percentile on Regulatory Quality, reflecting institutional capacity that exceeds most eurozone peers outside northern Europe.

However, political fragmentation increasingly constrains even robust institutions. Structural reforms in pensions, labour markets, and public sector efficiency require legislative action that the current parliament cannot deliver. The suspension of pension reform illustrates how political deadlock can reverse hard-won consolidation measures, whilst the inability to pass enabling legislation for EU recovery fund disbursements has delayed infrastructure investment. France risks entering a cycle where institutional quality erodes through prolonged political dysfunction—a pattern observed in Italy during the 2010s—unless the 2027 elections produce a governing majority capable of decisive action. The eighteen-month period until those elections represents a critical window in which France must demonstrate that its institutional foundations can withstand political stress without permanent damage to fiscal credibility.

Banking Sector and Financial Stability

France's banking sector enters the current crisis from a position of considerable strength, providing critical stability amid political and fiscal turbulence. The sector has undergone substantial reinforcement since the 2008-2012 financial crises, with major institutions now maintaining capital ratios well above regulatory minima and demonstrating resilient profitability despite compressed net interest margins. The four global systemically important banks—BNP Paribas, Crédit Agricole, Société Générale, and Groupe BPCE—collectively represent approximately 80% of domestic banking assets whilst maintaining significant international diversification that reduces concentration risk to French sovereign exposure.

Capital adequacy metrics reflect this strengthening trajectory. The aggregate Common Equity Tier 1 ratio for French significant institutions stood at 14.8% as of Q2 2025, comfortably exceeding the regulatory requirement of approximately 10.5% including buffers. BNP Paribas reported a CET1 ratio of 13.4%, Crédit Agricole 16.2%, Société Générale 13.1%, and Groupe BPCE 15.8%, providing substantial loss absorption capacity. These buffers have been accumulated through retained earnings during the post-pandemic recovery period, when French banks benefited from normalising credit costs and improving asset quality as government support measures prevented widespread corporate defaults.

Profitability has proven resilient despite challenging conditions. Return on equity across the sector averaged 8.2% in 2024, supported by rising interest rates that expanded net interest margins before the European Central Bank's pivot to monetary easing in mid-2024. The major banks have demonstrated effective cost discipline, with cost-to-income ratios declining to the 62-65% range through digital transformation initiatives and branch network optimisation. Non-performing loan ratios remain contained at approximately 2.3% of total loans as of Q3 2025, below the European average and reflecting both prudent underwriting standards and the strength of France's labour market, which has sustained household debt servicing capacity.

The sovereign-bank nexus nevertheless presents the primary vulnerability. French banks hold approximately €450 billion in French government debt across their balance sheets, representing roughly 15-18% of total assets for the major institutions. Under current accounting standards, securities held in the banking book are valued at amortised cost rather than market value, insulating regulatory capital from mark-to-market losses as French sovereign yields have widened. However, this accounting treatment does not eliminate economic risk. A sustained deterioration in French sovereign creditworthiness would transmit through multiple channels: direct valuation losses if securities are reclassified or sold, increased funding costs as bank credit ratings typically cannot exceed the sovereign rating by more than one to two notches, reduced value of government debt used as collateral in wholesale funding markets, and potential deposit flight if confidence erodes.

Rating agency methodologies explicitly link bank and sovereign creditworthiness through the sovereign ceiling concept. Moody's applies a two-notch uplift maximum above the sovereign rating for systemically important banks in advanced economies, meaning that if France were downgraded from Aa3 to A1, BNP Paribas and Crédit Agricole would face automatic downgrade pressure even absent deterioration in standalone credit profiles. S&P and Fitch apply similar constraints, though with marginally more flexibility for banks with substantial international diversification. The October 2025 downgrades by Fitch and S&P triggered corresponding reviews of French bank ratings, with BNP Paribas downgraded to A+ by both agencies whilst maintaining stable outlooks predicated on no further sovereign deterioration.

Funding and liquidity positions provide meaningful resilience. The loan-to-deposit ratio for French banks averaged 108% as of mid-2025, indicating moderate reliance on wholesale funding but within manageable parameters. Customer deposits totalling approximately €2.1 trillion provide a stable funding base, with retail deposits demonstrating minimal sensitivity to political developments thus far. French banks maintain substantial liquidity buffers, with liquidity coverage ratios averaging 145% and net stable funding ratios exceeding 115%, both comfortably above the 100% regulatory minima. Access to European Central Bank facilities provides additional backstop capacity, though reliance on central bank funding has declined to minimal levels as market conditions normalised following the pandemic.

