Colombia

Executive Summary

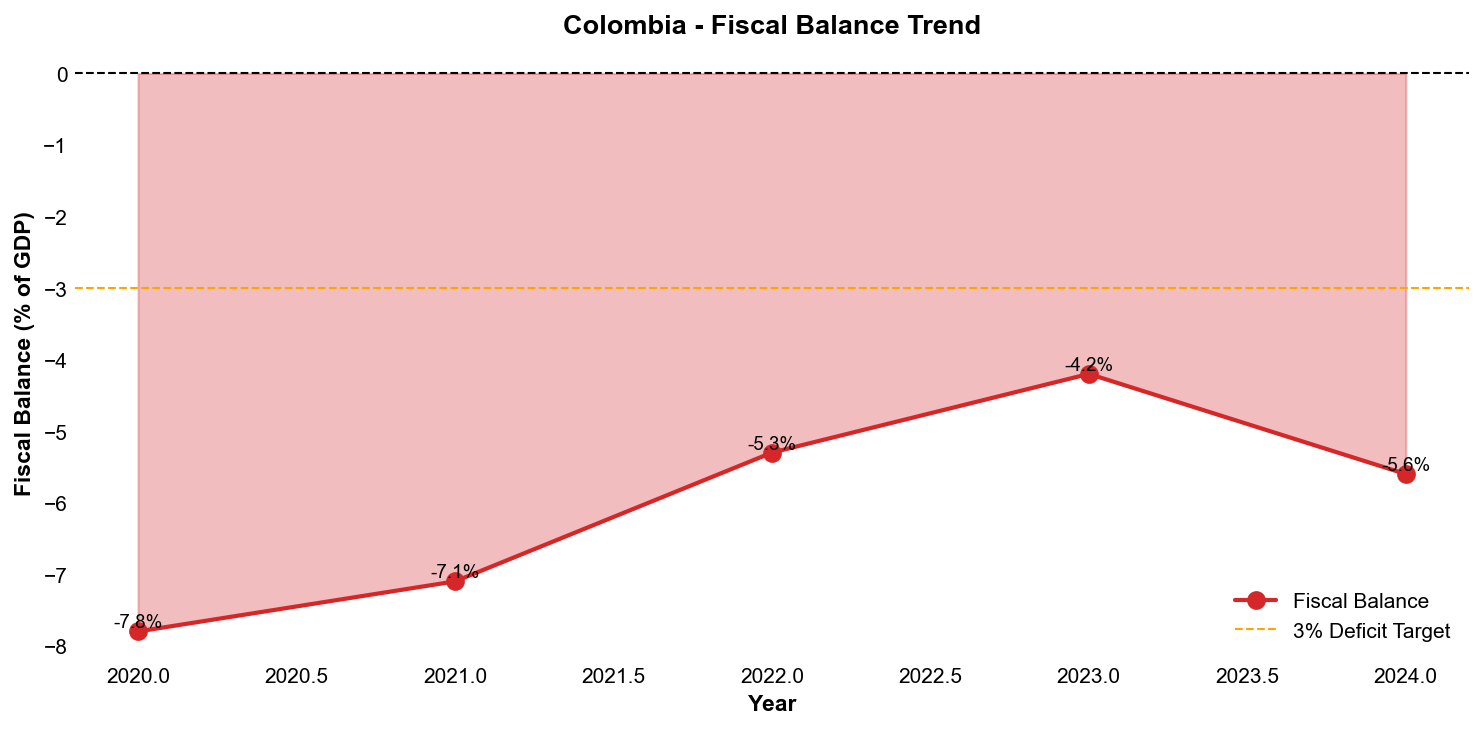

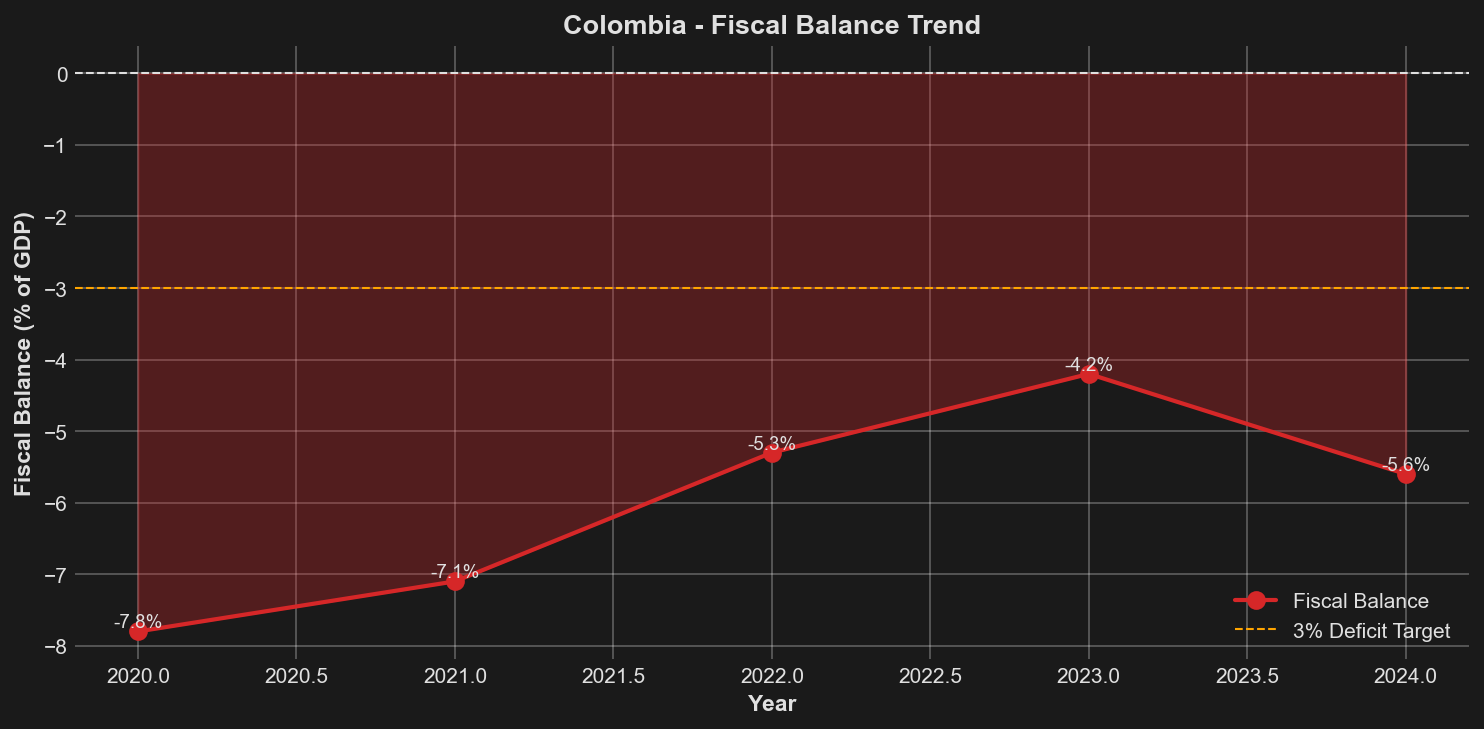

Colombia's credit profile remains under pressure, straddling the investment grade threshold with a Baa2 rating from Moody's whilst S&P and Fitch position the sovereign one notch below at BB+. The bifurcated assessment reflects the country's complex risk landscape, where robust institutional frameworks and demonstrated macroeconomic management capacity are increasingly tested by persistent fiscal deterioration and political constraints on reform implementation. Two of the three major rating agencies maintain negative outlooks, signalling heightened concern over the trajectory of public finances and the government's capacity to execute meaningful consolidation. The fiscal deficit widened to 5.6% of GDP in 2024, reversing earlier consolidation progress, whilst public debt climbed to 61.3% of GDP, with interest payments now absorbing 11% of government revenue and constraining fiscal flexibility.

