Chile

Executive Summary

Chile maintains the strongest sovereign credit profile in Latin America, underpinned by exceptionally robust institutional frameworks, prudent macroeconomic management, and a relatively moderate debt burden. As of early 2026, the country holds investment-grade ratings from all three major agencies with stable outlooks, reflecting its position as the region's highest-rated sovereign. Chile's creditworthiness is anchored by strong governance indicators, a credible monetary policy framework, and fiscal discipline that has seen the government commit to consolidation targets aimed at achieving balanced budgets by 2027. The country's public debt-to-GDP ratio of approximately 42% remains well below the 55% median for A-category peers, providing meaningful fiscal headroom despite recent increases from pandemic-era stimulus measures. Chile's external position is supported by its status as the world's largest copper producer, accounting for 24% of global output, alongside its position as the second-largest lithium producer, though this creates significant exposure to commodity price cycles and China concentration risk, with 36% of exports destined for Chinese markets.

The Chilean economy has demonstrated resilience through its post-pandemic recovery, achieving GDP growth of 2.2-2.6% in 2024 following near-stagnation in 2023. Inflation has declined substantially from its peak of approximately 14% in the third quarter of 2022 to 4.7% by early 2025, though it remains above the Central Bank's 3% target, partly due to a cumulative 60% electricity tariff increase implemented between June 2024 and February 2025. The fiscal deficit has improved markedly from a record -7.5% of GDP in 2021 to approximately -2.5% in 2024, whilst the current account deficit has narrowed to between -2.1% and -3.9% of GDP, supported by record exports of $103.3 billion. The unemployment rate remains elevated at 8.5-8.6%, reflecting persistent labour market challenges and underscoring ongoing social pressures. The administration of President Gabriel Boric achieved a significant breakthrough with comprehensive pension reform approval in January 2025, whilst the definitive end of constitutional reform efforts following two failed referendums has reduced political uncertainty and provided clearer regulatory frameworks for investors.

Chile faces a delicate balancing act between fiscal consolidation requirements and social spending pressures in a context of persistent inequality concerns and elevated unemployment. The country's heavy dependence on copper, with mining contributing 14-16% of GDP and over 50% of exports, creates vulnerability to commodity price volatility and global demand fluctuations, particularly given China's dominant role as an export destination. Whilst steel and aluminium tariffs of 25% became effective in March 2025, the direct impact on Chile has been moderate given that only 11.3% of copper exports are destined for the United States. However, potential copper tariffs threatened by the Trump administration and broader global trade uncertainty present downside risks to Chile's external accounts and investor sentiment. Political challenges persist, with President Boric's approval ratings remaining low at 30-35%, though the resolution of constitutional uncertainty has improved the policy environment.

Looking ahead, Chile's near-term growth potential remains constrained at 2-2.5% annually without successful implementation of structural reforms to enhance productivity and competitiveness. The country's ambitious green hydrogen strategy and extensive free trade agreement network covering 65 economies position it favourably for long-term economic transformation and diversification away from traditional commodity dependence. The government's commitment to fiscal consolidation, combined with the Central Bank's credible inflation-targeting framework, should support macroeconomic stability, though execution risks remain given social spending pressures and political constraints. Chile's strong institutional foundations and track record of policy credibility provide resilience against external shocks, though continued vigilance regarding copper price cycles, Chinese economic performance, and global trade dynamics will be essential for maintaining its credit profile. The successful navigation of pension reform demonstrates institutional capacity to address structural challenges, offering cautious optimism for future reform efforts necessary to unlock higher sustainable growth.

Ratings Summary

Chile maintains investment-grade sovereign credit ratings from all three major international rating agencies, reflecting the strongest credit profile in Latin America as of January 2026. S&P Global assigns Chile an A rating for foreign currency obligations and A+ for local currency debt, positioning the country two notches above Uruguay as the region's highest-rated sovereign. The agency upgraded Chile's outlook from negative to stable in October 2024, citing improved fiscal management and the government's commitment to arresting the multi-year rise in the debt burden. Moody's Investors Service rates Chile at A2 with a stable outlook, whilst Fitch Ratings maintains an A- rating, also with stable outlook following its most recent affirmation in January 2025. Fitch's assessment highlighted Chile's relatively strong sovereign balance sheet, with public debt-to-GDP projected at 42.6% compared to the 55.1% median for A-category peers, and noted the successful pension reform agreement as evidence of institutional strength. Across all three agencies, the ratings are anchored by Chile's strong governance frameworks, credible macroeconomic policy management, and sound fiscal institutions, though copper dependency and external vulnerabilities to commodity price cycles remain key monitoring factors that could influence future rating actions.

| Rating Agency | Current Rating | Outlook | Last Action Date |

|---|---|---|---|

| S&P Global | A (Foreign Currency) / A+ (Local Currency) | Stable | 15 October 2024 |