The corporate and commercial real estate lending portfolios warrant monitoring given the fiscal consolidation trajectory. French banks hold approximately €950 billion in corporate loans, with meaningful exposure to sectors facing headwinds from reduced government spending, including construction, public services contractors, and defence-adjacent industries. Commercial real estate exposures of roughly €180 billion face valuation pressure from rising capitalisation rates and reduced transaction volumes, though residential mortgage portfolios of €1.1 trillion demonstrate robust performance supported by France's housing shortage and strict underwriting standards that have limited loan-to-value ratios to an average of 75% at origination.

Stress testing by the European Banking Authority and Banque de France indicates adequate resilience to adverse scenarios. The 2024 EU-wide stress test modelled a severe recession with GDP contracting 4.2% cumulatively, unemployment rising to 10.5%, and sovereign yields widening by 150 basis points. Under this scenario, French banks' aggregate CET1 ratio declined to 10.9%—a 390 basis point reduction but remaining above regulatory minima. The most vulnerable institution reached 9.2%, still providing a modest buffer. These results suggest the sector could withstand a significant deterioration in economic conditions, though the stress scenarios did not fully capture the compounding effects of sustained political dysfunction and multi-notch sovereign downgrades.

The regulatory and supervisory framework provides institutional strength. The Autorité de Contrôle Prudentiel et de Résolution maintains rigorous oversight under the Single Supervisory Mechanism, with the European Central Bank directly supervising the four global systemically important institutions. France's implementation of Basel III requirements has been comprehensive, and the authorities have demonstrated willingness to impose additional capital requirements through Pillar 2 measures when institution-specific risks emerge. The deposit guarantee scheme provides €100,000 coverage per depositor per institution, though the scheme's €6.5 billion fund would require mutualisation or government support in a systemic crisis.

Looking forward, the banking sector's trajectory depends critically on sovereign developments. Absent further sovereign deterioration, French banks appear well-positioned to navigate the current environment through a combination of strong capital positions, diversified business models, and prudent risk management. However, a scenario in which France loses its remaining Aa3 rating from Moody's—potentially triggered by pension reform reversal or failure to implement the €120 billion consolidation plan—would likely precipitate a cascade of bank downgrades, increase funding costs by an estimated 30-50 basis points, and potentially trigger deposit migration towards German or Dutch institutions. The sector therefore represents both a source of stability in the current crisis and a transmission channel through which sovereign stress could amplify into broader financial instability.

Outlook and Scenarios

Short-Term Outlook (12 months)

France enters 2026 confronting acute fiscal and political pressures that will determine whether the current crisis represents a temporary disruption or a structural deterioration in creditworthiness. The immediate twelve-month horizon centres on three critical junctures: the government's ability to implement meaningful deficit reduction despite parliamentary fragmentation, the sustainability of the pension reform compromise that preserved Prime Minister Sébastien Lecornu's administration, and market tolerance for continued fiscal slippage as debt approaches 117-118% of GDP by year-end 2026.

Economic growth will remain subdued, with consensus projections clustering around 0.9-1.3% as fiscal consolidation efforts extract approximately 1% of GDP from domestic demand. Business investment faces particular headwinds from political uncertainty, with corporate surveys indicating postponement of major capital allocation decisions pending clarity on tax policy and structural reform trajectories. Consumer spending will benefit modestly from real wage growth as inflation undershoots the ECB's 2% target, though household confidence remains depressed by labour market concerns and the spectre of further austerity measures. The external sector provides limited support, with German industrial weakness constraining France's largest export market whilst global trade fragmentation impacts aerospace and luxury goods sectors.

The fiscal trajectory represents the paramount near-term risk. The government targets deficit reduction from 5.8% to approximately 5.0-5.2% of GDP in 2026, requiring expenditure restraint of €40-50 billion against a political backdrop that has already forced suspension of pension reform until 2028. Parliamentary arithmetic remains treacherous, with the National Rally holding effective veto power over budgetary measures whilst left-wing coalition partners demand increased social spending. The probability of achieving even this modest consolidation appears below 50%, with rating agencies explicitly warning that continued slippage toward 5.5% deficits would trigger further downgrades. France's borrowing costs have already widened to 80 basis points above German Bunds—territory historically associated with peripheral eurozone members—indicating market scepticism regarding fiscal credibility.

