Brazil

Executive Summary

Brazil's sovereign credit profile as of January 2026 reflects a maturing emerging market economy navigating the complex interplay between demonstrated economic resilience and persistent structural vulnerabilities. The country maintains sub-investment grade ratings across all three major agencies, with Moody's positioning Brazil closest to investment grade at Ba1 with a positive outlook, whilst S&P and Fitch maintain BB ratings with stable outlooks. This positioning reflects recognition of Brazil's substantial economic strengths—including a large, diversified $2.8 trillion economy, abundant natural resources spanning agricultural commodities and energy reserves, and a resilient banking sector with robust capitalisation—balanced against ongoing concerns regarding fiscal sustainability and institutional capacity for reform implementation.

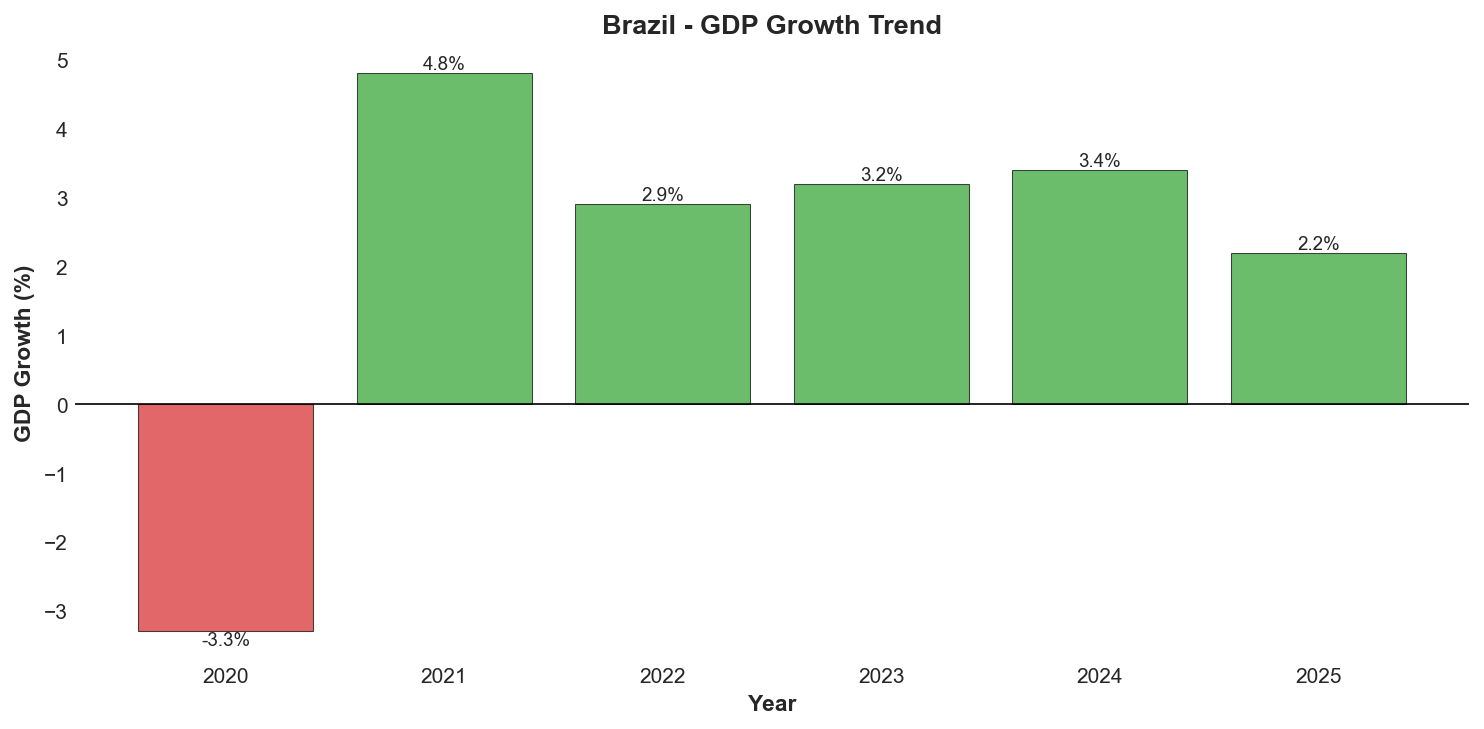

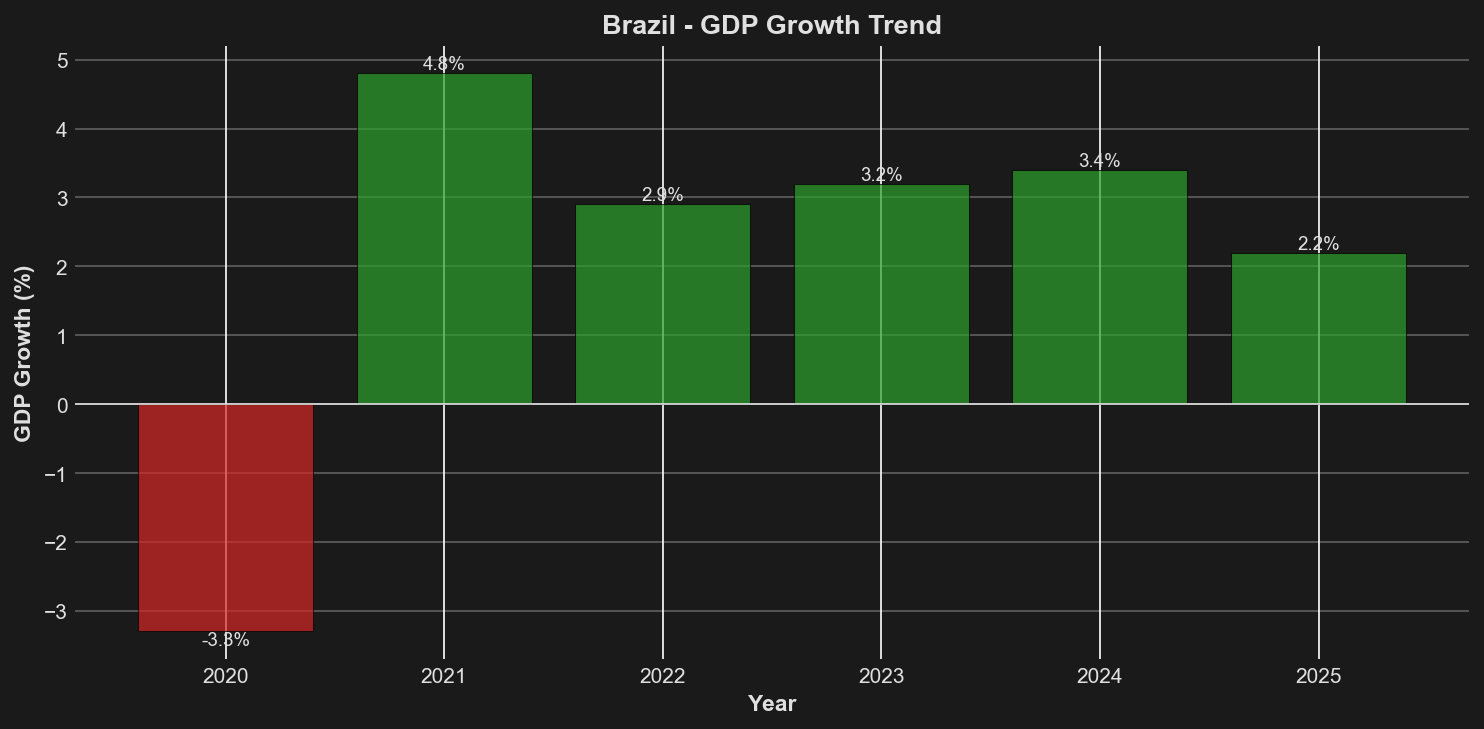

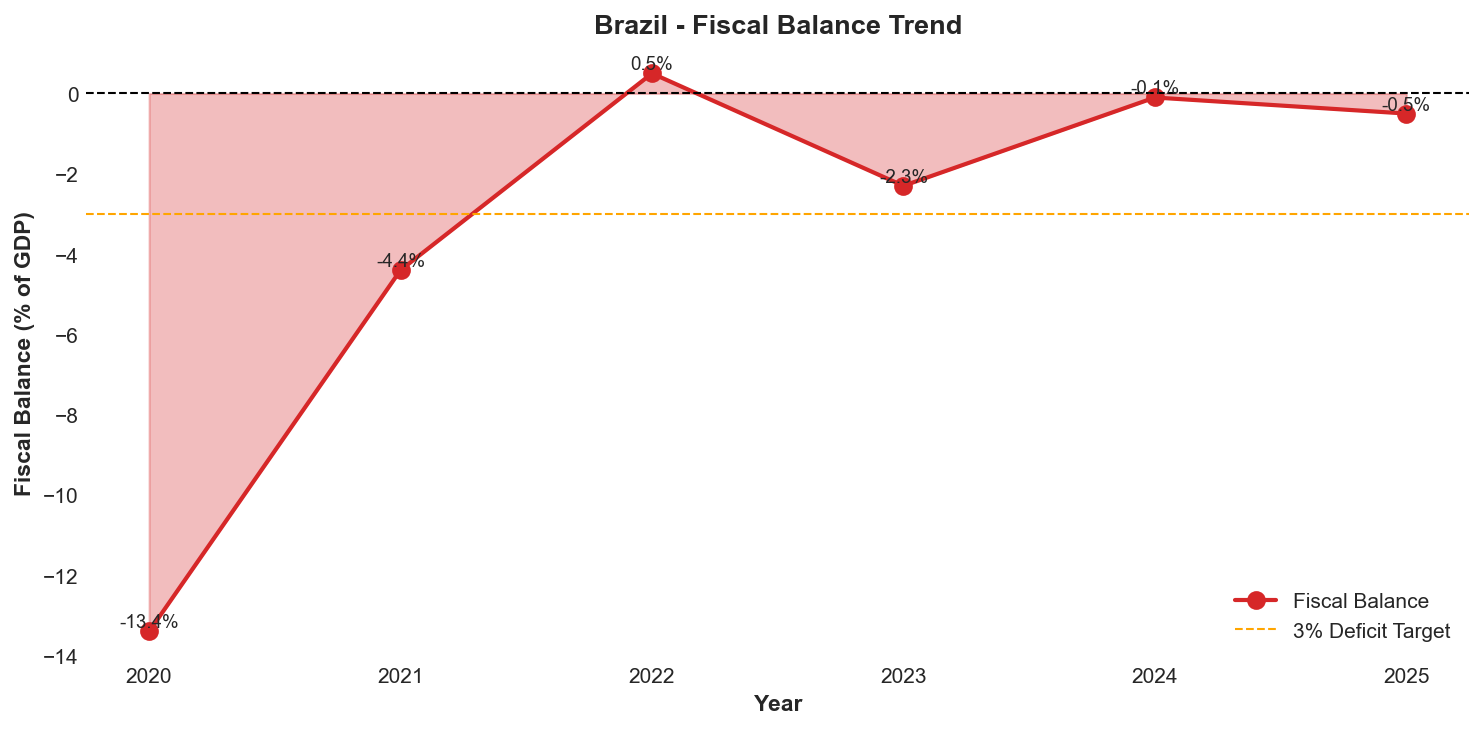

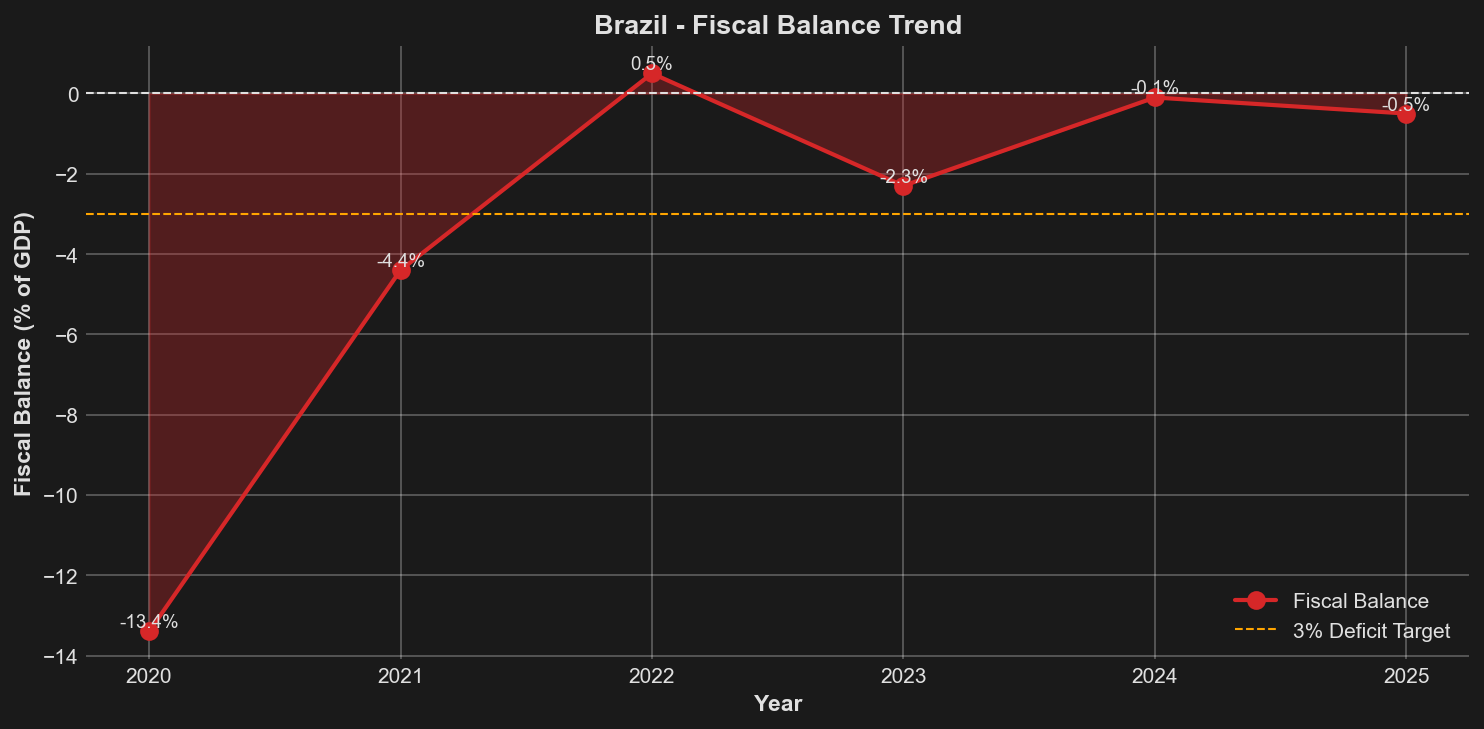

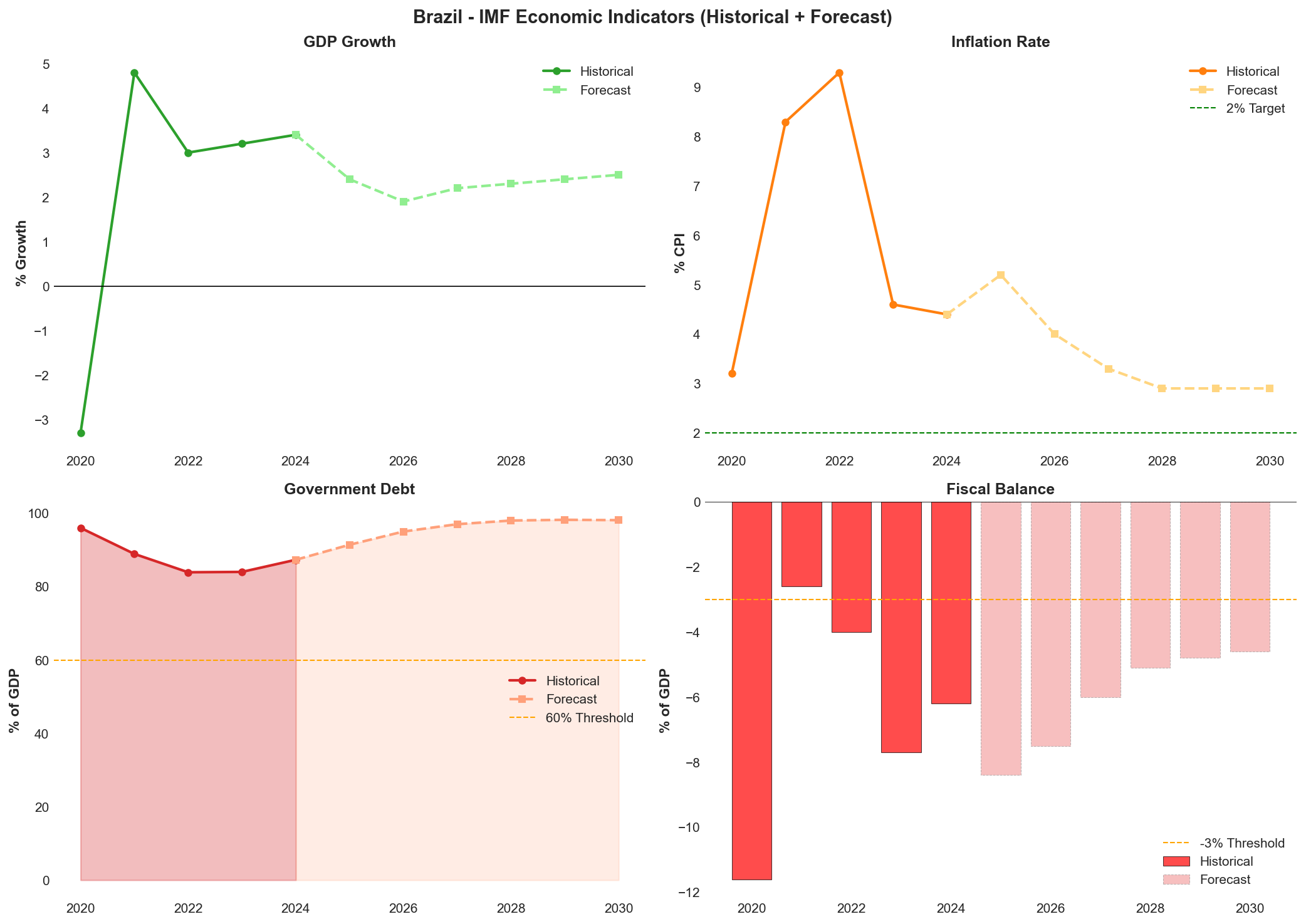

The economic trajectory through 2025 demonstrated the challenges inherent in Brazil's stabilisation efforts. Following robust 3.4% GDP growth in 2024, momentum decelerated significantly to a projected 2.2% in 2025 as aggressive monetary tightening aimed to combat inflation that breached the central bank's tolerance band, reaching 5.5% against a 3% target. The fiscal position, whilst showing improvement from pandemic-era deficits, remains constrained with public debt reversing its post-pandemic decline to reach 76.5% of GDP in 2024 and projected to climb to 77.8% in 2025. External vulnerabilities have moderated somewhat, with the current account deficit narrowing to 2.5% of GDP in 2025 from 2.8% in 2024, supported by adequate foreign exchange reserves of $335.7 billion. The imposition of 10% reciprocal tariffs by the United States in April 2025, layered atop existing steel and aluminium levies, introduces additional headwinds, though Brazil's diversified export markets and relatively balanced bilateral trade flows provide meaningful insulation compared to more concentrated emerging market peers.