| Moody's | A2 | Stable | 20 June 2024 |

| Fitch | A- | Stable | 23 January 2025 |

Economic Indicators

| Indicator | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

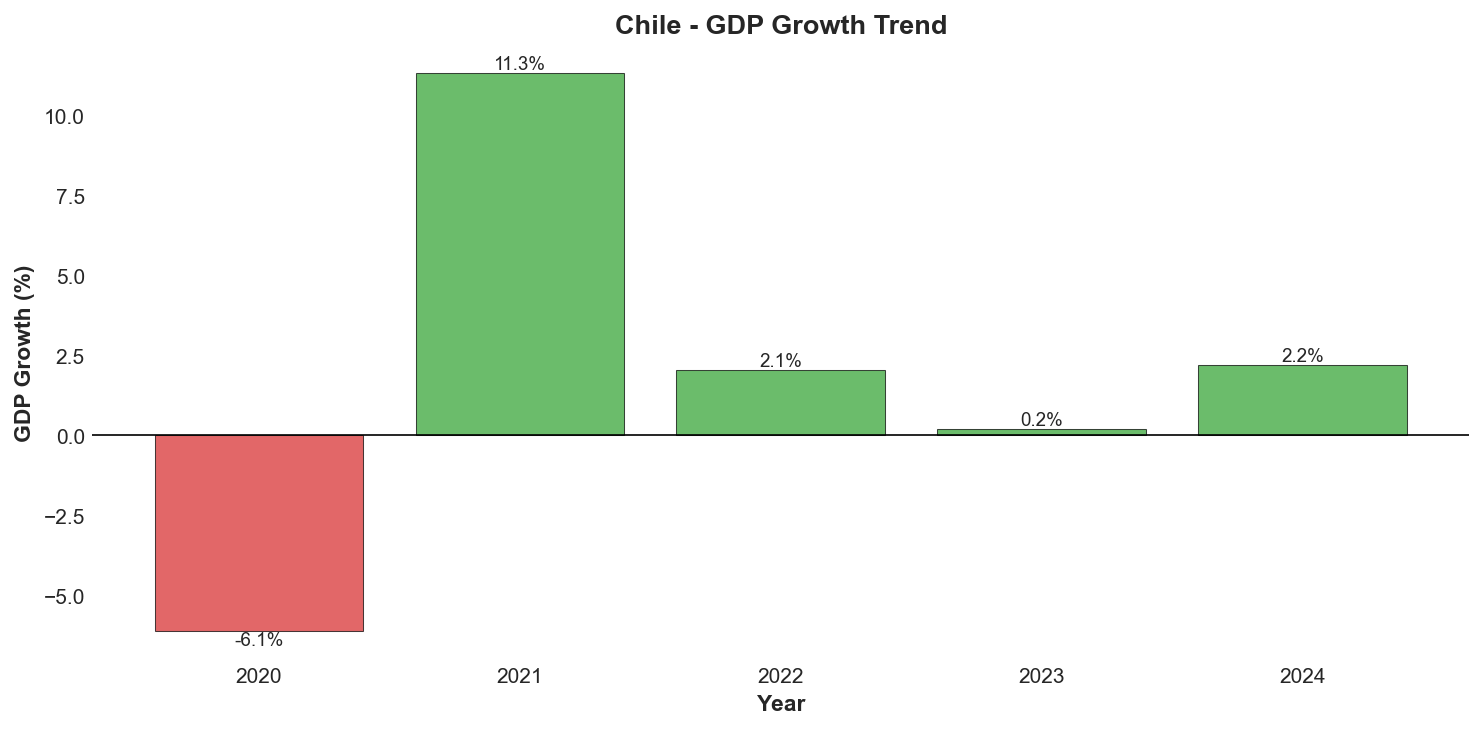

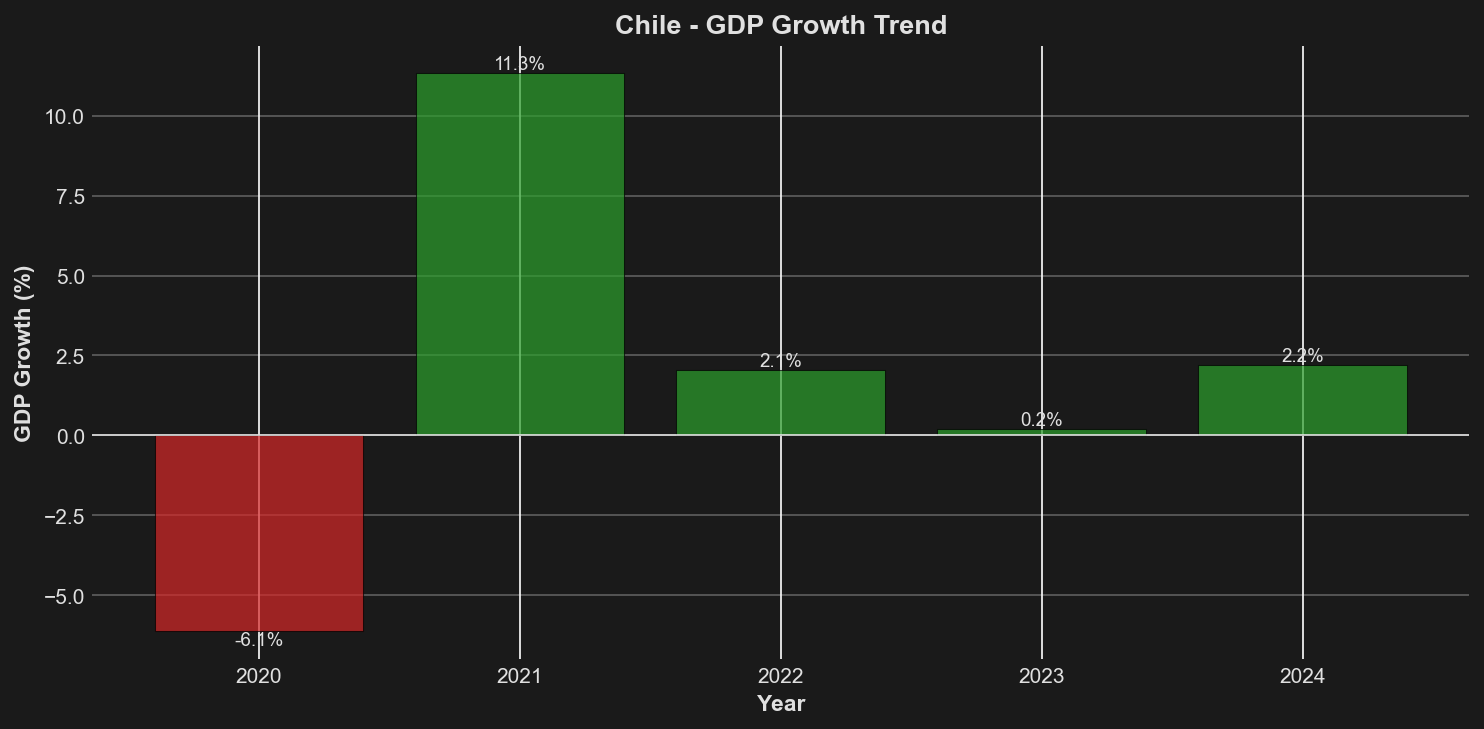

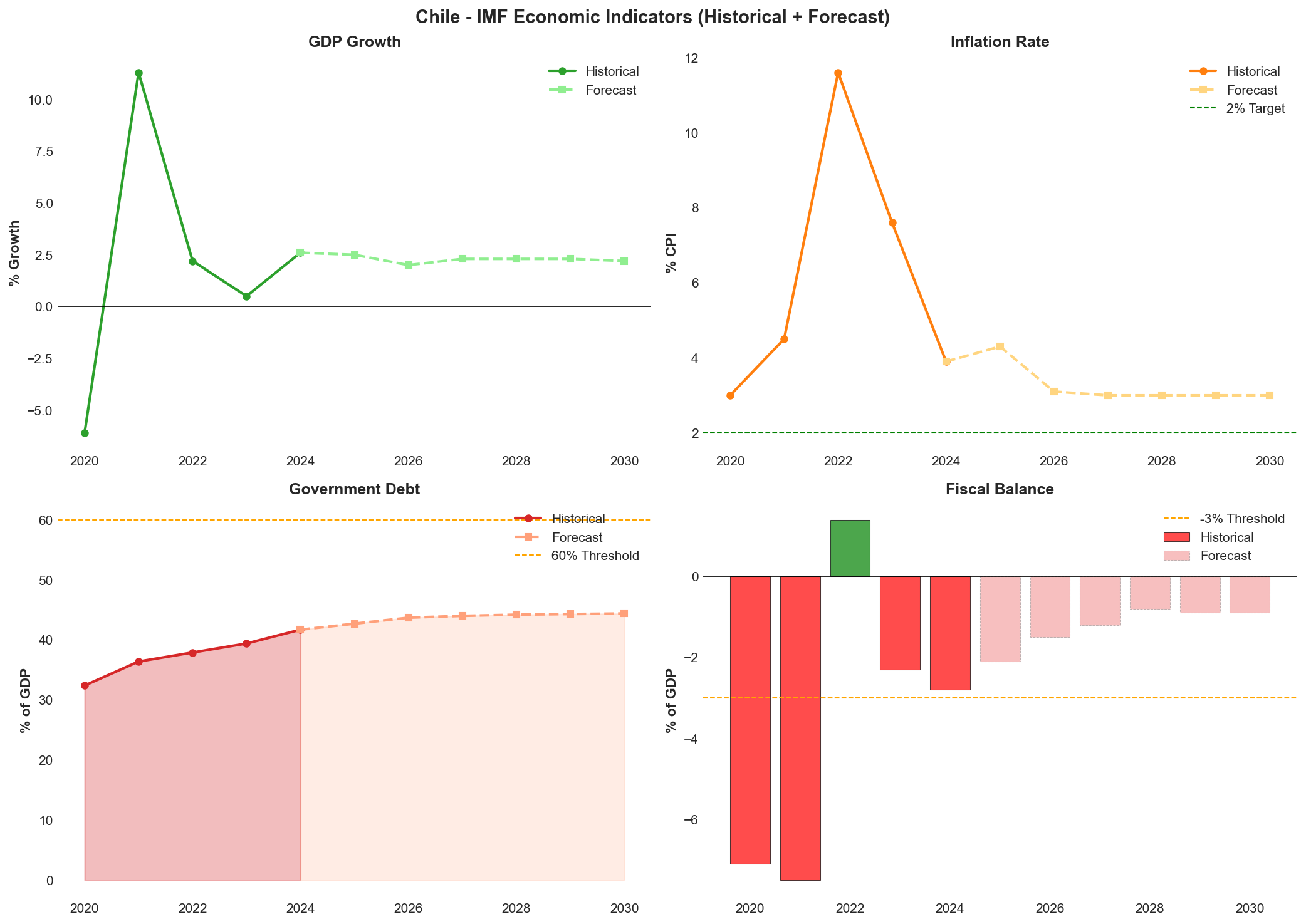

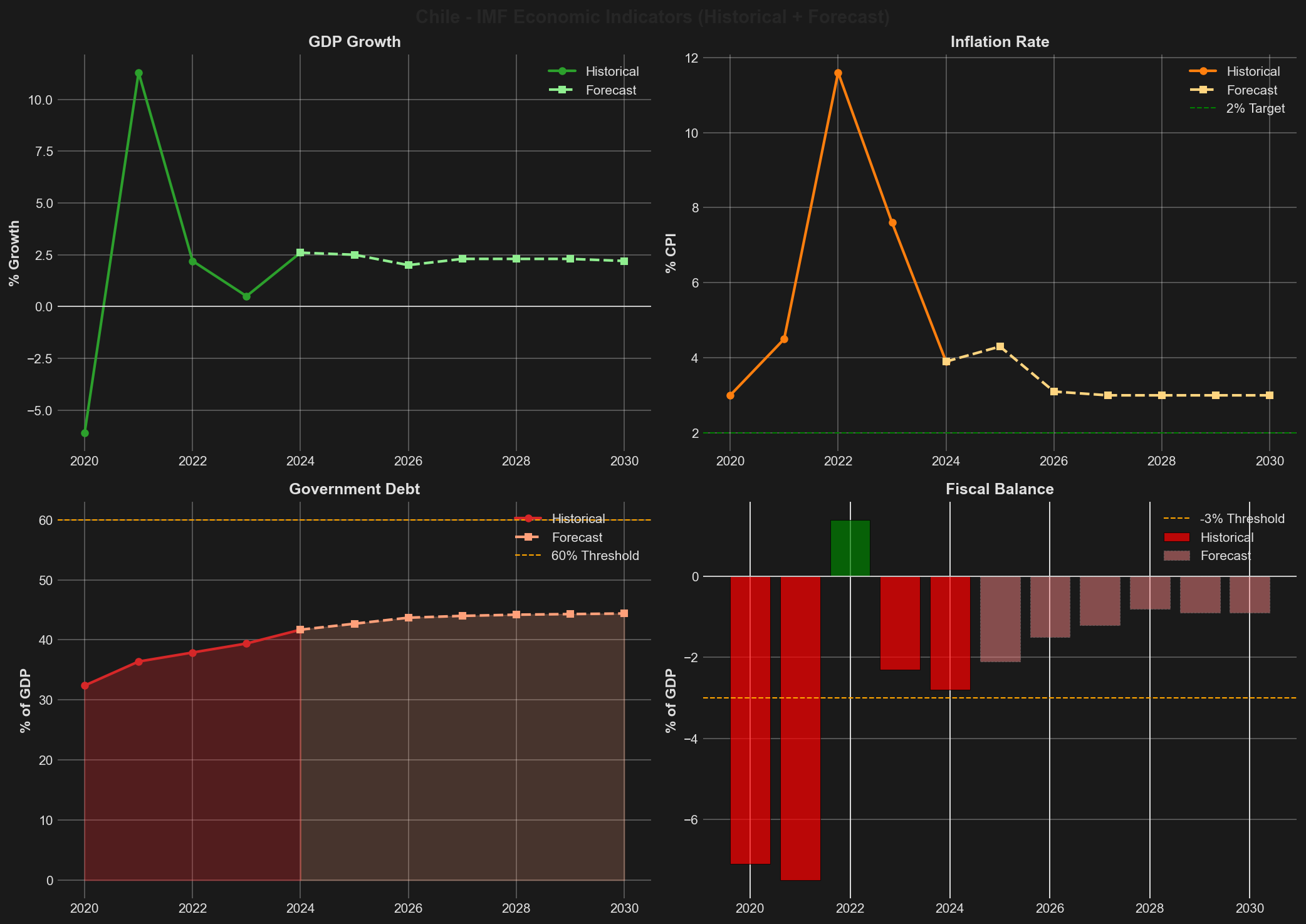

| GDP Growth (%) | -6.14 | 11.33 | 2.06 | 0.20 | 2.20-2.64 |

| Inflation Rate (%) | 3.0 | 4.5 | 11.6 | 7.6 (avg) / 3.9 (eoy) | 4.4-4.7 |

| Debt-to-GDP Ratio (%) | 32.5 | 36.3 | 37.3 | 39.4 | 42.1-44.0 |

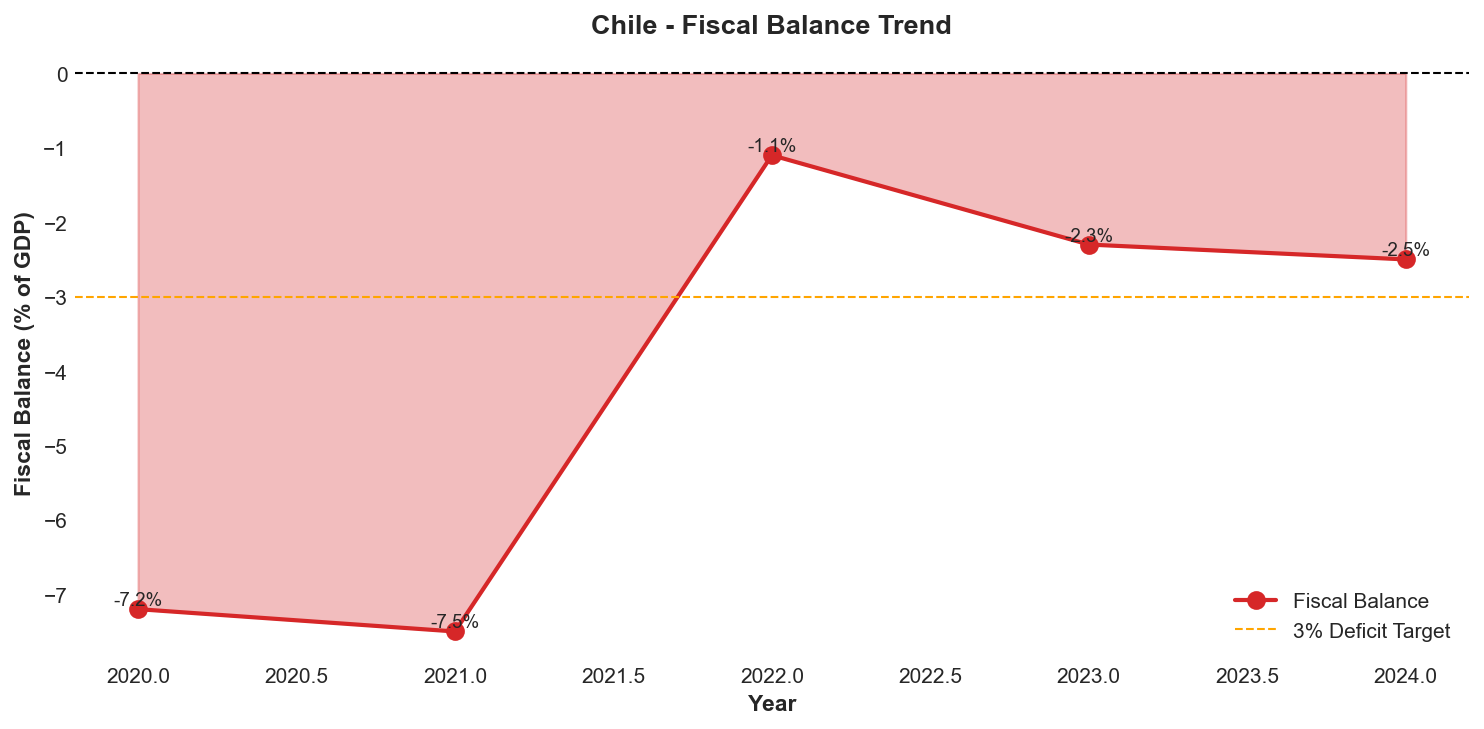

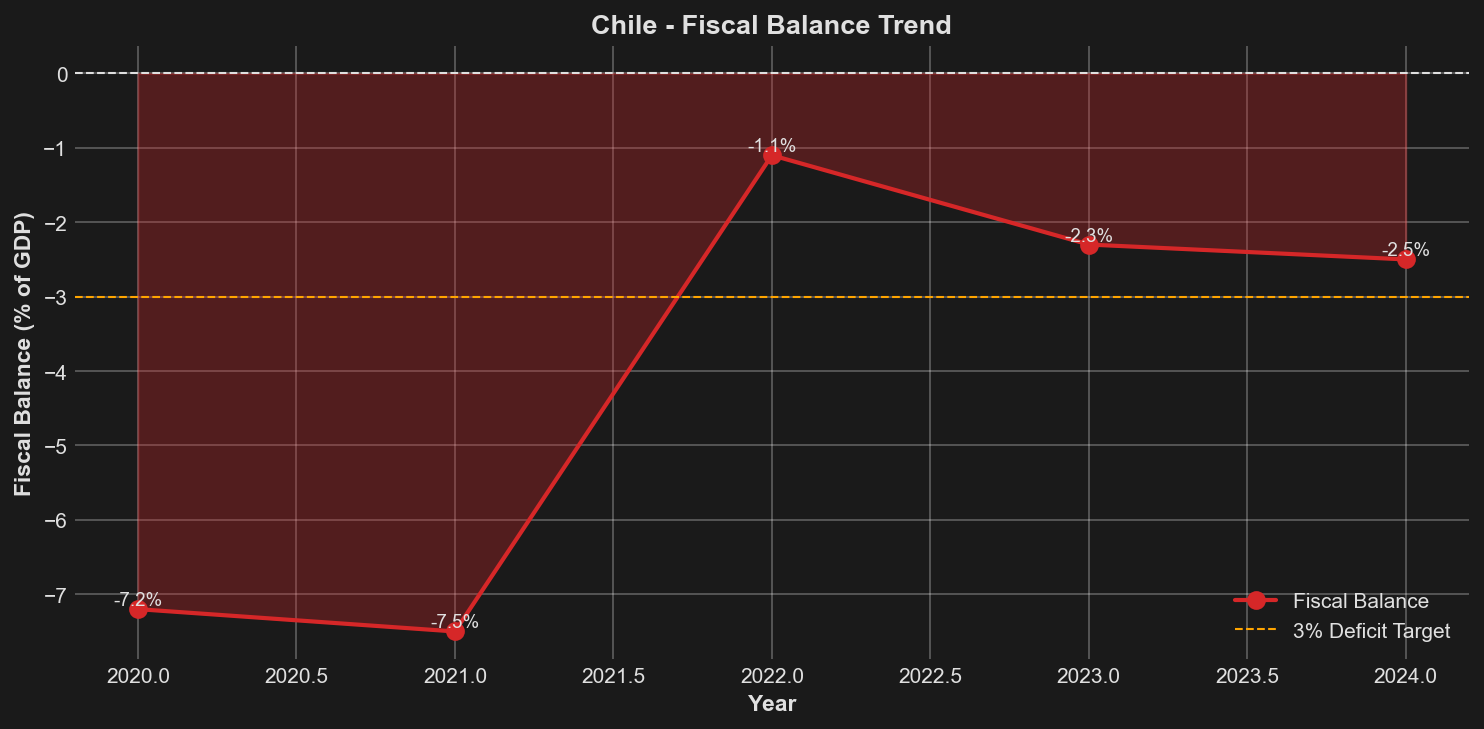

| Fiscal Balance (% GDP) | -7.2 | -7.5 | -1.1 | -2.3 | -2.5 to -2.7 |

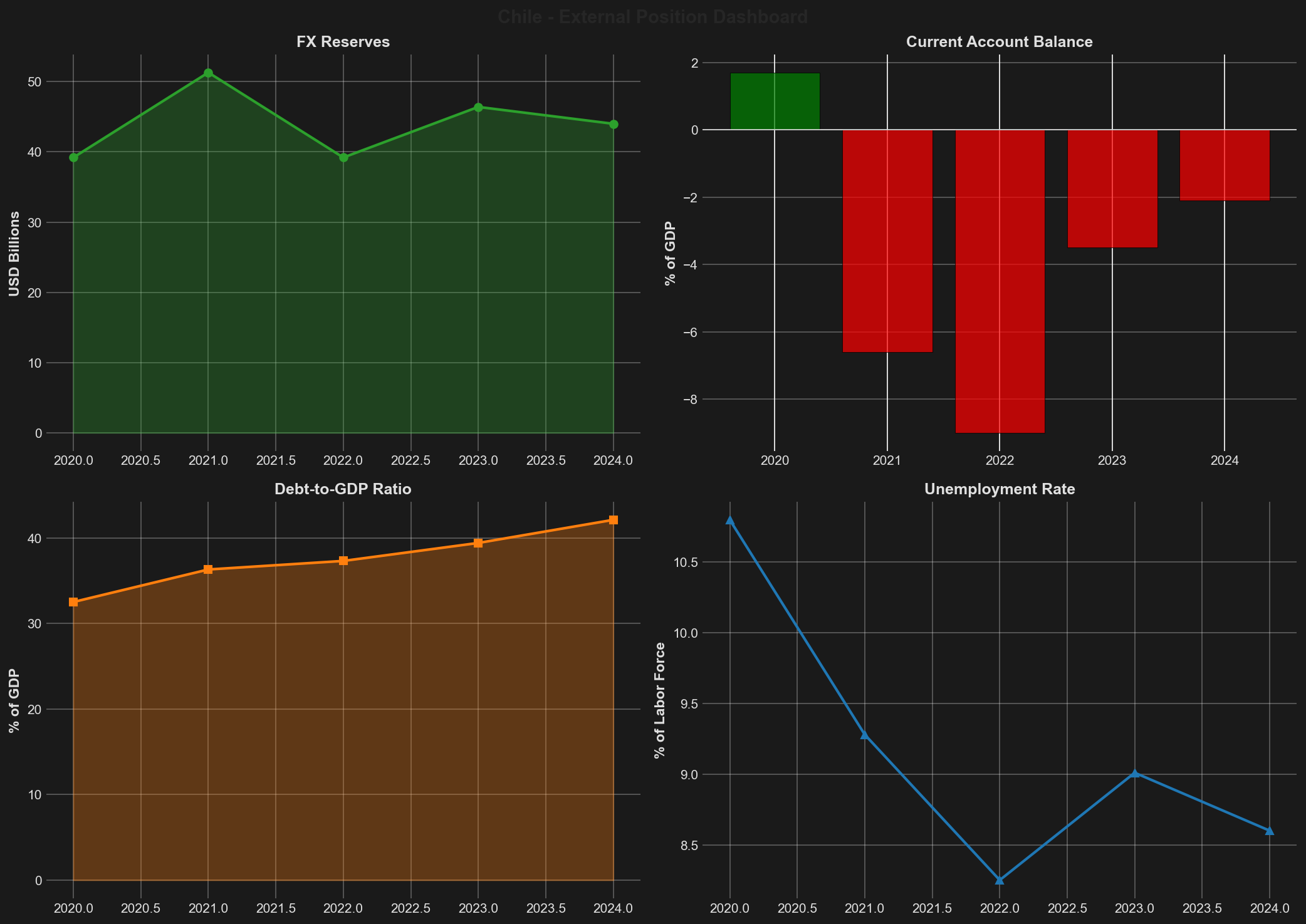

| Current Account (% GDP) | 1.7 | -6.6 | -9.0 | -3.5 | -2.1 to -3.9 |

| FX Reserves (USD bn) | 39.2 | 51.3 | 39.2 | 46.4 | 44.0-44.4 |

| Unemployment Rate (%) | 10.8 | 9.28 | 8.25 | 9.01 | 8.6 |

| Copper Price (USD/lb) | 2.80 | 4.23 | 4.00 | 4.04 | 4.18-4.20 |

The Chilean economy has demonstrated a clear trajectory of normalisation following the exceptional volatility of the pandemic period, transitioning from the dramatic 11.33% recovery surge in 2021 back towards trend growth rates of 2.2-2.6% in 2024. This moderation reflects the unwinding of extraordinary fiscal stimulus measures and the absorption of pandemic-era excess demand that had temporarily elevated growth above sustainable levels. The near-stagnation recorded in 2023 at 0.20% growth represented a necessary adjustment phase as monetary tightening worked through the economy to contain inflationary pressures. Looking ahead, IMF projections suggest Chile will maintain steady growth of approximately 2.2% through 2030, indicating a return to the country's structural growth potential in the absence of transformative productivity-enhancing reforms.

Inflation dynamics have followed a pronounced cycle, peaking at approximately 14% in the third quarter of 2022 before declining steadily to 4.7% by early 2025. Whilst this represents substantial progress in restoring price stability, the inflation rate remains above the Central Bank's 3% target, with persistence partly attributable to a cumulative 60% increase in