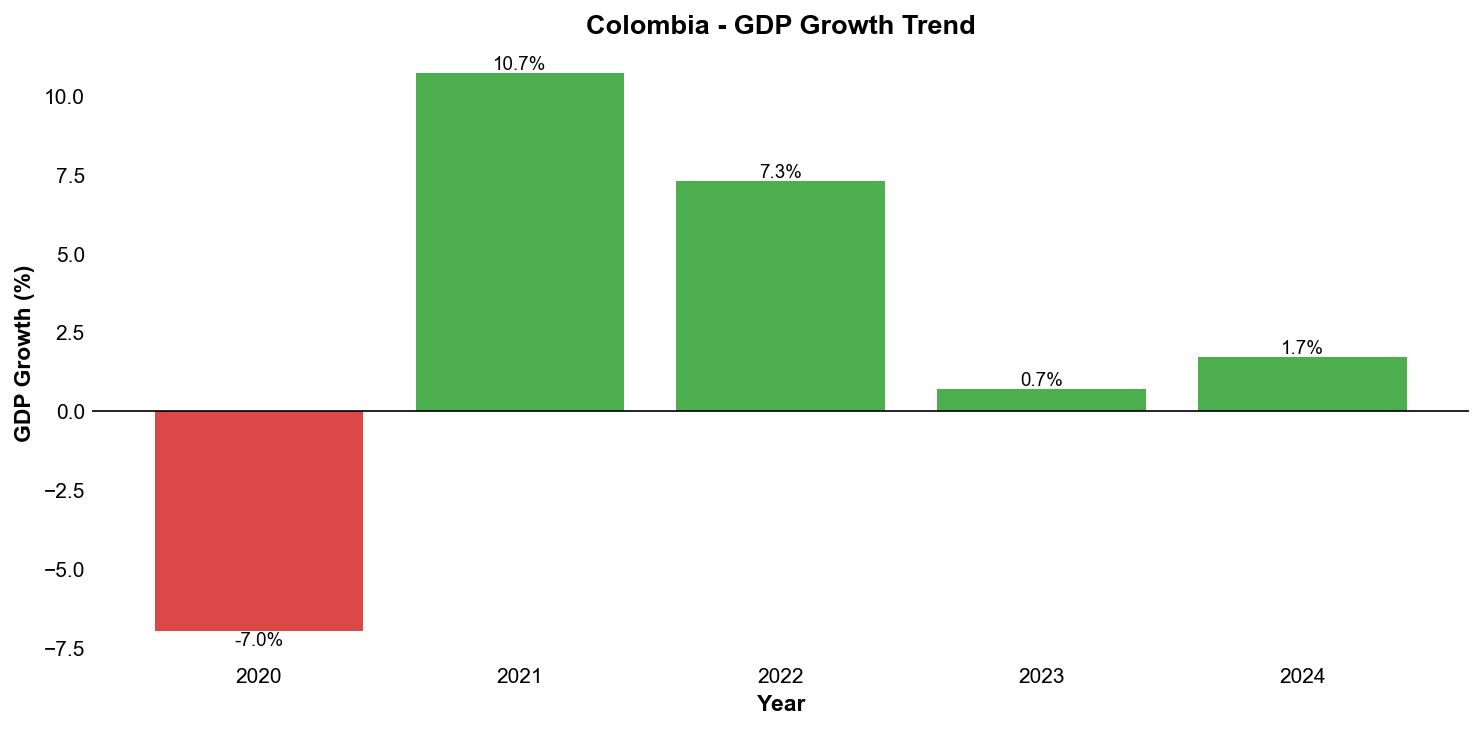

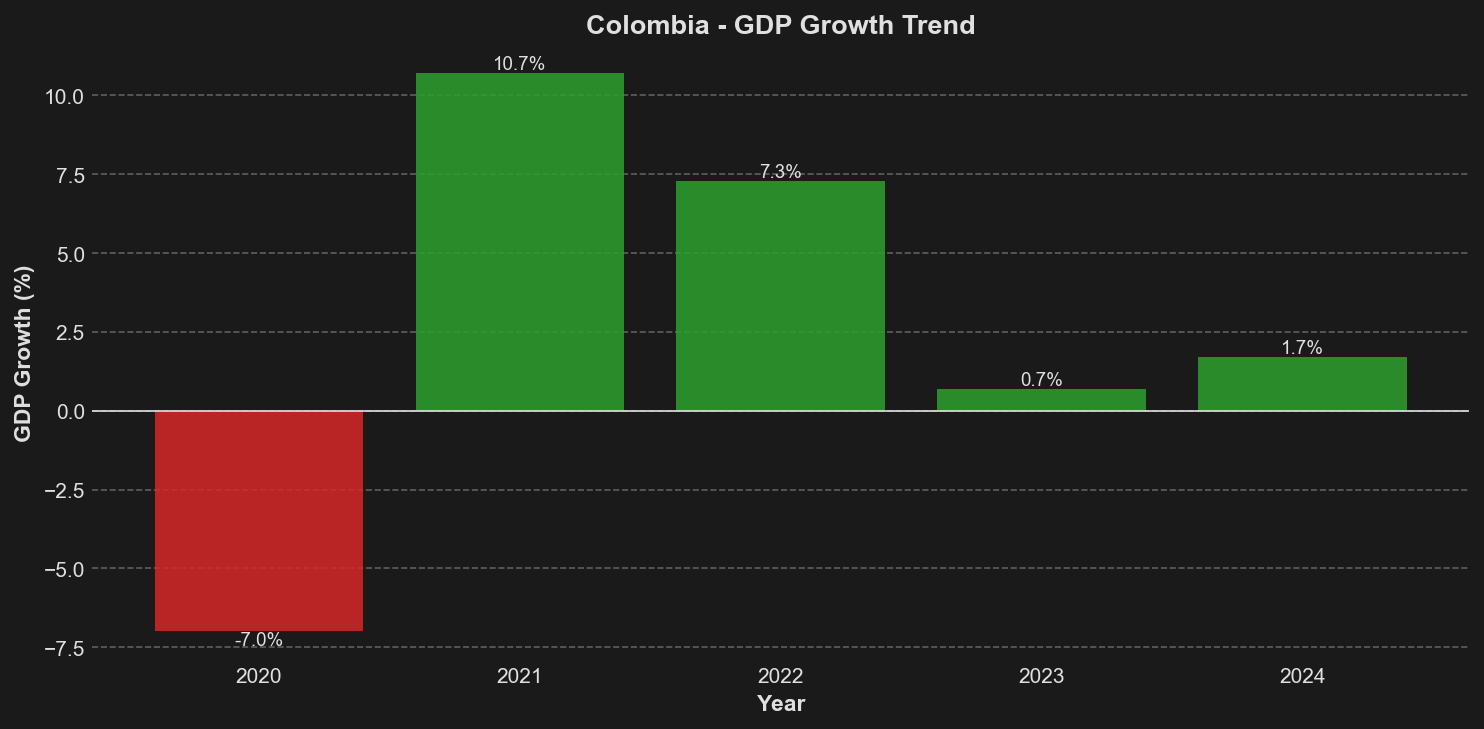

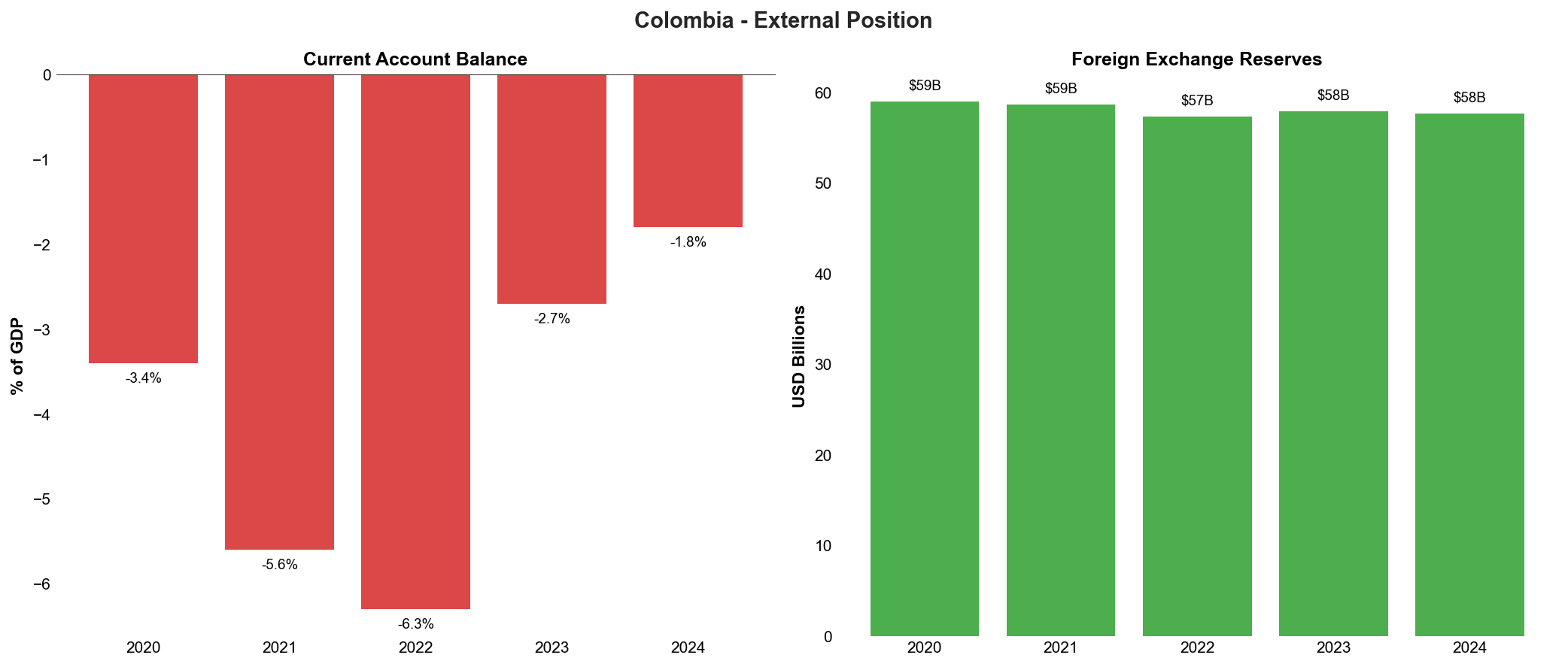

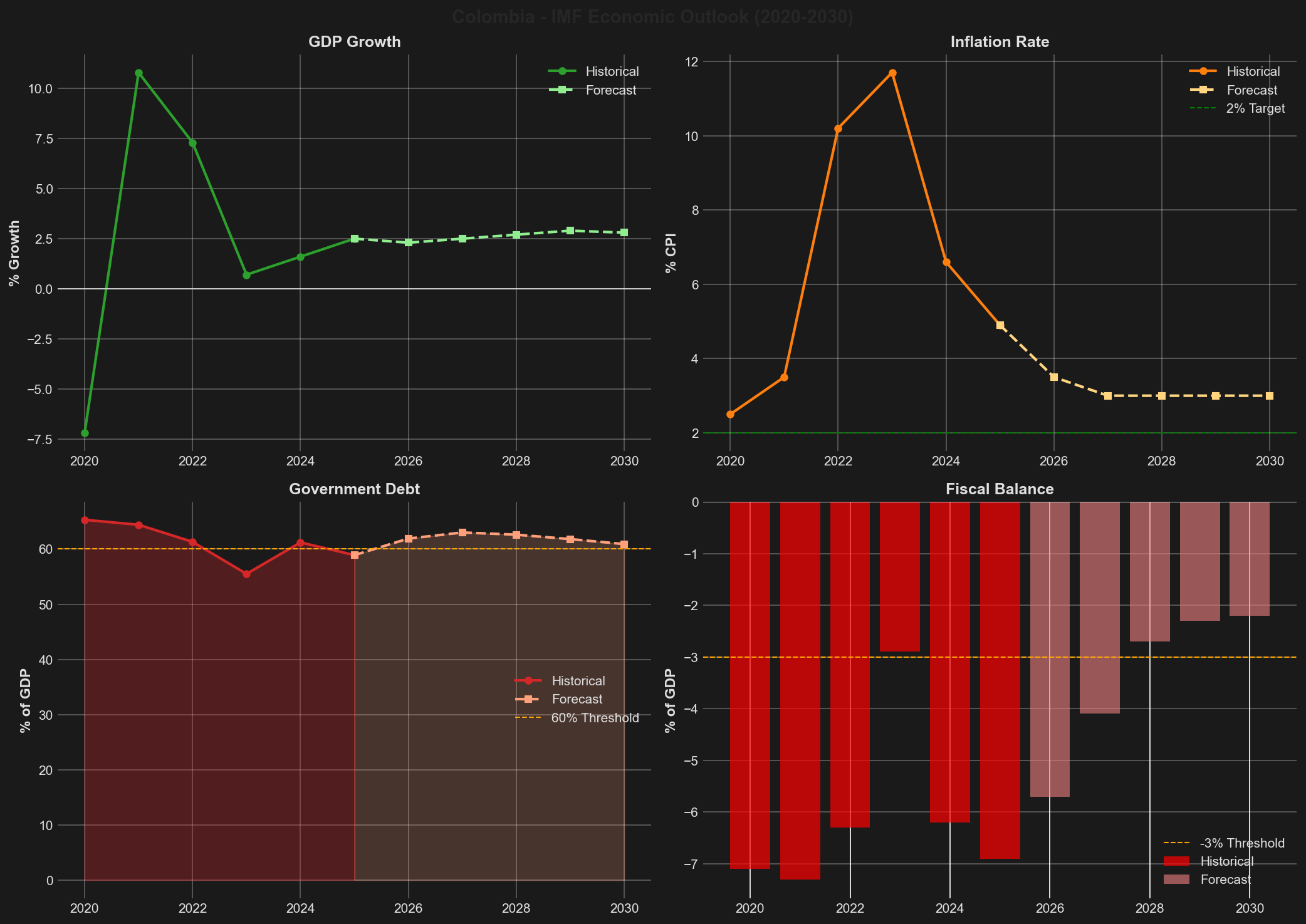

The economic backdrop has shifted from the volatile post-pandemic recovery to a more subdued growth environment, with GDP expansion moderating sharply to 0.7% in 2023 and 1.7% in 2024 following the exceptional rebound of 2021-2022. This deceleration reflects the lagged effects of aggressive monetary tightening undertaken to combat inflation, which peaked at 13.1% in 2022 before declining to 5.1% in 2024 through credible central bank action. The external position has improved materially, with the current account deficit narrowing to 1.8% of GDP in 2024 from 6.3% in 2022, supported by import compression and more favourable terms of trade. However, unemployment remains elevated at 9.1%, whilst foreign exchange reserves have remained broadly stable at approximately USD 58 billion, providing a modest buffer against external shocks.

Colombia confronts a challenging policy environment characterised by political gridlock under President Gustavo Petro, which has simultaneously stalled ambitious reform initiatives and preserved institutional checks and balances. The failure to advance major tax and pension reforms has contributed to revenue underperformance, even as social spending commitments have expanded. The country faces a delicate transition away from fossil fuel dependence, with hydrocarbons still accounting for approximately half of export revenues, creating vulnerability to both commodity price volatility and the global energy transition. Rising non-performing loans in the banking sector, though manageable given adequate capitalisation levels, signal stress in the real economy following the monetary tightening cycle.

The forward outlook anticipates moderate growth of 2.4-2.5% in 2025, contingent upon successful implementation of fiscal consolidation measures and restoration of private sector confidence. The primary risk to the credit profile centres on the government's ability to credibly demonstrate fiscal discipline whilst managing social pressures and political constraints. External vulnerabilities persist, including exposure to tighter global financial conditions, regional instability emanating from Venezuela, and the structural challenge of economic diversification. Conversely, Colombia's institutional resilience, flexible exchange rate regime, and track record of honouring debt obligations provide important mitigating factors. The credit trajectory will largely depend on whether fiscal consolidation can be achieved without undermining already-subdued growth prospects, a balance that will prove challenging given limited policy space and political fragmentation.

Ratings Summary