Brazil's path towards investment grade status hinges critically on the government's capacity to deliver sustained fiscal consolidation whilst maintaining macroeconomic stability and advancing structural reforms. The approval of historic tax reform legislation and demonstrated policy pragmatism under the current administration provide foundational support for medium-term credit improvement. However, near-term risks remain elevated, encompassing inflation persistence requiring extended monetary tightness, potential currency pressures from global risk sentiment shifts, and domestic political fragmentation that may constrain reform implementation. Moody's positive outlook signals potential upgrade momentum should fiscal metrics continue improving and debt trajectories stabilise, yet achieving broad investment grade recognition across all agencies will require sustained improvements in fiscal discipline, institutional strength, and structural competitiveness over a multi-year horizon. The balance of risks suggests gradual credit profile improvement remains achievable, contingent upon policy continuity and successful navigation of both domestic political constraints and external economic headwinds.

Ratings Summary

Brazil maintains sub-investment grade ratings across all three major credit rating agencies as of January 2026, though with notable differentiation in positioning and outlook. Moody's Investors Service rates Brazil at Ba1 with a positive outlook, placing the sovereign just one notch below investment grade following an upgrade in October 2024 that recognised material credit improvements stemming from robust GDP growth and fiscal reforms. The positive outlook reflects expectations of gradual fiscal improvement and debt stabilisation. S&P Global Ratings maintains a BB rating with a stable outlook, having upgraded Brazil from BB- in December 2023 on the strength of landmark tax reform approval and the country's strengthened track record of pragmatic policymaking, though the agency continues to express concerns about fiscal imbalances with projected general government deficits averaging 6.2% of GDP over 2023-2026. Fitch Ratings similarly holds Brazil at BB with a stable outlook, affirmed in December 2023, acknowledging policy pragmatism under President Lula whilst citing persistent concerns about elevated government debt levels and doubts regarding the authorities' capacity to deliver meaningful fiscal consolidation. The divergence in outlooks, with Moody's signalling potential upgrade momentum whilst S&P and Fitch maintain stable perspectives, underscores the critical juncture facing Brazil's creditworthiness as fiscal consolidation efforts compete with inflation pressures and political constraints.

| Rating Agency | Current Rating | Outlook | Last Action Date |

|---|---|---|---|

| S&P Global | BB | Stable | December 19, 2023 |

| Moody's | Ba1 | Positive | October 1, 2024 |

| Fitch | BB | Stable | December 15, 2023 |

Economic Indicators

| Indicator | 2020 | 2021 | 2022 | 2023 | 2024 | 2025* | 2026* |

|---|---|---|---|---|---|---|---|

| GDP Growth (%) | -3.3 | 4.8 | 2.9 | 3.2 | 3.4 | 2.2 | 2.4 |

| Inflation Rate (%) | 4.5 | 10.1 | 12.1 | 4.6 | 4.8 | 5.5 | 3.8 |

| Debt-to-GDP Ratio (%) | 88.8 | 80.3 | 72.9 | 73.8 | 76.5 | 77.8 | 81.2 |

| Fiscal Balance (% of GDP) | -13.4 | -4.4 | 0.5 | -2.3 | -0.1 | -0.5 | -2.8 |

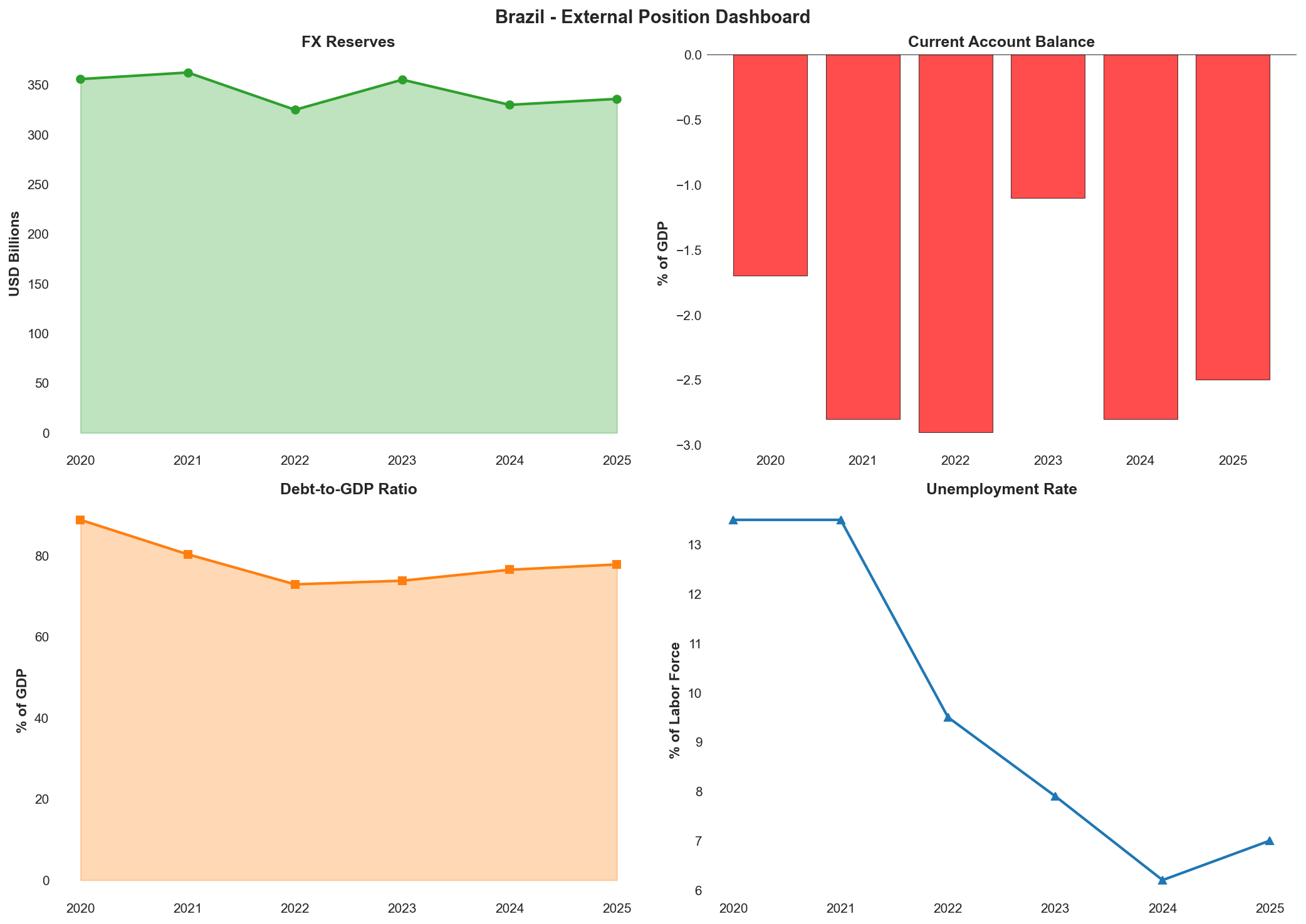

| Current Account Balance (% of GDP) | -1.7 | -2.8 | -2.9 | -1.1 | -2.8 | -2.5 | -2.9 |

| Foreign Exchange Reserves (USD bn) | 355.6 | 362.2 | 324.7 | 355.0 | 329.7 | 335.7 | 342.0 |

| Unemployment Rate (%) | 13.5 | 13.5 | 9.5 | 7.9 | 6.2 | 7.0 | 7.2 |

| Exchange Rate (BRL/USD) | 5.16 | 5.40 | 5.17 | 4.99 | 6.19 | 5.78 | 5.65 |

*Forecast/estimate

Brazil's economic trajectory demonstrates a post-pandemic recovery cycle that peaked in 2024 with GDP growth of 3.4%, representing the strongest performance since the 4.8% rebound in 2021. However, growth momentum has decelerated markedly through 2025, with expansion moderating to an estimated 2.2% as aggressive monetary tightening measures implemented to combat persistent inflationary pressures have dampened domestic demand. The growth slowdown reflects the lagged effects of the central bank's policy rate increases, which were necessitated by inflation that accelerated from 4.6% in 2023 to 4.8% in 2024 and further to 5.5% in 2025, breaching the upper bound of the central bank's tolerance band around its 3.0% target. Looking ahead to 2026, GDP growth is projected to stabilise at approximately 2.4% as monetary policy effects normalise, whilst inflation is expected to moderate towards 3.8% as tighter policy settings take effect. The IMF's medium-term projections suggest Brazil will settle into a growth trajectory of around 2.5% by 2030, reflecting structural constraints on potential output expansion.