electricity tariffs implemented between June 2024 and February 2025. The Central Bank's credible inflation-targeting framework and proactive monetary policy response have been instrumental in anchoring expectations and facilitating disinflation without precipitating a severe economic contraction. The IMF's forecast of 3.0% inflation by 2030 suggests confidence in Chile's ability to achieve convergence with its medium-term price stability objective, supporting the maintenance of accommodative real interest rates conducive to investment and growth.

Fiscal consolidation has progressed materially from the record deficit of 7.5% of GDP in 2021, with the fiscal balance improving to approximately 2.5-2.7% of GDP in 2024. This adjustment reflects both the withdrawal of emergency pandemic support measures and the government's commitment to fiscal discipline in response to rating agency concerns regarding debt trajectory. The authorities have articulated a credible medium-term fiscal framework targeting balanced budgets by 2027, with IMF projections indicating further consolidation to a deficit of 0.9% of GDP by 2030. Notwithstanding this improvement, the debt-to-GDP ratio has continued its upward trajectory, rising from 32.5% in 2020 to approximately 42-44% in 2024, though this remains comfortably below the 55.1% median for A-category sovereign peers. The IMF projects stabilisation at 44.4% of GDP by 2030, contingent upon successful implementation of the government's consolidation plans and the absence of significant adverse shocks.

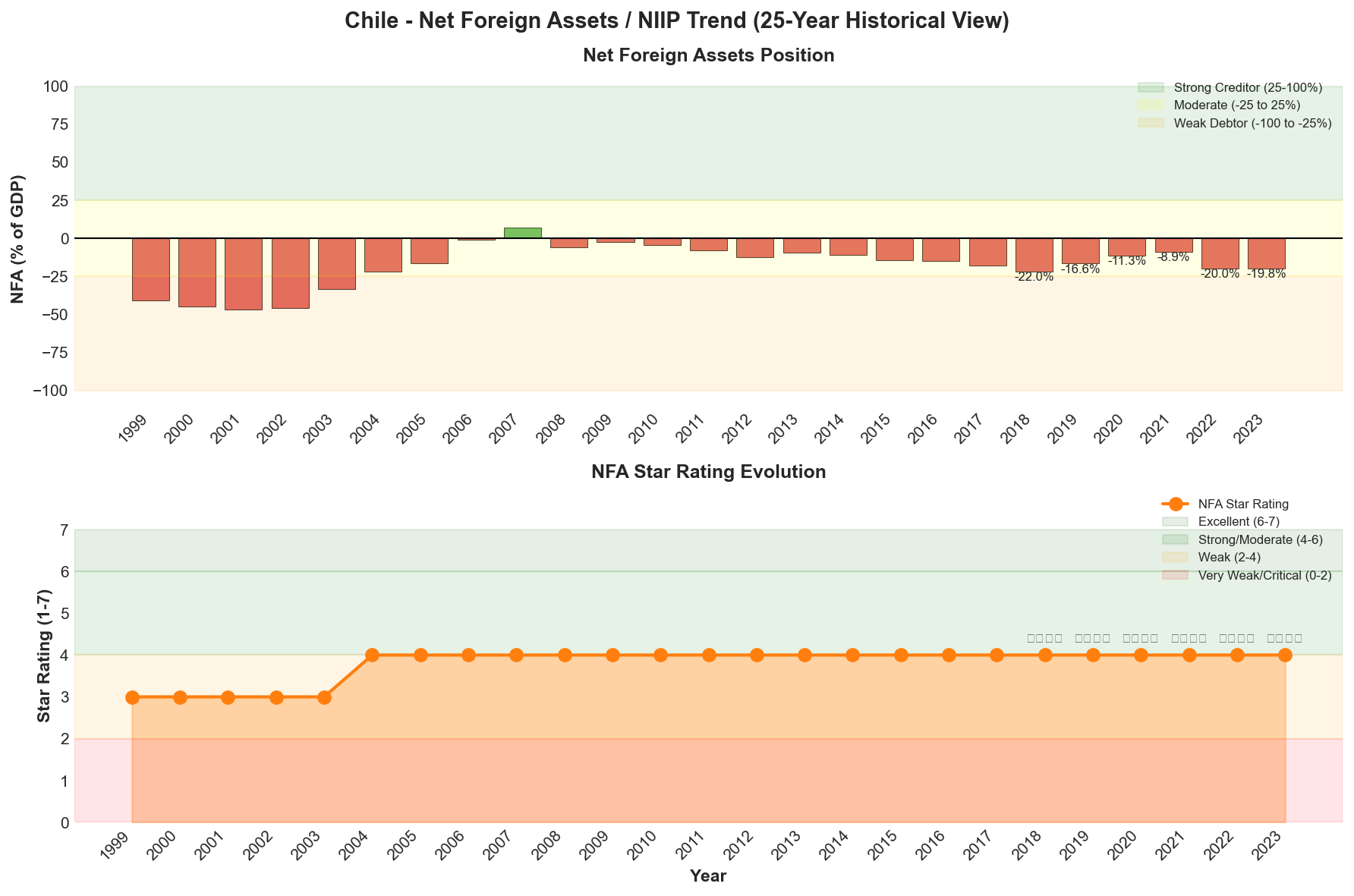

The external accounts have exhibited substantial improvement from the unsustainable current account deficit of 9.0% of GDP recorded in 2022, narrowing to approximately 2.1-3.9% of GDP in 2024. This adjustment primarily reflects the normalisation of domestic demand following the consumption boom financed by pension withdrawals and fiscal transfers during the pandemic, alongside record export performance of USD 103.3 billion in 2024 supported by resilient copper prices averaging USD 4.18-4.20 per pound. However, the IMF's projection of a widening current account deficit to 12.4% of GDP by 2030 warrants careful monitoring, as it suggests potential