Colombia's sovereign credit ratings reflect a bifurcated assessment amongst the major rating agencies, with the country maintaining investment grade status solely with Moody's at Baa2, whilst S&P and Fitch position it one notch below at BB+. The negative outlooks assigned by both S&P and Moody's underscore mounting concerns regarding the country's fiscal trajectory, characterised by persistent deficits and rising debt service burdens that have tested the government's commitment to fiscal consolidation. Fitch's stable outlook represents a more sanguine view of Colombia's capacity to adhere to its fiscal rules despite implementation challenges. All three agencies acknowledge Colombia's institutional strengths as fundamental credit supports, particularly the independence and credibility of its central bank, which has demonstrated considerable effectiveness in bringing inflation down from 13.1% in 2022 to 5.1% in 2024. The primary concerns weighing on the ratings centre on weak investor confidence that has constrained private investment, revenue collection shortfalls that have undermined fiscal targets, and the structural challenge of economic diversification away from hydrocarbon dependence. Any path towards rating upgrades would necessitate substantial and sustained fiscal consolidation, meaningful progress in economic diversification, and a return to stronger-than-expected growth that would improve debt dynamics and restore investor confidence in the country's medium-term economic trajectory.

| Rating Agency | Current Rating | Outlook | Last Action Date |

|---|---|---|---|

| S&P | BB+ | Negative | January 2024 |

| Moody's | Baa2 | Negative | June 2024 |

| Fitch | BB+ | Stable | November 2024 |

Economic Indicators

| Indicator | 2021 | 2022 | 2023 | 2024 | 2025F | 2026F |

|---|---|---|---|---|---|---|

| GDP Growth (%) | 10.8% | 7.3% | 0.7% | 1.6% | 2.5% | 2.3% |

| Inflation (%) | 3.5% | 10.2% | 11.7% | 6.6% | 4.9% | 3.5% |

| Unemployment (%) | 13.8% | 11.2% | 10.2% | 10.1% | 10.0% | 9.8% |

| Government Debt (% GDP) | 64.4% | 61.3% | 55.5% | 61.2% | 58.9% | 61.9% |

| Fiscal Balance (% GDP) | -7.3% | -6.3% | -2.9% | -6.2% | -6.9% | -5.7% |

| Current Account (% GDP) | -5.6% | -6.0% | -2.3% | -1.7% | -2.3% | -2.6% |

Colombia's economic performance has exhibited considerable volatility since 2020, transitioning from pandemic-induced contraction through a robust but inflationary recovery phase towards more subdued growth momentum. The economy contracted sharply by 7.0% in 2020 before staging a vigorous rebound with growth of 10.7% in 2021 and 7.3% in 2022. However, this recovery proved unsustainable, with growth decelerating markedly to 0.7% in 2023 and 1.7% in 2024 as the effects of monetary tightening and weakened investor confidence constrained domestic demand. IMF projections suggest a gradual acceleration towards 2.8% by 2030, though this remains contingent upon successful implementation of structural reforms and fiscal consolidation measures.

The inflation trajectory underscores the effectiveness of Colombia's independent central bank in managing price stability through a challenging external environment. After remaining subdued at 1.6% in 2020, inflation accelerated sharply to 13.1% by end-2022, driven by global commodity price shocks, supply chain disruptions, and peso depreciation. The central bank's aggressive monetary tightening campaign successfully brought inflation down to 9.3% in 2023 and 5.1% in 2024, approaching the upper bound of the target range. The IMF forecasts inflation stabilising at 3.0% by 2030, consistent with the central bank's medium-term objective, though this assumes continued policy discipline and anchored inflation expectations.