Political stability remains fragile despite Prime Minister Lecornu's survival of two no-confidence votes in October 2025. The pension reform suspension represents a tactical retreat that preserves near-term governability at the cost of medium-term fiscal sustainability, removing approximately €12-15 billion in annual savings from 2028 onwards. The arrangement satisfies neither reform advocates, who view it as capitulation to populist pressure, nor opponents, who demand permanent reversal. This unstable equilibrium could fracture under fiscal stress, particularly if unemployment rises above 8% or if additional austerity measures prove necessary to meet EU deficit targets. The twelve-month outlook assigns 30-40% probability to another government collapse, which would further delay consolidation efforts and likely trigger immediate rating action from Moody's, currently on negative outlook.

Medium-Term Outlook (1-3 years)

The medium-term trajectory hinges on France's capacity to execute a credible €120 billion fiscal consolidation programme through 2029 whilst navigating the 2027 presidential election and potential shifts in the European fiscal framework. The central scenario assumes muddled adjustment—partial deficit reduction to 4.0-4.5% of GDP by 2028, debt stabilisation around 120-122% rather than the government's 118% target, and continued political fragmentation that prevents comprehensive structural reform. This path maintains France's single-A rating tier but forecloses return to double-A status absent significant policy recalibration.

Fiscal consolidation of 2.8 percentage points by 2029, as required under the EU's Excessive Deficit Procedure, demands sustained annual adjustment of 0.7-0.9% of GDP—a politically arduous task that has eluded France since 2017. The composition of adjustment matters critically for both growth and political feasibility. Expenditure-based consolidation, favoured by rating agencies and centrist technocrats, faces resistance from both left-wing parties defending social programmes and right-wing populists protecting agricultural subsidies and regional transfers. Revenue-based measures encounter opposition from business lobbies and middle-class voters already bearing Europe's highest tax burden at 48% of GDP. The most probable outcome involves hybrid adjustment weighted toward expenditure restraint on operating costs and capital spending, with selective tax increases on corporations and high earners—a path that achieves deficit reduction but fails to address structural spending rigidities in pensions, healthcare, and public employment.

The pension reform question will resurface with particular intensity. Suspension until 2028 provides temporary political relief but creates a fiscal cliff as the measure's €12-15 billion annual savings remain unrealised whilst demographic pressures intensify. The 2027 presidential election will likely centre on this issue, with candidates positioned along a spectrum from permanent reversal (left-wing coalition and National Rally) to acceleration of retirement age increases (centre-right). Market confidence will erode significantly if the next government commits to permanent reversal, as this would signal broader retreat from structural reform and necessitate compensatory fiscal measures exceeding €60 billion through 2035. Rating agencies have explicitly identified pension reform rollback as a downgrade trigger, with Moody's warning that such action would likely prompt immediate move to A1 (equivalent to S&P and Fitch's A+).

Debt dynamics present a narrowing window for stabilisation. Under current policies, debt-to-GDP will reach 120-121% by 2027-2028, approaching the 125% threshold that rating agencies identify as consistent with further downgrades. Stabilisation requires primary surpluses of approximately 1.5-2.0% of GDP—a target France has not sustained since the early 2000s. The interest burden provides modest relief as the ECB's rate-cutting cycle reduces marginal borrowing costs, though the stock effect of higher rates on maturing debt will persist through 2026-2027. France benefits from average debt maturity of 8.2 years and deep domestic institutional investor base, but these advantages diminish if political dysfunction continues. The critical inflection point arrives in 2027-2028: successful deficit reduction to 3.5-4.0% of GDP stabilises debt and preserves A+ ratings, whilst continued slippage above 5% pushes debt toward 125% and triggers cascading downgrades.

Growth potential remains constrained by structural factors independent of the immediate political crisis. Productivity growth has averaged just 0.4% annually since 2015, reflecting rigid labour markets, elevated taxation on capital, and insufficient digital transformation outside leading sectors. Demographics turn increasingly adverse as the baby boom generation fully enters retirement, reducing the working-age population by 0.2-0.3% annually whilst increasing dependency ratios. France's industrial base retains significant strengths in aerospace, pharmaceuticals, luxury goods, and nuclear energy, but faces intensifying competition from Asian manufacturers and American technology platforms. The medium-term growth potential likely settles around 1.0-1.2% absent comprehensive structural reform—sufficient to prevent recession but inadequate to materially reduce debt ratios through growth alone.