structural challenges in maintaining external balance over the medium term. Chile's net foreign asset position stood at -19.8% of GDP in 2023, representing a moderate net debtor position that has deteriorated from -8.9% in 2021, though it remains within manageable parameters with a four-star rating indicating moderate external vulnerability.

Foreign exchange reserves have stabilised at approximately USD 44.0-44.4 billion in 2024, providing adequate coverage for external financing needs and supporting exchange rate flexibility. The unemployment rate has remained elevated at 8.6% in 2024, declining only modestly from the 9.01% recorded in 2023, reflecting persistent labour market slack that constrains household income growth and poses social policy challenges for the government. The IMF projects gradual improvement to 7.9% by 2030, though achieving this outcome will require sustained economic expansion and successful implementation of labour market reforms to enhance job creation in the formal sector. Copper prices have remained supportive at USD 4.18-4.20 per pound in 2024, though the concentration of 52% of exports to China and potential tariff threats from the United States administration introduce downside risks to this critical revenue source that underpins both fiscal receipts and external earnings.

Net Foreign Assets & External Position

Chile's external position reflects a moderate net debtor status that has remained relatively stable within manageable parameters despite cyclical fluctuations tied to commodity price movements and capital flow dynamics. As of 2023, the country's net international investment position (NIIP) stood at -19.8% of GDP, maintaining a four-star rating in the moderate debtor category. This position represents a modest deterioration from the -8.9% recorded in 2021, when elevated copper prices and pandemic-related current account dynamics temporarily strengthened the external balance sheet. The subsequent widening to approximately -20% of GDP in 2022-2023 primarily reflects the normalisation of commodity export revenues and the impact of large current account deficits during the post-pandemic consumption boom, when the current account deficit reached -9.0% of GDP in 2022.