The fiscal position represents a significant credit concern, having deteriorated markedly in 2024 despite earlier consolidation efforts. The fiscal deficit widened to 5.6% of GDP in 2024 from 4.2% in 2023, reflecting revenue underperformance and resistance to expenditure restraint amid political pressures for expanded social spending. Consequently, the debt-to-GDP ratio has risen to 61.3% in 2024, reversing the declining trend observed between 2021 and 2023. Whilst the IMF projects gradual fiscal consolidation towards a deficit of 2.2% of GDP by 2030 with debt stabilising around 60.9% of GDP, achieving this trajectory requires sustained political commitment to fiscal rules and revenue-enhancing measures that have thus far proven elusive. Interest payments now consume approximately 11% of government revenue, constraining fiscal flexibility and heightening refinancing risks.

Colombia's external position has shown notable improvement, with the current account deficit narrowing from 6.3% of GDP in 2022 to 1.8% in 2024, supported by import compression as domestic demand weakened and improved terms of trade for key commodity exports. However, the IMF's projection of the current account deficit widening substantially to 19.9% of GDP by 2030 appears anomalous and likely reflects data classification issues rather than a credible forecast of external imbalances. Foreign exchange reserves have remained relatively stable around USD 57-59 billion throughout the period, providing a modest buffer against external shocks, though coverage metrics have weakened as import levels recovered from pandemic lows.

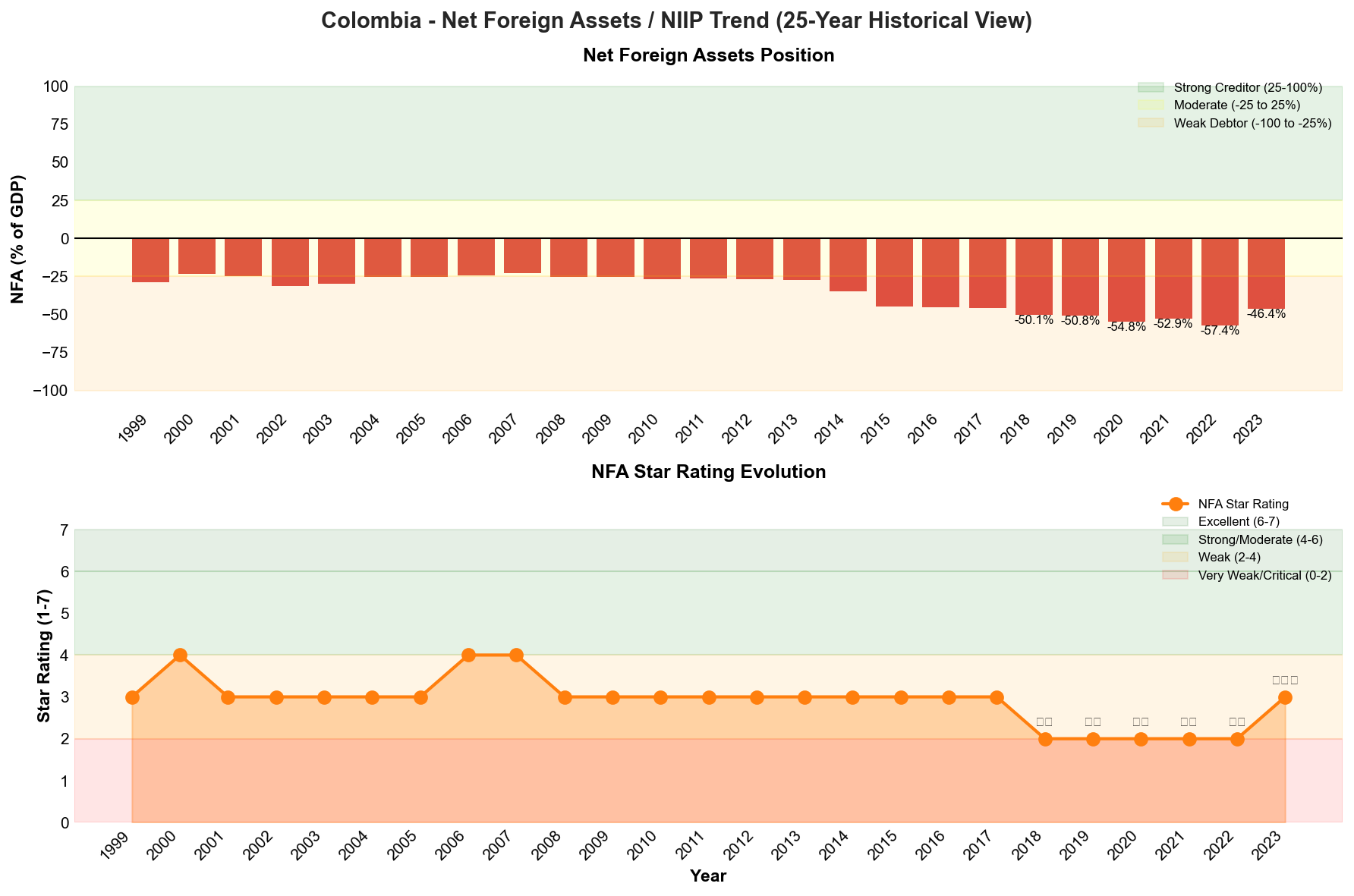

The external liability position, as measured by net foreign assets, stood at -46.4% of GDP in 2023, representing a notable improvement from -57.4% in 2022 and earning a three-star rating indicating a "weak" debtor position. This improvement reflects both nominal GDP growth in dollar terms and moderation in external borrowing. Whilst the net foreign asset position remains substantially negative, the recent trend suggests reduced external vulnerability compared to the "very weak" classification observed between 2019 and 2022. Nevertheless, Colombia's persistent negative net international investment position constrains its external creditworthiness and renders the economy vulnerable to shifts in global risk sentiment and financing conditions.

Labour market conditions have improved steadily, with unemployment declining from a pandemic peak of 16.0% in 2020 to 9.1% in 2024, though the rate remains elevated relative to pre-pandemic levels and regional peers. The IMF projects unemployment stabilising around 9.4% through 2030, suggesting persistent labour market slack that reflects structural challenges including high informality, skills mismatches, and regulatory rigidities. The elevated unemployment rate constrains household income growth and domestic consumption whilst contributing to social pressures for expanded government transfers, complicating fiscal consolidation efforts.

Net Foreign Assets & External Position

Colombia's external position reflects a persistent structural vulnerability characteristic of commodity-dependent emerging markets, though recent improvements have moderated the most acute concerns. The country's net international investment position (NIIP) stood at -46.4% of GDP in 2023, representing a notable improvement from the -57.4% recorded in 2022 but still indicating a substantial net debtor position. This improvement elevated Colombia's external position from a "Very Weak" to "Weak" category, achieving a three-star rating on a seven-point scale, yet the underlying fragility remains a constraint on creditworthiness and a key consideration in the negative outlooks maintained by both S&P and Moody's.

The trajectory of Colombia's NIIP over the past five years illustrates both the vulnerability to external shocks and the economy's capacity for adjustment. From 2019 through 2022, the net foreign asset position deteriorated progressively, reaching its nadir at -57.4% of GDP in 2022 during the period of elevated commodity prices and surging inflation that necessitated aggressive monetary tightening. The pandemic year of 2020 saw a particularly sharp deterioration to -54.8% of GDP as the economic contraction compressed nominal GDP whilst external liabilities remained elevated. The subsequent improvement to -46.4% in 2023 reflects multiple factors: the narrowing of the current account deficit from 6.3% of GDP in 2022 to 2.7% in 2023, the stabilisation of the peso following the central bank's successful inflation management, and improved terms of trade for Colombia's commodity exports during portions of the period.

Current Account Dynamics and Sustainability

The current account balance has demonstrated considerable volatility, moving from a deficit of 6.3% of GDP in 2022 to 2.7% in 2023 and further improving to 1.8% in 2024. This adjustment reflects both cyclical and structural factors. On the cyclical side, the sharp economic deceleration in 2023 (growth of just 0.7%) compressed import demand, particularly for capital goods and consumer durables, whilst export revenues remained relatively resilient due to sustained hydrocarbon prices through much of the period. The structural dimension relates to Colombia's persistent dependence on fossil fuel exports, which continue to account for approximately 50% of total export revenues, creating inherent volatility linked to global commodity cycles.

Looking forward, the IMF projects a concerning deterioration in the current account position, with forecasts indicating a deficit of 19.9% of GDP by 2030. Whilst this projection appears extreme and likely reflects specific modelling assumptions regarding investment flows or commodity price scenarios, it nonetheless highlights the structural vulnerabilities in Colombia's external accounts. The country faces the dual challenge of maintaining export competitiveness as global energy transition accelerates whilst simultaneously attracting sufficient foreign direct investment to finance external deficits without excessive reliance on more volatile portfolio flows.