The fiscal trajectory presents mounting challenges to Brazil's sovereign credit profile, with the debt-to-GDP ratio reversing its post-pandemic decline and resuming an upward path. After reaching a cyclical low of 72.9% in 2022, public debt has risen steadily to 76.5% in 2024 and an estimated 77.8% in 2025, driven by elevated interest costs, persistent primary deficits, and adverse debt dynamics. The fiscal balance deteriorated from a near-equilibrium position of -0.1% of GDP in 2024 to an estimated -0.5% in 2025, with projections indicating further widening to -2.8% in 2026 as fiscal consolidation efforts face political resistance and cyclical revenue pressures. The IMF's medium-term outlook projects the fiscal deficit reaching -4.6% of GDP by 2030, with government debt escalating to 98.1% of GDP, underscoring the unsustainability of current fiscal trends without meaningful structural reforms. This deteriorating fiscal outlook represents the most significant constraint on Brazil's sovereign creditworthiness and the primary obstacle to achieving investment grade status.

External sector indicators reveal a widening current account deficit that expanded from 1.1% of GDP in 2023 to 2.8% in 2024, driven by robust domestic demand that boosted import volumes alongside elevated profit and dividend remittances. The current account deficit is projected to remain elevated at approximately 2.5% of GDP in 2025 and 2.9% in 2026, though these levels remain manageable given Brazil's diversified export base and flexible exchange rate regime. Foreign exchange reserves have demonstrated resilience, recovering to USD 335.7 billion in 2025 from USD 329.7 billion in 2024, providing adequate coverage of external financing needs. However, Brazil's net foreign asset position remains weak at -45.0% of GDP as of 2023, having deteriorated from -43.0% in 2019, reflecting the country's persistent reliance on external financing and accumulation of foreign liabilities. The IMF's projection of the current account deficit reaching -49.2% of GDP by 2030 appears anomalous and likely reflects a data classification issue, though it underscores concerns about Brazil's external vulnerability trajectory.

Labour market conditions have tightened considerably through the recovery cycle, with unemployment declining from a pandemic peak of 13.5% in 2020-2021 to 6.2% in 2024, the lowest rate in the historical series. However, the economic slowdown has begun to reverse these gains, with unemployment rising to an estimated 7.0% in 2025 and projected to reach 7.2% in 2026 as growth moderates and monetary tightening constrains employment creation. The Brazilian real experienced significant volatility, depreciating sharply to BRL 6.19 per USD in 2024 before appreciating to BRL 5.78 in 2025, reflecting shifting market sentiment regarding fiscal sustainability, inflation dynamics, and external trade developments. The April 2025 imposition of 10% reciprocal tariffs by the United States administration on all Brazilian exports, supplementing existing 25% tariffs on steel and aluminium, has introduced additional uncertainty into the exchange rate outlook, though Brazil's relatively balanced bilateral trade relationship and diversified export markets have limited the immediate impact compared to other emerging market economies.

Net Foreign Assets & External Position

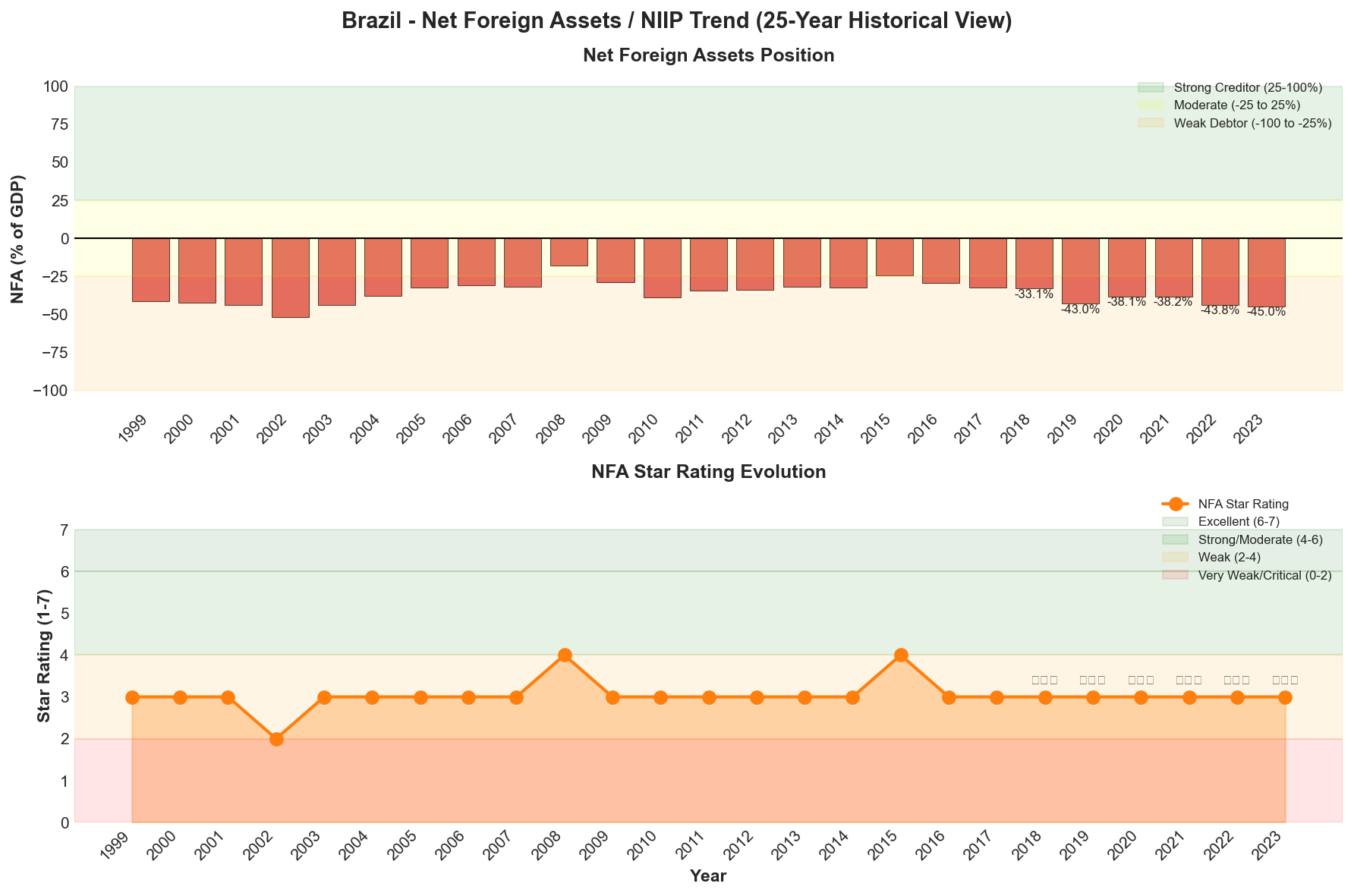

Brazil's external position reflects a persistent structural weakness characteristic of large emerging market economies with substantial foreign investment inflows and accumulated external liabilities. As of 2023, Brazil's net international investment position (NIIP) stood at -45.0% of GDP, representing a deterioration from -38.1% in 2020 and maintaining a "Weak" classification (⭐⭐⭐, 3/7 rating) according to the External Wealth of Nations database. This negative position underscores Brazil's status as a net debtor nation, though the scale remains manageable relative to the country's economic size and diversified funding sources.

The trajectory of Brazil's NIIP over the 2019-2023 period demonstrates cyclical volatility overlaying a structural debtor position. The ratio improved temporarily to -38.1% of GDP in 2020 as the pandemic-induced currency depreciation reduced the domestic currency value of external liabilities, before reverting to -43.8% in 2022 and further weakening to -45.0% in 2023. This recent deterioration reflects the combination of widening current account deficits, currency fluctuations affecting valuation effects, and continued foreign direct investment inflows that, whilst beneficial for productive capacity, mechanically increase gross external liabilities. The five-year trend indicates limited progress in strengthening the external balance sheet, with the NIIP remaining firmly within the "Weak" category throughout the period without meaningful structural improvement.

Composition and Vulnerabilities

Brazil's external liability structure provides important mitigating factors to the headline NIIP weakness. Foreign direct investment constitutes the predominant component of external liabilities, representing a stable, long-term funding source that does not create immediate rollover risks or currency mismatches. Portfolio equity investment forms another substantial component, with risks absorbed by foreign investors rather than creating sovereign obligations. External debt, whilst significant in absolute terms, remains moderate relative to GDP and benefits from Brazil's flexible exchange rate regime, which facilitates external adjustment through currency movements rather than disruptive policy interventions.

The current account deficit widened markedly to 2.8% of GDP in 2024 from 1.1% in 2023, driven by robust domestic demand stimulating import growth and deteriorating terms of trade as commodity prices moderated from earlier peaks. Projections indicate a modest improvement to 2.5% of GDP in 2025, though IMF medium-term forecasts suggest persistent external imbalances, with the current account deficit projected at an alarming 49.2% of GDP by 2030—a figure that likely reflects data inconsistencies or methodological issues requiring clarification, as such a deficit would be economically unsustainable. The more immediate concern centres on financing requirements in an environment of elevated global interest rates and potential capital flow volatility.