Rating Scenarios

Downgrade Scenario (Probability: 35-40%)

Further deterioration to A/A2 across all three agencies occurs if political fragmentation durably impairs fiscal consolidation capacity. Specific triggers include: deficit remaining above 5.5% through 2026-2027 despite government commitments; debt-to-GDP exceeding 123% by 2028; permanent reversal of pension reform removing €60+ billion in medium-term savings; or fourth government collapse within 24 months signalling institutional breakdown. This scenario assumes continued parliamentary gridlock prevents meaningful expenditure reform, forcing reliance on temporary revenue measures and accounting adjustments that fail to address structural imbalances. Market access remains secure given France's reserve currency status and ECB backstop, but borrowing costs rise to 100-120 basis points above German Bunds, adding €8-12 billion to annual interest expense and creating adverse debt dynamics. Economic growth weakens to 0.3-0.5% as fiscal uncertainty depresses investment and elevated taxation constrains consumption. The downgrade scenario does not envision acute crisis—France retains too many fundamental strengths—but rather Japanese-style stagnation with elevated debt, weak growth, and diminished policy flexibility.

Baseline Scenario (Probability: 45-50%)

France stabilises at A+/A1 tier through partial fiscal adjustment and political normalisation following the 2027 presidential election. This central case assumes deficit reduction to 4.5-5.0% in 2026, 4.0-4.5% in 2027, and 3.5-4.0% by 2029—falling short of the 3% Maastricht criterion but demonstrating credible consolidation trajectory. Debt peaks at 121-122% of GDP in 2027-2028 before stabilising, remaining elevated but avoiding the 125% threshold that agencies identify as critical. Political dynamics improve modestly as the 2027 election produces a clearer governing mandate, though parliamentary fragmentation persists at reduced intensity. Pension reform survives in modified form—retirement age reaches 64 by 2030 rather than 2028, with enhanced hardship provisions—preserving majority of fiscal savings whilst accommodating political constraints. Economic growth recovers to 1.0-1.3% as uncertainty diminishes and ECB rate cuts support domestic demand. This scenario maintains France's position as a core eurozone member with investment-grade ratings, though at the lower end of that spectrum and without prospect of near-term upgrade.

Upgrade Scenario (Probability: 15-20%)

Return to AA-/Aa3 tier requires comprehensive policy reset that appears unlikely within the three-year horizon but remains technically feasible. This optimistic case assumes the 2027 presidential election produces a reformist government with working parliamentary majority, enabling acceleration of structural reforms beyond current commitments. Specific elements include: deficit reduction to 3.0-3.5% by 2028 through expenditure-based consolidation targeting public sector efficiency, healthcare cost containment, and subsidy rationalisation; pension reform implementation on original 2028 timeline with retirement age reaching 64; labour market liberalisation reducing structural unemployment below 7%; and tax reform shifting burden from productive capital toward consumption and environmental externalities. Debt-to-GDP stabilises at 118-119% by 2028 with clear declining trajectory toward 115% by 2030. Economic growth accelerates to 1.5-1.8% as reforms boost productivity and business confidence. This scenario requires political conditions—decisive electoral mandate, cohesive governing coalition, public acceptance of reform necessity—that appear remote given current fragmentation, but historical precedent exists in France's 1980s and 1990s consolidation episodes. Rating agencies would likely require 18-24 months of sustained policy implementation before upgrading, placing any return to double-A status in 2028-2029 at earliest.

7. Conclusion

France's sovereign credit profile stands at a critical juncture, balancing formidable institutional strengths against unprecedented political dysfunction and fiscal deterioration. The convergence of three rating downgrades or negative actions within six weeks during autumn 2025 marks the most severe credit event in the Fifth Republic's history, stripping France of its double-A status with two agencies whilst placing the final Aa3 rating under explicit negative watch. The country now trades at single-A equivalent levels across all major rating agencies, with 10-year bond spreads widening to 80 basis points above German Bunds—a spread historically associated with peripheral eurozone economies rather than core founding members.

The fiscal arithmetic presents a daunting challenge. With the deficit reaching 5.8% of GDP in 2024—the highest in the European Union—France must deliver consolidation of 2.8 percentage points by 2029 to comply with the EU's Excessive Deficit Procedure whilst simultaneously stabilising a debt trajectory projected to reach 121% of GDP by 2027-2028. The €120 billion consolidation plan outlined in successive budget proposals represents the most ambitious fiscal adjustment attempted in modern French history, yet implementation remains at severe risk. The collapse of three governments within twelve months, culminating in Prime Minister Lecornu's survival only through suspending the landmark 2023 pension reform, demonstrates that France's fragmented National Assembly lacks the political cohesion necessary to deliver sustained fiscal discipline. The absence of a credible majority coalition capable of legislating difficult measures creates a structural impediment to deficit reduction that rating agencies have explicitly identified as the primary downgrade trigger.