Foreign Exchange Reserves and External Liquidity

Colombia's foreign exchange reserves have remained relatively stable at approximately USD 57-59 billion throughout the 2020-2024 period, demonstrating the central bank's commitment to maintaining adequate external buffers. The reserves stood at USD 57.6 billion in 2024, representing a modest decline from the USD 59.0 billion held in 2020 but reflecting deliberate policy choices rather than forced depletion. This stability is particularly noteworthy given the significant external pressures faced during this period, including the pandemic shock, the subsequent inflation surge, and periodic episodes of emerging market financial stress.

Reserve adequacy metrics suggest a moderately comfortable position by conventional standards. The reserves provide coverage of approximately 7-8 months of imports and exceed short-term external debt by a reasonable margin, offering a cushion against sudden stops in capital flows. However, the adequacy assessment must be tempered by recognition of Colombia's vulnerability to commodity price shocks and the potential for rapid capital outflows during periods of global risk aversion. The floating exchange rate regime provides an important shock absorber, allowing the peso to adjust to external pressures and thereby reducing the need for reserve depletion, but this flexibility comes at the cost of exchange rate volatility that can complicate debt dynamics for entities with foreign currency exposures.

Composition and Vulnerabilities

The composition of Colombia's external liabilities warrants careful scrutiny. The country benefits from a relatively favourable mix, with foreign direct investment representing a substantial portion of external liabilities. FDI inflows have historically been concentrated in the extractive sectors, particularly oil and mining, providing stable long-term financing that is less prone to sudden reversals than portfolio investment. However, this sectoral concentration creates its own vulnerabilities, as the energy transition threatens to reduce the attractiveness of Colombia's hydrocarbon sector to international investors over the medium term.

Portfolio investment flows have exhibited greater volatility, responding to both domestic political developments and global financial conditions. The period of President Petro's administration has seen episodes of portfolio outflows driven by concerns about policy direction, particularly regarding proposed reforms to the pension system and taxation. These outflows have been manageable thus far, absorbed by exchange rate adjustment and modest reserve utilisation, but they underscore the sensitivity of Colombia's external position to confidence factors.

External debt metrics present a mixed picture. Public sector external debt has risen alongside the overall increase in government indebtedness, with the debt-to-GDP ratio reaching 61.3% in 2024. Whilst a significant portion of this debt is domestically held, the external component creates vulnerability to exchange rate movements and shifts in global financing conditions. Private sector external debt, concentrated in the banking and corporate sectors, appears manageable based on available indicators, though rising non-performing loans in the domestic banking system warrant monitoring for potential spillovers to external debt servicing capacity.

The interaction between the fiscal position and external accounts represents a critical vulnerability. The widening fiscal deficit to 5.6% of GDP in 2024, combined with interest payments consuming 11% of government revenue, creates pressure for external financing that may prove challenging to secure on favourable terms if investor confidence continues to erode. The twin deficits—fiscal and current account—whilst not immediately alarming given the modest size of the current account gap, nonetheless create a configuration that historically has preceded external crises in emerging markets when accompanied by political uncertainty and weak growth prospects.

Regional and Geopolitical Considerations

Colombia's external position cannot be assessed in isolation from its regional context. The ongoing crisis in Venezuela, whilst creating humanitarian and security challenges, has paradoxically provided some economic benefits through migration of skilled labour and redirection of trade flows. However, the potential for Venezuelan instability to spill over through refugee flows, border tensions, or disruption of regional trade routes represents a tail risk to Colombia's external accounts.

The country's relationship with the United States remains economically significant, with the US representing a major export destination and source of investment. Any deterioration in this relationship, whether through trade policy changes or reduced security cooperation, could adversely affect both trade flows and investor confidence. Conversely, Colombia's efforts to diversify trade relationships, particularly with Asian markets, offer potential to reduce concentration risk in export destinations, though progress has been gradual.

The external position assessment for Colombia thus reflects a balance between demonstrated resilience—evidenced by the improvement from -57.4% to -46.4% of GDP in the NIIP—and persistent structural vulnerabilities related to commodity dependence, political uncertainty, and the challenging global environment for emerging market financing. The stable foreign exchange reserves and narrowing current account deficit provide near-term comfort, but the medium-term trajectory depends critically on successful fiscal consolidation, economic diversification, and maintenance of policy credibility. The IMF's projection of significant current account deterioration by 2030, whilst potentially overstated, serves as a reminder of the structural adjustments required to place Colombia's external position on a sustainably stronger footing.

Credit Strengths & Vulnerabilities

Strengths

Colombia's credit profile is anchored by a robust institutional framework that has demonstrated resilience through successive political transitions and economic shocks. The country's independent central bank stands as a cornerstone of macroeconomic stability, having successfully navigated the challenging inflation environment of recent years by bringing inflation down from 13.1% in 2022 to 5.1% in 2024 through credible monetary policy. This institutional strength extends to the floating exchange rate regime, which has provided an important shock absorber during periods of external stress, allowing the economy to adjust to changing global conditions without depleting foreign exchange reserves.

The banking sector remains well-capitalised, providing a stable foundation for financial intermediation despite rising non-performing loans. This financial sector resilience has been crucial in maintaining credit flows to the economy during periods of slower growth. Colombia's policy predictability in key macroeconomic areas has persisted despite political changes, offering investors a degree of confidence in the country's commitment to sound economic management. The economy has demonstrated notable resilience through repeated shocks, including the pandemic contraction, subsequent recovery, and the inflation surge, reflecting underlying structural strengths and adaptive capacity.

Political gridlock under President Gustavo Petro, whilst stalling major reforms, has paradoxically served to preserve institutional checks and balances, preventing potentially destabilising policy shifts. This has maintained a degree of continuity in economic policy that rating agencies view favourably, even as it has limited the government's ability to implement its more ambitious agenda.

Vulnerabilities

The deteriorating fiscal position represents Colombia's most pressing credit vulnerability. The deficit widened to 5.6% of GDP in 2024, driven by revenue underperformance and ambitious social spending commitments, whilst public debt has risen to 61.3% of GDP. This fiscal trajectory is particularly concerning given that interest payments now consume 11% of government revenue, creating sustainability concerns and limiting fiscal space for productive investments or countercyclical policy responses. The persistent fiscal deficits reflect structural challenges in revenue collection and the difficulty of containing expenditure growth in the face of social demands.

Colombia's continued dependence on hydrocarbons for approximately half of export revenues presents significant transition risks as global demand for fossil fuels faces long-term decline. This concentration in fossil fuel exports creates vulnerability to commodity price volatility and exposes the country to the risks associated with the global energy transition. The challenge of managing this transition whilst maintaining fiscal revenues and export earnings represents a fundamental structural vulnerability that will require careful policy navigation over the medium term.

Political gridlock has stalled structural reforms needed to address persistent inequality and enhance productivity. This reform paralysis limits Colombia's ability to raise its growth potential and address underlying social tensions. Weak investor confidence has affected private investment, contributing to below-potential economic growth and limiting job creation. The unemployment rate, whilst declining to 9.1% in 2024, remains elevated and reflects underlying labour market rigidities and insufficient economic dynamism.

Opportunities

Colombia has the potential to leverage its institutional strengths to implement meaningful fiscal consolidation that could restore market confidence and stabilise the debt trajectory. Successful adherence to fiscal rules, despite implementation challenges, could demonstrate the government's commitment to sustainability and potentially lead to rating upgrades from S&P and maintenance of investment grade status with Moody's. The narrowing of the current account deficit to 1.8% of GDP in 2024 suggests improving external balances that could reduce vulnerability to external financing conditions.

Economic diversification away from fossil fuel dependence presents opportunities for developing new export sectors and reducing commodity price vulnerability. Colombia's geographic position, educated workforce, and existing industrial base provide foundations for expanding into higher value-added manufacturing and services. The country's biodiversity and natural resources offer potential for sustainable development initiatives that could attract international investment and financing on favourable terms.

Structural reforms, if political conditions allow their implementation, could unlock significant productivity gains and raise potential growth. Improvements in infrastructure, education, and labour market flexibility would enhance competitiveness and attract foreign direct investment. The resolution of political gridlock through consensus-building could enable progress on tax reform to strengthen revenue collection and address inequality through more progressive fiscal policy.

Threats

The risk of rating downgrade remains substantial if fiscal consolidation efforts fail to materialise or prove insufficient to stabilise the debt trajectory. A downgrade by Moody's would result in Colombia losing investment grade status entirely, potentially triggering capital outflows and increasing borrowing costs. The combination of persistent fiscal deficits and rising interest burdens creates a negative feedback loop that could prove difficult to break without significant policy adjustment.

External risks pose considerable threats to Colombia's credit profile. Tighter global financial conditions would increase borrowing costs and potentially trigger capital outflows from emerging markets, affecting Colombia's access to international capital markets. Commodity price volatility, particularly in oil markets, could undermine fiscal revenues and export earnings, exacerbating fiscal pressures. Regional instability, particularly developments in Venezuela, presents ongoing security and migration challenges that strain public finances and create uncertainty.

Political uncertainty could further dampen investment and economic growth, creating a vicious cycle of weak revenues, higher deficits, and deteriorating debt dynamics. The inability to build political consensus around necessary reforms risks prolonging economic underperformance and eroding institutional credibility over time. Climate-related risks, including extreme weather events and the physical impacts of climate change on agriculture and infrastructure, represent growing threats that could impose significant fiscal costs and disrupt economic activity.