The trajectory of Chile's NIIP over the 2019-2023 period demonstrates both resilience and vulnerability to external shocks. The position improved markedly during 2020-2021, narrowing from -16.6% of GDP to -8.9% as copper prices surged to multi-year highs and pandemic-related import compression temporarily boosted the trade balance. However, this improvement proved transitory, with the NIIP deteriorating sharply to -20.0% in 2022 as domestic demand rebounded strongly, driving record import growth whilst copper prices moderated from their 2021 peaks. The stabilisation at -19.8% in 2023 suggests a new equilibrium as the economy has transitioned away from pandemic-era distortions, though the position remains weaker than pre-pandemic levels. This moderate debtor status, whilst manageable for an investment-grade sovereign, underscores Chile's structural dependence on external financing to support domestic investment needs that exceed national savings.

Chile's external liquidity position provides a substantial buffer against short-term vulnerabilities, with foreign exchange reserves of USD 44.0-44.4 billion as of 2024, equivalent to approximately 14-15% of GDP. These reserves, whilst modestly below the USD 46.4 billion peak recorded in 2023, remain adequate by conventional metrics, providing coverage of approximately 6-7 months of imports and substantially exceeding short-term external debt obligations. The Central Bank of Chile has demonstrated prudent reserve management throughout recent cycles, allowing reserves to decline moderately from the USD 51.3 billion peak in 2021 as intervention pressures eased following the peso's significant depreciation during 2022-2023. The flexible exchange rate regime has served as an effective shock absorber, with the peso adjusting to accommodate shifts in commodity prices and capital flows rather than requiring sustained reserve depletion.

The current account has improved markedly from the crisis levels of 2022, narrowing to between -2.1% and -3.9% of GDP in 2024 from -9.0% in 2022 and -3.5% in 2023. This consolidation reflects both cyclical factors—including the normalisation of domestic demand following the pandemic-era consumption surge—and structural improvements in export performance, with total exports reaching a record USD 103.3 billion in 2024. The trade balance remains fundamentally supported by Chile's position as the world's largest copper producer, accounting for 24% of global output, with copper and mining products comprising over 50% of total exports. However, this concentration creates significant vulnerability to commodity price cycles, with copper prices at USD 4.18-4.20 per pound in 2024 providing adequate support but remaining well below the USD 4.23 peak of 2021. The IMF's medium-term projections suggest potential challenges ahead, with the current account deficit forecast to widen to -12.4% of GDP by 2030, though this projection likely incorporates anticipated investment inflows related to Chile's ambitious green hydrogen and renewable energy development programmes.

External Vulnerability Factors

Chile's external position faces several structural vulnerabilities that warrant close monitoring despite the overall moderate risk profile. Geographic export concentration represents the most significant concern, with China accounting for 36% of total exports and 52% of copper shipments, creating substantial exposure to Chinese economic cycles and bilateral trade dynamics. The United States absorbs only 11.3% of copper exports, limiting direct exposure to US tariff policies, though the 25% steel and aluminium tariffs implemented in March 2025 and potential future copper tariffs threatened by the Trump administration could affect global commodity prices and investor sentiment. The country's extensive free trade agreement network covering 65 economies provides some diversification, though it cannot fully offset the structural dependence on Chinese demand for bulk commodities.

External financing requirements remain manageable but non-trivial, with the combination of current account deficits and debt amortisation schedules requiring continued access to international capital markets. Chile's investment-grade ratings and strong institutional credibility have historically ensured favourable financing conditions, with the sovereign able to access both dollar and local currency markets at competitive spreads. However, the moderate and potentially widening current account deficit position implies ongoing accumulation of external liabilities, which could gradually erode the NIIP if not offset by stronger export performance or increased foreign direct investment inflows. The government's fiscal consolidation path, targeting a balanced budget by 2027 from the -2.5% to -2.7% deficit recorded in 2024, should help contain external financing needs by reducing public sector borrowing requirements.

The composition of external liabilities provides some comfort, with a substantial portion consisting of foreign direct investment rather than debt obligations, reducing rollover risks and currency mismatch vulnerabilities. Chile's deep and liquid domestic capital markets, coupled with the Central Bank's credible inflation-targeting framework, have fostered development of local currency debt markets that reduce reliance on foreign currency borrowing. Nevertheless, the moderate net debtor position and structural current account deficit trajectory underscore the importance of maintaining investor confidence through continued policy credibility and institutional strength—factors that have historically distinguished Chile within the Latin American context but require ongoing reinforcement amid domestic political pressures and global economic uncertainty.

Credit Strengths & Vulnerabilities

Strengths

Chile's sovereign credit profile is underpinned by the strongest institutional frameworks in Latin America, reflected in its position as the region's highest-rated sovereign. The country maintains investment-grade ratings from all three major agencies, with S&P assigning an A rating for foreign currency debt and A+ for local currency obligations, positioning Chile two notches above Uruguay, the region's second-highest rated sovereign. This institutional strength manifests in robust democratic governance structures, credible macroeconomic policy frameworks, and a demonstrated commitment to fiscal prudence that has earned consistent recognition from rating agencies.

The government's debt position remains notably moderate at approximately 42% of GDP, substantially below the 55.1% median for A-category peers. This fiscal headroom provides meaningful capacity to absorb economic shocks whilst maintaining market confidence. The authorities have demonstrated commitment to fiscal consolidation, with the deficit improving from a pandemic peak of -7.5% of GDP in 2021 to approximately -2.5% in 2024, and a credible path towards balanced budgets by 2027. This trajectory of fiscal improvement was a key factor in S&P's decision to upgrade Chile's outlook from negative to stable in October 2024.

Chile's natural resource endowments constitute a fundamental credit strength, with the country serving as the world's largest copper producer, accounting for 24% of global output, and the second-largest lithium producer. These strategic minerals provide substantial export revenues, with total exports reaching a record $103.3 billion in 2024, whilst positioning Chile advantageously for the global energy transition. The mining sector's contribution of 14-16% of GDP and over 50% of exports generates significant fiscal revenues and foreign exchange earnings that support external stability. The country's extensive network of free trade agreements covering 65 economies further enhances trade resilience and market access, diversifying commercial relationships beyond traditional partners.

Vulnerabilities

The Chilean economy exhibits pronounced concentration risk through its heavy dependence on copper, creating significant vulnerability to commodity price cycles and global demand fluctuations. With mining contributing 14-16% of GDP and over 50% of exports, the fiscal accounts and external position remain highly sensitive to copper price movements. This vulnerability is compounded by geographic export concentration, with China accounting for 36% of total exports, creating exposure to Chinese economic cycles and bilateral relationship dynamics. Whilst only 11.3% of copper exports flow to the United States, the threat of potential copper tariffs from the Trump administration and broader global trade uncertainty present material downside risks to external accounts and investor sentiment.

Labour market conditions remain a persistent credit concern, with unemployment elevated at 8.5% as of early 2025, well above pre-pandemic levels. This elevated joblessness occurs alongside persistent inequality concerns that continue to generate social pressures and demands for increased government spending. The political environment has proven challenging, with President Gabriel Boric's administration recording approval ratings of only 30-35%, constraining the government's capacity to implement structural reforms. Whilst the definitive end of constitutional reform efforts following two failed referendums has reduced regulatory uncertainty, the low political capital limits the administration's ability to advance growth-enhancing reforms or undertake difficult fiscal adjustments.

Inflationary pressures, whilst moderating from the 14% peak in Q3 2022, remain above the Central Bank's 3% target at 4.7% in early 2025. This persistence reflects in part the impact of a 60% cumulative electricity tariff increase implemented between June 2024 and February 2025, which has sustained cost pressures across the economy. The inflation dynamic complicates monetary policy normalisation and constrains real income growth, potentially limiting consumption-driven economic expansion. The current account deficit, though improved to between -2.1% and -3.9% of GDP in 2024 from the -9.0% recorded in 2022, reflects ongoing external financing requirements that maintain vulnerability to shifts in global risk sentiment and capital flow reversals.

Opportunities

Chile's ambitious green hydrogen strategy positions the country to capitalise on the global energy transition, leveraging exceptional renewable energy resources in the Atacama Desert and Patagonian regions. The government has established regulatory frameworks and investment incentives to attract international capital to this emerging sector, with potential to diversify the export base beyond traditional copper dependency. Successful development of green hydrogen production could generate new revenue streams, create employment opportunities, and enhance Chile's position in global clean energy supply chains, whilst reducing domestic fossil fuel import requirements.

The successful approval of comprehensive pension reform in January 2025 represents a significant political breakthrough that demonstrates institutional capacity to address long-standing structural challenges. This achievement, following two failed constitutional referendums, signals potential for renewed reform momentum in other areas. The reform addresses critical social concerns regarding retirement adequacy whilst maintaining fiscal sustainability, potentially reducing social tensions that have constrained policy flexibility. This institutional demonstration may create political space for additional structural reforms in labour markets, education, and regulatory frameworks that could enhance medium-term growth potential.

The country's extensive free trade agreement network and strategic position on the Pacific Rim provide platforms for deeper integration into Asian value chains and expanding services exports. Chile's stable institutional environment and relatively sophisticated financial sector offer opportunities to develop Santiago as a regional financial hub, attracting capital flows and high-value service activities. The mining sector's technological advancement and operational expertise create potential for expanding mining services exports to other resource-rich nations, leveraging Chile's comparative advantages beyond raw commodity production.

Threats

The primary external threat stems from potential deterioration in global copper demand, particularly from China, which absorbs 52% of Chilean copper exports. A significant slowdown in Chinese construction and manufacturing activity, or a shift in Chinese industrial policy away from copper-intensive sectors, would materially impact Chile's export revenues, fiscal position, and growth trajectory. The threat of US copper tariffs, alongside the 25% steel and aluminium tariffs effective from March 2025, introduces additional uncertainty. Whilst direct US exposure is limited at 11.3% of copper exports, broader trade tensions could depress global commodity prices and risk sentiment, with spillover effects on Chilean asset valuations and capital flows.

Domestic political fragmentation and social pressures present ongoing governance challenges that could constrain policy effectiveness. President Boric's low approval ratings of 30-35% limit political capital for implementing necessary but unpopular measures, including fiscal consolidation or labour market reforms. The government faces competing pressures between fiscal consolidation targets and social spending demands in a context of elevated unemployment and persistent inequality. Failure to achieve the targeted balanced budget by 2027 could trigger negative rating actions, whilst excessive fiscal tightening risks exacerbating social tensions and unemployment, creating a difficult policy trade-off.