Political fragmentation has evolved from a temporary crisis into a systemic constraint on governance. The June 2024 legislative elections produced a tripartite deadlock amongst the left-wing Nouveau Front Populaire, President Macron's centrist coalition, and Marine Le Pen's Rassemblement National, with no bloc commanding even 200 of the Assembly's 577 seats. This configuration grants opposition forces—particularly the RN—effective veto power over fiscal legislation whilst denying the government capacity to implement coherent policy. The suspension of pension reform until 2028, extracted as the price for parliamentary survival, exemplifies how political weakness forces policy reversals that directly undermine fiscal sustainability. Rating agencies have warned explicitly that further rollback of structural reforms, particularly permanent abandonment of the retirement age increase to 64, would trigger additional downgrades by eliminating France's primary mechanism for containing long-term age-related expenditure.

Despite these formidable headwinds, France retains significant economic resilience that distinguishes it from previous eurozone crisis cases. The economy supports a diversified industrial base spanning aerospace, pharmaceuticals, luxury goods, and digital services, with globally competitive champions including Airbus, LVMH, Sanofi, and TotalEnergies. The banking sector emerged from the pandemic with strengthened capital positions, maintaining CET1 ratios above 13% whilst demonstrating limited direct exposure to sovereign debt relative to southern European peers. France's labour market achieved historic strength in 2025, with the employment rate reaching 69.3%—the highest on record—whilst unemployment declined to 7.4% despite anaemic growth. This labour market resilience provides both fiscal support through sustained tax revenues and social stability that has prevented the mass protests which characterised earlier reform attempts.

The external position has stabilised following years of deterioration, with the current account returning to approximate balance in 2024 after persistent deficits through 2022-2023. France's net international investment position of minus 28% of GDP, whilst negative, remains manageable compared to peripheral economies, and the country benefits from eurozone membership which eliminates currency risk and ensures ECB liquidity backstops. Inflation has moderated sharply to below-target levels of 0.9-1.2% in 2025, providing monetary policy space as the ECB continues its easing cycle. These factors collectively ensure that France faces a fiscal and political crisis rather than an economic or balance-of-payments crisis, maintaining market access even as spreads widen.

The central credit question is whether France's institutional framework can overcome political paralysis before market confidence erodes irreversibly. The country possesses the economic capacity to stabilise its fiscal trajectory—the required consolidation of approximately 0.6% of GDP annually through 2029 is substantial but achievable for an economy of France's sophistication. The impediment is political rather than economic. France's constitutional architecture, designed to produce strong executive authority, has proven inadequate to the challenge of governing without a parliamentary majority. The government's reliance on Article 49.3 to bypass legislative votes, whilst constitutionally valid, has become a symbol of democratic deficit that fuels opposition intransigence whilst failing to deliver durable policy outcomes.

The twelve to twenty-four month window identified by Moody's negative outlook represents France's opportunity to demonstrate governance capacity before losing its final double-A rating. Stabilisation requires three elements: first, a credible fiscal consolidation path that delivers at least 1% of GDP adjustment in 2026 through a combination of expenditure restraint and revenue measures; second, preservation of structural reforms, particularly the pension age increase, to anchor long-term sustainability; and third, emergence of a functional governing coalition capable of legislating beyond emergency measures. The formation of a broader centrist alliance incorporating moderate elements from Les Républicains and the Socialist Party, whilst politically difficult, represents the most viable path to breaking the current deadlock.

Absent such stabilisation, France faces a deteriorating credit trajectory. Further downgrades would push the sovereign firmly into single-A territory, potentially triggering mechanical selling by institutional investors with minimum rating requirements whilst raising funding costs across the economy. The debt dynamics remain adverse, with interest expenditure projected to reach 3% of GDP by 2027 even before accounting for higher risk premia, creating a fiscal trap where consolidation efforts are offset by rising debt service. The risk of a self-reinforcing confidence crisis—whilst not the base case—cannot be dismissed if political dysfunction persists through 2026.

France's credit assessment ultimately reflects a high-income economy with strong fundamentals confronting a crisis of political functionality. The country retains the economic resources and institutional capacity to stabilise its position, but the window for demonstrating political will is narrowing. The unprecedented nature of the current crisis—combining the highest deficit in the EU with the most fragmented parliament in modern French history—demands an equally unprecedented political response. Whether France's political class can forge the compromises necessary to preserve the country's creditworthiness will determine not only the sovereign's rating trajectory but also France's capacity to maintain its position as a core pillar of European integration and stability.