Economic Analysis

Growth Dynamics and Structural Challenges

Colombia's economic trajectory since 2020 illustrates the challenges of achieving sustainable growth amidst structural constraints and external volatility. The pandemic-induced contraction of 7.0% in 2020 gave way to an exceptionally strong rebound, with growth reaching 10.7% in 2021 and 7.3% in 2022. This recovery was driven primarily by pent-up demand, accommodative fiscal and monetary policies, and elevated commodity prices that boosted export revenues. However, the subsequent deceleration to 0.7% growth in 2023 and 1.7% in 2024 reflects the economy's underlying structural limitations and the dampening effects of monetary tightening implemented to combat inflation.

The growth slowdown has been particularly pronounced in domestic demand components. Private consumption, which accounts for approximately two-thirds of GDP, has weakened considerably as real wages declined during the high inflation period and household debt servicing costs increased. Investment activity has been especially subdued, constrained by elevated policy uncertainty, regulatory concerns in key sectors, and the lagged effects of higher interest rates. Gross fixed capital formation has remained below pre-pandemic levels as a share of GDP, reflecting persistent investor caution regarding the business environment and policy direction under the Petro administration.

The external sector has provided some offset to weak domestic demand. The narrowing of the current account deficit from 6.3% of GDP in 2022 to 1.8% in 2024 reflects both cyclical and structural factors. Weaker domestic demand has compressed import volumes, whilst export performance has been mixed. Traditional commodity exports, particularly petroleum and coal, have faced volume declines even as prices remained relatively elevated through much of the period. Non-traditional exports, including manufactured goods and services, have shown resilience but remain insufficient to offset the structural decline in hydrocarbon shipments.

Looking ahead to 2025, economic growth is projected to improve modestly to between 2.4% and 2.5%, supported by gradually recovering domestic demand as inflation normalises and monetary policy easing gains traction. However, this outlook remains contingent upon successful implementation of fiscal consolidation measures without excessive demand compression, continued improvement in consumer confidence, and a stable external environment. The economy's potential growth rate is estimated at approximately 3.0% to 3.5%, suggesting that Colombia will continue operating below capacity in the near term, with implications for employment generation and fiscal revenue collection.

Inflation Dynamics and Price Stability

Colombia experienced a severe inflation shock during 2022 and 2023, with consumer prices accelerating from 5.6% at end-2021 to a peak of 13.1% at end-2022, before moderating to 9.3% in 2023 and 5.1% in 2024. This inflation episode reflected both global and domestic factors. International commodity price surges, particularly for food and energy, transmitted rapidly through to domestic prices given Colombia's openness to trade. Supply chain disruptions persisted longer than initially anticipated, whilst the peso's depreciation during 2021 and 2022 amplified imported inflation pressures.

Domestic factors also contributed significantly to inflationary pressures. Strong aggregate demand during the recovery phase created capacity constraints in certain sectors, particularly services. Labour market tightening, with unemployment falling from 16.0% in 2020 to 9.1% in 2024, generated wage pressures that fed through to core inflation. Food price inflation proved particularly persistent, reflecting both international price movements and domestic supply constraints in agricultural production and distribution networks.

The disinflation process that brought inflation down to 5.1% by end-2024 demonstrates the effectiveness of Colombia's monetary policy framework, though inflation remains above the central bank's 3.0% target. Core inflation measures, which exclude volatile food and energy prices, have declined more gradually than headline inflation, suggesting that second-round effects and inflation expectations required sustained policy restrictiveness to contain. The central bank's credibility, built over decades of operational independence, has been crucial in anchoring expectations and preventing a more persistent inflation problem.

Monetary Policy Framework and Financial Conditions

The Banco de la República, Colombia's central bank, has operated with full independence since 1991 and maintains a flexible inflation targeting regime with a 3.0% target and a tolerance range of plus or minus one percentage point. This institutional framework represents one of Colombia's key credit strengths, providing a credible nominal anchor that has supported macroeconomic stability through multiple political transitions and external shocks.

In response to the inflation surge, the central bank implemented one of the most aggressive tightening cycles in its history, raising the policy rate from 1.75% in September 2021 to a peak of 13.25% by early 2023. This 1,150 basis point increase reflected the monetary authority's determination to prevent inflation expectations from becoming unanchored and to demonstrate its commitment to price stability despite political pressures. The central bank maintained the policy rate at this restrictive level through much of 2023 and into 2024, only beginning a gradual easing cycle once inflation showed sustained deceleration and inflation expectations began converging back towards the target.

The transmission of monetary policy to the real economy has functioned effectively through multiple channels. The interest rate channel has operated through higher borrowing costs for households and firms, dampening credit growth and interest-sensitive spending. Credit to the private sector decelerated markedly during 2023 and 2024, with real credit growth turning negative in several quarters. The exchange rate channel has also been operative, with higher interest rates supporting the peso and helping to contain imported inflation, though the currency has remained subject to considerable volatility reflecting both domestic political developments and external financial conditions.

Financial conditions have tightened considerably beyond the direct effects of policy rate increases. Commercial bank lending rates have risen across all segments, with mortgage rates, consumer lending rates, and corporate borrowing costs all increasing substantially. Credit standards have tightened as banks have become more cautious in their lending practices, reflecting both regulatory expectations and concerns about asset quality deterioration in a slowing economy. Non-performing loan ratios have edged higher, particularly in consumer lending segments, though they remain manageable and well below levels that would indicate systemic stress. The banking sector maintains strong capital buffers, with capital adequacy ratios well above regulatory minimums, providing resilience against potential credit losses.

The monetary easing cycle that commenced in late 2024 reflects the central bank's assessment that inflation risks have diminished sufficiently to warrant a gradual normalisation of policy rates. However, the pace of easing is constrained by several factors. Inflation remains above target, core inflation has proven sticky, and fiscal policy remains expansionary, requiring monetary policy to maintain a degree of restrictiveness. External considerations also influence the easing path, as excessive divergence from policy rates in advanced economies could trigger capital outflows and currency depreciation that would reignite inflation pressures. The central bank has signalled that policy normalisation will be gradual and data-dependent, prioritising the consolidation of inflation gains over providing stimulus to economic activity.

Political & Institutional Assessment

Colombia's political landscape presents a study in contrasts, where robust institutional frameworks coexist with significant policy implementation challenges. The administration of President Gustavo Petro, which began in August 2022, has encountered substantial legislative resistance that has effectively stalled major elements of its reform agenda whilst simultaneously preserving the country's system of institutional checks and balances. This dynamic has created a political environment characterised by gridlock rather than radical policy shifts, an outcome that has paradoxically provided some reassurance to investors concerned about the government's initially ambitious reform programme.

Institutional Strengths

Colombia's institutional architecture represents a fundamental credit strength, anchored by the independence and credibility of its central bank, Banco de la República. The central bank's successful navigation of the recent inflation surge demonstrates the effectiveness of this institutional framework. Having raised policy rates aggressively in response to inflation that peaked at 13.1% in 2022, the bank maintained its commitment to price stability despite political pressures, successfully guiding inflation down to 5.1% by 2024. This performance underscores the resilience of Colombia's monetary policy framework and the central bank's operational autonomy, which remains insulated from executive interference.

The country's floating exchange rate regime has functioned as an effective shock absorber, allowing for external adjustments without depleting foreign exchange reserves, which have remained relatively stable at approximately 57-58 billion US dollars throughout the 2020-2024 period. This flexibility in the exchange rate mechanism has enabled Colombia to weather external pressures whilst maintaining monetary policy independence, a critical advantage in an environment of global financial volatility.

Beyond monetary institutions, Colombia benefits from an independent judiciary, a Constitutional Court that has demonstrated willingness to check executive power, and a relatively free press that provides transparency and accountability. These institutional features distinguish Colombia within the Latin American context and provide important safeguards against governance deterioration.

Political Dynamics and Reform Challenges

The Petro administration's reform agenda, which initially encompassed ambitious changes to taxation, pensions, healthcare, and labour markets, has encountered formidable opposition in Congress, where the government lacks a stable majority. This legislative fragmentation has resulted in the dilution or outright rejection of key reform proposals. Whilst the government successfully passed a tax reform in 2022 aimed at raising revenues equivalent to approximately 1.5% of GDP, subsequent reform efforts have stalled, contributing to the fiscal underperformance evident in the widening deficit to 5.6% of GDP in 2024.

The political gridlock has had mixed credit implications. On one hand, the failure to implement structural reforms addressing pension sustainability, labour market rigidities, and revenue enhancement limits Colombia's capacity to address long-term fiscal challenges and improve potential growth. The stalled reform agenda also reflects broader governance challenges in building political consensus for difficult but necessary policy adjustments. On the other hand, the inability to advance more radical elements of the government's programme has alleviated investor concerns about potential policy discontinuity, particularly regarding the energy sector and private investment frameworks.

Fiscal Governance and Rule Adherence

Colombia's fiscal rule framework, established in 2011 and modified in subsequent years, has provided an important anchor for fiscal policy, though adherence has become increasingly challenging. The rule targets a structural deficit path and includes an escape clause for extraordinary circumstances, which was invoked during the pandemic. However, the return to compliance has proven difficult, with the actual deficit in 2024 exceeding targets due to revenue underperformance and expenditure pressures from expanded social programmes.