Reserve Adequacy and External Buffers

Brazil maintains substantial foreign exchange reserves that provide critical insurance against external shocks and capital flow reversals. Reserves stood at $335.7 billion as of May 2025, recovering from $329.7 billion in 2024 despite currency pressures and intervention requirements. This reserve level represents approximately 12% of GDP and provides coverage of roughly 18 months of imports, comfortably exceeding conventional adequacy metrics. The reserve position also covers approximately 100% of short-term external debt by remaining maturity, offering robust protection against sudden stops in capital flows.

| Indicator | 2020 | 2021 | 2022 | 2023 | 2024 | 2025* |

|---|---|---|---|---|---|---|

| Foreign Exchange Reserves (USD bn) | 355.6 | 362.2 | 324.7 | 355.0 | 329.7 | 335.7 |

| Current Account Balance (% of GDP) | -1.7 | -2.8 | -2.9 | -1.1 | -2.8 | -2.5 |

| NIIP (% of GDP) | -38.1 | -38.2 | -43.8 | -45.0 | n/a | n/a |

*Forecast/estimate

The flexible exchange rate regime serves as a primary shock absorber, with the real depreciating to 6.19 BRL/USD in 2024 from 4.99 in 2023 before partially recovering to 5.78 by May 2025. This flexibility allows relative price adjustments to support external rebalancing without depleting reserves or requiring draconian policy responses. However, exchange rate volatility creates challenges for inflation management, as pass-through effects from depreciation episodes complicate the central bank's mandate, particularly given Brazil's history of inflation sensitivity.

External Financing and Market Access

Brazil benefits from well-established market access and diversified funding sources that mitigate external vulnerability despite the weak NIIP position. The sovereign maintains regular presence in international capital markets with benchmark bond issuance across multiple currencies and maturities. Corporate and financial sector entities similarly access global funding, supported by Brazil's status as the largest economy in Latin America and its integration into global financial markets. Foreign direct investment inflows remain robust, attracted by Brazil's large domestic market, natural resource endowments, and improving business environment following structural reforms.

Nevertheless, external vulnerabilities warrant monitoring. The combination of persistent current account deficits, elevated domestic interest rates (the Selic rate reached 14.25% by mid-2025 amid inflation concerns), and potential global risk aversion creates refinancing challenges. Brazil's sub-investment grade ratings increase funding costs and limit the investor base, particularly for institutional investors with investment grade mandates. The imposition of US tariffs in April 2025, whilst manageable given Brazil's diversified export markets and relatively balanced bilateral trade, adds uncertainty to export performance and external earnings capacity.

Medium-Term External Outlook

The external position trajectory over the medium term depends critically on fiscal consolidation success, inflation control, and sustained structural reforms. Failure to achieve fiscal targets would likely perpetuate high domestic interest rates, attracting capital inflows that appreciate the currency and widen the current account deficit through competitiveness erosion—a pattern evident in Brazil's historical cycles. Conversely, successful fiscal adjustment could enable monetary easing, supporting currency stability and external rebalancing whilst reducing the interest burden on domestic debt that constrains fiscal space.

The IMF's medium-term projections, whilst requiring verification given apparent data anomalies in the 2030 current account forecast, suggest continued external financing requirements that will necessitate sustained market confidence and capital inflow maintenance. Brazil's external position, whilst weak by NIIP metrics, remains sustainable given the favourable liability composition, adequate reserves, exchange rate flexibility, and diversified economy. However, the lack of meaningful improvement in the NIIP ratio over recent years indicates that achieving investment grade status will require not only fiscal consolidation but also structural current account adjustment to demonstrate a credible path towards external balance sheet strengthening.

Credit Strengths & Vulnerabilities

Strengths

Brazil's sovereign credit profile is underpinned by several structural advantages that provide resilience against economic shocks. The country operates a large and diversified economy with GDP of $2.8 trillion, supported by a comprehensive industrial base that spans agriculture, manufacturing, and services sectors. This economic diversity reduces vulnerability to sector-specific downturns and provides multiple engines for growth.

The nation's abundant natural resources constitute a significant competitive advantage, with Brazil maintaining its position as the world's largest exporter of soybeans, coffee, and sugar, whilst also possessing substantial oil reserves that support energy security and export revenues. This resource endowment provides a stable foundation for foreign exchange earnings and fiscal revenues across commodity cycles.

Brazil's banking sector demonstrates notable resilience, characterised by adequate capitalisation with Common Equity Tier 1 ratios exceeding 13%, improving asset quality reflected in non-performing loans of 3.0%, and strong profitability metrics. This financial stability supports credit intermediation and provides a buffer against potential economic stress.

The flexible exchange rate regime serves as an effective external adjustment mechanism, allowing the currency to absorb external shocks whilst maintaining adequate foreign exchange reserves. With reserves of $335.7 billion, Brazil maintains comfortable coverage of external financing needs, providing confidence to international investors and supporting macroeconomic stability.

Vulnerabilities

Despite these strengths, Brazil faces persistent structural challenges that constrain its credit profile. The most significant vulnerability remains the elevated public debt trajectory, with debt projected to reach 79.6% of GDP by 2028. This upward path reflects the combination of primary fiscal deficits, high real interest rates, and limited fiscal space for countercyclical policy. The debt dynamics are particularly concerning given Brazil's history of fiscal slippage and the political difficulties associated with expenditure restraint.

Inflation persistence represents an ongoing challenge to macroeconomic stability. Consumer price inflation has consistently exceeded the central bank's 3% target, reaching 5.53% by April 2025 and necessitating aggressive monetary tightening. The Banco Central do Brasil has raised the Selic rate to 14.25%, with further increases anticipated, creating headwinds for economic growth and increasing debt servicing costs. This inflation persistence reflects both demand pressures from robust labour markets and supply-side constraints, whilst also raising questions about the credibility of the monetary policy framework.

Political fragmentation and governance weaknesses continue to impede policy effectiveness. President Lula's administration operates without a stable congressional majority, requiring coalition management and compromises that often dilute reform initiatives. The constitutional earmarking of revenues and mandatory spending programmes severely constrain fiscal flexibility, with approximately 93% of the budget effectively pre-committed. This rigidity limits the government's ability to respond to economic shocks or pursue strategic investments.

Currency volatility adds another layer of vulnerability, with the Brazilian real experiencing significant fluctuations that complicate monetary policy and affect inflation expectations. The exchange rate depreciated from 4.99 BRL/USD in 2023 to 6.19 in 2024, before partially recovering to 5.78 by mid-2025, reflecting both domestic policy uncertainty and global risk sentiment.

Opportunities

Brazil's medium-term credit trajectory presents several opportunities for improvement. The implementation of historic tax reform, approved in 2023 and being phased in through 2033, represents the most significant structural reform in decades. This reform simplifies Brazil's notoriously complex tax system, potentially boosting productivity, reducing compliance costs, and improving the business environment. Successful implementation could enhance growth potential and support fiscal revenues over time.

The global energy transition presents substantial opportunities for Brazil given its leadership in renewable energy and biofuels. The country already generates over 80% of electricity from renewable sources and is a global leader in ethanol production. Expanding these capabilities, alongside developing green hydrogen and sustainable aviation fuel industries, could attract significant foreign investment and create new export markets.

Nearshoring trends offer potential benefits as companies seek to diversify supply chains away from geopolitical risk zones. Brazil's large domestic market, established manufacturing base, and proximity to the United States position it to capture investment in sectors ranging from automotive to electronics, particularly if the government can improve the business environment and infrastructure.

The positive outlook from Moody's, positioning Brazil just one notch below investment grade, creates momentum for potential rating upgrades. Achieving investment grade status from multiple agencies would reduce borrowing costs, attract a broader investor base, and create a virtuous cycle of improved market access and lower debt servicing costs.

Threats

Several near-term threats could derail Brazil's credit improvement trajectory. The escalation of global trade tensions, particularly the April 2025 imposition of 10% reciprocal tariffs by the Trump administration on all Brazilian exports to the United States, adds to existing 25% tariffs on steel and aluminium. Whilst Brazil's diversified export markets and relatively balanced bilateral trade provide some insulation, further escalation could dampen growth prospects and complicate external accounts.

Domestic political risks remain elevated, with the 2026 presidential election cycle likely to intensify political polarisation and potentially undermine fiscal discipline. The temptation to pursue expansionary policies ahead of elections could derail the fiscal consolidation path, disappointing market expectations and potentially triggering rating downgrades rather than the anticipated upgrades.

Climate-related risks pose both physical and transition challenges. Brazil faces increasing frequency of extreme weather events affecting agricultural production, whilst deforestation in the Amazon attracts international scrutiny and potential trade sanctions. The European Union's proposed carbon border adjustment mechanism could affect Brazilian exports, particularly in agriculture and heavy industry.

External financing conditions could deteriorate if global monetary policy remains restrictive for longer than anticipated or if risk sentiment towards emerging markets weakens. Brazil's current account deficit of 2.5% of GDP requires continued capital inflows, making the country vulnerable to sudden stops or reversals in investor sentiment. Any combination of domestic policy missteps and external shocks could quickly erode the progress made in recent years and postpone the return to investment grade status.