Chile's near-term growth potential remains constrained at 2.0-2.5% annually without successful implementation of productivity-enhancing structural reforms. This modest growth trajectory limits fiscal revenue expansion and employment generation, potentially perpetuating social pressures and political instability. The electricity tariff increases, whilst necessary to address sector imbalances, have sustained inflationary pressures that constrain real income growth and consumption. Climate-related risks, including water scarcity affecting mining operations and agricultural production, alongside increased frequency of extreme weather events, present longer-term threats to economic stability and infrastructure resilience that could require substantial adaptation investments.

Economic Analysis

Growth Dynamics and Structural Constraints

Chile's economic trajectory through 2024 demonstrates a return to trend growth following the extraordinary volatility of the pandemic period. After experiencing a severe contraction of 6.14% in 2020, the economy rebounded dramatically with 11.33% growth in 2021, driven by unprecedented fiscal stimulus including pension withdrawal programmes that injected approximately 20% of GDP into household consumption. This stimulus-fuelled expansion proved unsustainable, with growth decelerating sharply to 2.06% in 2022 and near-stagnation at 0.20% in 2023 as monetary tightening and the exhaustion of excess savings constrained domestic demand. The recovery to 2.2-2.6% growth in 2024 represents a stabilisation around Chile's potential output, which most analysts estimate at 2-2.5% annually in the absence of significant structural reforms.

The composition of growth has shifted markedly from the consumption-led boom of 2021 towards a more balanced profile anchored by external demand. Mining exports, particularly copper, have provided crucial support as global prices stabilised around USD 4.18-4.20 per pound in 2024, maintaining the elevated levels observed since 2021. The sector's contribution of 14-16% of GDP and dominance of export revenues exceeding 50% underscores Chile's continued reliance on commodity cycles despite decades of diversification efforts. Services sectors have demonstrated resilience, though construction and manufacturing remain subdued relative to pre-pandemic trends, reflecting persistent uncertainty around regulatory frameworks and investment conditions.

The labour market presents a concerning dimension of Chile's growth challenge, with unemployment elevated at 8.6% in 2024 compared to the 7-8% range typical of the pre-pandemic decade. This elevated joblessness occurs despite modest economic expansion, suggesting structural mismatches and reduced labour market dynamism. Participation rates have not fully recovered to 2019 levels, particularly amongst women and younger workers, indicating scarring effects from the pandemic and social unrest periods. Wage growth has moderated from the double-digit rates observed during the inflationary surge of 2022, aligning more closely with productivity trends, though real wage recovery remains incomplete for many segments of the workforce.

Investment dynamics constitute perhaps the most significant constraint on Chile's medium-term growth potential. Gross fixed capital formation has failed to return to pre-2019 levels as a share of GDP, reflecting persistent uncertainty stemming from the constitutional reform processes, regulatory changes, and shifting policy priorities under the Boric administration. Mining investment, traditionally a pillar of Chilean capital formation, has been dampened by permitting challenges, community opposition to projects, and concerns about future taxation and regulatory treatment. The definitive conclusion of constitutional reform efforts following two failed referendums has removed a significant source of uncertainty, potentially creating conditions for investment recovery, though the materialisation of this effect remains contingent on consistent policy implementation and continued institutional stability.

Inflation Trajectory and Price Stability Challenges

Chile's inflation experience since 2020 reflects both global supply chain disruptions and domestic policy choices that amplified price pressures. From a benign 3.0% in 2020, inflation accelerated to 4.5% in 2021 as demand stimulus began overwhelming supply capacity, then surged to 11.6% in 2022 as global commodity shocks, supply chain bottlenecks, and peso depreciation combined with domestic overheating. The peak inflation rate reached approximately 14% in the third quarter of 2022, representing the highest levels in nearly three decades and prompting aggressive monetary policy tightening.

The subsequent disinflation process has been gradual but persistent, with inflation declining to an average of 7.6% in 2023 and ending that year at 3.9%, before moderating further to 4.4-4.7% in 2024. This trajectory demonstrates the effectiveness of monetary tightening and the dissipation of temporary supply shocks, though the pace of decline has been slower than initially anticipated by policymakers. Inflation expectations, which became unanchored during the 2022 surge, have gradually re-converged towards the Central Bank's 3% target, though they remain elevated at the one-year horizon, reflecting concerns about persistent service sector inflation and indexation mechanisms embedded in the Chilean economy.

A significant complicating factor in the disinflation process has been the electricity tariff adjustment implemented between June 2024 and February 2025, which cumulatively increased household electricity costs by approximately 60%. This adjustment, whilst necessary to address accumulated deficits in the electricity sector and align tariffs with generation costs, has sustained headline inflation above the Central Bank's target range and complicated monetary policy communication. The tariff increases reflect deferred adjustments from previous years when authorities froze rates to cushion households from energy price volatility, creating a policy trade-off between short-term price stability and long-term sectoral sustainability.

Core inflation measures, which exclude volatile food and energy components, have declined more consistently than headline figures, suggesting that underlying price pressures have moderated substantially from 2022 peaks. Services inflation, however, remains sticky at elevated levels, reflecting wage indexation practices, backward-looking price-setting behaviour, and the labour-intensive nature of the sector. This persistence in services inflation represents a challenge for achieving the Central Bank's 3% target on a sustained basis and may require inflation expectations to remain firmly anchored through credible forward guidance and consistent policy implementation.

Monetary Policy Stance and Central Bank Credibility

The Central Bank of Chile has navigated an exceptionally challenging policy environment since 2021, transitioning from pandemic-era accommodation through aggressive tightening and subsequently towards policy normalisation. The monetary policy rate was raised from 0.5% in mid-2021 to a peak of 11.25% by October 2022, representing one of the most rapid tightening cycles in Chilean monetary history. This decisive action, whilst economically painful in the near term, demonstrated the Central Bank's commitment to its inflation mandate and helped prevent a more severe de-anchoring of inflation expectations.

The easing cycle commenced in mid-2023 as inflation declined and economic activity weakened, with the policy rate reduced gradually to approximately 5.25-5.50% by early 2025. This normalisation process has been calibrated carefully to balance the need for continued disinflation against risks of excessive economic weakness and labour market deterioration. The Central Bank has emphasised data-dependence and gradualism in its communication, seeking to avoid premature easing that could reignite inflation whilst remaining responsive to evolving economic conditions.

The institutional credibility of the Central Bank, reinforced by its constitutional autonomy and track record of inflation targeting since 1999, has been crucial in managing the recent inflation episode. Despite intense political pressure during periods of high inflation and economic weakness, the Bank has maintained its policy independence and technical rigour. The successful navigation of the 2022-2024 inflation surge without a complete de-anchoring of expectations or resort to heterodox policies represents a significant achievement that distinguishes Chile from several regional peers. This credibility constitutes a valuable institutional asset that supports the sovereign credit profile by reducing macroeconomic volatility and enhancing policy predictability.

Looking forward, monetary policy faces the challenge of supporting economic recovery whilst ensuring inflation converges sustainably to the 3% target. The output gap appears to have closed or turned slightly positive by late 2024, suggesting limited scope for substantial further easing without risking renewed inflation pressures. External factors, including potential commodity price volatility, exchange rate movements, and global trade policy uncertainty stemming from US tariff threats, add complexity to the policy outlook. The Central Bank's ability to maintain its credible, forward-looking approach whilst navigating these cross-currents will be essential for sustaining macroeconomic stability and supporting Chile's investment-grade credit standing.

Political & Institutional Assessment

Chile's political landscape has undergone significant evolution since President Gabriel Boric assumed office in March 2022, representing the most left-leaning government in the country's post-dictatorship era. The administration has confronted persistently low approval ratings hovering between 30 and 35 per cent throughout much of its tenure, reflecting public frustration with the pace of reform implementation and ongoing socioeconomic challenges. Despite these political headwinds, Chile's institutional framework remains amongst the strongest in Latin America, underpinning the country's investment-grade credit profile and providing continuity in macroeconomic policy management that transcends electoral cycles.

Constitutional Reform and Political Stability

The definitive conclusion of Chile's constitutional reform process following two failed referendums has materially reduced political uncertainty, a development viewed favourably by credit rating agencies. The rejection of both a progressive constitution in September 2022 and a more conservative alternative in December 2023 effectively ended the constitutional rewriting effort that had been initiated in response to the 2019 social unrest. This outcome, whilst representing a setback for President Boric's political agenda, has paradoxically enhanced regulatory clarity for investors by removing the prospect of fundamental changes to property rights, resource ownership frameworks, and economic governance structures. The 1980 constitution, albeit amended numerous times, remains in force with its market-oriented provisions intact.

The failed constitutional processes revealed deep ideological divisions within Chilean society but also demonstrated the resilience of democratic institutions. The mandatory nature of both referendums, combined with high participation rates, reinforced the legitimacy of the outcomes and reduced the likelihood of renewed constitutional challenges in the near term. This political stabilisation has allowed policymakers to refocus attention on incremental reforms within the existing constitutional framework rather than pursuing transformative institutional change.

Pension Reform Achievement

The approval of comprehensive pension reform in January 2025 represents the Boric administration's most significant legislative accomplishment and provides evidence of Chile's capacity for political compromise on contentious issues. The reform addresses longstanding concerns about the adequacy of retirement benefits under Chile's fully privatised pension system, which has been criticised for generating insufficient replacement rates, particularly for lower-income workers and women with interrupted career trajectories. The agreement required extensive negotiations amongst government officials, opposition parties, and stakeholders, demonstrating that Chile's political system retains functionality despite polarisation.

The pension reform is expected to increase employer contributions and enhance solidarity mechanisms to improve benefit levels for vulnerable populations, though specific implementation details will influence its fiscal impact over the medium term. Rating agencies have interpreted the reform's passage as a positive signal regarding institutional strength and the government's ability to navigate complex political terrain to achieve policy objectives. However, the reform also underscores the persistent social pressures facing Chilean policymakers, as demands for enhanced social protection must be balanced against fiscal consolidation requirements and the imperative to maintain investment-grade creditworthiness.