The government's commitment to the fiscal rule remains a point of contention amongst rating agencies. Whilst authorities have expressed continued adherence to fiscal consolidation objectives, the practical implementation has lagged, raising questions about the credibility of medium-term fiscal targets. The Constitutional Court's role in reviewing fiscal legislation adds another layer of complexity, as judicial decisions can materially affect fiscal outcomes, as evidenced by rulings on pension and healthcare spending that have constrained the government's fiscal flexibility.

Political Stability and Succession Risks

Colombia's democratic institutions have demonstrated resilience through multiple political transitions, and the country maintains regular electoral cycles with peaceful transfers of power. However, President Petro's approval ratings have declined significantly since taking office, reflecting public frustration with economic performance and unfulfilled reform promises. With presidential elections scheduled for 2026, political uncertainty is likely to intensify, potentially affecting policy continuity and investment decisions.

The fragmented nature of Colombia's political party system means that coalition-building remains essential for governability, yet increasingly difficult to achieve. This fragmentation may persist beyond the current administration, suggesting that policy implementation challenges could extend into future governments regardless of their political orientation. The ability of future administrations to forge working legislative majorities will be critical for addressing Colombia's structural economic challenges, including fiscal sustainability, infrastructure gaps, and economic diversification.

Regional and Security Considerations

Colombia's political stability must also be assessed within its regional context and ongoing security challenges. The 2016 peace agreement with the Revolutionary Armed Forces of Colombia (FARC) represented a historic achievement, though implementation has been uneven and violence from remaining armed groups continues in certain regions. These security challenges, whilst significantly diminished from historical levels, continue to affect rural development, coca cultivation, and governance in peripheral areas.

The country's relationship with Venezuela remains a source of potential instability, affecting border security, migration flows, and trade relations. Colombia has absorbed over two million Venezuelan migrants and refugees since 2015, placing pressure on public services whilst also expanding the labour force. The government's approach to managing this migration challenge, including regularisation programmes, has demonstrated pragmatic policymaking but also highlights the external factors that can complicate domestic policy objectives.

Banking Sector & Financial Stability

Colombia's banking sector has demonstrated considerable resilience through recent economic turbulence, maintaining adequate capitalisation levels and profitability despite mounting asset quality pressures. The sector's stability represents a critical credit strength for the sovereign, providing a buffer against economic volatility whilst supporting credit intermediation during periods of subdued growth.

The Central Bank of Colombia (Banco de la República) has established itself as one of Latin America's most credible monetary authorities, successfully navigating the inflationary surge that peaked at 13.1% in 2022. Through decisive monetary tightening, the bank brought inflation down to 5.1% by end-2024, demonstrating both technical competence and institutional independence. This credibility has been essential in anchoring inflation expectations and maintaining confidence in the Colombian peso, despite periodic episodes of currency volatility. The bank's floating exchange rate regime has served as an effective shock absorber, allowing relative price adjustments without depleting foreign exchange reserves, which have remained stable around USD 57-59 billion throughout the 2020-2024 period.

Colombian banks entered the recent economic slowdown with robust capital buffers, reflecting both prudent regulatory standards and conservative risk management practices developed through previous credit cycles. The sector's capitalisation has provided capacity to absorb rising non-performing loans without threatening systemic stability. However, asset quality has deteriorated as the economic deceleration and elevated interest rates have strained borrower repayment capacity, particularly amongst consumer and small business segments. Non-performing loan ratios have increased from historically low levels, though they remain within manageable bounds relative to provisioning coverage and capital adequacy.

Profitability metrics have held up reasonably well despite the challenging operating environment, supported by wider interest margins during the monetary tightening cycle. Banks have benefited from repricing loan portfolios upwards more rapidly than deposit costs adjusted, though this dynamic has begun to reverse as policy rates stabilise and competitive pressures intensify. The sector's earnings generation capacity remains adequate to absorb credit losses and support organic capital accumulation, reducing reliance on external capital injections.

Liquidity conditions across the banking system remain comfortable, with institutions maintaining substantial buffers of high-quality liquid assets. Funding structures have proven stable, with deposit bases demonstrating resilience even during periods of economic uncertainty. The loan-to-deposit ratio remains at prudent levels, indicating limited reliance on wholesale funding sources that could prove volatile during stress episodes. Access to international capital markets has been maintained by larger institutions, though at higher spreads reflecting both domestic risk perceptions and tighter global financial conditions.

The regulatory and supervisory framework governing Colombia's financial sector represents a significant institutional strength. The Superintendencia Financiera de Colombia has implemented Basel III standards and maintains active oversight of systemic risks. Stress testing frameworks have been enhanced, providing authorities with improved tools to assess vulnerabilities and calibrate macroprudential policies. The financial safety net, including deposit insurance arrangements, provides credible protection for retail depositors whilst limiting moral hazard concerns.

Nevertheless, several vulnerabilities warrant monitoring. The banking sector's exposure to government debt has increased as fiscal deficits have widened, creating a sovereign-bank nexus that could amplify stress in adverse scenarios. Concentration risks persist in certain segments, with exposure to commodity-related sectors creating sensitivity to oil price movements. Foreign currency lending, whilst modest relative to total credit, presents risks for unhedged borrowers should the peso experience sharp depreciation. The continued economic dependence on hydrocarbon revenues creates indirect risks for banks through their corporate and household exposures to oil-dependent regions and industries.

Looking forward, the banking sector's performance will remain closely tied to the broader economic trajectory and the success of fiscal consolidation efforts. Sustained moderate growth in the 2.4-2.5% range would support gradual asset quality improvement and maintain profitability at levels sufficient to preserve capital strength. However, downside scenarios involving fiscal crisis, sharp currency depreciation, or prolonged economic stagnation could test the sector's resilience more severely. The sector's ability to support economic diversification efforts away from fossil fuel dependence will prove crucial for Colombia's longer-term credit profile, requiring both prudent risk management and willingness to finance emerging sectors.

Outlook & Scenarios

Short-Term Outlook (12 months)

Colombia's near-term economic trajectory through 2026 remains constrained by persistent fiscal challenges and subdued private investment, though macroeconomic stabilisation provides a foundation for modest recovery. Economic growth is projected to reach 2.4-2.5% in 2025, representing a gradual acceleration from the 1.7% recorded in 2024, supported primarily by recovering domestic consumption as inflation continues its downward trajectory towards the central bank's 3% target range. The Banco de la República's successful monetary policy normalisation, having brought inflation down from 13.1% in 2022 to 5.1% in 2024, creates scope for further interest rate reductions that should ease financing conditions for households and businesses. However, this growth outlook remains vulnerable to the government's ability to demonstrate credible progress on fiscal consolidation, with the 2024 deficit of 5.6% of GDP requiring substantial correction to restore market confidence and comply with the fiscal rule framework.

The fiscal position represents the most immediate credit challenge over the coming twelve months. Revenue underperformance has consistently undermined consolidation efforts, whilst expenditure pressures from social programmes and rising debt service costs—now consuming approximately 11% of government revenue—limit fiscal flexibility. The government faces the delicate task of implementing revenue-enhancing measures and expenditure restraint without further dampening economic activity or triggering social unrest. Political gridlock under President Petro's administration complicates this challenge, as legislative opposition has repeatedly blocked major reform initiatives. Nevertheless, Colombia's institutional framework, including its constitutional fiscal rule and independent central bank, provides important guardrails that should prevent extreme policy deviations.

The external sector outlook appears relatively stable in the short term, with the current account deficit having narrowed to 1.8% of GDP in 2024 from 6.3% in 2022. Foreign exchange reserves of USD 57.6 billion provide adequate coverage against external shocks, whilst the flexible exchange rate regime continues to serve as an effective shock absorber. However, Colombia remains exposed to commodity price volatility, particularly for oil and coal, which still account for approximately half of export revenues. Any significant deterioration in global commodity markets or tightening of international financial conditions could pressure the peso and complicate debt dynamics, given the government's external financing requirements.

Medium-Term Outlook (1-3 years)

Colombia's medium-term economic prospects hinge critically on the successful execution of fiscal consolidation and progress towards economic diversification, both of which face substantial implementation challenges. Sustained economic growth in the 2.5-3.0% range appears achievable if the government can restore investor confidence through credible fiscal adjustment whilst avoiding excessive contractionary impacts. This growth trajectory, whilst modest by historical standards and below the rates needed to meaningfully reduce unemployment and poverty, would nonetheless represent an improvement over recent performance and align with the economy's constrained potential given structural impediments including weak infrastructure, labour market rigidities, and persistent informality affecting nearly half the workforce.

The fiscal consolidation path over the next three years will determine whether Colombia can stabilise its debt trajectory and preserve market access on reasonable terms. With public debt reaching 61.3% of GDP in 2024 and interest burdens rising, the government must demonstrate commitment to its fiscal rule framework through a combination of revenue enhancement and expenditure prioritisation. This requires not only annual budget discipline but also structural reforms to broaden the tax base, improve collection efficiency, and rationalise spending programmes. The political economy of such reforms remains challenging, particularly given President Petro's focus on social spending and the fragmented nature of Colombia's congress. Failure to achieve meaningful fiscal consolidation would likely trigger rating downgrades and increase financing costs, creating a negative feedback loop that further complicates debt sustainability.