Economic Analysis

Growth Dynamics and Structural Performance

Brazil's economic trajectory through 2024 demonstrated remarkable resilience, with GDP expansion reaching 3.4% and marking the strongest performance since the post-pandemic rebound of 2021. This robust growth reflected a confluence of favourable domestic dynamics, including elevated commodity prices supporting agricultural and mining sectors, strong labour market conditions with unemployment declining to 6.2%, and sustained consumer demand underpinned by real wage gains and expanded social transfers under the Lula administration. The diversified nature of Brazil's $2.8 trillion economy, encompassing comprehensive industrial capacity alongside its position as the world's leading exporter of soybeans, coffee, and sugar, provided multiple engines of growth that offset external headwinds.

However, the momentum observed in 2024 has decelerated markedly as Brazil enters 2026. Growth projections for 2025 settled at 2.2%, representing a substantial moderation driven by the lagged effects of aggressive monetary tightening, deteriorating business confidence amid fiscal uncertainties, and external pressures from global trade tensions. The imposition of 10% reciprocal tariffs by the Trump administration in April 2025, layered atop existing 25% levies on steel and aluminium, introduced additional headwinds to manufacturing and export sectors, though Brazil's relatively balanced bilateral trade relationship with the United States and diversified export markets have mitigated the impact compared to more trade-dependent emerging economies. Domestic investment activity has shown particular weakness, constrained by elevated borrowing costs and political uncertainty surrounding the government's fiscal framework.

The structural composition of Brazil's growth presents both opportunities and constraints for medium-term performance. Agricultural productivity gains and expanding energy production, particularly in pre-salt oil reserves, provide sustainable growth foundations. Nevertheless, persistent infrastructure deficits, regulatory complexity, and labour market rigidities continue to constrain potential output growth, which most analysts estimate in the range of 2.0-2.5% annually. The implementation of historic tax reform, approved in 2023 and being phased in through 2033, represents a critical structural initiative that should reduce distortions and improve the business environment over time, though near-term growth benefits remain limited as the economy adjusts to the new framework.

Inflation Dynamics and Price Stability Challenges

Brazil's inflation trajectory has proven considerably more persistent than anticipated by policymakers, presenting the central bank with its most significant challenge since the post-pandemic price surge. After declining sharply from the 12.1% peak in 2022 to 4.6% in 2023, inflation stabilised at 4.8% in 2024 before accelerating to 5.53% by April 2025, substantially exceeding the Banco Central do Brasil's 3.0% target and breaching the upper bound of the tolerance band set at 4.5%. This resurgence reflects multiple reinforcing pressures, including currency depreciation following the real's weakening to 6.19 BRL/USD in 2024, elevated food prices driven by adverse weather conditions affecting agricultural output, and persistent services inflation supported by tight labour markets and indexed wage adjustments.

The composition of inflationary pressures reveals both demand-side and supply-side origins. Core inflation measures, which exclude volatile food and energy components, have remained stubbornly elevated, indicating that price pressures extend beyond transitory factors. Services inflation, in particular, has demonstrated considerable stickiness, reflecting wage indexation mechanisms and productivity constraints that limit the economy's capacity to absorb cost increases without passing them through to final prices. The depreciation of the real, whilst providing a competitive advantage to exporters, has transmitted imported inflation through higher costs for intermediate goods and capital equipment, sectors where Brazil maintains significant import dependence.

Inflation expectations, a critical determinant of price-setting behaviour and central bank credibility, have become increasingly unanchored. Market-based measures and survey data indicate that expectations for twelve-month-ahead inflation have drifted above the central bank's target range, reflecting scepticism about the monetary authority's ability to deliver price stability whilst the fiscal authority pursues expansionary policies. This de-anchoring of expectations complicates the central bank's task, as it must tighten policy more aggressively to achieve the same disinflation impact compared to an environment where expectations remain well-anchored to target.

Monetary Policy Stance and Central Bank Response

The Banco Central do Brasil has responded to persistent inflation pressures with a pronounced tightening cycle, raising the Selic policy rate from accommodative levels to restrictive territory in an effort to re-establish price stability and restore credibility. This monetary tightening represents a significant policy shift from the easing cycle that characterised 2023, when inflation appeared to be converging towards target and growth concerns dominated the policy calculus. The central bank's forward guidance has emphasised its commitment to bringing inflation back to the 3.0% target within the relevant horizon, signalling willingness to maintain restrictive policy for an extended period despite growth headwinds.

The transmission of monetary policy to the real economy operates through multiple channels in Brazil's financial system. Higher policy rates have translated into elevated borrowing costs across consumer credit, corporate lending, and mortgage markets, dampening interest-sensitive spending categories. The resilient banking sector, characterised by adequate capitalisation with CET1 ratios above 13% and improving asset quality with non-performing loans at 3.0%, has maintained lending capacity whilst appropriately tightening credit standards in response to economic uncertainty. The exchange rate channel has provided less support than typical tightening cycles, as currency pressures from fiscal concerns and external factors have partially offset the attractiveness of higher domestic yields.

The central bank's policy effectiveness faces constraints from fiscal dominance concerns, as market participants question whether monetary tightening alone can durably control inflation whilst government spending remains elevated and debt dynamics deteriorate. This fiscal-monetary policy mix creates tensions, with restrictive monetary policy increasing debt servicing costs and potentially undermining fiscal sustainability, whilst expansionary fiscal policy works at cross-purposes to monetary tightening by sustaining aggregate demand. The central bank's operational independence, whilst legally enshrined, faces periodic political pressures that introduce uncertainty about the institution's ability to maintain its inflation-fighting stance if growth weakens substantially or unemployment rises materially.

Looking forward into 2026, the monetary policy outlook depends critically on inflation developments and fiscal policy credibility. Should inflation expectations re-anchor and actual inflation begin converging towards target, the central bank would gain scope to moderate the restrictive stance, providing relief to growth. Conversely, continued inflation persistence or further expectation deterioration would necessitate additional tightening, risking a more pronounced growth slowdown. The interaction between monetary policy, fiscal dynamics, and external conditions will remain the dominant influence on Brazil's macroeconomic performance through the forecast horizon.

Political & Institutional Assessment

Brazil's political and institutional framework presents a mixed credit picture, characterised by democratic stability and institutional resilience alongside persistent governance challenges and policy implementation constraints. President Luiz Inácio Lula da Silva's third term, which commenced in January 2023, operates within a fragmented congressional landscape that necessitates coalition management and limits the scope for transformative policy action. Whilst the administration has demonstrated pragmatic policy-making—most notably in securing passage of landmark tax reform legislation in 2023—the political environment remains marked by ideological polarisation stemming from the contentious 2022 electoral contest and ongoing tensions with former President Jair Bolsonaro's political movement.

Governance Structure and Political Dynamics

Brazil's presidential system features strong checks and balances, with an independent judiciary, autonomous central bank (granted formal independence in 2021), and bicameral legislature. However, the political system's fragmentation across more than 20 parties represented in Congress creates inherent governance challenges. President Lula governs without a stable majority, requiring continuous negotiation with centrist parties and regional interests to advance legislative priorities. This dynamic has historically led to incremental rather than comprehensive policy reforms, though it also provides political stability by preventing radical policy shifts.

The administration's relationship with Congress has been characterised by pragmatic accommodation rather than confrontation. The successful passage of constitutional tax reform in December 2023—Brazil's most significant fiscal legislation in decades—demonstrated the government's capacity to build coalitions around critical structural reforms. However, this achievement required substantial concessions and compromises that diluted some reform elements, a pattern likely to persist for future legislative initiatives.

Institutional Strength and Policy Credibility

Brazil benefits from several institutional anchors that support credit quality. The Central Bank of Brazil, under Governor Roberto Campos Neto (appointed by the previous administration and serving through December 2024) and subsequently under his successor, has maintained operational independence and credibility in monetary policy execution. The aggressive tightening cycle initiated in 2024, with the Selic rate rising from 10.75% to 14.25% by early 2025, reflects the institution's commitment to price stability despite political pressures. This independence represents a critical safeguard for macroeconomic stability.

The judiciary, whilst independent, faces challenges related to efficiency and predictability. Brazil's complex legal system and extensive appeal processes create uncertainty for economic actors, though recent efforts to streamline procedures and reduce case backlogs have shown modest progress. The Federal Court of Accounts (TCU) provides effective fiscal oversight, and anti-corruption institutions, strengthened following the "Lava Jato" investigations, continue to function despite political pressures.

Fiscal Governance and Policy Framework

Fiscal governance represents a persistent institutional weakness that directly constrains Brazil's credit profile. The constitutional expenditure ceiling, introduced in 2016 to limit real spending growth, was replaced in 2023 by a new fiscal framework that allows greater spending flexibility tied to revenue performance. Whilst this framework provides more realistic fiscal targets than the previous rigid ceiling, it also introduces risks of pro-cyclical expansion and lacks the binding constraints that would ensure debt sustainability.

The government's fiscal credibility has been tested by its struggle to meet even the relatively accommodative targets established under the new framework. The 2024 primary deficit target of 0.5% of GDP was narrowly achieved through one-off measures and revenue windfalls rather than structural adjustment. For 2025, the government targets a balanced primary budget, but market scepticism remains elevated given the administration's resistance to meaningful expenditure reforms and reliance on revenue-enhancing measures that may prove unsustainable.