Institutional Quality and Governance

Chile's institutional framework significantly outperforms regional peers across multiple governance dimensions, providing a crucial foundation for its superior credit rating. The country benefits from an independent and technically proficient central bank that has successfully navigated the inflation cycle, raising policy rates aggressively to combat price pressures in 2022-2023 before beginning a gradual easing cycle as inflation declined towards target. The Central Bank of Chile's credibility and operational autonomy insulate monetary policy from political interference, enabling counter-cyclical responses to economic shocks.

Fiscal institutions similarly demonstrate strength, with the government adhering to structural balance rules and maintaining transparent reporting frameworks. The commitment to fiscal consolidation, targeting a balanced budget by 2027, reflects institutional discipline despite political pressures for increased social spending. Chile's public financial management systems, procurement processes, and regulatory frameworks are well-developed by emerging market standards, contributing to relatively low corruption levels and efficient public service delivery.

The judiciary maintains independence, and property rights protections remain robust, though indigenous land rights issues in southern regions occasionally generate tensions. Chile's extensive network of free trade agreements covering 65 economies reflects decades of consistent trade policy orientation that has survived multiple changes in government, demonstrating institutional continuity in strategic economic areas.

Political Outlook and Reform Agenda

Looking ahead to the November 2025 presidential and congressional elections, Chile faces a period of political transition that will test institutional resilience. President Boric is constitutionally barred from seeking re-election, and polling suggests a competitive electoral environment with no clear frontrunner. The political spectrum remains fragmented, with traditional centre-right and centre-left coalitions competing alongside newer movements that emerged from the 2019 protests. This fragmentation may complicate coalition-building and governance in the next administration, potentially constraining the scope for ambitious policy initiatives.

The incoming government will inherit significant challenges, including elevated unemployment at 8.5 per cent, persistent inequality concerns, and the need to continue fiscal consolidation whilst addressing social demands. The pension reform implementation will require careful management, and additional reforms to healthcare, education, and taxation remain on the political agenda. However, the conclusion of constitutional reform efforts and the demonstrated capacity for legislative compromise on pensions suggest that Chile's institutional framework can accommodate incremental policy adjustments without threatening macroeconomic stability.

The political environment also reflects ongoing debates about resource nationalism, particularly regarding lithium and copper extraction. Whilst Chile has maintained an open investment climate in mining, proposals for increased state participation and higher royalties periodically surface, creating uncertainty for long-term investment planning. The government's ability to balance resource revenue optimisation with the need to attract private capital for mining expansion and green hydrogen development will influence Chile's economic trajectory and credit profile over the medium term.

Overall, Chile's political and institutional assessment reflects a mature democracy with strong governance frameworks that provide credit stability despite periodic political turbulence. The country's institutional quality significantly exceeds what would typically be expected at its income level, representing a key rating strength that partially offsets vulnerabilities related to commodity dependence and external exposure. The capacity for political compromise, evidenced by the pension reform achievement, suggests that Chile can navigate social pressures through incremental policy adjustments rather than disruptive changes, supporting the stable outlook maintained by all three major rating agencies.

Banking Sector & Financial Stability

Chile's banking sector represents a cornerstone of the country's investment-grade credit profile, characterised by robust capitalisation, prudent risk management frameworks, and sophisticated regulatory oversight that ranks among the strongest in Latin America. The financial system has demonstrated considerable resilience through multiple stress episodes, including the social unrest of 2019, the COVID-19 pandemic, and the subsequent inflationary cycle, emerging with balance sheet strength that continues to support economic activity whilst maintaining stability.

Sector Structure and Capitalisation

The Chilean banking system comprises approximately 24 institutions managing combined assets equivalent to roughly 120% of GDP, with the sector dominated by five major banks that control approximately 70% of total system assets. This concentration has fostered operational efficiency whilst maintaining competitive dynamics that have driven innovation in digital banking and financial inclusion initiatives. Foreign participation remains significant, with Spanish and Canadian institutions maintaining substantial operations that contribute to knowledge transfer and adherence to international best practices.

Capital adequacy ratios across the system remain comfortably above regulatory minimums, with the sector maintaining a Tier 1 capital ratio averaging 10-11% and total capital ratios near 14-15% as of late 2024. These buffers exceed Basel III requirements and provide substantial cushioning against potential credit deterioration. The Central Bank of Chile and the Financial Market Commission (CMF) have implemented countercyclical capital buffer frameworks that adjust requirements based on credit cycle dynamics, demonstrating the sophisticated macroprudential approach that underpins systemic stability.

Asset Quality and Credit Dynamics

Non-performing loan ratios have remained contained at approximately 2.0-2.5% of total loans throughout 2024, reflecting both the quality of underwriting standards and the gradual economic recovery following the 2023 near-stagnation. Consumer lending segments, particularly unsecured personal loans and credit cards, exhibit higher delinquency rates in the 4-6% range, consistent with elevated unemployment levels of 8.5% and persistent household financial pressures stemming from inflation that peaked at 14% in 2022. Commercial and mortgage portfolios demonstrate stronger performance, with NPL ratios typically below 2%, supported by conservative loan-to-value requirements and rigorous income verification protocols.

Provisioning coverage ratios across the system average 120-140% of non-performing exposures, providing adequate buffers against potential losses. Banks have maintained disciplined provisioning practices throughout the economic cycle, with forward-looking expected credit loss models implemented in accordance with IFRS 9 standards. The pension reform approved in January 2025, which allows partial withdrawals whilst establishing mandatory contribution increases, presents both opportunities and risks for the banking sector. Whilst increased liquidity may temporarily boost deposit bases, the reform could also affect long-term savings patterns and mortgage market dynamics as households adjust financial planning strategies.

Liquidity and Funding Profiles

Chilean banks maintain healthy liquidity positions, with loan-to-deposit ratios averaging 90-95% across the system, indicating balanced funding structures that reduce reliance on wholesale markets. The sector's access to international capital markets remains robust, with major institutions regularly issuing bonds in both domestic and international markets at spreads that reflect Chile's strong sovereign rating. Foreign currency funding represents approximately 15-20% of total liabilities, creating manageable currency mismatches that are largely hedged through derivative instruments and natural hedges from trade finance activities.

The Central Bank's monetary policy normalisation, with the benchmark rate declining from a peak of 11.25% in late 2022 to approximately 5.25-5.50% by early 2025, has supported net interest margin compression whilst stimulating credit demand. Banks have adapted through operational efficiency improvements and diversification into fee-generating activities, including wealth management, insurance distribution, and transaction banking services. Deposit growth has remained stable at 4-6% annually, though competition for retail deposits has intensified as customers have become more rate-sensitive following the inflationary episode.

Regulatory Environment and Supervision

The Financial Market Commission exercises comprehensive oversight authority, conducting regular stress tests that evaluate resilience against scenarios including copper price shocks, interest rate volatility, and credit deterioration. Recent stress testing exercises conducted in 2024 demonstrated that major banks could withstand severe adverse scenarios whilst maintaining capital ratios above regulatory minimums, though profitability would face significant pressure. The regulatory framework incorporates risk-based supervision, corporate governance requirements, and consumer protection standards that align with international benchmarks established by the Basel Committee and Financial Stability Board.

Chile's adoption of Basel III standards has proceeded methodically, with full implementation of liquidity coverage ratios and net stable funding ratios achieved ahead of many emerging market peers. The CMF has also implemented enhanced disclosure requirements and resolution planning frameworks that reduce systemic risk and provide authorities with tools to manage potential bank failures without taxpayer-funded bailouts. These institutional strengths contribute materially to rating agency assessments, with Moody's assigning high scores for banking sector strength in its sovereign methodology.

Systemic Risks and Vulnerabilities

Despite overall sector resilience, several vulnerabilities warrant monitoring. Household indebtedness remains elevated at approximately 75-80% of disposable income, though this has declined from pandemic-era peaks following the extraordinary pension withdrawal programmes that injected liquidity into the economy during 2020-2021. Mortgage lending, which represents roughly 30% of total system loans, faces potential pressure from property market adjustments, particularly in Santiago where prices increased substantially during the commodity boom years. However, conservative underwriting standards with typical loan-to-value ratios of 80% or below provide meaningful protection against potential price corrections.

The banking sector's indirect exposure to copper price volatility through corporate lending to mining companies and related service providers creates cyclical vulnerabilities, though diversification across sectors has increased over time. Approximately 15-20% of commercial loan portfolios maintain direct or indirect linkages to mining activities, creating transmission channels through which commodity price shocks could affect asset quality. Banks have developed sophisticated risk management frameworks for commodity-exposed lending, including covenant structures and hedging requirements that mitigate downside scenarios.

Climate-related financial risks have gained prominence in supervisory frameworks, with the CMF requiring banks to develop climate risk assessment capabilities and disclosure practices. Chile's vulnerability to physical climate risks, including water scarcity affecting mining operations and agricultural lending, alongside transition risks from the global shift toward renewable energy, necessitates ongoing adaptation of risk management practices. The country's ambitious green hydrogen strategy presents opportunities for project finance activities whilst requiring banks to develop expertise in emerging technologies and associated risk profiles.

Financial Stability Assessment

Overall, Chile's banking sector continues to function as a source of credit strength rather than vulnerability within the sovereign credit profile. The combination of strong capitalisation, prudent regulatory oversight, and demonstrated resilience through stress episodes provides confidence in the system's ability to support economic activity whilst maintaining stability. Profitability metrics, with return on equity averaging 12-15% across major institutions, remain healthy by regional standards, though margin compression from monetary policy normalisation and competitive pressures may constrain earnings growth in the near term.

The sector's integration with international financial markets through foreign ownership, cross-border funding, and correspondent banking relationships enhances access to global capital whilst creating potential transmission channels for external shocks. However, the Central Bank's substantial foreign exchange reserves of approximately USD 44 billion and the flexible exchange rate regime provide important shock absorbers that reduce systemic vulnerabilities. The banking sector's capacity to intermediate capital flows and support trade finance activities remains essential to Chile's external sector performance, particularly given the concentration of exports to China and exposure to commodity price cycles.