Economic diversification away from hydrocarbon dependence represents both a necessity and an opportunity over the medium term. The global energy transition poses existential risks to Colombia's traditional export model, with fossil fuels accounting for approximately 50% of export revenues. The government's stated commitment to accelerating this transition through investment in renewable energy, sustainable agriculture, and tourism sectors is economically rational but faces significant execution risks. Success requires not only public investment in enabling infrastructure but also regulatory reforms to attract private capital, improvements in security conditions in rural areas, and development of human capital. The mining sector, particularly for minerals critical to the energy transition such as copper and nickel, offers potential diversification opportunities that could partially offset declining hydrocarbon revenues whilst remaining within the extractive sector framework.

The banking sector's resilience will be tested as the economy navigates this transition period. Whilst Colombian banks remain well-capitalised with adequate provisioning levels, non-performing loans have risen as higher interest rates and slower growth have pressured borrowers' repayment capacity. The sector's exposure to both consumer credit and corporate lending to commodity-dependent sectors creates vulnerabilities should economic conditions deteriorate further. However, the banking system's track record of weathering previous crises, combined with effective supervision by financial authorities, suggests manageable risks absent severe external shocks. The gradual normalisation of monetary policy should ease pressure on asset quality whilst the flexible exchange rate regime helps distribute adjustment costs across the economy.

Rating Scenarios

Colombia's credit rating trajectory over the next 12-24 months will be determined primarily by fiscal performance, with secondary factors including economic growth outcomes, political stability, and external financing conditions. The current split rating—with Moody's maintaining investment grade at Baa2 whilst S&P and Fitch rate the sovereign at BB+—reflects genuine analytical uncertainty about the balance between Colombia's institutional strengths and its fiscal vulnerabilities. The negative outlooks from both S&P and Moody's signal elevated downgrade risk absent demonstrable improvement in key credit metrics.

A downgrade scenario, which carries approximately 30-35% probability over the next twelve months, would most likely be triggered by continued fiscal slippage and failure to implement credible consolidation measures. Specifically, if the fiscal deficit remains above 5% of GDP through 2025 without a clear path to compliance with the fiscal rule, or if public debt exceeds 65% of GDP with an upward trajectory, rating agencies would likely conclude that fiscal sustainability risks have intensified beyond levels consistent with current ratings. Additional downgrade catalysts include a significant deterioration in economic growth prospects, potentially triggered by external shocks or further erosion of investor confidence leading to capital outflows and currency pressure. Political developments that undermine institutional independence, particularly of the central bank or fiscal oversight bodies, would also prompt negative rating actions. For Moody's, a downgrade would move Colombia to Ba1, eliminating its investment grade status entirely and potentially triggering forced selling by institutional investors with investment grade mandates.

The baseline scenario, carrying approximately 50-55% probability, envisions rating stability with gradual outlook revisions to stable as the government demonstrates progress on fiscal consolidation without achieving dramatic improvements. This scenario assumes the fiscal deficit narrows to approximately 4.5% of GDP in 2025 and continues declining towards 3.5% by 2027, whilst public debt stabilises around 62-63% of GDP before beginning a gradual descent. Economic growth in the 2.4-2.6% range, combined with continued inflation control and external sector stability, would support this outcome. Critically, this scenario requires the government to implement at least partial revenue-enhancing measures and expenditure restraint whilst avoiding major policy mistakes or institutional deterioration. Political gridlock, whilst frustrating for reform advocates, may paradoxically support rating stability by preventing potentially destabilising policy experiments whilst preserving institutional checks and balances.

An upgrade scenario, carrying only 10-15% probability over the medium term, would require substantial outperformance across multiple dimensions. For S&P and Fitch to upgrade Colombia back to investment grade (BBB-), the sovereign would need to demonstrate sustained fiscal consolidation with the deficit declining below 3% of GDP and debt clearly on a downward trajectory towards 55% of GDP. This would need to be accompanied by stronger economic growth in the 3.0-3.5% range, reflecting successful structural reforms that enhance productivity and attract private investment. Progress on economic diversification, reducing hydrocarbon dependence below 40% of exports, would also support upgrade considerations by reducing external vulnerability. For Moody's to upgrade from Baa2 to Baa1, an even higher bar applies, requiring not only fiscal consolidation but also evidence of enhanced growth potential and reduced political uncertainty. Given Colombia's challenging political environment and the structural nature of its fiscal challenges, such comprehensive improvements appear unlikely within the next two to three years, though not impossible if a reform-oriented consensus emerges following the next electoral cycle.

The balance of risks tilts modestly negative in the near term, reflecting the immediacy of fiscal challenges and the difficulty of implementing consolidation in Colombia's current political context. However, the country's strong institutional framework, demonstrated central bank credibility, and track record of policy pragmatism provide important buffers against severe deterioration. The flexible exchange rate regime and adequate foreign exchange reserves offer protection against external financing shocks, whilst the diversified economic base—despite hydrocarbon dependence—provides resilience against sector-specific downturns. Ultimately, Colombia's credit trajectory will reflect the government's ability to balance competing demands for social spending, fiscal sustainability, and economic growth within the constraints imposed by political fragmentation and global economic uncertainty.

Conclusion

Colombia's sovereign credit profile reflects a delicate equilibrium between institutional resilience and mounting fiscal pressures. The country's split ratings—maintaining investment grade status with Moody's (Baa2) whilst rated sub-investment grade by S&P and Fitch (BB+)—accurately capture this duality. The negative outlooks from two of the three major agencies underscore the precarious nature of this balance and the tangible risk of further deterioration absent decisive policy action.

The fundamental credit strengths that have historically supported Colombia's ratings remain intact. The central bank's independence and credibility, demonstrated through its successful reduction of inflation from 13.1% in 2022 to 5.1% in 2024, continues to anchor macroeconomic stability. The flexible exchange rate regime has facilitated external adjustment, with the current account deficit narrowing to a manageable 1.8% of GDP. The banking sector's resilience, characterised by adequate capitalisation despite rising non-performing loans, provides an additional buffer against financial instability. These institutional foundations represent genuine credit positives that differentiate Colombia from regional peers with weaker policy frameworks.

However, these strengths are increasingly overshadowed by fiscal deterioration that threatens medium-term sustainability. The widening of the fiscal deficit to 5.6% of GDP in 2024, coupled with public debt reaching 61.3% of GDP, marks a concerning reversal of consolidation efforts. The structural nature of these challenges—rooted in revenue underperformance and rigid expenditure commitments—suggests that adjustment will require politically difficult reforms rather than cyclical improvement alone. With interest payments now consuming 11% of government revenue, the fiscal space for countercyclical policy or growth-enhancing investment has narrowed considerably.

The political environment adds complexity to the credit outlook. Whilst gridlock under President Petro has prevented potentially destabilising policy shifts, it has simultaneously blocked reforms necessary to address structural weaknesses in tax collection, labour markets, and productivity. This stalemate preserves institutional checks and balances but defers critical adjustments, allowing imbalances to accumulate. The resulting weakness in investor confidence has manifested in subdued private investment, constraining potential growth and creating a self-reinforcing cycle of fiscal pressure and economic underperformance.

Colombia's continued dependence on hydrocarbons for approximately half of export revenues presents an additional layer of vulnerability. The global energy transition, whilst gradual, creates asymmetric risks for fossil fuel exporters. Colombia's challenge lies in managing this transition whilst maintaining fiscal revenues and export earnings, a task made more difficult by the current administration's reluctance to expand hydrocarbon production even as diversification efforts remain nascent.

Looking ahead to 2025 and beyond, Colombia's credit trajectory hinges on fiscal consolidation credibility. Projected growth of 2.4-2.5% provides a modest tailwind but insufficient momentum to materially improve debt dynamics without revenue enhancement and expenditure discipline. The government's commitment to fiscal rules will be tested as social spending pressures persist and political constraints limit policy options. Success in narrowing the deficit towards the 2.3% target would stabilise the debt trajectory and potentially support ratings, whilst continued slippage would likely trigger downgrades from Moody's, eliminating Colombia's remaining investment grade rating.

The external environment presents both opportunities and risks. Moderating global interest rates may ease financing conditions, whilst commodity price volatility and regional instability, particularly spillovers from Venezuela, pose downside risks. Colombia's flexible exchange rate and adequate foreign exchange reserves (USD 57.6 billion) provide important shock absorbers, but cannot substitute for fundamental fiscal adjustment.

In summary, Colombia stands at a credit crossroads. Its institutional strengths and economic resilience provide a foundation for stability, but fiscal challenges and structural vulnerabilities create meaningful downside risks. The credit outlook for the next 12 to 18 months is contingent on demonstrable progress towards fiscal consolidation, maintenance of central bank credibility, and avoidance of policy missteps that could further erode investor confidence. Without such progress, the probability of losing investment grade status entirely remains elevated, which would increase borrowing costs and potentially trigger capital outflows, further complicating the adjustment process. The window for decisive action is narrowing, and Colombia's policymakers face difficult choices that will determine whether the country stabilises its credit profile or enters a period of sustained deterioration.