Corruption and Governance Quality

Brazil continues to face significant governance challenges related to corruption, bureaucratic inefficiency, and regulatory complexity. The country ranks in the 38th percentile globally on Transparency International's Corruption Perceptions Index, reflecting persistent issues despite institutional improvements. Corruption risks are particularly acute at sub-national levels, where oversight mechanisms are weaker and political patronage networks remain entrenched.

The business environment, whilst improved from historical standards, remains constrained by regulatory complexity, lengthy bureaucratic processes, and legal uncertainty. Brazil ranks 124th out of 190 economies in the World Bank's Ease of Doing Business indicators, with particular weaknesses in contract enforcement, tax administration, and construction permitting. These structural impediments limit potential growth and reduce the efficiency of public spending, indirectly affecting fiscal sustainability.

Political Risk Outlook

Looking ahead through 2026, Brazil's political landscape is expected to remain stable but fragmented. President Lula's administration faces no immediate threats to governability, though his approval ratings have moderated from initial highs as economic challenges mount. The 2026 electoral cycle will begin to influence policy dynamics by mid-2025, potentially constraining appetite for politically difficult reforms whilst incentivising expansionary fiscal measures.

Key political risks include potential conflicts between the executive and judiciary over policy prerogatives, tensions with Congress over fiscal targets and spending priorities, and the possibility of renewed social unrest if economic conditions deteriorate significantly. However, Brazil's democratic institutions have demonstrated resilience through multiple political crises, and the probability of severe political disruption remains low. The greater concern for credit quality is not political instability but rather the political system's limited capacity to deliver the sustained fiscal consolidation and structural reforms necessary to achieve investment-grade status.

The administration's ability to maintain coalition discipline whilst advancing reforms will be critical for credit trajectory. Moody's positive outlook implicitly recognises recent improvements in policy pragmatism, but sustained progress requires overcoming entrenched political resistance to expenditure restraint and pension system adjustments—reforms that remain politically contentious across Brazil's fragmented party system.

Banking Sector & Financial Stability

Brazil's banking sector demonstrates considerable resilience and represents a fundamental pillar of credit strength within the sovereign profile. The sector maintains robust capitalisation levels, with Common Equity Tier 1 (CET1) ratios consistently exceeding 13%, providing substantial buffers against potential shocks. Asset quality has shown marked improvement, with non-performing loans declining to 3.0% of total loans, reflecting both improved underwriting standards and the benefits of strong economic performance through 2024. Profitability metrics remain strong, supported by wide interest rate spreads characteristic of the Brazilian market and diversified revenue streams across retail, corporate, and investment banking activities.

The Central Bank of Brazil has established itself as a credible and technically competent institution, demonstrating independence in monetary policy formulation and execution. The aggressive tightening cycle initiated in 2024 and continuing into 2025, with the Selic rate reaching 14.25% by May 2025, underscores the institution's commitment to price stability despite political pressures. This monetary policy credibility enhances financial stability by anchoring inflation expectations and supporting currency stability, though the elevated interest rate environment does create challenges for borrowers and fiscal dynamics.

The banking system's structure, dominated by large state-owned institutions alongside robust private sector banks, provides both stability and complexity. State banks, particularly Banco do Brasil and Caixa Econômica Federal, play significant roles in policy lending and financial inclusion whilst maintaining generally sound financial metrics. The presence of substantial foreign bank participation and a developed capital markets infrastructure further enhances system resilience and provides alternative funding channels for the economy.

Regulatory and supervisory frameworks align broadly with international standards, with the Central Bank implementing Basel III requirements and maintaining active oversight of systemic risks. The development of open banking initiatives and digital payment systems, including the highly successful Pix instant payment platform, has enhanced financial inclusion and system efficiency whilst introducing new operational and cyber risks that require ongoing supervisory attention.

Financial stability risks remain manageable but warrant monitoring. The elevated interest rate environment, whilst necessary for inflation control, increases debt servicing costs for households and corporates, potentially pressuring asset quality if sustained. The sovereign-bank nexus, characterised by significant bank holdings of government securities, creates potential feedback loops between fiscal stress and banking sector health. However, the sector's strong capital position, adequate provisioning levels, and the Central Bank's demonstrated crisis management capabilities provide confidence in the system's ability to absorb moderate shocks without systemic disruption.

Outlook & Scenarios

Short-Term Outlook (12 months)

Brazil's near-term credit trajectory through 2026 faces headwinds from persistent inflationary pressures and the lagged effects of aggressive monetary tightening. The central bank's policy rate cycle, which reached restrictive territory in response to inflation breaching the upper bound of the tolerance band at 5.53% in April 2025, will continue to weigh on economic activity throughout the year. GDP growth is expected to decelerate markedly to approximately 2.2% in 2025 from the robust 3.4% recorded in 2024, with further moderation likely in 2026 as tight monetary conditions suppress domestic demand and investment activity.

The fiscal position remains the primary constraint on creditworthiness over the coming twelve months. Whilst the headline fiscal balance showed improvement to -0.1% of GDP in 2024, structural challenges persist as elevated interest payments consume an increasing share of government revenues. The debt-to-GDP ratio is projected to continue its upward trajectory, reaching 77.8% in 2025 and potentially approaching 79% by end-2026, reflecting both the stock-flow dynamics of high real interest rates and limited scope for primary surplus generation. The government's ability to adhere to its fiscal framework, which targets a balanced primary budget by 2025, will be tested by political pressures and the economic slowdown's impact on revenue collection.

External vulnerabilities warrant close monitoring despite adequate reserve buffers. The current account deficit, which widened to 2.8% of GDP in 2024, is expected to moderate slightly to 2.5% in 2025 as import growth slows alongside domestic demand. However, the imposition of 10% reciprocal tariffs by the United States in April 2025, layered atop existing 25% levies on steel and aluminium, introduces uncertainty into export performance. Whilst Brazil's diversified export base and relatively balanced bilateral trade relationship with the US provide some insulation, prolonged global trade tensions could pressure the current account and currency stability. Foreign exchange reserves of $335.7 billion provide adequate coverage, though capital flow volatility remains a risk factor given Brazil's substantial external financing requirements.

The banking sector continues to demonstrate resilience, with capital adequacy ratios above 13% and non-performing loans stabilising at 3.0%, providing a buffer against credit quality deterioration as monetary tightening impacts borrowers. However, the transmission of higher interest rates through the economy will test asset quality, particularly in consumer and small business segments. Labour market conditions, whilst remaining relatively healthy with unemployment around 7.0%, show signs of softening as growth momentum wanes, which could further constrain household consumption and credit demand.

Medium-Term Outlook (1-3 years)

Brazil's medium-term credit profile hinges critically on the authorities' capacity to deliver credible fiscal consolidation whilst maintaining macroeconomic stability and advancing structural reforms. The trajectory of public debt represents the central challenge, with projections indicating a rise to 79.6% of GDP by 2028 under current policies. Reversing this trend requires sustained primary surpluses of 1.5-2.0% of GDP, a threshold that has proven elusive given political fragmentation and competing spending pressures. The government's fiscal framework, whilst providing an institutional anchor, faces implementation risks as expenditure rigidities limit adjustment flexibility and revenue enhancement measures encounter legislative resistance.

The successful implementation of the landmark tax reform approved in 2023 offers meaningful medium-term support to the credit profile. The transition to a value-added tax system is expected to reduce compliance costs, broaden the tax base, and improve the business environment over the 2026-2033 implementation period. However, the reform's revenue-neutral design means fiscal consolidation must come from expenditure restraint rather than tax increases, placing greater emphasis on politically challenging spending reforms. Progress on pension system adjustments, public sector wage moderation, and subsidy rationalisation will be essential to create fiscal space for debt stabilisation.

Inflation dynamics over the medium term will significantly influence monetary policy settings and, consequently, debt servicing costs and economic growth potential. The central bank's credibility and operational independence remain crucial assets, though political pressures have periodically tested institutional resilience. Achieving sustained convergence of inflation to the 3.0% target with tolerance bands of ±1.5 percentage points would enable gradual monetary easing, reducing real interest rates that currently amplify debt dynamics. Conversely, persistent inflation above target would necessitate prolonged restrictive policy, constraining growth and complicating fiscal arithmetic.

Structural competitiveness and productivity enhancements represent critical determinants of Brazil's medium-term growth potential and debt sustainability. The economy's diversified industrial base and natural resource endowments provide foundations for expansion, yet infrastructure deficiencies, regulatory complexity, and skills gaps constrain potential output growth to an estimated 2.0-2.5% annually. Advancing reforms in areas including infrastructure concessions, labour market flexibility, and business environment simplification could lift the growth trajectory, improving debt dynamics through denominator effects. The government's pragmatic policy approach, evidenced by the tax reform achievement, suggests capacity for incremental progress, though comprehensive transformation faces political economy constraints.

External sector developments will shape Brazil's financing conditions and vulnerability to global shocks. The current account deficit, whilst manageable at projected levels of 2.0-2.5% of GDP, requires continued foreign direct investment inflows averaging $70-80 billion annually to ensure sustainable financing. Brazil's integration into global value chains, particularly in agriculture, energy, and manufacturing, provides diversification benefits but also exposes the economy to trade policy shifts and commodity price volatility. The evolution of US-China trade relations and potential reshoring trends could create both opportunities and challenges for Brazilian exporters over the medium term.