Looking ahead, the banking sector faces a transitional period as the economy navigates fiscal consolidation requirements, structural reform implementation, and adaptation to global trade uncertainties including potential US tariff measures. The sector's ability to maintain credit provision whilst managing asset quality through this adjustment period will prove crucial to supporting the 2-2.5% annual growth trajectory anticipated over the medium term. Rating agencies continue to view the banking sector as a stabilising force within Chile's credit profile, with systemic risks remaining manageable and regulatory frameworks providing robust safeguards against potential instability.

Outlook & Scenarios

Short-Term Outlook (12 months)

Chile's near-term credit trajectory remains stable, underpinned by continued fiscal consolidation efforts and moderating inflation dynamics. Over the next twelve months, the economy is expected to maintain growth within the 2.0-2.5% range, supported by recovering domestic demand and sustained copper exports, though constrained by elevated unemployment levels around 8.5% and limited productivity gains. The Central Bank of Chile is likely to maintain an accommodative monetary stance as inflation converges towards the 3% target, having already declined from its 2022 peak to approximately 4.7% by early 2025. The completion of electricity tariff adjustments, which cumulatively increased 60% between June 2024 and February 2025, should alleviate upward price pressures in the coming quarters.

Fiscal performance will remain a critical monitoring factor, with the government targeting a deficit reduction to approximately 1.8-2.0% of GDP by end-2026 as part of its commitment to achieve balanced budgets by 2027. The successful passage of pension reform in January 2025 demonstrates the administration's capacity to navigate complex legislative processes despite low approval ratings, though implementation challenges and potential resistance to further structural reforms may constrain policy flexibility. The external position is expected to remain manageable, with the current account deficit projected to narrow further towards 2.0-2.5% of GDP, supported by robust copper prices in the USD 4.00-4.30 per pound range and diversified export markets.

The principal near-term risk stems from global trade policy uncertainty, particularly potential US tariffs on copper imports under the Trump administration. Whilst direct exposure to US markets is moderate at 11.3% of copper exports compared to 52% destined for China, broader commodity price volatility and deteriorating investor sentiment could pressure Chile's external accounts and fiscal revenues. The March 2025 implementation of 25% steel and aluminium tariffs has had limited direct impact, but escalation of protectionist measures represents a material downside scenario. Domestically, the November 2025 municipal and regional elections will provide an important gauge of political sentiment ahead of the 2026 presidential election cycle, with potential implications for policy continuity and reform momentum.

Medium-Term Outlook (1-3 years)

Chile's medium-term credit profile will be shaped by its ability to execute fiscal consolidation whilst addressing structural economic challenges and capitalising on emerging opportunities in green energy transition. The government's commitment to achieving fiscal balance by 2027 represents a credible anchor for debt stabilisation, with public debt projected to peak around 43-45% of GDP before gradually declining. Successful implementation of this consolidation path would maintain Chile's favourable position relative to A-category peers, whose median debt burden stands at 55.1% of GDP. However, execution risks remain substantial given persistent social spending pressures, inequality concerns, and the political challenges of implementing expenditure restraint in an environment of modest economic growth.

Structural growth potential over the 2026-2028 period is likely to remain constrained at 2.0-2.5% annually absent significant productivity-enhancing reforms. The pension reform approved in January 2025, whilst politically significant, primarily addresses social protection gaps rather than capital accumulation dynamics that could boost investment rates. Labour market rigidities, regulatory uncertainty following two failed constitutional reform attempts, and limited progress on education and innovation policies continue to constrain Chile's growth ceiling. The country's demographic transition, with an ageing population and declining labour force participation rates, will increasingly weigh on potential output growth.

Chile's ambitious green hydrogen strategy and position as a global leader in copper and lithium production present substantial medium-term opportunities aligned with global decarbonisation trends. The country's renewable energy potential, particularly in solar and wind resources, positions it favourably to develop competitive green hydrogen production capabilities, potentially diversifying the economic base beyond traditional mining activities. The extensive free trade agreement network covering 65 economies provides market access advantages, though realising these opportunities requires sustained investment in infrastructure, regulatory clarity, and technological development.

Rating Scenarios

Chile's investment-grade ratings appear secure over the medium term under the baseline scenario of continued prudent macroeconomic management and gradual fiscal consolidation. However, rating trajectories could diverge based on fiscal performance, external conditions, and structural reform progress.

Upside Scenario (Positive Outlook or Upgrade): A positive rating action would require demonstrable progress on multiple fronts. Successful fiscal consolidation achieving balanced budgets by 2027 whilst maintaining debt-to-GDP ratios below 40% would strengthen Chile's fiscal metrics relative to rating peers. Implementation of structural reforms that credibly lift potential growth above 3% annually, particularly through productivity enhancements, labour market improvements, or successful diversification into green hydrogen and advanced manufacturing, would address concerns about growth constraints. Reduced copper dependency through economic diversification, evidenced by mining's contribution to GDP declining below 12% and export concentration diminishing, would mitigate commodity cycle vulnerabilities. Additionally, sustained political stability with broad consensus on market-friendly policies and successful navigation of the 2026 presidential transition would reinforce institutional strength perceptions.

Baseline Scenario (Stable Outlook Maintained): The most probable scenario involves Chile maintaining its current rating levels with stable outlooks across agencies. This assumes fiscal consolidation proceeds broadly as planned, with deficits declining to 1.5-2.0% of GDP by 2027 and debt stabilising around 43-45% of GDP. Economic growth would remain in the 2.0-2.5% range, sufficient to support gradual employment recovery and maintain social stability without generating significant fiscal pressures. Copper prices would fluctuate within the USD 3.80-4.50 per pound range, providing adequate export revenues and fiscal income without dramatic volatility. The external position would remain manageable with current account deficits below 3% of GDP and foreign exchange reserves maintained above USD 40 billion. Political dynamics would continue to reflect polarisation and modest approval ratings for the administration, but without destabilising institutional frameworks or triggering major policy reversals.

Downside Scenario (Negative Outlook or Downgrade): Rating pressure would emerge from fiscal slippage, with deficits persisting above 3% of GDP beyond 2026 and debt trajectories rising towards 50% of GDP, eroding Chile's comparative advantage versus rating peers. A sustained copper price decline below USD 3.50 per pound, potentially triggered by Chinese economic slowdown or global recession, would simultaneously pressure fiscal revenues, export earnings, and growth prospects. Escalating trade protectionism, including implementation of significant US tariffs on copper imports or broader deterioration in global trade conditions, could materially impact Chile's external accounts given the economy's openness and commodity dependence. Domestically, political instability manifesting through renewed constitutional conflicts, inability to pass necessary fiscal measures, or erosion of central bank independence would undermine institutional strength perceptions. Social unrest comparable to the 2019 protests, potentially triggered by inadequate progress on inequality or pension system shortcomings, could force expansionary fiscal policies incompatible with consolidation targets.

The balance of risks appears tilted slightly towards the baseline scenario, with Chile's strong institutional frameworks and track record of prudent policy management providing resilience against moderate shocks. However, the narrow growth potential and persistent structural challenges limit upside possibilities, whilst external vulnerabilities to commodity cycles and trade policy shifts represent material downside risks requiring continuous monitoring.

Conclusion

Chile's sovereign credit profile remains the strongest in Latin America, underpinned by robust institutional frameworks, prudent macroeconomic management, and a moderate debt burden that compares favourably to rating peers. The country's investment-grade ratings across all three major agencies, with stable outlooks as of early 2026, reflect confidence in Chile's capacity to navigate near-term challenges whilst maintaining fiscal discipline. The government's commitment to achieving balanced budgets by 2027, combined with successful inflation reduction from the 2022 peak to approximately 4.7% by early 2025, demonstrates effective policy coordination between fiscal and monetary authorities.

The resolution of constitutional uncertainty following two failed referendums has provided greater regulatory clarity for investors, whilst the landmark pension reform agreement in January 2025 evidences the resilience of Chile's democratic institutions despite the Boric administration's low approval ratings. These developments have contributed to improved market sentiment and support the stable outlook trajectory. Chile's external position remains solid, with record exports of $103.3 billion in 2024 and foreign exchange reserves of approximately $44 billion providing adequate buffers against external shocks.

Nevertheless, significant vulnerabilities persist that constrain Chile's credit profile and limit upside rating potential in the medium term. The economy's structural dependence on copper, which accounts for over 50% of exports and 14-16% of GDP, creates inherent volatility linked to global commodity cycles and Chinese demand dynamics, with 36% of exports concentrated in a single market. The elevated unemployment rate of 8.5% and persistent inequality concerns generate ongoing social spending pressures that complicate fiscal consolidation efforts. Furthermore, the potential for US copper tariffs under the Trump administration and broader global trade tensions present material downside risks to export revenues and economic growth.

Chile's near-term growth potential remains constrained at 2.0-2.5% annually without successful implementation of structural reforms to enhance productivity and diversify the economic base. The ambitious green hydrogen strategy and renewable energy transition offer promising long-term opportunities for economic transformation, though these initiatives require sustained investment and supportive policy frameworks over multiple electoral cycles. The country's extensive network of free trade agreements covering 65 economies provides important diversification benefits, yet cannot fully offset the concentration risks inherent in Chile's export structure.

Looking ahead, Chile's credit trajectory will depend critically on the government's ability to execute fiscal consolidation whilst managing social demands, the evolution of copper prices and Chinese economic growth, and progress on structural reforms to lift potential output. The stable outlooks from all three rating agencies suggest limited near-term rating migration risk, with Chile's strong governance and policy credibility providing resilience against moderate shocks. However, sustained improvement in the credit profile would require meaningful economic diversification, reduction in external vulnerabilities, and demonstration of fiscal consolidation achievement without compromising social stability. Conversely, downside risks include failure to meet fiscal targets, prolonged social unrest, or a severe deterioration in copper markets that would pressure external accounts and fiscal revenues simultaneously.