Rating Scenarios

Upside Scenario (Upgrade Probability: 25-30% over 18-24 months)

An upgrade to investment grade by one or more rating agencies would likely require demonstration of sustained fiscal discipline resulting in debt stabilisation below 77% of GDP, accompanied by credible medium-term consolidation plans. Specifically, Moody's positive outlook positions Brazil closest to investment grade at Ba1, with an upgrade to Baa3 contingent upon primary surpluses consistently exceeding 1.5% of GDP, inflation convergence to target enabling monetary policy normalisation, and continued structural reform implementation. S&P and Fitch would require similar fiscal achievements alongside evidence of reduced political uncertainty and strengthened governance frameworks.

Key catalysts for positive rating action include successful adherence to the fiscal framework through 2026-2027, with the primary balance reaching surplus territory and debt-to-GDP ratio demonstrating a clear downward trajectory. Inflation returning sustainably to the 3.0% target range would enable the central bank to reduce policy rates towards neutral levels of 8-9%, alleviating debt servicing pressures and supporting growth. Meaningful progress on second-generation reforms, including administrative streamlining, further pension adjustments, and subsidy rationalisation, would signal enhanced institutional capacity and political commitment to fiscal sustainability.

External sector improvements, such as current account deficit compression to 1.5% of GDP or below through export competitiveness gains rather than import compression, would strengthen the credit profile. Additionally, resolution of global trade tensions with reduced tariff barriers and sustained foreign direct investment inflows above $80 billion annually would bolster external resilience. The banking sector maintaining robust capitalisation and asset quality through the economic cycle would provide further support, ensuring financial stability underpins the sovereign credit standing.

Baseline Scenario (Stable Ratings: 60-65% probability over 18-24 months)

The most likely scenario envisions Brazil maintaining its current sub-investment grade ratings with stable outlooks from S&P and Fitch, whilst Moody's positive outlook either converts to stable or results in an upgrade to Baa3 without triggering broader investment grade recognition. Under this scenario, fiscal consolidation proceeds gradually, with primary balances improving to 0.5-1.0% of GDP by 2027 but falling short of levels required for decisive debt stabilisation. The debt-to-GDP ratio peaks near 80% before plateauing, reflecting modest primary surpluses offset by elevated interest costs as monetary policy remains moderately restrictive.

Economic growth settles into a 2.0-2.5% annual range, supported by commodity exports and domestic consumption but constrained by infrastructure bottlenecks and productivity challenges. Inflation gradually converges towards target, averaging 4.0-4.5% through 2026-2027, enabling measured monetary easing but maintaining real interest rates in positive territory. The tax reform implementation proceeds on schedule, delivering incremental efficiency gains, though transformative impacts remain several years distant. Political fragmentation persists, limiting the scope for ambitious structural reforms whilst preventing major policy reversals.

The current account deficit stabilises around 2.0-2.5% of GDP, financed comfortably through foreign direct investment and portfolio inflows, with foreign exchange reserves maintained above $320 billion. US tariffs remain in place but do not escalate materially, with Brazilian exporters partially mitigating impacts through market diversification and exchange rate adjustment. The banking sector navigates the slower growth environment without systemic stress, though asset quality shows modest deterioration in consumer segments. This scenario reflects continuity of pragmatic policymaking without breakthrough achievements, maintaining Brazil's position as a stable sub-investment grade credit.

Downside Scenario (Downgrade Probability: 10-15% over 18-24 months)

Negative rating action would likely stem from fiscal deterioration, with the primary balance remaining in deficit territory beyond 2026 and debt-to-GDP ratio exceeding 82-85%, signalling unsustainable dynamics. Such an outcome could result from political gridlock preventing expenditure reforms, revenue shortfalls due to deeper-than-expected economic slowdown, or policy slippages undermining the fiscal framework's credibility. Moody's would likely revise its outlook to stable or negative before considering a downgrade, whilst S&P and Fitch could move outlooks to negative if fiscal metrics deteriorate materially.

Key triggers for downgrade consideration include sustained inflation above 6%, necessitating prolonged monetary tightening that suppresses growth below 1.5% annually whilst amplifying debt servicing costs. Political instability, whether from executive-legislative conflicts, corruption scandals, or social unrest, could undermine policy continuity and reform momentum. Abandonment or significant weakening of the fiscal framework would constitute a major negative signal, particularly if accompanied by central bank independence erosion threatening inflation anchoring.

External shocks pose additional downside risks, including escalation of US tariffs to 25% or higher on broader product categories, commodity price collapses reducing export revenues by 15-20%, or sudden stops in capital flows triggered by global risk aversion. A current account deficit widening beyond 3.5% of GDP without corresponding foreign direct investment increases would pressure reserves and currency stability. Banking sector stress, whether from asset quality deterioration, liquidity pressures, or contagion from external financial turbulence, could necessitate public sector support with fiscal implications. Whilst not the baseline expectation, this scenario reflects Brazil's vulnerability to policy missteps and external shocks given limited fiscal buffers and structural constraints.

Conclusion

Brazil's sovereign credit profile as of January 2026 reflects a jurisdiction at a critical juncture, balancing demonstrated economic resilience against persistent structural vulnerabilities that continue to constrain its path towards investment grade status. The sovereign maintains sub-investment grade ratings across all three major agencies, with Moody's Ba1 positive outlook positioning Brazil closest to the investment grade threshold, whilst S&P and Fitch maintain BB ratings with stable outlooks. This divergence in agency perspectives underscores both the progress achieved and the challenges that remain.

The Brazilian economy has demonstrated considerable strength through the post-pandemic period, achieving robust 3.4% growth in 2024 supported by a large and diversified economic base exceeding $2.8 trillion in GDP. The country benefits from substantial natural resource endowments, maintaining its position as the world's largest exporter of soybeans, coffee, and sugar, alongside significant petroleum reserves. The banking sector has proven resilient, with capital adequacy ratios exceeding 13% and non-performing loans contained at 3.0%, providing a stable foundation for economic activity. External buffers remain adequate, with foreign exchange reserves of $335.7 billion offering meaningful protection against external shocks, whilst the flexible exchange rate regime provides an important adjustment mechanism.

However, these strengths are counterbalanced by significant fiscal and monetary challenges that pose material risks to the credit trajectory. Public debt has resumed an upward path, reaching 76.5% of GDP in 2024 and projected to climb towards 79.6% by 2028, driven by elevated interest costs and insufficient primary surplus generation. Inflation has proven persistently above target, accelerating to 5.53% by April 2025 and necessitating aggressive monetary tightening with the Selic rate reaching 14.25%. This monetary policy stance, whilst necessary to anchor inflation expectations, has contributed to a marked deceleration in economic momentum, with growth projected at 2.2% for 2025. The current account deficit widened substantially to 2.8% of GDP in 2024, reflecting strong import demand, though this remains manageable given Brazil's diversified export base and adequate reserve coverage.

Political fragmentation and governance challenges continue to complicate policy implementation, with President Lula's administration navigating a fractured Congress that constrains the scope for decisive fiscal consolidation. Whilst the approval of landmark tax reform in 2023 demonstrated capacity for pragmatic policymaking and provided the catalyst for rating upgrades from both S&P and Moody's, doubts persist regarding the government's ability to deliver the sustained fiscal discipline necessary to stabilise and eventually reduce the debt burden. The external environment has become more challenging, with US tariff impositions in April 2025 adding uncertainty, though Brazil's relatively balanced bilateral trade relationship and diversified export markets mitigate the direct impact compared to more trade-dependent emerging markets.

The path towards investment grade status, whilst visible, remains contingent upon sustained progress across multiple dimensions. Moody's positive outlook signals potential upgrade momentum should Brazil demonstrate continued fiscal improvement and debt stabilisation, maintain inflation within target ranges through credible monetary policy, and advance structural reforms that enhance productivity and institutional strength. However, achieving broad investment grade recognition across all three major agencies will require a multi-year track record of fiscal consolidation, with primary surpluses sufficient to place debt on a declining trajectory, alongside evidence of durable political commitment to reform despite electoral cycles and coalition pressures.

In the near term, risks remain elevated. Inflation persistence could necessitate prolonged monetary tightness, further dampening growth and complicating debt dynamics. Currency pressures, whilst moderated from 2024 peaks, remain sensitive to shifts in global risk sentiment and domestic policy credibility. Global trade tensions and commodity price volatility present external headwinds that could test Brazil's economic resilience. Nevertheless, the sovereign's large economy, diversified production base, and demonstrated policy pragmatism provide meaningful buffers against adverse scenarios.

Brazil's sovereign credit profile ultimately reflects a jurisdiction with substantial economic potential constrained by fiscal imbalances and governance challenges that have proven resistant to resolution. The positive rating momentum achieved through 2023-2024 demonstrates that progress is possible when political will aligns with pragmatic policymaking. Sustaining this trajectory will require continued discipline in fiscal management, credible inflation control, and advancement of structural reforms that address long-standing productivity constraints. Whilst the journey towards investment grade remains challenging, Brazil possesses the fundamental economic strengths necessary to achieve this objective should policymakers maintain reform momentum over the medium term.